Please see the below article from Brewin Dolphin discussing market optimism driven by AI strength despite ongoing geopolitical and UK economic pressures, received yesterday – 27/05/2026.

Stocks rally on hopes for a U.S.-Iran deal and AI enthusiasm

Global stocks hit new highs this week. Investors were increasingly willing to look past geopolitical volatility, focusing instead on the strength of corporate earnings and the ongoing AI investment cycle.

The Iran-U.S. war continues to dominate the geopolitical backdrop. Oil prices have remained highly reactive to headlines surrounding ceasefire negotiations and the Strait of Hormuz. Oil prices have fluctuated sharply around the $100 per barrel level as markets weigh hopes of eventual de-escalation against the risk of prolonged supply disruption.

While negotiations remain complicated and unpredictable, investors still broadly believe both sides have incentives to avoid a sustained closure of the Strait of Hormuz.

Despite elevated oil prices and persistent geopolitical uncertainty, risk sentiment has remained remarkably constructive. A major reason is the continued strength of the AI ecosystem, which is increasingly driving both earnings growth and market leadership.

Recent semiconductor earnings (e.g. Nvidia’s results last week, which sizeably beat earnings expectations) once again reinforced that demand for AI infrastructure remains exceptionally strong. Companies across the ecosystem continue to report rapid revenue growth, strong pricing power and very high profit margins, supported by relentless spending on data centres and computing capacity.

One of the standout developments this week was semiconductor manufacturer Micron reaching a $1 trillion market capitalisation milestone, highlighting how enthusiasm has broadened beyond just the largest AI chip designers. Memory chips have become one of the clearest beneficiaries of the AI boom, as increasingly sophisticated AI models require enormous amounts of high-bandwidth memory to process and train data efficiently.

Importantly, this is both a demand story and pricing story. Tight supply conditions and surging demand for advanced memory products have driven sharp increases in memory chip prices, leading investors to significantly rerate valuations across parts of the semiconductor sector.

More broadly, markets are becoming increasingly optimistic that the AI investment cycle still has substantial room to run. U.S. hyperscalers continue to commit enormous capital expenditure towards AI infrastructure, reinforcing confidence that this is evolving into a multi-year structural growth theme rather than a short-term technology rally.

For now, that powerful combination of resilient earnings, expanding profit margins and sustained AI spending continues to outweigh concerns around geopolitics and energy volatility.

Markets remain hopeful that tensions in the Middle East will eventually ease and that shipping through the Strait of Hormuz can normalise. In the meantime, AI remains the dominant anchor for investor sentiment.

All eyes are on the UK economy

The UK economy is in focus as it’s at risk from higher energy prices, in turn causing higher interest rates and borrowing costs, while at the same time suffering from a political crisis.

Crucial to this is the outlook for inflation. Last Wednesday’s consumer price index (CPI) release showed headline inflation dropping to 2.8% in April, down from 3.3% in March. Core CPI also moderated to 2.5%, driven largely by downward pressure in housing and household services offsetting a sharp spike in motor fuel costs.

This softer-than-expected reading provides the BoE with some breathing space on interest rates. But it also highlights the cost of the war in the Middle East: without the geopolitical disruption to energy markets, inflation would likely have returned to the 2% target this month.

The reprieve is temporary: the energy price cap is set on a lagging basis and will shift from tailwind to headwind in June, and will be felt in July’s bills. Fortunately, for now there’s little evidence of second-round effects where fuel causes higher wage demands. In fact, the labour market seems weak, a far cry from 2022 when the last energy-driven price spike hit.

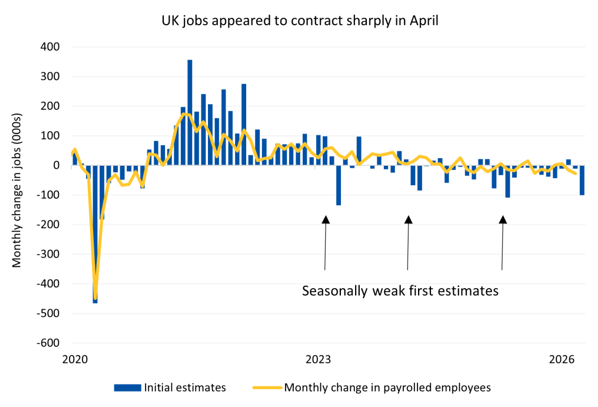

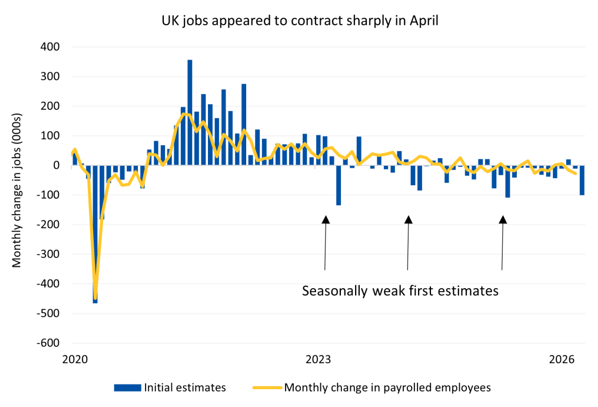

Last Tuesday’s Office for National Statistics release was materially worse than expected. Unemployment ticked up to 5%, but the real alarm was the early estimate of payrolled employees for April, showing a drop of 100,000 – far exceeding the roughly 20,000 decline economists had pencilled in, and the largest single-month fall since the start of the pandemic.

Source: LSEG Datastream

However, these data get heavily revised, particularly at this time of year. Each of the last three years have seen similar estimates of lost jobs, which have proven to be false when revised the following month. Nevertheless, the BoE faces a genuinely difficult balancing act and is now expected to defer interest rate increases until July or September.

Friday’s data showed UK government borrowing reached £24.3 billion in April, significantly exceeding the £20.9 billion forecast and applying further pressure to the national deficit.

Retail sales contracted by 1.3%, heavily concentrated in a striking 10% drop in fuel sales – indicating a clear behavioural shift as consumers actively drive less and dip into savings to manage sustained high energy costs. Consumer confidence slipped further into negative territory.

Thursday’s flash purchasing managers indices confirmed the pattern of divergence: U.S. manufacturing surprised to the upside, signalling resilience in the American industrial sector, while Eurozone indices remained largely in contraction territory. The UK services sector moved into deep contraction, though manufacturing held up.

This combination of softening inflation and strained consumer activity caused a slight recalibration in fixed-income markets. As the data suggested the economy is cooling, investors pared back expectations for prolonged elevated rates. In the UK, gilt yields fell marginally toward the end of the week, with the 10-year dipping to 4.9%.

Please continue to check our blog content for the latest advice and planning issues from leading investment management firms.

Marcus Blenkinsop

28th May 2026