Please see the below article from Brooks Macdonald detailing their discussions on markets. Received this afternoon 02/04/2026.

What has happened?

Global equity markets extended their rally yesterday, led once again by US tech stocks. The S&P 500 rose +0.72%, with the NASDAQ (+1.16%) and the Mag 7 (+1.37%) outperforming. European markets played catch up to Monday night’s US gains, recording sharp advances across the region. The STOXX 600 (+2.50%), DAX (+2.73%) and FTSE 100 (+1.85%) all posted their largest daily gains since last April. The risk on mood also spilled over into bond markets, helped by easing energy prices. Natural gas prices fell sharply, with front month TTF futures down -5.49% to €47.51/MWh, the lowest level since early March. As a result, government bond yields declined, with 10 year bund yields falling -1.8bps to 2.98%, while UK gilt yields dropped more sharply after a downward revision to the UK manufacturing PMI. Elsewhere, euro area manufacturing data was revised slightly higher, pointing to resilience despite recent energy price volatility.

Trump rhetoric offered little reassurance

Market sentiment has weakened overnight after President Trump’s widely anticipated address offered little clarity on the timing or conditions for ending hostilities with Iran. While suggesting the military operation was “very close” to completion, he also warned of further escalation if negotiations fail, with no clear signal of an imminent off ramp. The US again emphasised that safeguarding shipping through the Strait of Hormuz should fall largely to other nations. In response, Brent crude rose sharply and is trading above $107 this morning. Meanwhile, the UK is set to convene talks with around 35 countries to discuss restoring shipping routes, highlighting the growing role of US allies in managing regional fallout. Separately, renewed commentary around a potential US withdrawal from NATO briefly drew attention, though significant political hurdles remain.

What does Brooks Macdonald think?

Attention now turns back to US economic data, particularly the labour market, which remains a key anchor for market expectations. After yesterday’s firmer than expected ISM manufacturing reading and stronger ADP employment data, investors will be watching today’s weekly jobless claims and Friday’s non farm payrolls report closely, even as many global markets are closed for Good Friday. With inflation pressures still present and energy prices volatile, incoming labour market data will be important in shaping views on the resilience of the US economy and the path for monetary policy.

Please continue to check our blog content for advice, planning issues and the latest investment, market and economic updates from leading investment houses.

Please see the below article from EPIC Investment Partners received this afternoon 04/03/2026.

Both the Asia ex Japan and the Emerging Market asset classes are dominated by four countries. Namely China, Taiwan, South Korea and India. The top ten index weights in the latter index are all Asian companies. These two asset classes are essentially twins.

In the decade to October 2022, the World Index achieved a compound growth rate of 8.93%. Asia ex Japan managed just 2.41% and the EM Index only 1.12%. It was a lost decade for both asset classes – painful for managers and clients alike as investors deserted both.

The shares outstanding in the US listed iShare Asia ex Japan Index more than halved between mid 2021 and mid 2024 as capitulation accelerated, while the shares outstanding in the US listed iShare EMF Index fell by two thirds between early 2013 and early 2025.

Things may be looking up. Since the global market bottom in October 2022 both Asia ex and EM indices have outperformed the World Index. They have compounded at nearly 25% while the World Index has achieved a little over 20%. There has been a very modest uptick in the shares outstanding in both ETFs but one almost needs a magnifying glass to see this.

Events over the last five days in the Middle East have seen equities fall sharply, especially in Asia. South Korea has fallen 18.4%, Taiwan 7.3% and the Hang Seng Index 5.2%. India has fared better, -2.8%, but the market was closed today. The North Asian markets have powered the region higher year to date so a correction from record highs is not unsurprising.

That said, the successful strikes on energy facilities, coupled with the effective closure of the Strait of Hormuz, were unexpected developments and have caused oil and gas prices to rise sharply. Not great news in the short term for energy hungry Asia. Further scares, and more volatility, is to be expected. However, taking a longer-term view, we believe this downturn represents an excellent chance for investors to open or increase exposure to both asset classes.

Please continue to check our blog content for advice, planning issues and the latest investment market and economic updates from leading investment houses.

Please see the below article from Brooks Macdonald detailing their discussions on UK and US markets. Received this morning 10/02/2026.

What has happened?

Global equity markets extended their rebound yesterday, with the S&P 500 (+0.47%) closing just shy of a record high and the STOXX 600 (+0.70%) reaching another all time high. Technology stocks led the move, reversing much of their recent weakness, and the S&P 500’s software segment (+3.36%) registered its strongest daily gain since May last year. The recovery in sentiment also lent support to other asset classes, including gold (+1.88%), while broader newsflow remained relatively muted. US Treasury yields drifted lower following comments from NEC Director Kevin Hassett, who suggested that markets may see “slightly lower jobs numbers” in tomorrow’s delayed January employment report, though he cautioned that such an outcome “shouldn’t trigger any panic.”

Political unease pressures UK markets

UK assets came under renewed pressure as domestic politics returned to the spotlight. Gilts weakened from the open after weekend news of the Prime Minister’s chief of staff stepping down. The selloff intensified as Labour’s leader in Scotland publicly called on PM Starmer to resign, prompting concerns that any change in leadership could lead to looser fiscal rules and higher borrowing. At the intraday peak, 10 year gilt yields were more than +8bps higher and 30 year yields around +9bps, though both moves eased significantly after the full cabinet expressed support for the Prime Minister. Even so, UK markets lagged global peers, with the FTSE 100 (+0.16%) delivering only a modest gain.

What does Brooks Macdonald think?

Hassent’s comments were framed as part of a broader discussion around slowing population growth and improving productivity, rather than a warning about imminent weakness. However, markets remain cautious heading into tomorrow’s delayed January jobs report, given its potential influence on expectations for the Federal Reserve’s policy path. While one data point is unlikely to shift the overall narrative meaningfully, any moderation in job creation or wage growth could reinforce the case for a gradual cooling in labour market conditions.

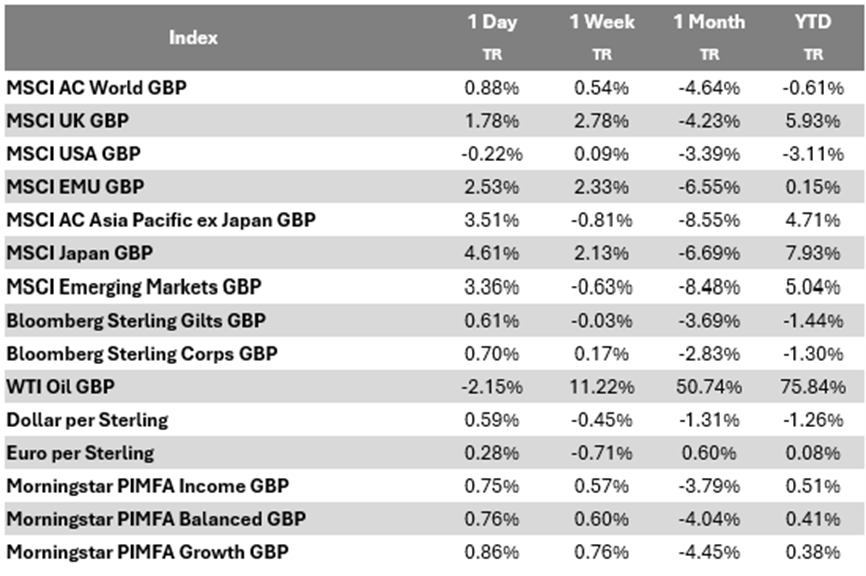

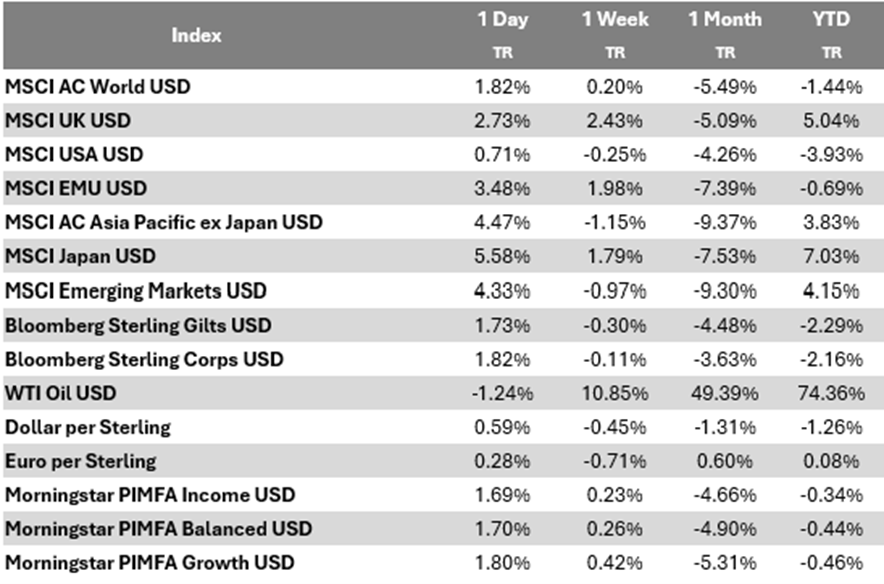

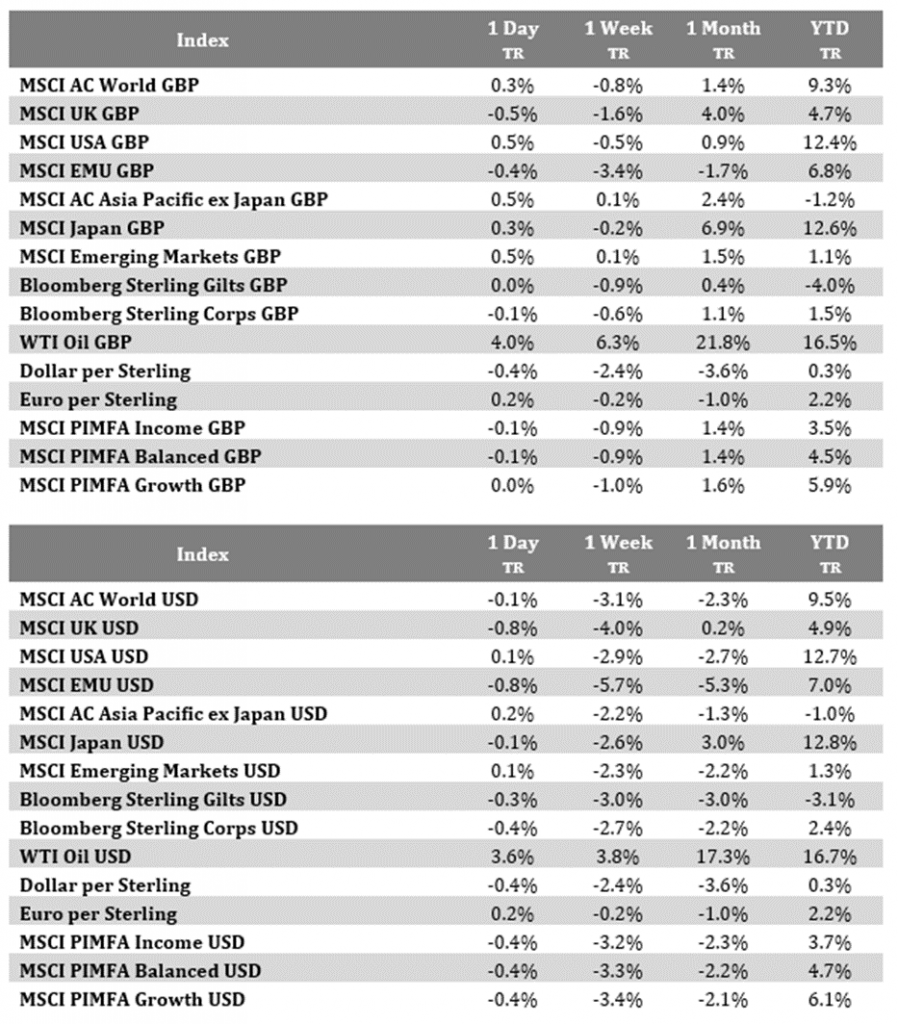

Bloomberg as at 10/02/2026. TR denotes Net Total Return.

Please continue to check our blog content for advice, planning issues and the latest investment, market and economic updates from leading investment houses.

Please see below the daily update article from EPIC Investment Partners, received this morning – 15/10/2025

Trade tensions remain elevated ahead of the planned meeting between President Trump and President Xi Jinping early next week. Toe to toe negotiations can be expected.

An interesting article from Goldman Sachs’ economists, recently published, is worthy of note. Elsie Peng and David Mericle suggest that the vast majority of tariffs increases will be borne by Americans, perhaps three quarters. Consumers are estimated to shoulder 55% of tariff costs while American business absorb a further 22%.

The pair estimate that foreign exporters would absorb just 18% of tariff costs by cutting pricing while 5% of tariffs will be evaded by one means or another.

Last year the United States was China’s largest export market accounting for roughly 15% of total exports but exports have fallen sharply this year. This has been more than offset by higher Chinese exports to other markets, especially the Global South.

Following the Irish famine of 1845, the following year Conservative Prime Minister Robert Peel, assisted by the Liberal Party, abolished high tariffs on imported grain which had protected British landowners.

This ended protectionism and ushered in an era of free trade which Britain, unchallenged on the seas, took full advantage of.

Please continue to check our blog content for advice, planning issues and the latest investment market and economic updates from leading investment houses.

Please see this week’s Markets in a Minute update below from Brewin Dolphin, received yesterday afternoon – 15/07/2025.

Global trade wars and UK growth concerns

U.S. market rallies amid global trade tensions and UK growth concerns.

Key highlights

Breaking new ground: The U.S. stock market has soared over 25% since 8 April, fuelled by President Trump’s tariff deferral, but uncertainty looms with new tariff plans.

Global trade tensions: Tariffs on Brazil, Canada, and copper imports highlight escalating trade tensions, raising costs for key industries and straining international relations.

Economic ripples: Weak UK GDP growth add to the clamour for lower interest rates in the UK, that in turn would be helpful for the public finances.

Market highs amid trade turmoil

The U.S. stock market has risen by over 25% since 8 April, reaching a new all-time high. The rally began when President Trump announced a deferral of the tariffs he had introduced on 2 April. However, the significance of this move seems to have been lost on President Trump, who remarked that he thinks the tariffs have been well received and noted the stock market’s record high.

These comments came in an interview with NBC, during which he floated the idea of imposing 15% or 20% blanket tariffs on “all the remaining countries.” It’s unclear which countries he was referring to. Some media outlets have speculated that he means replacing the baseline 10% rate with a higher rate of 15% to 20%. However, it seems more likely that he means those countries who had deferred tariff rates but haven’t received a letter. The latter explanation seems more plausible, as the Trump administration seems to have reached far fewer trade agreements than it had expected during the 90-day deferral period. Instead, most countries are expected to receive letters, some of which were sent out early last week.

However, by the start of this week, the majority of countries have neither received a letter nor reached a deal, and the 90-day deferral period has now expired.

Last week, additional punitive tariffs were announced on Canada and Mexico, with goods not already covered by the United States-Mexico-Canada Agreement (USMCA) now subject to 35% or 30% tariffs respectively.

Brazil attracted the president’s ire for pursuing a conviction against former President Bolsonaro. President Trump described the charges as a “witch hunt” and responded by imposing a 50% tariff on Brazil. Additionally, several other countries have received individual tariff letters. In most cases, these tariffs are close to the previous individual rates, although those rates were only in effect for a matter of hours before being deferred for 90 days.

The European Union continues to try and find a deal, but if it’s unsuccessful, President Trump announced that it would face a 30% tariff, an unusual 10%-point increase on the ‘Liberation Day’ rate.

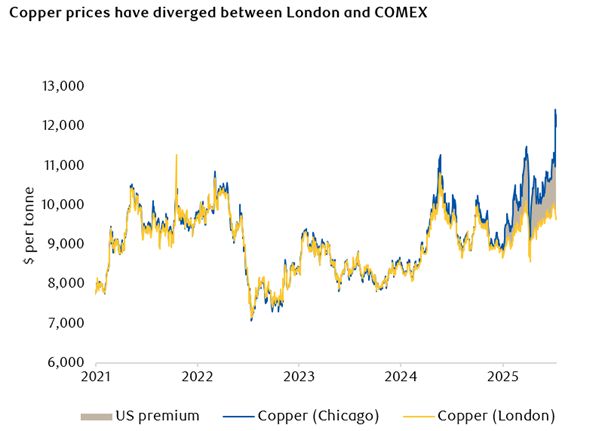

The president has also begun announcing the results of sector-specific tariffs, including a 50% tariff on copper imports. The U.S. currently imports roughly half the copper it needs, as domestic production has been declining. While the tariff could help to reverse that trend, it can take between five and ten years to bring a copper mine from conception to production. In the meantime, the copper import tax is expected to increase costs for U.S. industries such as construction, electronics, automobiles, renewable energy and data centres. The impact of this policy was immediately seen in the diverging price of copper in London and Chicago trading venues. Previously, the two prices were virtually identical, but since President Trump began discussing the possibility of a copper tariff, the two prices have diverged by 25%. While the gap should arguably be 50%, transportation costs for moving copper between markets account for part of the difference.

Copper prices have diverged between London and COMEX

Source: Bloomberg

Whether industry lobbying will be enough for the president to walk back these tariffs, as he has done several times this year, remains to be seen. This is certainly the expectation of the pharmaceutical industry, which has been threatened with a 200% tariff. The tariff is set to be introduced after a grace period of about a year to allow companies to shift their manufacturing to the U.S. However, there’s no way this will result in a meaningful increase in domestic drug manufacturing before it effectively triples drugs prices − an especially contentious issue at a time when the cost of medication is a major concern for voters.

The president, buoyed by calmer markets, appears emboldened to return to the policies which triggered market sell-offs in the first place. He may also have been influenced by criticism of the policies from other billionaires such as JPMorgan Chase CEO Jamie Dimon, who recently expressed concerns about market complacency regarding tariffs during an appearance on Fox News. Obviously, those investors who panicked last time will be wary of doing so again. The risks of getting whipsawed when the market is being driven by the president’s erratic decision making add yet another factor to an already complicated situation.

However, President Trump himself has pushed back against claims of erratic policymaking. Last week, he remarked “We don’t change very much and every time we put out a statement, they say he ‘made a change’… I didn’t make a change, [a] clarification maybe.”

UK starts to feel tax pressures

Source: LSEG

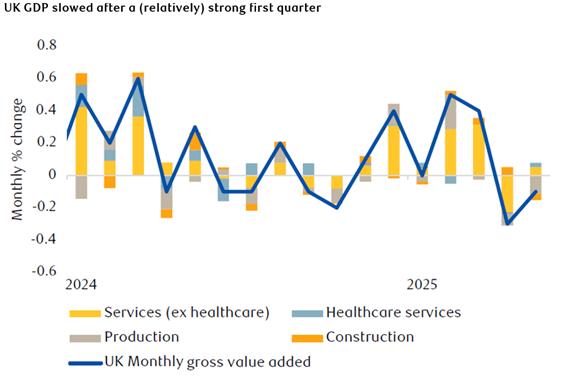

UK gross domestic product (GDP) data released this morning revealed that the economy contracted again in May, defying forecaster expectations of a rebound following April’s decline. UK GDP has been buffeted by a few forces. Tax increases in April, including a rise in National Insurance, contributed to the contraction, and will likely have a lasting impact. An effective increase in stamp duty pulled some housing transactions forward into the first quarter, while exports to the U.S. were also brought forward to get ahead of tariffs.

The UK economy has been slow to recover its momentum. June should be better, though, with positive momentum rebuilding in trade after the earlier shocks this year. Nonetheless, weak growth makes an August interest rate cut increasingly likely. Lower interest rates would be very welcome, as they play a large role in determining whether the public finances stay within the chancellor’s fiscal rules, or whether tax increases are needed this autumn.

Please continue to check our blog content for advice, planning issues and the latest investment market and economic updates from leading investment houses.

Please see below, an article from Tatton Investment Management, analysing the key factors currently affecting global investment markets. Received this morning – 14/07/2025

Trump turns nasty; markets turn nice

Markets were on summer holidays last week: volatility dropped and stocks broke all-time highs in local currency terms, thanks to abundant liquidity. However, nasty Trump is back and markets frayed a little as the negotiating tactic of increased tariff pressure played out. As we start this week, Europe and Mexico are under the cosh, as Trump threatens a 30% blanket rate in addition to unchanged sectoral rates. Economic Advisor Hassett told us that the US President sees current EU concessions as insufficient. The EU’s pause in imposing countermeasures may suggest faster progress but the German DAX40 futures were down about 1% as the week’s trading opened. The Euro edged lower against the US dollar by 0.25%.

Last week in the UK, the FTSE 100 broke another all-time high, but the media narrative was about inevitable tax rises. Without underplaying these, some of the rumoured figures (£20bn in hikes) look implausibly high. But a CGT hike is likely, which could cause some pre-emptive asset selling. But the impact on UK stocks will be limited by the fact that Britons don’t own much of their own market. UK bond investors will likely welcome a tax hike, ensuring fiscal discipline, lower growth, and hence lower interest rates (another expected next month). That’s hardly a rosy outlook, but it’s a stable one.

US monetary policy looks less stable, with rumours that Fed chair Powell could be ousted for the more Trump-friendly Kevin Hassett. Those rumours lowered US interest rate expectations, steepening the yield curve, due to both lower near-term rates expectations and higher long-term inflation expectations. Our preferred measure of government ‘credit risk’ moved up – not just for the US but everywhere. That bond move would normally hurt stocks, but investors instead saw it as a growth positive. Optimism was helped by improved US company earnings.

Optimism is also helped by abundant liquidity. CrossBorder Capital point out that the US treasury has injected around $400bn into the financial system in the last six months – via the reduction of its Treasury General Account (TGA). The TGA has fallen even lower than the pre-pandemic trend, partly due to US debt ceiling constraints. But US congress has just raised the ceiling and passed new tax cuts. Compared to the recent months, that will mean a less supportive liquidity flow from the US Treasury.

Investors might therefore be less optimistic. But at the same time, analyst upgrades to company earnings estimates show there is hard data to back up the positivity. We just hope growth signals are enough to support markets when they are less liquid.

Markets doubt copper tariffs

Donald Trump’s surprise 50% copper tariff sent US prices for the metal to record highs last week. The president announced the levy in an off-hand remark, but Treasury Secretary Howard Lutnick reiterated that it would take effect next month – and the episode sent US copper prices 17% higher in a single day. London’s copper futures came down (reflecting a loss of US demand) and the difference between the two rose to an astounding 25%. The fact the premium is less than 50% suggests that markets don’t believe the US – which imports around half of its copper – will totally follow through. The fact other markets didn’t react suggests copper prices could come down even more if and when Trump backs off.

The simple reason markets don’t buy it is because a 50% copper tariff would be extreme self-sabotage. Trump wants to build American industry and win the high-tech race with China – but those things need copper. Ironically, the smelters and refineries needed to expand the US copper industry need the raw metal too. Trump is no stranger to self-sabotage, of course, but the “TACO trade” would suggest that the threat of genuine economic harm will make the president relent.

If that logic doesn’t prevail, things could get nasty. Most tariffs are regarded as one-off cost shocks, but copper demand is structural – and a price hike now could have multiplier effects down the production chain. The threat alone has pushed up US copper prices in the short-term, and adds to the general sense that Trump is back to his disruptive ways, after a period of relative calm for markets.

It will be crucial to watch how this affects other tariffs. The optimistic view is that a blowback on copper weakens Trump’s hand elsewhere; the pessimistic view is that ‘nasty Trump’ is back.

Will China address its overproduction? Chinese producer price inflation (PPI) declined 3.6% year-on-year in June, a stark reminder of China’s deflation problems. Hopes that Beijing will respond with extra demand stimulus buoyed its markets on Friday, but nothing concrete has come through yet.

US tariffs don’t help Chinese deflation, but problems started long before Trump. Chinese companies have little pricing power and have been routinely slashing prices – so much so that the government has told businesses to stop. Consumer demand is weak, hurting company profits and hampering wages, feeding back into weak demand. The housing market never truly recovered from its crash years ago either, further sapping consumer confidence.

Beijing has been pursuing stimulus measures for nearly a year, but the impacts have been underwhelming. Its fundamental problem is that the Communist Party’s main lever for boosting growth – ramping up production – just makes the oversupply issues worse. Official growth numbers still show the economy reaching the 5% target, but that’s largely because of how production – the “P” in GDP – is counted. The factories are firing; people just aren’t buying what they produce. This isn’t to say the official figures are lying, but that the growth targets officials judge the economy against don’t always reflect how the economy feels for most people.

President Xi Jinping has prioritised stability over prosperity in recent years, but there are high-ups in China who are deeply concerned about deflation (as the crackdown on price-cutting shows). Rumours of deflation-busting measures were enough to push Chinese stocks and iron ore prices higher on Friday – as these rumours usually suggest someone is leaking a story.

There are also tentative reports that Xi’s authority might be waning (from total control to near-total control), after the politburo agreed rules on delegating some powers. That’s speculative, but it’s worth remembering that, since 1989, strong growth has been the party’s side of the social contract.

Please continue to check our blog content for the latest advice and planning issues from leading investment management firms.

Please see below article received from Brooks Macdonald this morning, which provides a global market update for your perusal.

What has happened

A good-but-not-great set of results from Nvidia on Wednesday evening plus more trade tariff comments from US President Trump in the past 24 hours collectively weighed on sentiment yesterday. The US technology megacap ‘Magnificent Seven’ group fell -3.03% on Thursday, with Nvidia down -8.48%. That pushed the US S&P500 equity index down -1.59% yesterday, and on course for its worst week since September, while the pan-European STOXX600 equity index dropped around -0.46%, all in local currency price return terms.

More Trump tariff headwinds for markets

Markets had to weather more Trump tariff headwinds on Thursday. Yesterday saw US President Trump announce an additional 10% trade tariff hike on China, as well as pushing ahead with 25% tariffs on Canada and Mexico, all due to be effective from Tuesday next week, 4th March. In addition, Trump said his plan for “reciprocal” tariffs on those countries that currently tariff US trade would still go ahead as planned in just over a month’s time on 2nd April.

A mixed US economic and inflation picture

Yesterday saw a second update on calendar Q4 2024 US economic growth and inflation. In the mix, US Gross Domestic Product (GDP) rose by an unrevised +2.3% quarter-on-quarter annualised – still a decent number versus the US Federal Reserve’s longer-run US economic growth estimate of +1.8%. However, as regards underlying inflation, according to the US Personal Consumption Expenditures (PCE) price index, core prices (excluding energy and food) rose to +2.7% quarter-on-quarter annualised, faster than the +2.5% initially reported and expected.

What does Brooks Macdonald think

Trump’s tariffs hold a stagflationary tilt-risk for markets, in that, at the edges, such trade levies would dampen economic growth, while buoying inflationary pressures. Of course, it is worth bearing in mind that we have potentially seen this movie before so-to-speak .. at the start of February, Trump’s proposed tariffs against Canada and Mexico were extended by a month with just hours to spare until they had been due to come into force. As the late British historian A.J.P. Taylor, who specialised in 19th and 20th century international diplomacy, reminds us, “nothing is inevitable until it happens.”

Bloomberg as at 28/02/2025. TR denotes Net Total Return.

Please check in again with us soon for further relevant content and market news.

Please see the below update from Evelyn Partners Investment Strategy team on today’s Bank of England MPC decision to continue to hold interest rates at 5.25%:

What happened?

The Bank of England (BoE) held the base rate at 5.25% at their meeting today. This was consistent with market expectations and marks the fourth consecutive meeting where rates have been held at this level.

Interestingly, the committee vote was split three ways, with two members voting for a hike, six voting to hold, and Swati Dhingra voting for a 25 basis point cut.

What does it mean?

As expected, the BoE held interest rates at 5.25%. Markets are now focused on when the Bank will cut interest rates and how far they will go. And perhaps Swati Dhingra’s vote to cut the base rate signals that the tide is set to turn. This was the first vote for a cut since the pandemic started almost four years ago. Although clearly this will continue to depend on the incoming data, which has been favourable since the Monetary Policy Committee (MPC) last met in December.

December CPI came in at 4.0% year-on-year, which was well below the Bank’s forecast of 4.6%. The headline figure was helped by services inflation, which was 0.5% percentage points below the Bank’s November forecast of 6.9% year-on-year. Similarly, the latest wage data shows further deceleration. The direction of travel seems encouraging, so much so, that the consensus forecast is that CPI will be 2.1% by the second quarter of this year.

The guidance published today by the MPC provided more hints on how they see the economic outlook. Compared to December’s guidance, the MPC dropped the language mentioning the risk of further interest rate tightening, signalling they are less concerned about inflation remaining stubbornly high. We also received the Bank’s latest forecasts. It expects GDP growth of 0.25% in 2024 and 0.75% in 2025. Similar to the consensus view provided in the Bloomberg survey of economists, the Bank sees inflation decelerating to 2% in Q2 2024, before it picks up again in the second half of the year.

This should give the Bank the ammunition it needs to cut rates around the middle of the year. Money markets are split on whether the base rate will be cut in May, but they have more conviction that we will see at least one cut by June. They are also pricing 100 basis points of cuts by the end of 2024.

Bottom Line

The BoE held interest rates at 5.25%. We expect to see the first rate cut around the middle of the year as inflation decelerates to the 2% mark.

Please continue to check our Blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.

Please see below, Brewin Dolphin’s ‘Markets in a Minute’ which provides a brief analysis of the key news from global economies. Received late yesterday afternoon – 14/11/2023

Stocks mixed on hawkish central bank comments

Stocks gave a mixed performance last week following hawkish comments from central bank policymakers.

After enjoying its longest winning streak in two years, the S&P 500 slumped on Thursday after Federal Reserve chair Jerome Powell said the central bank was not confident it had done enough to rein in inflation. A tech-driven rally on Friday helped the S&P 500 end the week up 1.1%.

Powell’s comments weighed on indices in Europe, with the Stoxx 600 slipping 0.1%. European Central Bank (ECB) president Christine Lagarde added to concerns about rates staying higher for longer, saying it would take more than the next couple of quarters for the ECB to start cutting rates. The FTSE 100 declined 0.8% after Bank of England governor Andrew Bailey said it was “really too early” to talk about cutting rates.

In Asia, China’s Shanghai Composite declined 0.6% after consumer prices fell in October, adding to concerns about the country’s economic outlook.

Investors await US inflation data

Stocks were mixed on Monday (13 November) as investors awaited the release of US inflation data on Tuesday. The Stoxx 600 rose 0.8%, the FTSE 100 added 0.9% and the S&P 500 edged down 0.1%. In economic news, figures from Rightmove showed new seller asking prices in the UK fell 1.7% this month, the largest November drop for five years. Nevertheless, Rightmove’s director of property science Tim Bannister said the year so far had been better than many expected, with new seller asking prices just 3% behind May’s peak.

The FTSE 100 was flat at the start of trading on Tuesday as figures from the Office for National Statistics (ONS) showed wage growth cooled slightly in the three months to September. Earnings excluding bonuses were 7.7% higher than in Q3 2022. This was a slight slowdown from 7.8% in the previous period, which was the highest since comparable records began in 2001.

UK economy stagnates in third quarter

As well as interest rate commentary, last week saw the release of some important pieces of economic data, including the latest UK gross domestic product (GDP) figures. The data from the ONS showed GDP was flat in the third quarter compared with the previous three months, following a 0.2% expansion in the second quarter. There was a 0.1% decline in services sector output, which offset a 0.1% increase in contraction sector output and broadly flat production sector output.

The 0% figure was in line with the Bank of England’s expectations and better than the 0.2% contraction forecast by economists. Flat growth means the UK has managed to avoid a recession this year, which is defined as two consecutive quarters of declining GDP.

Eurozone retail sales fall for third straight month

In the eurozone, the latest retail sales data continued to point to a weak European economy. Retail sales fell for the third consecutive month in September, declining by 0.3% from the previous month, according to Eurostat. An increase in sales of food, drinks and tobacco was offset by falls in non-food products and automotive fuel. The decline was worse than the 0.2% drop expected by analysts, although sales for August were revised up from -1.2% to -0.7%.

On an annual basis, sales were 2.9% lower than in September 2022. This was worse than the 1.8% year-on-year decline in August, but better than the 3.2% contraction forecast by economists.

US consumer sentiment drops to six-month low

In the US, consumer sentiment fell for the fourth-consecutive month in November, according to the University of Michigan’s preliminary consumer sentiment index. The headline index fell from 63.8 in October to 60.4 in November, the lowest level since May. The preliminary gauge of current conditions fell from 70.6 to 65.7, and the expectations index declined from 59.3 to 56.9. Joanne Hsu, the University of Michigan’s surveys of consumer director, said the decline was in part due to growing concerns about the negative effects of high interest rates, as well as geopolitical concerns.

The report also showed that year-ahead inflation expectations rose from 4.2% to 4.4%, the highest since April 2023, while long-run inflation expectations rose from 3.0% to 3.2%, the highest since 2011.

China’s consumer prices fall in October

Over in China, consumer prices fell in October, according to the National Bureau of Statistics. The consumer price index fell 0.2% year-on-year after being unexpectedly flat in September, underscoring the country’s fragile economic recovery since the pandemic. Food prices were the main culprit, with overall food prices down 4.0% from a year ago. Pork prices were 30.1% lower than in October 2022.

Meanwhile, producer prices declined 2.6% year-on-year, compared with a fall of 2.5% in September. The producer price index has now been in negative territory for 13 consecutive months.

Please continue to check our blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.

Please see below, Brooks Macdonald’s ‘Daily Investment Bulletin’ which provides a brief update on global investment markets. Received this afternoon – 28/09/2023

What has happened?

US bond yields continued their grind higher yesterday with the US 10-year Treasury yield now at 4.61% after another rise in oil prices stirred fears of a higher for longer inflationary backdrop. With these moves the US dollar has also been appreciating further, with the dollar index almost back to levels seen in November last year. US equities managed to stay flat for the day, but this conceals a high level of intraday volatility and general uncertainty.

Bond moves

Bond markets are certainly leading broader financial markets now with bonds seeing another heavy selloff yesterday. The Bloomberg aggregate global bond index, a widely used measure of the broad bond market, reached its lowest price level of 2023 as the benchmark 10-year and 30-year Treasury prices fell. These moves are quickly moving into the real economy with the US 30-year mortgage rate now at 7.41%, the highest level since December 2020. While the lag is relatively short, mortgage rates do act with a delay so there is likely further upside to these rates in the coming weeks. European bonds were also under pressure with 10-year bund yields hitting a 10-year high and Italian bonds underperforming after the Italian government unveiled a 4.3% expected deficit for 2024.

Oil Prices

The latest move higher in bond yields, which move inversely to prices, has been catalysed by growing inflation expectations caused by the uptick in energy prices. Brent crude closed above $96 per barrel yesterday, a fresh high for 2023. The US oil benchmark, WTI, saw an even greater percentage climb yesterday with the price moving to a one-year high of $93.68. While recent moves have been spurred by supply cuts, yesterday’s moves reflected lower-than-expected storage levels in the Cushing oil reserves.

What does Brooks Macdonald think?

Robust US economic data has been a key pillar of the soft-landing narrative in recent months however the recent consumer confidence data, and yesterday’s card spending data, suggests that the US consumer is showing signs of slowing. The US consumer discretionary sector has declined by almost 10% over the last fortnight as investors start to price in a heightened risk of a hard landing.

Please continue to check our blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.