Please see below for one of AJ Bell’s latest articles received by us yesterday 10/10/2021, looking at the importance of the US Dollar to Global Markets:

The International Monetary Fund’s quarterly Composition of Official Foreign Exchange Reserves report may not be everyone’s idea of bedtime reading but one trend immediately emerges from the latest data. The dollar is still – slowly – falling from favour as the globe’s reserve currency with non-US central banks.

As of June 2021, the dollar represented 59% of global exchange reserves, only a fraction above December’s 25-year low and way down from this century’s 73% peak, reached in 2001.

The creation of the euro may have something to do with this and the rise of the Chinese renminbi may be another, while the US may not have helped its cause with rampant deficit creation and money printing since 2009 (even if it is not on its own in either respect).

This has perhaps tempted some central banks to sell dollars in exchange for something else (gold or other currencies), because the greenback trades well below its early-century highs, as measured by the trade-weighted DXY index. The so-called ‘Dixie’ benchmark currently stands at 94 compare to its 2002 peak (for this century) of 120.2.

This may feed into the ‘demise of the dollar’ narrative that is popular with some economists and investors (even if that neglects the lack of credible alternatives, especially as the Chinese renminbi still represents just 2.6% of global foreign reserves). Yet for all of that, the DXY index trades at its highest mark for 2021 and all market participants, not just currency traders, will know that attention must be paid when the US currency starts to make a move, up or down.

Dollar dynamic

Two asset classes are particular sensitive to the dollar, at least if history is any guide.

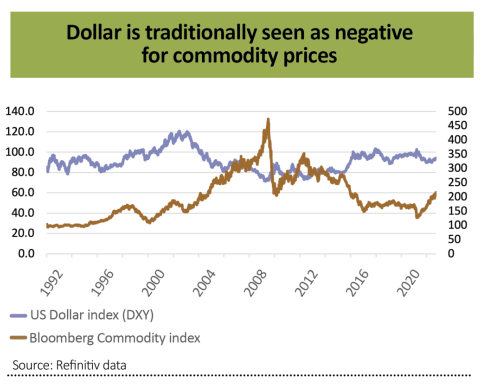

The first is commodities. All major raw materials, except cocoa (which is traded in sterling) are priced in dollars. If the US currency rises then that makes them more expensive to buy for those nations whose currency is not the dollar or is not pegged to it and that can dampen demand, or so the theory goes.

While the past is by no means a guarantee for the future, it can be argued that there is an inverse relationship between ‘Dixie’ and the Bloomberg Commodity Price index.

The second is emerging equity markets. They do not appear to welcome a strong dollar either, judging by the inverse relationship which seems to exist between the DXY and MSCI Emerging Markets benchmarks. Dollar strength at the very least coincided with major swoons in EM, or at least periods of marked underperformance relative to developed markets, during 1995-2000 and 2012-15. Retreats in the greenback, by contrast, appeared to give impetus to emerging equity arenas in 2003-07, 2009-12 and 2017-18.

This also makes sense, in that many emerging (and frontier) nations borrow in dollars and weakness in their currency relative to the American one makes it more expensive to pay the coupons and eventually repay the original loans.

Sovereign defaults are thankfully few and far between in 2021 – Suriname and Belize are the only ones that spring to mind – but a rising dollar could put more pressure on potential strugglers whose credit ratings continue to slip, notably Tunisia.

Bouncy buck

But before investors jump on the dollar bandwagon – and to conclusions – it must be worth asking why the US currency is back on a roll, and there are a couple of possibilities here.

The first is risk aversion. It may seem strange to say this as so many equity markets trade at or near all-time highs and so many sub-classes of the bond market offer record-low yields, but it may not be entirely a coincidence that the S&P 500 index has just served up its weakest month since the outbreak of the pandemic.

China’s regulatory crackdown, and signs of an accompanying economic slowdown, may be tempting some investors to seek out a haven asset and the dollar, as the globe’s reserve currency, still fits that bill.

The good news here is that the DXY index is nowhere its all-time high of 160 in the mid-1980s (a situation that was only resolved by 1985’s Plaza Accord, when the G5 unilaterally revalued the deutschmark, as they were then, against the US currency), let alone that 120 peak of 2002, but substantial further dollar gains could be a warning of a market dislocation of some kind.

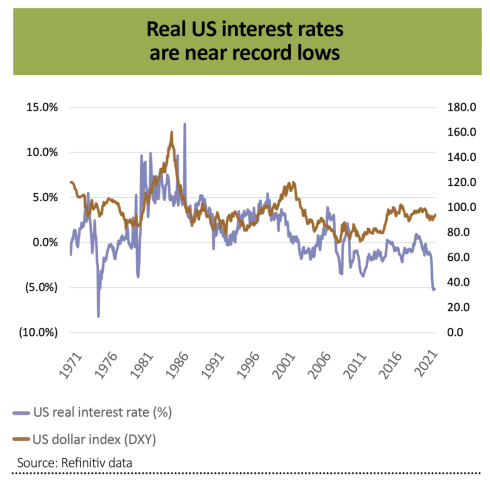

The second is US monetary policy. Whether you believe it or not, the US Federal Reserve is again discussing the prospect of tapering quantitative easing and raising interest rates in either 2022 or 2023.

Real US interest rates, adjusting for inflation, are as deeply in negative territory now as they have been for 50 years, thanks to record-low interest rates and a 5.2% inflation reading. History suggests a move upward, either due to lower inflation, higher borrowing costs or both, could boost the buck.

Yet the sensitivity of the emerging markets and commodity prices to sharp moves in the dollar suggests the Fed will have to move carefully, as the US central bank will not wish to cause – or be blamed – for the sort of upset which is now known as 2013’s taper tantrum. If monetary policy does become less loose, it seems sensible to expect higher volatility at the very least.

Please continue to utilise these blogs and expert insights to keep your own holistic view of the market up to date.

Keep safe and well

Paul Green DipFA

11/10/2021