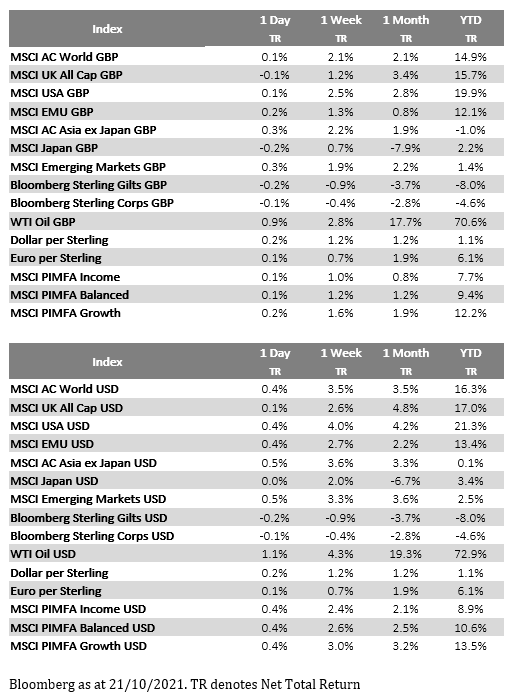

Please see below for Brooks MacDonald’s Daily Investment Bulletin, received by us late yesterday 21/10/2021:

What has happened

US and European equities continued their recent run of positive days with a small gain in the US leaving the index only a fraction away from its all-time high set in September. US earnings were, again, the driver of this upswing with around two-thirds of companies reporting yesterday beating expectations.

COVID-19

With the recent pickup in cases, headlines filtered through yesterday from across the globe. In Russia, President Putin has mandated a ‘non-working’ firebreak between the 31st October and 7th November whilst the Czech Republic has mandated the wearing of masks in indoor spaces. In New York City, municipal workers will need to show proof of vaccination to continue in their roles with the option of showing a negative test no longer available. Global governments appear to be taking one of two paths as cases increase in the northern hemisphere, either enacting restrictions now or doubling down on their vaccination/booster strategy. In the UK, weekly average cases have now risen to 45k per day with the Health Secretary yesterday urging citizens to register for vaccinations and for booster jabs ahead of the winter period.

Inflationary pressures

Whilst equities recorded another strong day yesterday, sovereign bonds remained under siege due to inflationary concerns. Oil prices hit another high for the year after reports from the US EIA pointed to falling inventories of both crude oil and gasoline. US 10 year inflation breakevens are now sitting at 2.6%, their highest level since 2012. Fed Speakers have been keen to push back against market expectations for interest rates, which are now running far ahead of the latest Fed dot plot from September. Fed Governor Quarles said yesterday that whilst he sees ‘significant upside risks’ to inflation, that his base case sees US inflation heading towards 2% next year. Quarles also addressed the elephant in the central bank room, saying that a demand/supply imbalance is not best addressed by curtailing demand via tighter monetary policy, describing such an approach as ‘premature’.

What does Brooks Macdonald think The market has fully priced in one rate hike in the US in 2022 with a second hike three-quarters priced in. The first step on the Fed’s monetary normalisation process will be the tapering of pandemic quantitative easing programmes so this will buy some time for the Fed to settle on the exact timing and pace of rate hikers, in the interim the Fed wants to avoid the market pricing in too rapid a tightening.

Please continue to utilise these blogs and expert insights to keep your own holistic view of the market up to date.

Please see below for Brooks MacDonald’s Daily Investment Bulletin received by us yesterday 19/08/2021:

What has happened

Markets spent much of Wednesday in a holding pattern ahead of the release of the Fed July meeting minutes. That changed when the minutes came out, as they showed that most officials looked to be favour of starting to taper bond purchases by the end of 2021. As a result, expectations around Fed Chair Powell’s speech next week at Jackson Hole will have gone up a notch or two, as investors await fresh clues on what a potential strategy for tapering might look like. After the release, US 10-year Treasury yields gave up the day’s gains of around 3bps to finish broadly flat at around 1.26%, but in early trade this morning, have traded lower, below 1.25%. US equities, already small down on the day, moved lower after the report was published, with cyclical and growth sectors falling in broadly equal measure. Overnight Asian markets are following Wall Street’s lead, trading lower this morning. Separately, Wednesday also saw the latest UK Consumer Price Index (CPI) data for July, which came in at 2% year on year, below June’s 2.5%, and below expectations of 2.3%. However, such is the ongoing distortion from base effects and reopening imbalances that neither the ‘transitory’ nor ‘sustained’ inflation camp was able to claim the advantage.

Fed releases its July meeting minutes

The release of Fed meeting minutes doesn’t normally get this much attention, but such is the focus around when the US Fed might look to start tapering its asset purchase programme. Regarding the subject of the taper, the minutes showed that ‘most participants noted that, provided that the economy were to evolve broadly as they anticipated, they judged that it could be appropriate to start reducing the pace of asset purchases this year.’ The committee also discussed the method by which to taper asset purchases, with most participants wanting to taper purchases of Treasury securities and Mortgage Backed Securities ‘proportionally in order to end both sets of purchases at the same time.’ Finally, the minutes showed members wanted to emphasise the decisions between tapering and rate hiking would be separate and not dependent on each other, saying that ‘participants indicated that the standards for raising the target range for the federal funds rate were distinct from those associated with tapering asset purchases’. This last point seemed to fit with comments earlier in the day on Wednesday from St Louis Fed President Bullard, who said that he preferred that tapering were finished by Q1 2022, and that Q4 2022 was a ‘logical place’ for interest rate hikes to commence.

US health officials announce plan for widescale COVID vaccine booster shots

US health officials including Dr Fauci, Biden’s Chief Medical Advisor, came out with a joint statement on Wednesday, saying that subject to final FDA (Food and Drug Administration) and CDC (Centers for Disease Control and Prevention) approvals, the US would recommend booster shots to all Americans who had received the Pfizer or Moderna vaccines. The outlined plan on Wednesday suggested an booster dose should follow eight months after the second dose, and that the booster doses could begin during the week of 20th September. The drive to offer booster shots has come because of the rise in delta variant cases, as well as signs that the vaccines’ effectiveness is falling over time. According to CDC Director Walensky on Wednesday, ‘our plan is to protect the American people, to stay ahead of this virus’. As for those who had received the single-dose Johnson & Johnson (J&J) vaccine, health officials suggested they might also need booster shots, but that they were awaiting more data, principally because the J&J vaccine rollout had started much later than the other vaccines.

What does Brooks Macdonald think

Vaccines remain the ultimate game-changer in the fight against the pandemic. With concerns of falling protection over time, booster shots have been expected, but the fact that the US has formalised a widescale plan around this should be positive for markets. The flip-side is that for every Pfizer or Moderna vaccine given as a booster, it is potentially one-less shot available for those in poorer economies who have yet to get their first or second shots. Reiterating this point, the WHO (World Health Organization) on Wednesday objected to the US plan on the grounds that it could exacerbate vaccine-inequality especially for relatively poorer countries globally. If that assessment is right, then it probably lengthens the odds of seeing a synchronised economic recovery globally.

Please continue to utilise these blogs and expert insights to keep your own holistic view of the market up to date.

Please see below for Legal & General’s latest Asset Allocation Team Key Beliefs Article, received by us yesterday afternoon 19/07/2021:

Bearish sentiments

This week, we look at investor sentiment, Peru, and China – can you guess the obvious link between them?

Bulls and bears

The latest AAII Bull/Bear spread, which is based on a survey of investors’ outlooks, has started to drift lower again. The number of bullish investors has now declined to a year-to-date low.

Overall, there are still more bulls out there than bears, but the dampening of excessively positive sentiment can be seen in other indicators too. For us, this is a positive, as it reduces the risk that frothy sentiment quickly unwinds, prompting investors to pull positions and cause a market slump of their own creation.

Yet the overall bullish tone does still remain. Yields are low, policy conditions are generally supportive, and inflation – although high – is not seen as problematic. The vaccine story is also generally good, although we are aware of the risks.

In our own scenario analysis, the conclusions look similar – and that in itself acts as a red flag. Both our most likely scenario of a healthy recovery and the weighted average scenario in our analysis suggest above-trend growth and modestly above-target inflation ahead.

Given the positive sentiment, we think that is pretty well priced by markets too, so return expectations shouldn’t be too lavish from here if that scenario plays out. The upside is a ‘Roaring 20s’ type recovery; the downside is a COVID-19 variant or vaccine failure inducing a deflationary slump or rapid cycle compression, although neither attracts a particularly high probability in our view.

It’s fine to be in the crowd for a while – indeed, some of us may look forward to being in actual crowds again – but as investors we don’t want to stay there for too long. Consensus thinking can be dangerous.

Change at Paddington’s home

There is a new Paddington Bear movie in the pipeline, a Paddington exhibition at the British Library has opened, and Gareth Southgate’s management style has been juxtaposed against Paddington Bear.

Our reason for bringing him up, though, is his origins in “deepest darkest Peru”. Our economist Erik has had his spectacles on to look at Peru and other Latin American economies recently.

Peru now has a decidedly leftist government, but we believe it is a country with enviable fundamentals and China-like growth rates. In the run up to the recent elections, the currency sold off in anticipation of a hard-left candidate winning the vote.

Pedro Castillo did indeed win the presidency, and has vowed to overhaul the country’s economic model. But while his party is socialist, Castillo has drawn up more neutral policies since his victory, including central-bank independence and not nationalising the mining sector.

While we are wary of Castillo and will continue to monitor his policies and cabinet appointments closely, our view is that he may not be as negative for the country as the media are making out. With strong economic fundamentals, the risk event of the election behind us, and attractive valuations after the recent selloff, we have moved in on the currency, looking for negative sentiment to moderate.

Panda pop

This month has brought news that giant pandas are no longer endangered in the wild, according to China. The species is native to South Central China and, thanks to conservation areas, its outlook has been improving. Our view is that the Chinese economy is on a good footing too.

Much of the economic data looks solid and second-quarter growth came in stronger than expected. This made us a little surprised to see a cut in the reserve requirement ratio (RRR), one of the tools used to manage the economy, last week.

GDP is broadly back to its pre-pandemic trend, so if anything is responsible for the RRR cut it could be that growth remains a little unbalanced, with retail sales remaining depressed.

We added Chinese bonds to a number of portfolios in the early parts of the year as we believe the highly rated securities still offer an attractive yield and can play a role as an interesting diversifier in our portfolios. We still think that holds. The downside risk of a vaccine failure causing an economic slump in the country also makes us think these bonds could help should a bear market prevail.

Please continue to utilise these blogs and expert insights to keep your own holistic view of the market up to date.

Please see below for Brewin Dolphin’s latest markets in a minute article, received by us yesterday evening 27/04/2021:

Most major stock markets declined last week on fears that rising Covid-19 infections could hinder economic recovery.

With Europe firmly in the grip of the so-called ‘third wave’, the pan-European STOXX 600 ended the week down 0.8%, while Germany’s Dax fell 1.2% and France’s CAC 40 declined 0.5%. The UK’s FTSE 100 slid 1.2%, with positive economic data failing to lift investors’ spirits.

Rising infections also weighed on Japan’s Nikkei, which dropped 2.2% after the country reported nationwide daily infections of more than 5,000 for the first time in three months. This led to another state of emergency being declared in several prefectures.

US stock markets posted small declines last week after President Joe Biden announced proposals to nearly double taxes on capital gains for those earning more than $1m a year. In contrast, Chinese stock markets posted solid gains following strong inflows from Hong Kong via the Stock Connect trading programme.

Last week’s markets performance*

FTSE 100: -1.2%

S&P 500: -0.1%

Dow: -0.5%

Nasdaq: -0.3%

Dax: -1.2%

Hang Seng: +0.4%

Shanghai Composite: +1.4%

Nikkei: -2.2%

* Data from close on Friday 16 April to close of business on Friday 23 April.

European stocks gain on travel plans

UK and European stocks rose on Monday after European Commission president Ursula von der Leyen told the New York Times that inoculated Americans will be able to visit the EU in the summer. The STOXX 600 added 0.3% and the FTSE rose 0.4%, with shares in easyJet, Ryanair and TUI all posting strong gains.

In the US, the Dow slipped 0.2% whereas the S&P 500 and the Nasdaq rose 0.2% and 0.9%, respectively. Tesla started a busy week of corporate earnings statements, reporting a 74% surge in quarterly revenues. Apple, Microsoft, Amazon, Alphabet, Boeing and Ford are all due to release first quarter results this week.

HSBC and BP were in focus at the start of trading on Tuesday, with the former posting a 79% rise in first quarter pre-tax profit, and the latter receiving an earnings bump from higher oil prices and a surge in revenue from natural gas trading. The FTSE 100 opened flat ahead of the US Federal Reserve’s two-day policy meeting.

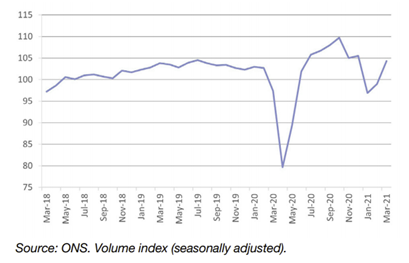

UK economy shows signs of rebound

Last week saw the release of several pieces of economic data that suggest the UK economy is starting to rebound from the Covid-19 crisis. Friday’s IHS Markit/CIPS flash composite PMI showed a strong revival in private sector output following the downturn seen at the start of 2021. The index rose to 60.0 in April from 56.4 in March – the strongest overall rise in private sector output since November 2013.

For the first time since the pandemic began, service activity growth outperformed manufacturing production growth. The service sub-index rose from 56.3 to 60.1, marking the fastest pace of expansion for more than sixand-a-half years. The manufacturing sub-index increased from 58.9 to 60.7, the highest since July 1994.

Separate data from the Office for National Statistics (ONS) showed UK retail sales volumes continued to recover in March, increasing by 5.4% from the previous month. This reflected the easing of Covid-19 restrictions on consumer spending. Sales were 1.6% higher than in February 2020 – the month before the pandemic struck.

UK retail sales surge 5.4% in March

Non-food stores provided the largest positive contribution to the monthly growth, with increases of 17.5% and 13.4% in clothing stores and other non-food stores, respectively. Fuel retailers reported monthly growth of 11.1%.

However, the ONS said retail sales for the quarter were subdued overall. In the three months to March, sales fell by 5.8% when compared with the previous three months because of tighter lockdown restrictions.

US economy moving to post-pandemic state

Last week’s flurry of US corporate earnings reports suggest the economy is starting to transition to life after the pandemic. Most notably, Netflix announced it had added just under four million subscribers in the first quarter – missing its forecast of six million. The company said it expected one million paid net additions for the second quarter – versus ten million in the second quarter of 2020, when it benefitted from a surge in demand at the beginning of the crisis.

Elsewhere, figures showed US weekly jobless claims fell to their lowest level since the onset of the pandemic, declining by 39,000 to 547,000 in the week ending 17 April. This was far better than the 617,000 figure. forecast by analysts.

US existing home sales declined by 3.7% between February and March to a seven-month low, largely because of the acute shortage of houses on the market. Compared with a year ago, when home sales first started to fall when the pandemic hit, sales were 12.3% higher. Limited supply and strong demand pushed the median existing home sales price by a record-breaking annual pace of 17.2% to an historic high of $329,100, the National Association of Realtors said.

Eurozone manufacturing enjoys record boom

Over in the eurozone, business activity in April experienced its fastest rate of increase since July 2020, thanks to record expansion in manufacturing output and a return to growth in the service sector. The composite PMI rose from 53.2 in March to 53.7 in April, according to IHS Markit’s preliminary ‘flash’ reading, which is based on around 85% of final responses to the survey.

Manufacturing output grew for a tenth straight month, expanding at a rate unsurpassed in more than two decades of survey history. The service sector continued to lag because of Covid-19 restrictions in many member states, but still reported the first expansion of activity since August 2020, rising from 49.6 in March to 50.3 in April.

Please continue to utilise these blogs and expert insights to keep your own holistic view of the market up to date.

Please see below for one of AJ Bell’s latest investment articles, received by us yesterday 18/04/2021:

As the UK starts to emerge from its latest (and hopefully final) lockdown, the FTSE 100 already trades above the levels reached just before the pandemic first made its presence felt in China and Southern Europe in early 2020.

There can be no finer example of how financial markets are forward-looking, discounting mechanisms which seek to price in future events before they happen. Yet they are not right all the time. No-one, but no-one, owns a crystal ball (or at least one that works) and if markets really were that prescient, then there would never be major sell-offs or upward surges, as no-one would ever be surprised by anything.

What the advisers and clients must therefore do, in order, is assess the facts as they are known, determine the current consensus about what will happen and – by looking at valuation – decide whether the risks are to the upside or downside. Therefore, they must look at the broad range of possibilities concerning what may happen, what could be the biggest surprises and their potential impact so they can decide whether the potential upside rewards outweigh the downside risks over their preferred time horizon.

In sum, the best fund managers are not necromancers or chancers trying to guess the future. They are experts at judging probabilities and act according to the cold maths of valuation, be that measured by earnings, cash flow or yield. It may not take much good news to boost a market that has fallen sharply to price in negative events (it may even just take the absence of fresh bad news), while it may not take much bad news to jolt a market if it has made big gains.

The FTSE 100 bottomed in late March 2020 at 4,994, long before the worst news about the pandemic and its toll on lives and the economy became known. After a near-40% gain in the UK’s headline index over the past year, advisers and clients must once more assess the balance of probabilities so they can decide whether the index has further to run or not and a good place to start is earnings forecasts.

New highs

At face value, it does seem odd that the FTSE 100 is trading above its pre-pandemic levels, even if the number of daily new COVID-19 cases is back to where it was last March and last September, and the vaccination programme continues apace. The economic outlook is still uncertain: the effects upon the behaviour of corporations and consumers alike are yet to reveal themselves and other parts of the globe are less advanced in their race to inoculate their populations.

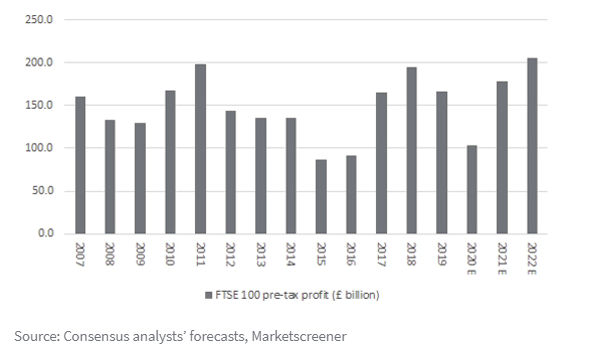

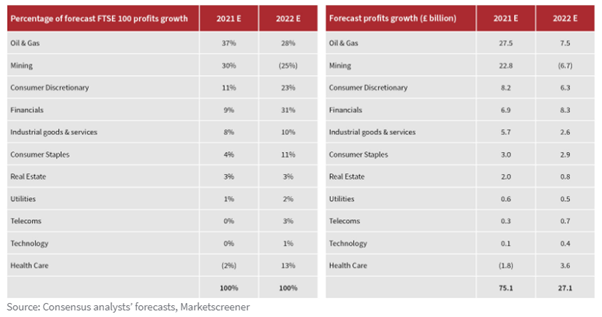

But it does make sense if you think that the consensus earnings forecasts for the FTSE 100 are going to be accurate. An aggregate of the estimates made for each member of the index suggests that the FTSE 100’s total pre-tax profit will be £178 billion in 2021 and £205 billion in 2022.

FTSE 100 is forecast to make record pre-tax profit in 2022

Those figures exceed the £166 billion made in 2019, before the pandemic hit home. Moreover, if the 2022 forecast is attained, then that would represent a new all-time high for annual earnings, surpassing the £199 billion made in 2011.

In this context, it is not too hard to see why the FTSE 100 is trading where it is, or even make a case for further gains, since the index trades below its May 2018 zenith of 7,779 even though record profits are expected for 2022.

Advisers and clients must therefore decide whether the forecasts are reliable, too optimistic or too pessimistic and what must happen for analysts to be off-beam (which they usually are, owing to the absence of that crystal ball).

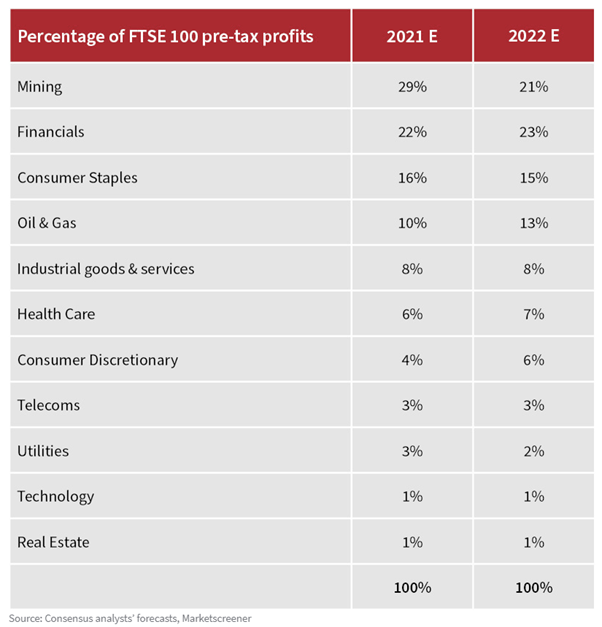

Heavy metal

To do this, advisers and clients need to parse the FTSE 100’s earnings mix. Roughly 60% of forecast profits come from just three sectors: mining (now the single biggest earner), financials, and oil and gas.

Just three sectors are expected to generate around 60% of FTSE 100 earnings in 2021 and 2022

In some ways, this makes it easy for advisers and clients to judge the upside and downside potential: in crude terms, the stronger the economic recovery the better, so far as the FTSE 100 is concerned as the index’s key industries offer huge gearing into GDP growth. The opposite also applies. A weak recovery (or heaven forbid an unexpected double-dip) would be potentially a nasty surprise.

A breakdown of forecast earnings growth makes this picture clearer still. Analysts think that the FTSE 100’s aggregate pre-tax profit will rise by £75.1 billion this year and by a further £27.1 billion in 2022. Miners and oils are expected to generate two thirds of that between them in 2021. Oils, consumer discretionary and financials are forecast to provide four fifths of the expected profit uplift in 2022.

Just three sectors are expected to generate more than 75% of forecast earnings growth in 2021 and 2022

Rising commodity prices and steepening yield curves would therefore be a good sign; falling and flattening ones would not. Those advisers and clients who buy into the narrative that inflation is coming, after being largely dormant for 40 years, will therefore feel right at home in the UK. Those who still fear debt-ridden deflation may be tempted to steer clear and seek their fortunes elsewhere.

Please continue to utilise these blogs and expert insights to keep your own holistic view of the market up to date.

Please see below for one of the latest Invesco Insight articles written by Kristina Hooper, Chief Global Market Strategist at Invesco Ltd. This article was received by us today 07/04/2021:

A month ago, I wrote about the great progress Israel was making in terms of inoculating its citizens against COVID-19. At the time, I said that we would want to follow economic data in Israel closely for indications of what the US and UK could expect in the near future — as they are making swift progress in vaccinating their respective populations — as well as what any country can expect once it successfully vaccinates a significant portion of its population. Therefore, I think it’s worth re-visiting Israel to see the impact that widespread immunization has had on its economy. It’s clear that Israel’s vaccination program is not only having a substantial impact on consumer confidence, but also on spending.

Israel’s data shows the impact of vaccines

While vaccinations only began in December, they ramped up quickly. As of April 4, Israel has given at least one dose of a COVID-19 vaccine to 59% of its population, with 54% fully vaccinated.1 The economic impact was seen relatively early on. As morbidity moderated, restrictions eased and the third lockdown was rolled back — and the Bank of Israel’s Composite State of the Economy Index for February increased by 0.4%.2

Mobility, which we have found to be a helpful indicator of economic activity, has increased substantially. By the end of March 2021, retail and recreation mobility (restaurants, cafes, shopping centers, movie theaters, etc.) was off by only 6% from January 2020 levels, while grocery and pharmacy mobility is actually higher than those early 2020 levels.3 And, not surprisingly, economic activity accelerated in March. Daily credit card data shows that the value of transactions for the week ending March 22 was actually 15% higher than it was in January 2020.4 By comparison, back in April 2020, the value of transactions was more than 40% below its level in January of 2020.4 The rebound in spending has been strongest in some of the areas hardest hit by the pandemic, especially leisure and tourism.

Why is this time different?

What makes this time different than past economic re-openings, like we saw in spring 2020? Before broad vaccinations, the re-opening of an economy was a double-edged sword. Typically, a re-opening would often be followed, after a lag, with an increase in COVID-19 infections. In addition, the increase in economic activity would typically be tempered because some consumers would be reluctant to go out and spend despite the re-opening because of health safety concerns.

I believe this time is different because vaccinated consumers will be more likely to re-engage in pre-pandemic economic activity and, according to medical research, should be well protected against COVID-19 — so spending should not be tempered as in past re-openings. Israel’s re-opening is already proving that vaccinations are leading to an uptick in consumer activity, and they haven’t seen another wave of COVID-19 infections.

A preview of what’s to come in the US and UK?

In my view, Israel’s current state illustrates what we can soon expect in countries such as the United States and then the United Kingdom — and in any country once it has achieved broad vaccination of its population. In the United States, 31% of the population has received at least one dose of a vaccine, and 18% have been fully vaccinated.1 In the United Kingdom, 47% of the population has received at least one dose of a COVID-19 vaccine, although only 7.8% of the population is fully vaccinated.1

The US economy is already seeing significant improvement, further helped by fiscal stimulus. For example, the March employment situation report saw a far-better-than-expected increase in non-farm payrolls at 916,000.5 And we just got the ISM Services PMI for March, which was also far better than expected, clocking in at 63.7 with all 18 services industries reported growth.6 The only problem is that COVID-19 infections are on the rise in some states in the US, so vaccinations will need to maintain momentum in order to slow and ultimately stop the rise in infections.

The UK is a bit more complicated and hasn’t shown as much improvement yet because it remains at a relatively strict level of pandemic-related lockdown, although stringency is being eased gradually.

Investment implications

I expect that rising vaccinations and improving economic data are likely to lead to a continued rise in bond yields and outperformance of smaller-cap and cyclical stocks, especially in countries that are leading the recovery.

I should add that in the US, there are a few clouds on the horizon in the form of growing fears of rising taxes. And that is likely to be the case for a number of countries burdened with higher debt levels created by the pandemic. While far from a reality at the moment, if an increase in taxes becomes more likely — especially a large increase in corporate taxes – we could see some shift in leadership, albeit modest, to larger-cap and more defensive names. However, it’s important to stress I don’t believe this would end the stock market recovery, but could just cause some rotation in leadership.

But right now, the focus is on the virus and vaccinations. As the Brookings-FT Tracking Index for the Global Economic Recovery has indicated, the ability to control COVID-19 is likely to be the main determinant of economic success in 2021.7 That is why the index shows major economies such as China and the US leading the global recovery. The index suggests that there may not be a coordinated global economic rebound, but that instead there may be a time lag for some countries, especially Europe and Latin America, given their lack of progress in vaccine rollout and general difficulties in controlling the virus. This isn’t surprising — and it’s something we anticipated last year when putting together our 2021 outlook. In other words, we believe an economic recovery is in the future for all parts of the world, but its timing and strength will be dictated by control of the virus and vaccine rollout progress, and so we will want to follow this data closely.

Key takeaways

Recent data has been positive

Mobility, which we have found to be a helpful indicator of economic activity, has increased substantially in Israel.

A preview of what’s to come?

In my view, Israel’s current state illustrates what we can expect in countries that achieve broad vaccination of their populations.

What might this mean for stocks?

I expect this economic recovery to be very robust, which may lead to outperformance by smaller-cap stocks and cyclical stocks.

Please continue to utilise these blogs and expert insights to keep your own holistic view markets up to date.

Please see below for Legal & General’s latest Asset Allocation Team Key Beliefs Article, received by us yesterday afternoon 22/02/2021:

The consumer economy

Tim Drayson, our head of economics, often warns us not to bet against the US consumer. Last week, the US retail sales numbers for January smashed forecasts and once again showed that stimulus works, especially direct cash payments to households. Around 25% of the $600 received by individuals earning $75,000 or less was immediately spent, generating a $30 billion bounce in retail sales across all categories. Perhaps as a sign that economic optimism is already well priced in, equity markets chopped around last week although Treasury yields have been drifting higher.

The price of everything…

Clients are asking whether stock markets are getting ahead of themselves. We push back on this. If equity prices move up in lockstep with your view of the future improving, you should become neither more nor less optimistic. Given we believe we are early in the cycle, the mantra should remain unchanged: stay long, buy the dips.

Price is no determinant of value or valuations; it is only useful in relation to what you get for what you’ve paid. Is $100,000 a lot for a car? It depends if it’s for a Golf or a Ferrari. This is one reason we use multiples to think about valuations. Multiples that have historically exhibited mean-reverting properties over the long run have had some predictive power for longer-term returns. Prices, though, are not mean reverting and tell you nothing about future returns.

We pay particular attention to relative valuation. The yield gap is one representative measure; it hasn’t moved much recently but is still high by historical standards. Moreover, early in the cycle it’s quite normal for valuations to shoot up. This rebound has, so far, looked quite similar to the one in 2009 in magnitude.

Our baseline is that this bull market will last until the next recession. There’s a lot of runway left before then, in our view, and we expect the S&P 500 to be materially higher before the bull market ends.

Real talk

Investors are becoming more worried about the rise in bond yields and the possible impact on equity markets. The recent choppiness in equities while yields have drifted up adds to their nervousness. Although we believe nominal and real yields will rise further (and by more than currently priced in the forwards), we think this should be well digested by equity markets. We note that the 2013 taper tantrum saw a 75 basis point spike in bond yields but ‘only’ a 6% correction in the S&P. (Tim recently discussed the possibility of new US tapering.)

Empirically, there’s not much evidence that rising real yields are particularly bad news for equities, especially from these very low levels. In fact, rising real yields have mostly been associated with higher equities. Historically, the correlation between real yields and equity markets has turned negative at much higher real yields.

It’s crucial to understand what is driving yield moves. As long as rising yields reflect a combination of higher inflation and better growth prospects, this should be positive for markets. Only when policymakers become worried should we be ready for change. Equity markets may panic when they see either a de-anchoring of inflation expectations or they need to bring forward the timing of policy normalisation. In our view, it is far too early for either of these, but clearly both need to be monitored very closely.

All about that base effect

The next round of stimulus is still being debated by Congress. Last week, Treasury Secretary Yellen commented that “the risk of doing too little is greater than of doing too much”. If such an approach is adopted, the direct uplift to household incomes will potentially be at least three times larger than included in the COVID relief bill at the end of 2020. This money should hit people’s accounts just as the US begins to re-open more fully. Alongside the excess household savings accumulated during the pandemic, this could fuel a surge in demand.

This makes us think about the implications of the money supply glut. None of us have seen money supply grow on the current scale, the only precedent being during the Second World War. Half of the increase in broad money supply sits directly in household accounts, and cash as a share of financial assets for non-financial corporates is at its highest levels since 1969. We believe that a significant amount of this cash will be spent, boosting growth, corporate profitability, and possibly inflation.

On inflation, we know there will be a pronounced base effect around the spring as prices fell sharply while the economy was locked down last year. This, plus later boosts from CPI components that were depressed by restrictions like airfares and hotel prices, could temporarily raise inflation above target-consistent levels.

The Federal Reserve has highlighted this potential outcome, with January’s minutes containing a discussion on why it would be prudent to look through this increase. This makes sense in our view as it is equally likely that inflation will fall back in the summer. Base effects reverse, and there are also some aspects of inflation that have been lifted by the pandemic but are likely to weaken once the economy reopens. Used-car prices are an example.

Further out, the inflation picture becomes much murkier. How much slack will be left in the economy? Does the jump in money supply matter? Are some of the structural disinflationary forces of the past decade, like technology, beginning to shift? How well anchored are inflation expectations?

We believe that inflation becoming high enough to constrain monetary policy is still a way off. But if we get there, central banks in developed markets might be surprised by how much they have to raise rates to reduce inflationary pressure. Money doesn’t play a role in their models, despite monetary aggregates generally being excellent predictors of economic aggregates, and they aren’t able to directly undo the monetary and fiscal one-two that’s been so effective at putting cash in consumers’ pockets.

Please continue to utilise these blogs and expert insights to keep your own holistic view of the market up to date.

Please see below for the latest Brooks MacDonald Daily Investment Bulletin received by us today 11/02/2021:

What has happened

Markets were largely rangebound for the second day in a row as investors await any change to the vaccine narrative and the size and pace of US Fiscal Stimulus.

Fed Chair Powell

Yesterday Fed Chair Powell spoke to the Economic Club of New York. The two overall themes were an ongoing need for fiscal support and pushing back against concerns over inflationary pressures. Powell highlighted that the US market had struggled to generate inflation even when the jobless rate was at the multi-decade lows of 3.5% and that significant slack existed now. The Federal Reserve’s estimates of the true level of unemployment are c. 10% after the ‘hidden slack’ has been adjusted for. Powell weighed in on the stimulus debate stressing the headwinds to inflationary pressures and pushing back on the notion that larger stimulus would cause the US economy to overheat. These comments come as the various votes on the elements of the stimulus bill are moving through the House of Representatives with a vote expected on the full bill in a fortnight. On monetary policy, he stressed the need for ‘supportive monetary policy’ for the US to reach full employment again, calming fears that the Federal Reserve would look to reduce stimulus in the foreseeable future.

Vaccine update

The World Health Organisation recommended that the Oxford/AstraZeneca vaccine should be used on all adults even in countries where new variants are present. The WHO also endorsed the method, trialled by the UK government, to delay the second dose in order to provide a higher percentage of protection in the community at a faster rate. There has been some debate, particularly in European countries, over the efficacy of the Oxford/AstraZeneca vaccine in various demographic groups and the WHO’s support should help shift that debate. As we have mentioned previously, the Oxford/AstraZeneca vaccine is expected to be a workhorse for population wide protection due to its low cost and easier logistics, the WHO’s comments reduce the risk of countries needing to seek new supply sources.

What does Brooks Macdonald think

Fed Chair Powell’s comments yesterday very much played to the market’s narrative that the output gap (the gap between current output and potential output) will keep inflation under control for the time being. The debate on the overall size of the US Fiscal Stimulus package is being determined by a series of smaller votes on components of the broader bill. Powell’s comments yesterday may help calm concerns over the overall size of the bill as it progresses through Congress.

Markets globally will be responding to ongoing vaccination rollouts and keeping up to date with developments as they happen can, as ever, help inform your own views of the markets.

Please utilise our blogs in keeping your own views of the market up to date.

Please see below for the latest Brooks MacDonald Daily Investment Bulletin received by us today 21/01/2021:

What has happened

Markets greeted the inauguration of Joe Biden with a rally driven by the tech heavyweights. Some markets concerns remained around the final handover of Presidential power from Trump to Biden so there will be an element of welcoming the calmer tone of the new President as well as removing a transition risk premium.

President Biden

Yesterday’s inaugural Presidential address saw President Biden attempt to change the tone in Washington by encouraging bipartisan debate rather than absolutism. This speech was followed by a series of executive orders as expected. This included the US re-joining the Paris climate agreement, ceasing the withdrawal from the WHO, ending the travel ban on a number of Muslin countries and a federal mask rule on interstate travel and within federal buildings. As a sign of the focus for the new administration’s economic goals, there were also some specific COVID support measures such as pausing federal student loan repayments and extending the federal eviction moratorium. Yesterday’s speech, coupled with that of Janet Yellen earlier this week, paints a market friendly picture where near term support remains the focus. Of course, the sting in the tail could be higher taxes down the line but we need to remind ourselves of the thin Senate majority and the fact the midterms are in November next year and this could change the power balance in Congress yet again.

Central bank decisions

Yesterday we heard from the Bank of Japan which left monetary policy unchanged whilst predicting economic challenges over the course of 2021. Today is the turn of the ECB and given the central bank announced a further easing package in December, little dramatic change is expected. The central bank meets under the cloud of Euro Area CPI estimates that showed the region in deflation (-0.3%) compared to the year before. Whilst forward looking CPI estimates have been rising, in line with the broad global market reflation narrative, even these future estimates remain well below the ECB’s 2% target. The central bank therefore likely has room to increase stimulus but it isn’t clear that simply doing more of what has been tried before (bank lending, negative rates and quantitative easing) will have the desired effect.

What does Brooks Macdonald think

Equities rose and volatility fell as power transitioned peacefully between President Trump and President Biden. It is interesting that yesterday’s rally was so tech focused given fears over regulation under a Democrat White House and Congress. The rally yesterday implies that investors are confident the new administration has its hands full with the COVID response and is unlikely to look towards market unfriendly reform within that context.

Daily investment bulletins like this could prove to be very useful in the near future. Yesterday’s Presidential Inauguration is sure to cause ripples in the markets globally and keeping up to date with developments as they happen can, as ever, be very beneficial to your own views of the markets.

Please utilise our blogs in keeping your own views of the market holistic and up to date.

Please see below for Invesco’s article on Market Predictions for the year ahead, received by us yesterday 06/01/2020:

Happy New Year! No one wants a year in review for 2020, but here is what I learned from the past year: History may not repeat itself, but it sure does rhyme. What we learned from 2020 is a repeat of the lesson we learned from the global financial crisis (GFC): Central banks are very powerful. They can’t cure viruses and they can’t create jobs, but they can boost confidence and move markets — a lot. That is the big similarity 2020 had with 2009: Central bank intervention mattered, especially by benefiting risk assets.

When I think of the New Year, I think of predictions and resolutions. And so today, I provide you with a little of both.

My New Year’s predictions

1. US-China relations may get warmer. There seem to be two factions emerging among Biden loyalists: “reformists” who want to push China aggressively on key issues and check its power, and “restorationists” who want to restore US-China relations to where they were in the Obama administration. I believe Biden will do what he typically does: land somewhere in the middle. I don’t expect US-China relations to return to what they were pre-Trump. However, I do expect the relationship between the two countries to improve and normalize. In particular, I expect more predictability and less volatility. While Biden may not unwind tariffs immediately, I do expect him to unwind the Trump administration tariffs after a “study” of their impact (which has obviously been negative for parts of the US economy, especially agriculture). The Biden administration will likely be aggressive on specific issues with China and pursue those issues multilaterally — but I expect that to occur within the context of a broader US-Sino relationship that is more cordial because the fortunes of many US businesses are tied to China. The Chinese economy is on pace to soon overtake that of the US, with the timeline expedited due to COVID, which gives China growing leverage. In fact, the Centre for Economics and Business Research recently released its forecast that China will overtake the United States by 2028 as the world’s largest economy, which is five years earlier than previously estimated due to the two countries’ very different recoveries from the pandemic.1 In addition, China has already begun to signal that it would like improved relations with the US. China’s Foreign Minister Wang Yi said in a recent interview with the South China Morning Post that both the US and China have been negatively impacted by the deterioration in their relationship over the past several years, and that US-China relations have come to a “new crossroads” with a “new window of hope” opening.2

2. Developed countries may have a better recovery than they did post-GFC. As COVID-19 vaccines are broadly distributed, I expect the economic recovery to be far more robust and inclusive than the economic recovery coming out of the global financial crisis. I believe the services industry will rebound with greater intensity, benefiting many lower income workers. That doesn’t mean that there won’t be more glitches in distribution — I fully expect there to be. And there will likely be more pandemic-related headwinds, such as the development of worse strains of the virus. However, once a substantial portion of the population is inoculated, I expect the economic recovery to be powerful.

3. Oil may rise. Given my expectation for a strong economic recovery in 2021 as vaccines are distributed, I also expect demand for oil to increase significantly. I believe this will lead to a substantial increase in the price of West Texas Intermediate crude oil — even if we see a ramp up in oil production.

4. Bitcoin may fall. I know there is a lot of excitement over Bitcoin, but it’s starting to feel a bit like Tulipmania. Bitcoin rose more than 300% in 2020, with much of the gains made in the last few months of the year.3 I continue to believe gold is a far better choice for diversification into “hard assets” and as a hedge against geopolitical risk. Bitcoin might continue to run for a while this year, but I expect it to be volatile and to ultimately disappoint, as it has in the past after strong rallies.

5. The S&P 500 Index may have another double-digit return in 2021. With vaccine distribution beginning, a robust economic recovery anticipated in the not-too-distant future, as well as extraordinary accommodation from the Federal Reserve, I expect a continuation of the stock rally we saw in 2020, albeit with drops and pauses along the way. Better-than-expected corporate earnings should also help.

My New Year’s resolutions

1. Stay invested and well diversified. While I feel very confident about risk assets in 2021, that doesn’t mean there won’t be volatility and sell-offs in the coming year. I believe having adequate exposure to stocks, fixed income, and alternative asset classes is key to building a portfolio that may withstand volatility.

2. Look to Asia’s emerging markets. My outlook is especially bright for the emerging markets countries that have managed the pandemic well, such as China and Korea. These economies have a head start on the robust vaccine-fueled economic recovery that I expect in 2021.

3. Don’t overlook tech. While the economic rebound may result in strong performance by cyclical stocks in sectors such as energy and consumer discretionary, I don’t necessarily expect tech stocks to underperform. I continue to favor adequate exposure to the technology sector, as I believe many tech stocks may continue to benefit from trends that accelerated during the pandemic.

Although nothing is guaranteed for the future as proven by the year 2020, expert insight and opinion like this is a good way of seeing how actions and news developing worldwide could have an impact on the investment markets, and thus highlights good topics for discussion.

Please utilise blogs like these to aid your own informed opinions on what may lie ahead for the markets, but I reiterate that nothing is guaranteed for the future.