Please see below for Brooks MacDonald’s Daily Investment Bulletin, received by us late yesterday 21/10/2021:

What has happened

US and European equities continued their recent run of positive days with a small gain in the US leaving the index only a fraction away from its all-time high set in September. US earnings were, again, the driver of this upswing with around two-thirds of companies reporting yesterday beating expectations.

COVID-19

With the recent pickup in cases, headlines filtered through yesterday from across the globe. In Russia, President Putin has mandated a ‘non-working’ firebreak between the 31st October and 7th November whilst the Czech Republic has mandated the wearing of masks in indoor spaces. In New York City, municipal workers will need to show proof of vaccination to continue in their roles with the option of showing a negative test no longer available. Global governments appear to be taking one of two paths as cases increase in the northern hemisphere, either enacting restrictions now or doubling down on their vaccination/booster strategy. In the UK, weekly average cases have now risen to 45k per day with the Health Secretary yesterday urging citizens to register for vaccinations and for booster jabs ahead of the winter period.

Inflationary pressures

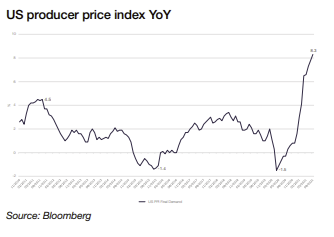

Whilst equities recorded another strong day yesterday, sovereign bonds remained under siege due to inflationary concerns. Oil prices hit another high for the year after reports from the US EIA pointed to falling inventories of both crude oil and gasoline. US 10 year inflation breakevens are now sitting at 2.6%, their highest level since 2012. Fed Speakers have been keen to push back against market expectations for interest rates, which are now running far ahead of the latest Fed dot plot from September. Fed Governor Quarles said yesterday that whilst he sees ‘significant upside risks’ to inflation, that his base case sees US inflation heading towards 2% next year. Quarles also addressed the elephant in the central bank room, saying that a demand/supply imbalance is not best addressed by curtailing demand via tighter monetary policy, describing such an approach as ‘premature’.

What does Brooks Macdonald think The market has fully priced in one rate hike in the US in 2022 with a second hike three-quarters priced in. The first step on the Fed’s monetary normalisation process will be the tapering of pandemic quantitative easing programmes so this will buy some time for the Fed to settle on the exact timing and pace of rate hikers, in the interim the Fed wants to avoid the market pricing in too rapid a tightening.

Please continue to utilise these blogs and expert insights to keep your own holistic view of the market up to date.

Keep safe and well

Paul Green DipFA

22/10/2021