Please see below the Brooks MacDonald Daily Investment Bulletin received by us yesterday, 22/09/2021:

What has happened

European indices posted strong gains yesterday, offsetting much of Monday’s weakness, however US bourses performed less well remaining mostly flat from Monday’s close.

Evergrande

Whilst Evergrande has been at the centre of the financial world this week, Chinese markets have been on holiday. When the equity markets opened for trading this morning shares dipped however the People’s Bank of China injected CNY 90bn of liquidity into the system to steady investor nerves. Reports are suggesting that Evergrande will make the domestic coupon payment due tomorrow however there has been no word yet as to payments on the foreign dollar denominated bond. The interest payments due on bank loans at the start of the week are reportedly yet to be paid so plenty of moving parts to this story. Expectations are pointing to a restructuring orchestrated by Chinese authorities and for the government to allow Evergrande itself to default but to take steps to ensure there isn’t extensive contagion into either Chinese property prices or the property investment sector.

US Infrastructure

The bipartisan $500bn physical infrastructure bill that passed the Senate vote but was held up in the House is now said to be moving to a House vote on Monday. This has less to do with any movement on the broader ‘social infrastructure’ bill but more to do with the proximity of the debt ceiling which is now demanding the focus of Democrats and the White House. Should the Republicans not support the government funding bills the White House will be forced to use budget reconciliation to pass the bills. Given there are procedural limits on the number of reconciliation bills in a Congress year, this risks Democrats having to hastily incorporate the least contentious parts of the $3.5 trillion social infrastructure bill, effectively watering down the size and scope quite considerably.

What does Brooks Macdonald think At 7pm UK time we will receive the latest policy statement from the Federal Reserve followed by a press conference by the Fed Chair. Expectations are for the bank to continue to guide to tapering this year but with the caveat that the economy must remain on track for the central bank to pull the taper trigger. This optionality will be important for market sentiment as if the Fed leaves a delay of taper on the table, even if it’s likely they won’t use it, this will provide a release valve for market concerns over the coming months.

Please continue to utilise these blogs and expert insights to keep your own holistic view of the market up to date.

Please see below for Brooks MacDonald’s Daily Investment Bulletin received by us yesterday 19/08/2021:

What has happened

Markets spent much of Wednesday in a holding pattern ahead of the release of the Fed July meeting minutes. That changed when the minutes came out, as they showed that most officials looked to be favour of starting to taper bond purchases by the end of 2021. As a result, expectations around Fed Chair Powell’s speech next week at Jackson Hole will have gone up a notch or two, as investors await fresh clues on what a potential strategy for tapering might look like. After the release, US 10-year Treasury yields gave up the day’s gains of around 3bps to finish broadly flat at around 1.26%, but in early trade this morning, have traded lower, below 1.25%. US equities, already small down on the day, moved lower after the report was published, with cyclical and growth sectors falling in broadly equal measure. Overnight Asian markets are following Wall Street’s lead, trading lower this morning. Separately, Wednesday also saw the latest UK Consumer Price Index (CPI) data for July, which came in at 2% year on year, below June’s 2.5%, and below expectations of 2.3%. However, such is the ongoing distortion from base effects and reopening imbalances that neither the ‘transitory’ nor ‘sustained’ inflation camp was able to claim the advantage.

Fed releases its July meeting minutes

The release of Fed meeting minutes doesn’t normally get this much attention, but such is the focus around when the US Fed might look to start tapering its asset purchase programme. Regarding the subject of the taper, the minutes showed that ‘most participants noted that, provided that the economy were to evolve broadly as they anticipated, they judged that it could be appropriate to start reducing the pace of asset purchases this year.’ The committee also discussed the method by which to taper asset purchases, with most participants wanting to taper purchases of Treasury securities and Mortgage Backed Securities ‘proportionally in order to end both sets of purchases at the same time.’ Finally, the minutes showed members wanted to emphasise the decisions between tapering and rate hiking would be separate and not dependent on each other, saying that ‘participants indicated that the standards for raising the target range for the federal funds rate were distinct from those associated with tapering asset purchases’. This last point seemed to fit with comments earlier in the day on Wednesday from St Louis Fed President Bullard, who said that he preferred that tapering were finished by Q1 2022, and that Q4 2022 was a ‘logical place’ for interest rate hikes to commence.

US health officials announce plan for widescale COVID vaccine booster shots

US health officials including Dr Fauci, Biden’s Chief Medical Advisor, came out with a joint statement on Wednesday, saying that subject to final FDA (Food and Drug Administration) and CDC (Centers for Disease Control and Prevention) approvals, the US would recommend booster shots to all Americans who had received the Pfizer or Moderna vaccines. The outlined plan on Wednesday suggested an booster dose should follow eight months after the second dose, and that the booster doses could begin during the week of 20th September. The drive to offer booster shots has come because of the rise in delta variant cases, as well as signs that the vaccines’ effectiveness is falling over time. According to CDC Director Walensky on Wednesday, ‘our plan is to protect the American people, to stay ahead of this virus’. As for those who had received the single-dose Johnson & Johnson (J&J) vaccine, health officials suggested they might also need booster shots, but that they were awaiting more data, principally because the J&J vaccine rollout had started much later than the other vaccines.

What does Brooks Macdonald think

Vaccines remain the ultimate game-changer in the fight against the pandemic. With concerns of falling protection over time, booster shots have been expected, but the fact that the US has formalised a widescale plan around this should be positive for markets. The flip-side is that for every Pfizer or Moderna vaccine given as a booster, it is potentially one-less shot available for those in poorer economies who have yet to get their first or second shots. Reiterating this point, the WHO (World Health Organization) on Wednesday objected to the US plan on the grounds that it could exacerbate vaccine-inequality especially for relatively poorer countries globally. If that assessment is right, then it probably lengthens the odds of seeing a synchronised economic recovery globally.

Please continue to utilise these blogs and expert insights to keep your own holistic view of the market up to date.

Please see below for Brooks MacDonald’s Daily Investment Bulletin received by us yesterday 28/07/2021:

What has happened

Equities had a weaker session yesterday with defensive equities outperforming technology stocks in particular. Some of this weakness in technology can be attributed to the concerns that China might continue to expand regulation after their foray into educational technology earlier this week.

Chinese technology

Markets have long had a concern around technology regulation in the US where a Democrat White House could try to curb the perceived overreach of big technology. Investors had downgraded this risk due to the economic impact of the pandemic but also a belief that the US would be unlikely to do anything too aggressive in case Chinese companies gained a competitive advantage. With China ‘going first’ on technology regulation this not only increases risks around Chinese securities but removes one of the arguments as to why the US would stay quiet on technology regulation for now. Meanwhile in the US, technology earnings saw some winners and losers with Alphabet rising 3% in the after-market but Microsoft losing an equal amount after it’s cloud-services business saw less growth than expected.

Federal Reserve

Now to the week’s major event, the Federal Reserve’s latest policy statement which is due out at 7pm UK time tonight followed by Fed Chair Powell’s press conference. Policy risk is at its highest at points of transition and the Fed will need to tread a delicate path today. The tapering genie is out of the bottle and will almost certainly be a conversation topic at the meeting however the extent to which Powell majors on this will give an important steer to the market. The rising risks around the delta variant and lower global growth expectations have both contributed to a less positive market backdrop ahead of tonight’s announcement. The statement will also need to address inflation where we have seen another upside beat to price levels in the June CPI numbers but inflation expectations have been falling in the bond market. Some of this reduction in inflation expectations is due to a belief that the Fed will not be afraid of raising rates over the next two years so there is a complex interplay that Powell will need to consider.

What does Brooks Macdonald think

Due to the rising uncertainties around the pandemic and economic growth, we expect Powell to stop short of warning that tapering is imminent. This meeting may well therefore serve as a placeholder until either the Jackson Hole Economic Symposium in August or indeed the meeting in September.

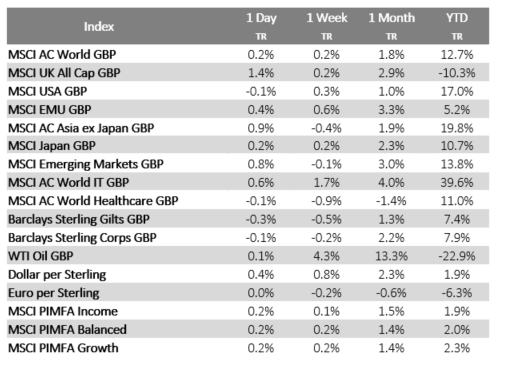

Source: Bloomberg as at 28/07/2021. TR denotes Net Total Return

Please continue to utilise these blogs and expert insights to keep your own holistic view of the market up to date.

Please see the below article from Invesco received late yesterday afternoon:

Key takeaways

The Fed does not have a trigger finger

Just because the Fed reacts negatively to a data point doesn’t mean it’s going to tighten monetary policy at its next meeting.

Some inflation is expected

Time and again, Fed officials have warned that a spike in inflation is likely as the US economy re-opens.

The Fed’s approach has changed

The Fed has gone through a paradigm shift when it comes to inflation targeting.

Last week, investors shuddered as data showed a big rise in prices in the US and a greater-than-expected rise in prices in the eurozone. Stocks sold off, US Treasury yields climbed higher, and market pundits obsessed over inflation. I feel it’s important at this juncture to remind investors of a few truths surrounding inflation and the Federal Reserve.

1. The Fed does not have a trigger finger

Just because the Fed reacts negatively or says it’s surprised by one or more data points doesn’t mean it’s going to tighten monetary policy at its next meeting. Some investors were taken aback by Fed Vice Chair Richard Clarida’s comments last week when he said he was surprised by some recent data points such as the Consumer Price Index, which was much higher than he expected. However, he was quick to reassure: “Honestly, we need to recognize that there’s a fair amount of noise right now, and it will be prudent and appropriate to gather more evidence…” Don’t forget that the Fed’s new catch phrase is “patiently accommodative.” In other words, the Fed is going to err on the side of accommodation and is likely to deliberate extensively before tightening.

2. The Fed anticipates a spike in inflation as the economy re-opens

At a Wall Street Journal conference in early March, Fed Chair Jay Powell explained that, “We expect that as the economy reopens and hopefully picks up, we will see inflation move up through base effects. That could create some upward pressure on prices.” In fact, time and again, Powell and other Fed officials have telegraphed that a spike in inflation is likely as the US economy re-opens. The Fed is ready and accepting of that rise in inflation.

3. We won’t know any time soon if the increase in inflation is temporary or persistent

A temporary rise in inflation is at least partially the result of base effects — in other words, the comparisons to a year ago look distorted given what poor shape the economy was in last spring as the pandemic took hold. In addition, there is currently a mismatch between supply and demand which can drive up prices — think of the supply chain issues that are being experienced right now in some industries and the pent-up demand that is now being exercised as economies re-open. However, these are likely to create only temporary inflation. After all, how many flights can you take and haircuts can you get once the economy re-opens? Clearly, the law of diminishing marginal utility suggests that at a certain point, satisfaction with each additional flight or haircut is reduced.

Now, there are forces that can lead to more persistent inflation. Typically wage increases lead to “stickier” inflation. We have not yet seen a significant rise in average hourly earnings in the United States, and it seems unlikely that will happen quickly given the very substantial amount of labor market slack.

Monetarists would argue that it all comes down to money supply; a significant increase in money supply can spur persistent inflation, and right now we have seen a very significant increase. However, one other key ingredient is usually present as well: an increase in the velocity of money, which we have not yet seen. The quantity theory of money posits that inflation is not just a function of money supply but also the velocity of money. As the St. Louis Fed explained in a brief research note, “If for some reason the money velocity declines rapidly during an expansionary monetary policy period, it can offset the increase in money supply and even lead to deflation instead of inflation.” But even if a money supply increase is enough to spur persistent inflation, this would not occur immediately — it usually occurs with an 18-24 month lag, suggesting we may not see it until late 2021 or early 2022.

4. The Fed’s inflation targeting policy represents a paradigm shift for the Fed

The Fed has gone through several paradigm shifts in the last several decades, and they’ve been transformational. I’m old enough to remember when the Fed didn’t believe in regular communication with the public, when the size of then-Fed Chair Alan Greenspan’s briefcase was the best indicator of what the Fed’s decision on rates would be at the next Federal Open Market Committee (FOMC) meeting. And now of course, the Fed is extremely transparent, working hard to telegraph its views and actions before taking them. Similarly, the Fed had a very different inflation targeting policy before last summer. Its current policy, called Average Inflation Targeting (AIT), means that the Fed’s objective is to push inflation enduringly above 2% and attain full employment before considering tightening. In other words, this new policy enables the Fed to be far more flexible and essentially tolerate economic overheating. This is NOT the Fed of yesteryear, which believed that its role was to take away the punch bowl just as the party was getting started. This Fed might leave out the punch bowl into the wee hours, even as partygoers get drunk.

What does this mean for investors?

This begs the question: what are investors afraid of? Are they afraid of inflation — or the Fed tightening in reaction to inflation? It seems to me that they are far more worried about the latter than the former. That would explain why last week’s negative reaction to signs of inflation was so very short-lived, as Fed officials provided reassurance. And so perhaps investors should be more concerned about the former, especially if the Fed remains “behind the curve” and is unable to easily tame inflation once it tries to. While I must stress that this is far from my base case scenario, it is a risk that needs to be considered since inflation can have a negative impact on some asset classes. If persistently higher inflation were to occur, investors could benefit from exposure to commodities, cyclical stocks, inflation-protected securities, emerging market assets and even dividend-paying stocks as part of a diversified portfolio.

This week there is more potential for volatility, as investors wait with bated breath for the FOMC minutes, which could offer more insight into what the Fed is thinking with regard to inflation and tightening.

Our Comments

The markets are still volatile at the moment but are generally on an upwards trend as you can see from the below chart of the FTSE 100 over the past year:

Source: Google, as at 16:35 BST 19/05/2021

Global markets are increasingly more interconnected and US inflation fears affects the UK markets (and vice versa).

Inflationary fears will continue as will the volatility however as we always state, its important to remain calm and ride the volatility out.

Please see below for the Daily Investment Bulletin from Brooks McDonald, received by us today 17/12/2020:

What has happened

The Federal Reserve had their final rate setting meeting of the year and were eager to reassure markets that quantitative easing would remain until the economy had improved substantially. Whilst markets initially wavered over the lack of further measures they eventually settled largely unchanged.

Last Fed meeting of 2020

The Federal Reserve has been responsible for a large number of the blockbuster stimulus headlines over 2020 but those hoping for another round of accommodation were disappointed. The committee stressed that it would continue with the current pace of quantitative easing until ‘substantial further progress’ had been achieved towards their inflation and employment targets. There was some change to the 2023 interest rate expectations with one member showing a hike that year and also to the 2023 inflation level expectations where 4 members pointed to a small overshoot of the 2% target. Of course, a small overshoot would not pose a problem for the bank given it has unveiled average inflation rate targeting earlier in the year which will give them additional room if needed.

Update on unfinished business

The tone around Brexit talks improved again yesterday with sterling seeing further strength but remaining in the 1.09-1.11 band versus the Euro that it has been maintaining despite the high jinks of recent weeks. EC President von der Leyen said yesterday that ‘there is a path to an agreement now’ but reports suggest that fisheries remain a stumbling block. Rumours are circulating that Parliament is readying to return early next week to vote on a deal which is also supporting the UK currency. Meanwhile US Fiscal Stimulus talks continue amidst a positive tone, but the spectre of Christmas is nearing so there is a narrowing path to pass through Congress. The more contentious $160bn bill appears to have been predictably side-lined but the more substantial package seems to have the support of both sides.

What does Brooks Macdonald think

Economic data over the last few days has seen beats in Europe (specifically the compositive PMIs) and misses from the US on retail sales. This highlights how difficult it is for economists to calculate activity during periods where restrictions are gradually tightening, and consumer behaviour is shifting. The miss in US retail sales does provide further impetus for fiscal stimulus however and markets shrugging this off reflects hope that this may provide a catalyst for support rather than be a sign of things to come.

Regular daily updates like these are a useful method of frequently updating your holistic view of the markets, especially given the way the market is rapidly changing by the day with Coronavirus and Brexit.

Please continue to utilise these blogs to help inform your own views of the markets.