Please see below for Blackfinch Group’s latest Monday Market Update Article, received by us yesterday 31/08/2021 due to the Bank Holiday:

UK COMMENTARY

Recruitment company Hays warned of “clear signs” of skills shortages worldwide and said hiring woes were pushing up wages in some hard-hit sectors. It also noted salaries are rising in certain industries as employers seek to attract and retain staff, particularly in the technology and life sciences sectors.

British car factories produced the fewest cars for any July since 1956 as they struggled with worker absences and the global shortage of computer chips. UK carmakers made 53,400 vehicles in July, a 37.6% drop when compared with July 2020, according to data from the Society of Motor Manufacturers and Traders (SMMT), the industry’s lobby group.

US COMMENTARY

The Chair of the US Federal Reserve (Fed), Jerome Powell, expressed concern about rocketing COVID-19 infections and was cautious on when it would start easing back on its stimulus programme. Powell’s remarks were far less hawkish than some Wall Street analysts had expected, and had a positive instant impact on the financial markets.

A new survey from the University of Michigan showed weakening US consumer confidence. Its consumer sentiment index fell from July’s final reading of 81.2 to 70.3 in August, the lowest recorded since December 2011.

EUROPE COMMENTARY

Rising prices, and the increase in COVID-19 cases, have knocked consumer confidence in Germany, the eurozone’s largest economy.

Figures released by Destatis showed that the German government’s efforts to fight the pandemic saw its budget deficit expand by €80.9bn in the first six months of 2021. That’s equal to 4.7% of GDP, and the highest reading since 1995.

ASIA COMMENTARY

Sentiment was weighed down by weaker-than-expected August Purchasing Managers’ Indices (PMIs) from China. The non-manufacturing PMI fell to 47.5, the first sub-50 reading since February 2020 (a sub-50 reading represents a contraction), which was below the 52.0 expected and down from 53.3 in July. Several factors were behind the slowdown, including further lockdowns to control the spread of the Delta variant, flooding in some regions, and ongoing regulatory changes that have impacted domestic wealth.

Please continue to utilise these blogs and expert insights to keep your own holistic view of the market up to date.

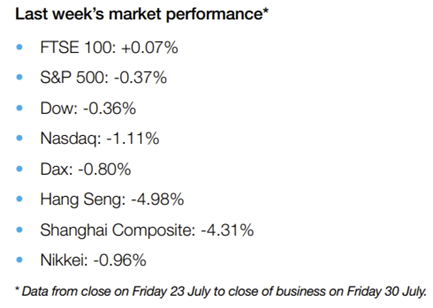

Please see below for Brewin Dolphin’s latest ‘Markets in a Minute’ article, received by us yesterday evening 03/08/2021:

Global equities were mixed last week as weaker-thanexpected US economic data offset strong corporate earnings reports.

In the US, the S&P 500 and the Nasdaq slipped 0.4% and 1.1%, respectively, after gross domestic product (GDP) growth and durable goods orders missed expectations. Amazon’s warning of slower growth in the months ahead weighed on the consumer discretionary sector, whereas utilities and real estate stocks outperformed.

The pan-European STOXX 600 ended the week flat amid ongoing concerns about the spread of Covid-19. The UK’s FTSE 100 was also little changed after a spike in the number of people told to self-isolate continued to disrupt production.

Over in Asia, Japan’s Nikkei 225 lost 1.0% as new Covid-19 cases reached record levels, resulting in Tokyo’s state of emergency being extended until the end of August. China’s Shanghai Composite slumped 4.3% following the country’s regulatory crackdown on the technology and education industries.

Delta woes weigh on markets

US stocks closed slightly lower on Monday as concerns about the Delta variant were compounded by softer-than expected manufacturing growth. The Institute for Supply Management’s index of national factory activity fell from 60.6 in June to 59.5 in July, the lowest reading since January and the second consecutive month of slowing growth.

Asian markets followed Wall Street lower on Tuesday, with the Nikkei 225 and Hang Seng tumbling 0.5% and 0.4%, respectively, as fears about the spread of coronavirus overshadowed strong US corporate earnings.

In contrast, the FTSE 100 and the STOXX 600 added 0.7% and 0.6%, respectively, on Monday, following news that British engineering firm Meggitt has agreed a £6.3bn takeover by US company Parker-Hannifin. Shares in Meggitt surged 56.7% from Friday’s close.

Market gains continued into Tuesday, with the FTSE 100 and the STOXX 600 up 0.4% and 0.3%, respectively, at the start of trading.

US economic data misses estimates

Last week’s headlines were dominated by the latest GDP figures from the US. According to preliminary data from the Commerce Department, the US economy expanded by an annualised rate of 6.5% in the second quarter. This was better than the 6.3% increase seen in the first quarter but was significantly below forecasts of 8.5% growth.

Personal consumption was the biggest driver of growth, as the stimulus cheques issued between mid-March and April fuelled an 11.8% year-on-year increase in household spending. This was partially offset by lagging property investments and inventory drawdowns.

Separate data from the US Census Bureau showed orders for cars, appliances and other durable goods in June were also weaker than expected. Orders rose by 0.8% from the previous month versus estimates of 2.2% growth, although May’s reading was revised up to 3.2% from 2.3%. It came amid continued shortages of parts and labour as well as higher material costs.

Meanwhile, the Labor Department reported that 400,000 people filed initial claims for unemployment benefits for the week ending 24 July, above the Dow Jones estimate of 380,000 and nearly double the pre-pandemic norm.

More positively, US consumer confidence was little changed in July, hovering at a 17-month high of 129.1. Economists polled by Reuters had forecast a decline to 123.9.

Inflation picks up in Europe

Over in the eurozone, inflation accelerated to 2.2% in July from 1.9% in June, according to figures from Eurostat. This was the highest rate since October 2018 and above the 2.0% reading forecast by economists. Higher inflation came amid faster-than-expected monthly GDP growth of 2.0% in the April to June period. Compared with the same period a year ago, GDP surged by 13.7%. The eurozone economy is still around 3% smaller than at the end of 2019, but the expansion marked a strong rebound from the 0.3% contraction seen in the first quarter of 2021.

Germany missed expectations with a quarterly expansion of 1.5%, as supply constraints left manufacturers short of materials such as semiconductors.

Half a million come off furlough

Here in the UK, more than half a million people came off furlough in June. The gradual reopening of the hospitality sector drove more than half the total fall in jobs supported by wage subsidies, according to data from HM Revenue & Customs.

Shortages of labour and materials and problems recruiting staff meant manufacturing output and order book growth slowed to its weakest level in four months in July. The manufacturing PMI stood at 60.4, down from 63.9 in June. IHS Markit said July’s performance was still among the best on record but would have been even better had it not been for supply constraints.

Nevertheless, the International Monetary Fund (IMF) upgraded its 2021 growth forecast for the UK to 7%, meaning that together with the US it would have the joint fastest growth of the G7 countries this year. In 2020, the UK’s economic contraction was the deepest in the group.

Please continue to utilise these blogs and expert insights to keep your own holistic view of the market up to date.

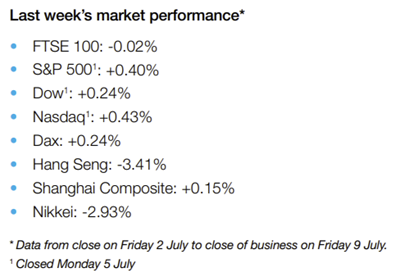

Please see below for Brewin Dolphin’s latest ‘Markets in a Minute’ article, received by us yesterday evening 13/07/2021:

Equities mixed as US Treasury yields slide

Stock markets were mixed last week as fears about a slowdown in global economic growth led to a steep decline in longer-term bond yields. US indices suffered heavy losses on Thursday as the yield on the benchmark ten-year Treasury note slid to a near five-month low. Although falling bond yields usually increase the relative appeal of equities, investors feared it signalled expectations of a slower recovery from the pandemic. The S&P 500 and the Dow managed to claw back losses on Friday to end the holiday-shortened week up 0.4% and 0.2%, respectively.

The spread of the Delta variant of Covid-19 also weighed on investor sentiment, particularly in Asia where Japan’s Nikkei 225 plunged by nearly 3.0%. Tokyo is being placed under a fourth state of emergency to try to curb the rise in infections. In Europe, the STOXX 600 recovered from Thursday’s sharp pullback to end the week up 0.2%. Germany’s Dax also added 0.2%, whereas France’s CAC 40 slipped 0.4%. The UK’s FTSE 100 was flat as the government confirmed it would ease quarantine rules for fully vaccinated adults and under-18s from mid-August, despite the surge in infections.

Stocks rise ahead of Q2 earnings season

Wall Street stocks were in the green on Monday (12 July) ahead of the start of the second quarter earnings season. Analysts expect strong results from banks such as JP Morgan Chase and Bank of America. The Dow, S&P 500 and Nasdaq all closed at fresh record highs, with the Dow narrowly missing the 35,000 mark. The FTSE 100 edged up 0.1%, with insurer Admiral leading the way on news its first half profits are likely to be higher than expected. Travel-related stocks underperformed amid data showing passenger numbers at Heathrow Airport in June were almost 90% lower than pre-pandemic levels. The FTSE 100 was up 0.3% at Tuesday’s market open, after the Bank of England said it was lifting Covid-19 restrictions on dividends from lenders. Shares in NatWest, HSBC and Lloyds all rose by around 2% following the announcement.

US economic data miss forecasts

A raft of worse-than-expected US economic data weighed on equities and bond yields last week. The Institute for Supply Management’s gauge of service sector activity fell to 60.1 in June, lower than the 63.5 figure forecast by economists in a Reuters poll and down from 64.0 in May. It came amid labour and raw material shortages, which resulted in the survey’s measure of backlog orders rising to 65.8 from 61.1 in May. The IBD / TIPP economic optimism index also slipped from 56.4 in June to 54.3 for July, its lowest reading since February. Elsewhere, figures from the Labor Department showed US weekly jobless claims rose to 373,000 for the week ending 3 July, worse than the 350,000 Dow Jones estimate. Job openings hit a record high of 9.2m in May, which was up 1.7% on the previous month but lower than the expected 9.3m.

UK economic rebound slows

Here in the UK, gross domestic product (GDP) expanded by 0.8% in May from a month ago, down from April’s 2.0% increase and weaker than the 1.5% expansion predicted in a Reuters poll. The Office for National Statistics said GDP growth remained 3.1% below its level in February 2020, just before the pandemic struck. The services sector rose by a weaker-than-expected 0.9% between April and May, as the huge surge in accommodation and food services output failed to offset slower increases elsewhere. Services growth was 3.4% below its February 2020 level. Meanwhile, manufacturing output slipped by 0.1% as the ongoing microchip shortage disrupted car production, leading to the steepest fall in the manufacture of transport equipment since April 2020. Construction output fell for a second consecutive month, down 0.8%, but remained the only sector to have output levels at above its pre pandemic level.

Eurozone retail sales rebound

There was more positive economic data from the eurozone, where monthly retail sales rose more than expected in May following a decline the previous month. According to Eurostat, retail sales rose by 4.6% monthon-month and by 9.0% from a year ago. This was above consensus forecasts of a 4.4% monthly rise and an 8.2% annual increase. The surge was driven by purchases of non-food products and car fuel as several countries lifted coronavirus restrictions. However, the rapid spread of the Delta variant has cast doubt over the speed of Europe’s economic recovery. On Friday, Germany and France warned people against travelling to Spain, where the infection rate is the highest in mainland Europe. The Netherlands said it would reintroduce restrictions on hospitality venues just two weeks after lifting them. Figures from the European Centre for Disease Prevention and Control, reported by the Financial Times, showed the weekly Covid-19 infection rate for the EU and European Economic Area rose to 51.6 per 100,000 people on Friday, from 38.6 the week before. The infection rate is expected to exceed 90 per 100,000 people in four weeks’ time.

Please continue to utilise these blogs and expert insights to keep your own holistic view of the market up to date.

Please see below for one of Invesco’s latest Investment Intelligence Updates, received by us yesterday 14/06/2021:

After April’s US CPI upside surprise, last week’s May reading was eagerly anticipated, albeit with a degree of trepidation. It didn’t disappoint. Headline CPI came in at 0.6%mom and 5%yoy, its highest level since 2008 (inflation peaked at 5.6%yoy then), while Core CPI rose even more at 0.7%mom, leaving it at 3.8%yoy, its highest since 1993. Both were 30bp above consensus expectations on a year-on-year basis. Strength was largely led by what are seen as “transitory” components, such as used cars (7.3%), car and truck rental (12.1%) and airfares (7%), even if there are other elements of consumer prices, such as shelter costs, that show more sustainable price pressures. Notwithstanding that we are probably close or at peak inflation as the impact of the lockdown starts to fall out of the calculation. How quickly and how far it will drop will be a function of whether rising costs, corporate pricing power and rising wages in a stimulus fuelled economy translate into more persistent inflation. For now, the Federal Reserve and increasing numbers of investors, witness a 10yr UST that is at its lowest level since early March, appear unconcerned about this risk. Time will tell whether this complacency is warranted or not, but it clearly remains a significant tail risk for financial markets.

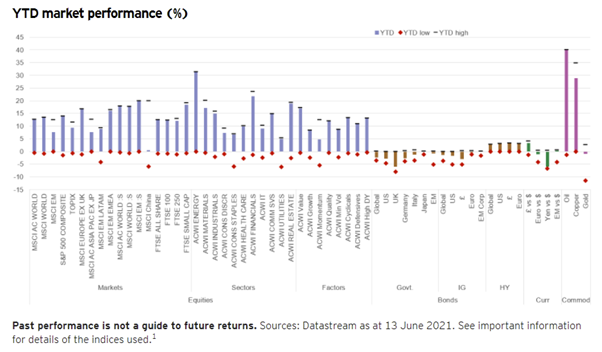

Global equity markets finished the week at a fresh all-time high, with a rise of 0.6% for MSCI ACWI. It is now up 12.7% YTD. DM (0.6%) led EM (flat), with both the US and Europe ex UK hitting new all-time highs, up 13.8% and 16.7% respectively YTD, with the latter the strongest major market of the week (1.2%). Small Caps (1.3%) outperformed again, hitting new all-time highs, with DM (1.3%) ahead of EM (1.1%). It was a rare week of Tech and tech-related sector outperformance, led by IT (1.6%). HealthCare (2.8%) was the best performing sector. Real Estate also had a good week (2.1%) and is now the third best performing sector YTD, up 18.8%, behind Energy and Financials. Lower bond yields weighed on Financial sector performance, while commodity sectors also lagged. Sector performance underpinned a strong relative performance week for Growth (1.4%) versus Value (-0.3%), while Quality (1%) had a good week too. UK equities were slightly ahead (All Share 0.9%) on the back of a good week for large caps (FTSE 100 0.9%) on strength in HealthCare, Telecoms and Energy.

Government bonds had a strong week with yields pushed lower by the belief that US inflationary pressures are transitory and a dovish stance at the latest ECB meeting. 10yr USTs and Gilts fell 10bp and 8bp respectively, taking them to their lowest levels since early March. They are now down 28bp and 18bp below their YTD highs, but are still higher than their starting level, hence the negative returns YTD from the asset class. Bunds and BTPs fell 6bp and 12bp. The better tone in government bond markets supported a good week for credit markets, where IG outperformed HY globally. IG yields fell 5bp with spreads narrowing by 2bp. The latter at 91bp are within touching distance of their post-GFC low (87bp). In HY a decline of 5bp in yields took them to all-time record lows (4.54%), but spreads at 353bp remain somewhat above their post-GFC lows (311bp).

The US$ edged higher over the week with the US Dollar Index up 0.5%, its third weekly gain, leaving it up 0.7% for the year. The Euro and £ were down -0.4% and -0.3% respectively.

Commodities overall were down slightly on the week with a -0.6% loss for the Bloomberg Commodity Spot Index, which is up just under 22% YTD. Brent, up 0.9%, hit its highest level ($73) in two years. In its latest monthly report, the IEA said that OPEC+ would need to boost output to meet demand that is set to recover to pre-pandemic levels by the end of 2022. Copper was up marginally too, 0.4% on the week, after a late rally on Friday as investors bet that China’s sales of strategic reserves would have a muted impact on demand. Gold edged lower (-0.6%) as it continued to consolidate around the $1900 level.

Andy Haldane, the Bank of England’s outgoing Chief Economist, described the UK’s housing market as being “on fire” last week. Recent House Price indices from the Halifax and Nationwide, the two biggest mortgage lenders, showed annual price growth of 9.6%yoy and 10.9%yoy respectively. These were the fastest rates of growth since 2007 and 2014 respectively and a lot faster than the rates of growth (3% and 3.5% CAGR respectively) seen in the decade leading up to the pandemic, described by another senior BoE official as housing’s “Quiet Decade”. And last Thursday’s RICS House Price Net Balance reading, which measures the breadth rather than magnitude of price falls or rises over the previous 3 months, hit +83% – its highest level since the housing boom of the late 1980s. Regionally it hit +100% in the N, NW and SW of England and Wales, while London was the standout laggard at just +46%.

All in all, a very uncharacteristic housing market, which typically fall and only recover slowly in severe economic contractions. This time around a combination of factors have delivered a very different market outturn: easing of lockdown restrictions have released pent-up demand. The government has supported the market through the Stamp Duty holiday (due to finish at the end of September), although it may not be as big a motivator for moving as some think. A recent survey by Rightmove shows that it is not the biggest motivation, with only 4% saying that they would abandon purchase plans if they missed the Stamp Duty deadline. Mortgage availability has improved, particularly for first-time buyers. Borrowing costs are low. Excess savings built up during the pandemic have provided cash for larger deposits. Finally, lifestyle factors (more space, relocating from large metropolitan areas) are at play. This has created an excess of demand over supply (the gap between new buyer enquiries and new instructions in the RICS survey was the widest since 2013) and, as with any commodity, when these imbalances occur prices tend to rise.

So, will the market remain “on fire”? In the RICS survey a national net balance of +45% envisage higher prices in the short-term (3m), while a greater +64% see them higher over 12m, although prices are only seen rising between 2-3%. Halifax and Nationwide also see the potential for further price rises in the coming months as most of the current demand drivers remain in place against a backdrop of a continued shortage of properties for sale. So, the fire may rage for a bit longer. Longer-term the RICS survey sees house prices appreciating by between 4-5% over the next 5 years. A still robust market, but certainly not to the same degree that we’re seeing currently. That would be a positive outturn for the economy.

Key economic data in the week ahead

The Federal Reserve and Bank of Japan meet this week to set their respective policy rates. Inflation data is a feature in both Japan and the UK this week, with the UK also publishing its latest employment report. In China economic activity for May is also released. Finally, there will be a number of post-G7 meetings in Europe next week, which may stir some interest, particularly those between the US and EU and Biden’s meeting with Putin.

In the US Retail Sales data for May is released on Tuesday. A decline of -0.6%mom is expected after no growth the previous month as the impact of pandemic-relief cheques faded. On Wednesday the Federal Reserve’s FOMC meets. While no change in policy is expected, market focus will be on its update of its economic projections, particularly any changes to the rates dot plot, employment and inflation projections (after two strong prints recently), as well as any clues on the future tapering of QE. Last week’s Initial Jobless Claims fell to a new pandemic low of 376k as the number of job openings has surged. On Thursday a further decline to 360k is expected.

There are a number of important data points this week in the UK. April’s Unemployment figures are published on Tuesday. A small decline to 4.7% from 4.8% is forecast. This compares to a recent high of 5.1% and 3.8% before the pandemic struck. On Wednesday May’s CPI will come out. Headline inflation is estimated to have increased 0.3%mom to 1.8%yoy mainly due to higher fuel prices. This will take inflation back to the levels seen immediately pre-pandemic. Core is also expected higher at 1.5%yoy from 1.3%yoy. So, both measures remain below the Bank of England’s 2% target. Retail Sales for May are released on Friday. After the non-essential shops re-opening bounce last month, a more sedate 1.6%mom is expected this month for sales ex Auto Fuel.

In Japan the Bank of Japan meets on Friday and is expected to keep its policy unchanged. CPI on the same day is forecast to have increased in May, but the Headline rate is still expected to be negative at -0.2%yoy, while Core is seen as flat, having fallen 0.1%yoy in April.

Chinese activity data for May is released on Wednesday. Industrial Production is forecast to have risen 9.2%yoy, slightly lower than 9.8%yoy in April. Retail Sales are also expected lower, but still strong at 14%yoy compared to 17.7%yoy in April. Fixed Asset Investment is seen up 17%yoy from 19.9%yoy last month.

There is no significant data coming from the EZ this week.

Please continue to utilise these blogs and expert insights to keep your own holistic view of the market up to date.

Please see below for one of the latest Invesco Insight articles written by Kristina Hooper, Chief Global Market Strategist at Invesco Ltd. This article was received by us today 07/04/2021:

A month ago, I wrote about the great progress Israel was making in terms of inoculating its citizens against COVID-19. At the time, I said that we would want to follow economic data in Israel closely for indications of what the US and UK could expect in the near future — as they are making swift progress in vaccinating their respective populations — as well as what any country can expect once it successfully vaccinates a significant portion of its population. Therefore, I think it’s worth re-visiting Israel to see the impact that widespread immunization has had on its economy. It’s clear that Israel’s vaccination program is not only having a substantial impact on consumer confidence, but also on spending.

Israel’s data shows the impact of vaccines

While vaccinations only began in December, they ramped up quickly. As of April 4, Israel has given at least one dose of a COVID-19 vaccine to 59% of its population, with 54% fully vaccinated.1 The economic impact was seen relatively early on. As morbidity moderated, restrictions eased and the third lockdown was rolled back — and the Bank of Israel’s Composite State of the Economy Index for February increased by 0.4%.2

Mobility, which we have found to be a helpful indicator of economic activity, has increased substantially. By the end of March 2021, retail and recreation mobility (restaurants, cafes, shopping centers, movie theaters, etc.) was off by only 6% from January 2020 levels, while grocery and pharmacy mobility is actually higher than those early 2020 levels.3 And, not surprisingly, economic activity accelerated in March. Daily credit card data shows that the value of transactions for the week ending March 22 was actually 15% higher than it was in January 2020.4 By comparison, back in April 2020, the value of transactions was more than 40% below its level in January of 2020.4 The rebound in spending has been strongest in some of the areas hardest hit by the pandemic, especially leisure and tourism.

Why is this time different?

What makes this time different than past economic re-openings, like we saw in spring 2020? Before broad vaccinations, the re-opening of an economy was a double-edged sword. Typically, a re-opening would often be followed, after a lag, with an increase in COVID-19 infections. In addition, the increase in economic activity would typically be tempered because some consumers would be reluctant to go out and spend despite the re-opening because of health safety concerns.

I believe this time is different because vaccinated consumers will be more likely to re-engage in pre-pandemic economic activity and, according to medical research, should be well protected against COVID-19 — so spending should not be tempered as in past re-openings. Israel’s re-opening is already proving that vaccinations are leading to an uptick in consumer activity, and they haven’t seen another wave of COVID-19 infections.

A preview of what’s to come in the US and UK?

In my view, Israel’s current state illustrates what we can soon expect in countries such as the United States and then the United Kingdom — and in any country once it has achieved broad vaccination of its population. In the United States, 31% of the population has received at least one dose of a vaccine, and 18% have been fully vaccinated.1 In the United Kingdom, 47% of the population has received at least one dose of a COVID-19 vaccine, although only 7.8% of the population is fully vaccinated.1

The US economy is already seeing significant improvement, further helped by fiscal stimulus. For example, the March employment situation report saw a far-better-than-expected increase in non-farm payrolls at 916,000.5 And we just got the ISM Services PMI for March, which was also far better than expected, clocking in at 63.7 with all 18 services industries reported growth.6 The only problem is that COVID-19 infections are on the rise in some states in the US, so vaccinations will need to maintain momentum in order to slow and ultimately stop the rise in infections.

The UK is a bit more complicated and hasn’t shown as much improvement yet because it remains at a relatively strict level of pandemic-related lockdown, although stringency is being eased gradually.

Investment implications

I expect that rising vaccinations and improving economic data are likely to lead to a continued rise in bond yields and outperformance of smaller-cap and cyclical stocks, especially in countries that are leading the recovery.

I should add that in the US, there are a few clouds on the horizon in the form of growing fears of rising taxes. And that is likely to be the case for a number of countries burdened with higher debt levels created by the pandemic. While far from a reality at the moment, if an increase in taxes becomes more likely — especially a large increase in corporate taxes – we could see some shift in leadership, albeit modest, to larger-cap and more defensive names. However, it’s important to stress I don’t believe this would end the stock market recovery, but could just cause some rotation in leadership.

But right now, the focus is on the virus and vaccinations. As the Brookings-FT Tracking Index for the Global Economic Recovery has indicated, the ability to control COVID-19 is likely to be the main determinant of economic success in 2021.7 That is why the index shows major economies such as China and the US leading the global recovery. The index suggests that there may not be a coordinated global economic rebound, but that instead there may be a time lag for some countries, especially Europe and Latin America, given their lack of progress in vaccine rollout and general difficulties in controlling the virus. This isn’t surprising — and it’s something we anticipated last year when putting together our 2021 outlook. In other words, we believe an economic recovery is in the future for all parts of the world, but its timing and strength will be dictated by control of the virus and vaccine rollout progress, and so we will want to follow this data closely.

Key takeaways

Recent data has been positive

Mobility, which we have found to be a helpful indicator of economic activity, has increased substantially in Israel.

A preview of what’s to come?

In my view, Israel’s current state illustrates what we can expect in countries that achieve broad vaccination of their populations.

What might this mean for stocks?

I expect this economic recovery to be very robust, which may lead to outperformance by smaller-cap stocks and cyclical stocks.

Please continue to utilise these blogs and expert insights to keep your own holistic view markets up to date.

Please see below for one of AJ Bell’s latest Investment Insight articles, received by us yesterday 28/03/2021:

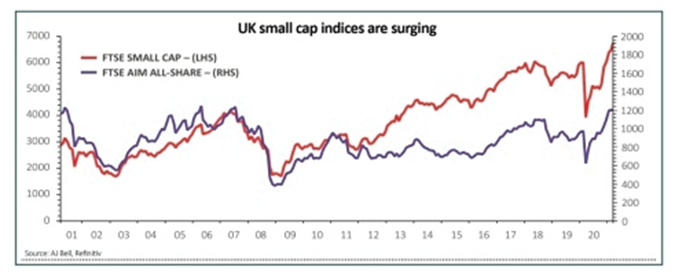

Small cap stocks are perceived to be riskier than their large cap counterparts and with good reason. As such, they can be used to judge wider market risk appetite – if small caps are rolling higher, we are likely to be in a bull market. If they are falling, we could be shifting to a bear market.

In general, small caps tend to be younger firms that are still developing. They are potentially more dependent upon certain key products or services, a narrower range of clients and even key executives.

Their finances might not be as robust as large caps and they are more exposed to an economic downturn, especially as they are less likely to have a global presence and be more reliant on domestic markets.

The UK’s FTSE Small Cap index currently trades at record highs, while the FTSE AIM All-Share stands near 20-year peaks. The latter is still well below its technology-crazed highs of 1999-2000. Equally, they are more geared into any local economic upturn.

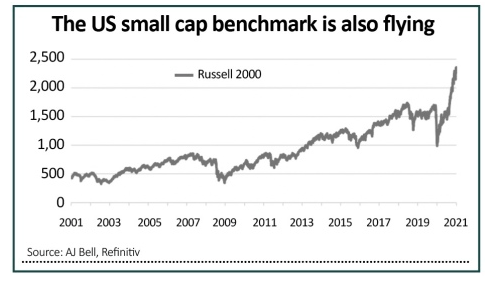

America’s Russell 2000 index, the main small cap benchmark in the US, is up 16% this year and by 116% over the past 12 months. That beats the Dow Jones Industrials, S&P 500 and NASDAQ Composite hands down on both counts.

In fact, the Russell 2000 now trades near its all-time highs, having gone bananas since last March’s low. Such a strong performance suggests that investors are in ‘risk-on’ mode and pricing in a strong economic recovery for good measure.

Rising Prices

One data point which does not sit so easily with the US small cap surge is the slight pullback in America’s monthly NFIB smaller businesses sentiment survey, which still stands 12 percentage points below its peak of summer 2018.

This indicator must be watched in case it does not pick up speed as America’s vaccination programme continues and lockdowns are eased. Further weakness could suggest the recovery might not be everything markets currently expect.

Equally, inflation-watchers will be intrigued by the NFIB’s sub-indices on prices. In particular, the balance between firms that are reporting higher rather than lower prices for their goods and services, and especially the shift in mix towards smaller companies that are planning price rises rather than price cuts.

If both trends continue, then bond markets could just be right in fearing that an inflationary boom is upon us.

Interest rates on the move

The number of interest rate rises continues to gather pace on a global basis. Last month there had already been five hikes this year in borrowing costs, in Zambia, Venezuela, Mozambique, Tajikistan and Armenia. There have now been six more – Kyrgyzstan, Georgia, Ukraine, Brazil, Russia and Turkey.

The 11 rate increases we’ve seen year to date is already two more than in the whole of 2020.

In contrast, the US Federal Reserve is content to sit on its hands despite what is happening elsewhere. Chair Jerome Powell continues to reaffirm the American central bank’s commitment to running its quantitative easing scheme at $120 billion a month, while any plans to increase interest rates from their record lows seem to be on hold until 2024.

Powell does not seem concerned about inflation and is seemingly willing to risk its resurgence to ensure that the economy gets back on track in the wake of the pandemic.

Yet financial markets are still taking the view that a strong upturn is coming, because US government bond prices are currently going down, and yields are going up, regardless of what the Fed says. That is a huge change from the last decade or so, when bond and stock markets have been happy to slavishly take their lead from central bank policy announcements.

Please continue to utilise these blogs and expert insights to keep your own holistic view of the market up to date.

Please see below for AJ Bell’s latest Investment Insight article, received by us yesterday 14/03/2021:

In some ways, markets had little to digest in the immediate wake of the Budget, as so much of the chancellor of the exchequer’s speech had made its way into the newspapers the previous weekend.

Rishi Sunak did come up with a couple of surprises all the same, in the form of the superdeduction for capital investment and his plan for eight freeports, designed to boost the UK’s trade flows in a post-Brexit world. The key issues raised by the Budget, at least from an investment perspective, passed unasked:

Why should anyone lend the UK money (and therefore buy its government bonds, or gilts) when it does not have the means to pay them back?

Why should anyone lend money to someone who cannot pay them back in return for a yield of just 0.77% a year for the next ten years (assuming they buy the benchmark 10-year gilt)?

Why would anyone buy a 10-year gilt with a yield of 0.77% when inflation is already 0.7%, according to the consumer price index, and potentially heading higher, especially if oil prices stay firm, money supply growth remains rampant and the global economy finally begins to recover as and when the pandemic is finally beaten off?

Anyone who buys a bond with a yield of 0.77% is locking in a guaranteed real-term loss if inflation goes above that mark and stays there for the next decade.

In sum, do UK government bonds represent return-free risk? And if so, what are the implications for asset allocation strategies and investors’ portfolios?

GILT YIELDS ON THE CHARGE

The benchmark 10-year gilt yield in the UK has surged of late. It is not easy to divine whether this is due to the fixed-income market worrying about inflation or a gathering acknowledgement that the UK’s aggregate £2 trillion debt is only going one way – up. But the effect on gilt prices is clear, since bond prices go down as yields go up (as is also the case with equities).

This is inevitably filtering through to exchange-traded funds (ETFs) dedicated to the UK fixed income market. The price of two benchmark-tracking ETFs has fallen, albeit to varying degrees. The instrument which follows shorter-dated (zero-to-five year) gilts has fallen just 2% since the August low in yields.

Meanwhile, the ETF which tracks and delivers the performance of a wider basket of UK gilts (once its running costs are taken into account) has fallen 8% since yields bottomed last summer.

That 8% capital loss is at least a paper-only one, unless an investor chooses to sell now, but the yield on offer does not come even close to compensating the holder for that paper loss, which supports the view that bonds now represent return-free risk.

SAVING GRACES

However, the higher bond yields go, the greater the return they offer and that means at some point investors may decide that the rewards are sufficient compensation for the risks, especially as three arguments could still support exposure to UK gilts.

The market’s fears of inflation could be misplaced. Bears of bonds have been growling about record-low interest rates and record doses of quantitative easing would lead to inflation for over a decade – and it has not happened yet.

If the West does turn Japanese and tip into deflation, even bonds with small nominal yields would look good in real terms and possibly better than equities, which would do poorly into a deflationary environment, at least if the Japanese experience from 1990 until very recently is a reliable guide.

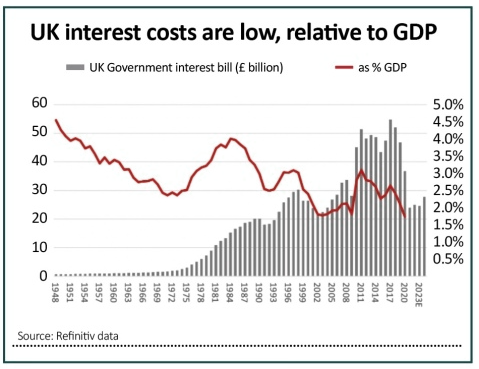

The UK’s financial situation may not be quite as bad as it seems. Yes, the national debt is growing but the Bank of England’s monetary policy is keeping the interest bill to manageable levels.

The Government’s interest bill as a percentage of GDP has hardly ever been lower. That buys everyone time and is also why Sunak is tinkering with taxes, to convince bond vigilantes and lenders alike that the UK can and will repay its debts, as it has every year since 1672 under King Charles II. A big leap in bond yields (borrowing costs) would be expensive.

The Bank of England could move to calm bond markets with more active policy. Whether that calms inflation fears is open to question but financial repression (see a recent edition of this column) could yet come into play, supporting bond prices and reducing yields.

In sum, no-one has a crystal ball. Therefore, bonds could yet have a role to play in a well-balanced portfolio over time, but it is inflation, rather than risk of default, that looks likely to be the greatest threat to any holder of gilts.

Please continue to utilise these blogs and expert insights to keep your own holistic view of the market up to date.

Please see below for Blackfinch Asset Management’s latest Monthly Market Moves article, received by us yesterday 08/03/2021:

Market Performance

1st- 28th February 2021 (in GBP Total Return)

FTSE 100

+ 0.65%

S&P 500 (USA)

– 1.21%

FTSE Europe (Ex UK)

– 0.94%

TOPIX (Japan)

– 1.87%

MSCI Emerging Markets

– 3.82%

Market Overview – February 2021

February was a tale of two halves for global bond and equity markets. What started out as a relatively positive month quickly reversed into a period of turbulent trading. Almost exactly one year to the day since the initial pandemic sell-off, inflation concerns caused bond yields to rise, causing a negative impact on equity markets, particularly those tilted towards growth stocks.

Inflation Fears Shake Markets

It has long been assumed that the economic recovery from the pandemic would cause some inflationary pressures. However, the fear that central banks, particularly in the US, may withdraw their substantial monetary policy support gripped investor attention.

President Biden’s $1.9trn stimulus package, which includes issuing further cheques to large swathes of the US population, moved closer to being agreed. This added further fuel to the inflation flames, evidenced already by the $600 cheques issued in January causing retail sales to come in way ahead of market expectations.

US Federal Reserve Chairman, Jerome Powell, did his best to reassure investors that the central bank will not consider raising interest rates, but his assurances did little to calm their nerves.

These fears caused the value of the US Dollar to appreciate. This in turn negatively impacts Emerging Markets, where countries hold significant portions of their debt in Dollars and therefore servicing this debt becomes more expensive.

Is the End in Sight for Lockdown?

More than 20 million people in the UK, almost one-third of the population, have received their first COVID-19 vaccine injection, with nearly 800,000 having received both doses.

Prime Minister Boris Johnson set out his ‘roadmap’ for an end to lockdown measures in England, starting with children returning to school on 8th March. While proposed dates are in place for a complete easing of lockdown, the public, and investors, should not get complacent given the prevailing uncertainty in the interim.

UK Gross Domestic Product came in ahead of expectations in December, reiterating the ongoing economic recovery.

Despite this, the UK economy contracted by a record 9.9% in 2020 but has so far managed to avoid a double-dip recession.

Little Change in Central Bank Policy

The Bank of England (BoE) left interest rates unchanged at 0.1% and kept its bond-buying programme at £895bn.

The BoE also commented on the possibility of negative interest rates, stating that most banks would need six-months to prepare for such a move. While this could be seen as foreshadowing a potential move towards negative rates in the future, it at least gives institutions some comfort that any move would not be in the near term.

The European Central Bank made no change to its monetary policy, keeping interest rates on hold as well as maintaining the €1.8trn Pandemic Emergency Purchase Programme (PEPP), confirming it will run until at least March 2022.

Chairman Jerome Powell announced that the US Federal Reserve will need to remain accommodative for “some time” yet. While its programme of substantial monthly government bond purchases looks likely to continue, Powell noted this could be eased once inflation and employment targets are reached

Summary

With markets having a difficult month, it is important to recognise just how far they have come in the last 12 months. As we pass the one-year anniversary since developed equity markets started to decline, as the potential impact of the pandemic became a reality, we must keep in mind that markets have rallied strongly since their trough in mid-March 2020. Therefore, periods of profit-taking are to be expected, particularly in those areas that have rallied the strongest.

While an end to lockdown measures feels within touching distance for some countries, including the UK, the emergence of new variants of COVID-19 remains a concern. As such, we need to temper any excitement of a ‘return to normal life’, as there is still a long way to go. Even so, right now in the UK the signs are promising that we may have our freedoms returned to us come the summer.

Please continue to utilise these blogs and expert insights to keep your own holistic view of the market up to date.

Please see below for Brooks MacDonald’s latest weekly market commentary received by us late afternoon 01/03/2021:

In Summary:

Yield rises remain the major driver of equity markets

Johnson & Johnson’s single shot vaccine is approved in the US, adding to the breadth of vaccine supply

Israel eases some restrictions as the UK is set to lay out its reopening plans

Yield rises remain the major driver of equity markets

Last week saw a large uptick in volatility as higher yields caused a sell-off in markets that focused on secular growth sectors such as technology. Meanwhile, previously unloved sectors such as banks performed strongly on the back of steepening yield curves and lower expected defaults in the future as the economy recovers.

Johnson & Johnson’s single shot vaccine is approved in the US, adding to the breadth of vaccine supply

The theme of the last few days has been a tightening of restrictions, rather than loosening, as several European countries needed to roll back liberties and Auckland, New Zealand entered a fresh lockdown. More positively, the Johnson & Johnson (J&J) vaccine has been approved in the US with the company saying they can ship 100 million doses in H1 2021. While the efficacy data was less compelling for the J&J vaccine, it is recommended as a single dose vaccine which makes the rollout of logistics simpler.

The change in yields has had an outsized impact on technology companies

The ‘price’ of a financial asset is the sum of its future cashflows adjusted for a discount rate. In practice this means the sum of a company’s future earnings which are adjusted for interest rates plus an extra company specific risk premium on top. Value companies tend to produce higher earnings now but less exciting earnings in the future. Growth companies, by contrast, produce little now but are expected to make outsized earnings in the future. Because the earnings in growth companies tend to be further away, the discount rate is more important. Due to the power of compounding, a small change in interest rates can significantly reduce the present value of future earnings 10 or 20 years away. This is exactly what happened last week when a pickup in interest rate expectations caused high growth companies to look less attractive. The moves were relatively small, with the US 10 year rising around 7bps to just over 1.4% but with valuations richer in the technology space, this was enough to catalyse a sell-off.

Of course, the question is whether central banks will let further yield rises happen. So far, the Federal Reserve have pushed back against expectations for sustained inflation but have broadly welcomed the pickup in yields, saying it is reflective of an improved economic backdrop. The next Federal Reserve (Fed) meeting is on 16-17 March, however this week we hear from a series of members including Fed Chair Jerome Powell. Should rapid rises in yields continue to be a theme, we expect the Federal Reserve to step in, at least verbally, to steady further rises. Yield rises can impact both financial stability and damage the economic recovery so central banks will be paying close attention.

Please continue to utilise these blogs and expert insights to keep your own holistic view of the market up to date.

Please see below for the latest Brooks MacDonald Weekly Investment Bulletin received by us yesterday 01/02/2021:

Vaccine nationalism raises its head as competing contracts and supply issues collide

A bout of risk off sentiment hit equities, bringing most European and US indices slightly negative for the first month of 2021. The risk of a vaccine trade war, less positive data from Johnson & Johnson’s vaccine and the risk of further COVID-19 restrictions all dampened the mood. Friday saw a bubbling over of increasingly hostile words between the EU and AstraZeneca. In short, the EU imposed the right to ban vaccine exports outside of the EU (and select countries) and effectively imposed a hard border between Northern Ireland and the Republic of Ireland. This proved only temporary, with the hard border reversed and the prospect of export bans to the UK played down as Friday and the weekend progressed. So called ‘vaccine nationalism’ has been a threat for several months as issues over regional supply chains combine with the sequencing of competing contracts and an increasingly frustrated populace. On Sunday, the UK announced that it had provided almost 600,000 vaccinations in one day (over 1% of adults), which may suggest that as supply increases, countries will be able to work quickly to inoculate their populations.

Markets look ahead to Friday’s US employment data after last month’s disappointment

This Friday sees the important non-farm payroll US employment figures released. Last month saw a decline of 140,000 jobs1 , the first decline since the first wave of the pandemic. This month economists are expecting a 50,000 increase and therefore for the headline 6.7% unemployment rate to remain stable2 . US economic data has shown resilience in the face of the current COVID-19 wave but there is still a large amount of spare capacity in the labour market, something that may curb any bubbling inflationary pressures. With employment a major item on President Biden’s agenda, it seems likely that the US Stimulus Package will move through Congress under the Budget Reconciliation rules. The downside of using this process is that there is a limit on the scope of the legislation and a limit on the number of times the process can be used.

US stimulus may progress using the budget reconciliation process but this has limits

The prospect of using the budget reconciliation process has dampened expectations of a bipartisan agreement that could leave the door open for further stimulus over the coming months. The reconciliation process means that the bill can pass with a simple majority in the Senate rather than being held up by the filibuster. The reconciliation process has historically only been used once per calendar year due to its inbuilt limitations, so there will be additional scrutiny on the proposed package if it is expected to be the only US stimulus in 2021.

Weekly investment bulletins like these are a good way to get regular input from market experts.

The mass rollout of the vaccine is set to cause gradual change to the market outlook, hopefully life and economies will improve.