Please see below for Blackfinch Group’s latest Monday Market Update Article, received by us yesterday 31/08/2021 due to the Bank Holiday:

UK COMMENTARY

Recruitment company Hays warned of “clear signs” of skills shortages worldwide and said hiring woes were pushing up wages in some hard-hit sectors. It also noted salaries are rising in certain industries as employers seek to attract and retain staff, particularly in the technology and life sciences sectors.

British car factories produced the fewest cars for any July since 1956 as they struggled with worker absences and the global shortage of computer chips. UK carmakers made 53,400 vehicles in July, a 37.6% drop when compared with July 2020, according to data from the Society of Motor Manufacturers and Traders (SMMT), the industry’s lobby group.

US COMMENTARY

The Chair of the US Federal Reserve (Fed), Jerome Powell, expressed concern about rocketing COVID-19 infections and was cautious on when it would start easing back on its stimulus programme. Powell’s remarks were far less hawkish than some Wall Street analysts had expected, and had a positive instant impact on the financial markets.

A new survey from the University of Michigan showed weakening US consumer confidence. Its consumer sentiment index fell from July’s final reading of 81.2 to 70.3 in August, the lowest recorded since December 2011.

EUROPE COMMENTARY

Rising prices, and the increase in COVID-19 cases, have knocked consumer confidence in Germany, the eurozone’s largest economy.

Figures released by Destatis showed that the German government’s efforts to fight the pandemic saw its budget deficit expand by €80.9bn in the first six months of 2021. That’s equal to 4.7% of GDP, and the highest reading since 1995.

ASIA COMMENTARY

Sentiment was weighed down by weaker-than-expected August Purchasing Managers’ Indices (PMIs) from China. The non-manufacturing PMI fell to 47.5, the first sub-50 reading since February 2020 (a sub-50 reading represents a contraction), which was below the 52.0 expected and down from 53.3 in July. Several factors were behind the slowdown, including further lockdowns to control the spread of the Delta variant, flooding in some regions, and ongoing regulatory changes that have impacted domestic wealth.

Please continue to utilise these blogs and expert insights to keep your own holistic view of the market up to date.

Please see below for Brooks MacDonald’s Daily Investment Bulletin received by us yesterday 19/08/2021:

What has happened

Markets spent much of Wednesday in a holding pattern ahead of the release of the Fed July meeting minutes. That changed when the minutes came out, as they showed that most officials looked to be favour of starting to taper bond purchases by the end of 2021. As a result, expectations around Fed Chair Powell’s speech next week at Jackson Hole will have gone up a notch or two, as investors await fresh clues on what a potential strategy for tapering might look like. After the release, US 10-year Treasury yields gave up the day’s gains of around 3bps to finish broadly flat at around 1.26%, but in early trade this morning, have traded lower, below 1.25%. US equities, already small down on the day, moved lower after the report was published, with cyclical and growth sectors falling in broadly equal measure. Overnight Asian markets are following Wall Street’s lead, trading lower this morning. Separately, Wednesday also saw the latest UK Consumer Price Index (CPI) data for July, which came in at 2% year on year, below June’s 2.5%, and below expectations of 2.3%. However, such is the ongoing distortion from base effects and reopening imbalances that neither the ‘transitory’ nor ‘sustained’ inflation camp was able to claim the advantage.

Fed releases its July meeting minutes

The release of Fed meeting minutes doesn’t normally get this much attention, but such is the focus around when the US Fed might look to start tapering its asset purchase programme. Regarding the subject of the taper, the minutes showed that ‘most participants noted that, provided that the economy were to evolve broadly as they anticipated, they judged that it could be appropriate to start reducing the pace of asset purchases this year.’ The committee also discussed the method by which to taper asset purchases, with most participants wanting to taper purchases of Treasury securities and Mortgage Backed Securities ‘proportionally in order to end both sets of purchases at the same time.’ Finally, the minutes showed members wanted to emphasise the decisions between tapering and rate hiking would be separate and not dependent on each other, saying that ‘participants indicated that the standards for raising the target range for the federal funds rate were distinct from those associated with tapering asset purchases’. This last point seemed to fit with comments earlier in the day on Wednesday from St Louis Fed President Bullard, who said that he preferred that tapering were finished by Q1 2022, and that Q4 2022 was a ‘logical place’ for interest rate hikes to commence.

US health officials announce plan for widescale COVID vaccine booster shots

US health officials including Dr Fauci, Biden’s Chief Medical Advisor, came out with a joint statement on Wednesday, saying that subject to final FDA (Food and Drug Administration) and CDC (Centers for Disease Control and Prevention) approvals, the US would recommend booster shots to all Americans who had received the Pfizer or Moderna vaccines. The outlined plan on Wednesday suggested an booster dose should follow eight months after the second dose, and that the booster doses could begin during the week of 20th September. The drive to offer booster shots has come because of the rise in delta variant cases, as well as signs that the vaccines’ effectiveness is falling over time. According to CDC Director Walensky on Wednesday, ‘our plan is to protect the American people, to stay ahead of this virus’. As for those who had received the single-dose Johnson & Johnson (J&J) vaccine, health officials suggested they might also need booster shots, but that they were awaiting more data, principally because the J&J vaccine rollout had started much later than the other vaccines.

What does Brooks Macdonald think

Vaccines remain the ultimate game-changer in the fight against the pandemic. With concerns of falling protection over time, booster shots have been expected, but the fact that the US has formalised a widescale plan around this should be positive for markets. The flip-side is that for every Pfizer or Moderna vaccine given as a booster, it is potentially one-less shot available for those in poorer economies who have yet to get their first or second shots. Reiterating this point, the WHO (World Health Organization) on Wednesday objected to the US plan on the grounds that it could exacerbate vaccine-inequality especially for relatively poorer countries globally. If that assessment is right, then it probably lengthens the odds of seeing a synchronised economic recovery globally.

Please continue to utilise these blogs and expert insights to keep your own holistic view of the market up to date.

Please see below for Legal & General’s latest ‘Asset Allocation Team’s Key Beliefs’ article, received by us late yesterday 28/06/2021:

There are still a few weeks until Q2 earnings season, but early indications point to mainly positive news when events kick off properly in July. In this week’s Key Beliefs, we also discuss the ‘meme’ stock phenomenon and whether the 1960s pose a historical parallel for inflation today.

We’re in the middle of pre-announcement season for corporate results. While this is always very anecdotal in nature, company comments have so far had a generally positive tone and, perhaps even more tellingly, there has been an absence of any high-profile negative pre-announcements. Results from early reporters, companies with different quarter ends, have had a similar positive tone.

Another positive indicator is that earnings revision ratios have stayed at exceptionally high levels. There are always fewer forecast changes by analysts in between earnings seasons, but from the data that have come in, there have been far more upward than downward revisions. In May and the first few weeks of June, more than three quarters of revisions in the US were to the upside, a figure only matched in the immediate aftermath of recessions and after the corporate tax cut at the end of 2017.

All of this bodes well for the upcoming earnings season and adds confidence to the view that we’ll see another round of significant upgrades to analyst forecasts in the summer. And of course, significant analyst upgrades either put upward pressure on share prices or downward pressure on valuation multiples. We believe the truth will likely lie somewhere in between and continue the pattern of equities grinding higher at a slower pace than earnings estimates, which gradually deflates the high PE (price to earnings) ratios of the immediate recession aftermath.

Retail is here to stay

Retail investors and ‘meme’ stocks have been centre stage again in equity markets in recent weeks. Three things come to mind on the topic from a macro perspective.

First, the extreme moves continue to be limited to a handful of stocks. There are still no obvious signs of the volatility in affected stocks spilling over into the wider market. If you look closely enough, you can see the gyrations of Gamestop* and AMC* reflected in the relative intraday performance of US small cap indices like the Russell 2000. But the S&P 500 put together a long string of daily moves smaller than 1% in the last period of meme stock volatility.

Second, this most recent rally in retail favourites has been far weaker than what we saw in spring. This applies both to the magnitude of the outperformance of the stocks involved and to retail trading volumes. The share of TRF volumes (seen as a proxy for retail activity) of overall US volumes has stayed in the low-mid 40% range, which is far above pre-2020 levels, but a good bit below the nearly 50% mark regularly reached earlier this year. Overall, it’s still fair to say that the froth that was apparent in several retail-driven niches of the market in spring is much less of a concern today. Indeed, SPAC (‘special purpose acquisition company’) activity and prices have dropped a lot, as have prices in the digital asset sphere, like bitcoin.

Finally, if retail is a growing part of equity flows, then we are still in the early part of this story. The activity has so far been concentrated in Robinhood-type investors, who tend to be younger and less wealthy than the traditional retail investor base. US households own just under a third of US equities, but the top 10% of households own almost all of that, according to Goldman Sachs. Private client flow data from brokers show net purchases of equities this year, but their magnitude still pales into insignificance when compared with the previous decade’s net selling. So far, the increase in retail activity appears to have been driven by the smallest section of retail investors. The private client flow data suggest activity is spreading to traditional retail investors, but from today’s perspective we believe this theme remains much more of an upside than a downside risk.

Sounds of the ‘60s

In the mid-1960s, after years of subdued core inflation, there was a sudden increase which began a period of prices ratcheting higher. Unemployment fell through the first part of the decade, but as soon as it reached 4%, both wages and inflation moved up significantly. This suggested the economy was overheating and unemployment had probably breached the NAIRU a couple of years earlier. Indeed, it took a recession in 1970 to halt wage and price pressures temporarily, before the oil-shock induced big inflation of the 1970s.

The simultaneous increase in wages and inflation is a finding consistent with Ram’s econometric work, which shows that neither wages nor prices tend to lead one another; the wage and inflation process seems to happen simultaneously. So, if we wait for wages to move materially higher, we could be too late in spotting the inflation outbreak.

But there were some unique features of the ‘60s:

The Vietnam war played a crucial role. US Federal spending (entirely on defence) shot up by over 1% of GDP from mid-1965 to early 1967. The deployment of over 300,000 more troops served to tighten the domestic labour market further. This episode shows it is not a good idea to add stimulus to an economy already at full employment. The stimulus today has been in response to a large amount of slack, with unemployment still relatively high and participation low. We expect the current labour market demand and supply imbalances to be resolved later this year, but there are some risks if Congress passes a large deficit-funded infrastructure package

Unionisation exacerbated the wage-price spiral. The labour market appears much more flexible today, aided by an increasing number of ‘digital nomads’ or ‘work anywhere’ jobs

In the ‘60s, the Fed had far less sophisticated understanding of the role of inflation expectations (there was no TIPS market) and was less independent. We are confident that the central bank will take appropriate action, should the current wave of inflation not prove transitory

The increase in prices was broad-based. This is a clear difference from today, where the median CPI is still behaving well

In 1966, England last won a major football tournament (though I’m still convinced that the ball never crossed the line on England’s winning goal). This time round, however, we’ll need to wait a few more days to know whether it’s a unique feature of the 1960s or not…

Please continue to utilise these blogs and expert insights to keep your own holistic view of the market up to date.

Please see below for one of AJ Bell Youinvest’s latest Investment Insight articles, received by us yesterday 21/03/2021:

New consumer research* by Opinium for AJ Bell shows Cash ISA savers are holding high levels of cash, and aren’t switching accounts looking for better rates, partly because they think they’re getting more interest than they probably are.

We know that since the start of the pandemic, many savers have been all cashed up with nowhere to go. But our research shows that cash hoarding isn’t just a recent phenomenon, it’s been happening for some time, and reflects a natural aversion to taking risk with money that has been hard-earned.

It’s definitely prudent to build up a cash buffer to deal with any unexpected costs, particularly in uncertain times. But Cash ISA savers may well be doing themselves a disservice by holding too much money in cash, opening themselves up to inflation risk, and missing out on the potentially higher returns available from investments. As stock market investors need to avoid irrational exuberance, so cash savers should be wary of excessive prudence.

Over the last ten years, the average Cash ISA has turned £10,000 into £9,770 after factoring in inflation, while in contrast, an investment in the global stock market has turned £10,000 into £20,760 in real terms.** Looking at returns from 1899, Barclays found that over ten years, UK equities have beaten cash 91% of the time. Given that today cash interest rates are at record lows, it would have to be an extremely anomalous decade for the next ten years to buck that trend.

Cash ISA savers aren’t shopping around for the best rate a great deal either. Much of their apathy can be attributed to ultra-low interest rates, but part of it may simply be that they haven’t checked the rate they’re getting. Our survey found that on average Cash ISA holders hadn’t reviewed their rate for two and a half years, over which time the average Cash ISA interest rate has more than halved, from 0.9% to 0.4%.

Not all rates move in step though, and individual savers can suffer as a result of their provider slashing rates more aggressively than the rest of the market, hence why it continues to make sense to shop around. For instance, last November, savers in NS&I’s Direct ISA saw their interest rate cut from 0.9% to 0.1%, while the best rates on the market are around 0.5%.

Even the top rates on offer aren’t exactly going to set pulses racing, but switching can mean hundreds of pounds extra for those with large amounts held in Cash ISAs. At the very least Cash ISA savers should find out what rate they’re getting right now, to make an informed decision on whether it’s worth moving on.

All cashed up and nowhere to go

Our survey shows Cash ISA savers reported holding on average £27,727 in their accounts. That’s enough to pay for 11 months of household expenses, which come in at £2,538 on average according to the ONS.*** When you consider that many households will contain two Cash ISA holders, and may also own other cash products like savings accounts and Premium Bonds, that suggests that savers have enough built up to deal with any emergency spending, and then some. On top of that, 6 out of 10 (59%) or respondents said they intended to add more to their Cash ISA in this tax year or next, no doubt in part thanks to the pandemic savings turbo-charging cash balances, as spending options have dried up.

While this is encouraging from the point of view of short term financial security, it does mean savers are sitting on cash for the long run, missing out on potential returns from other assets, and seeing the buying power of their cash eroded by inflation. Clearly there is a balance to be struck here between having a robust safety net, and seeking higher returns by investing in the stock market, which can lead to a loss of capital in the short term. Typically, savers should seek to have 3 to 6 months of expenses in cash to deal with any emergencies, beyond that they should seek to tilt the balance between security and return more towards the latter.

Three to six months of expenses equates to £7,613 to £15,226 for the average household, which may well have two Cash ISA savers in it. This broadly ties in with the view expressed by the FCA in December, that those with more than £10,000 held solely in cash were missing out on the historically higher returns from investing their money, and opening themselves up to inflation risk.****

There are some reasons why you might want to hold more than six months of expenses in an ISA, namely if you are saving for a specific goal, for instance a house deposit. This probably explains a surprising kink in the data, which shows that younger savers actually have more held in Cash ISAs than older generations.

Broadly speaking, if you think you may need access to your money within five years, then cash might be the best option. If you’re putting money away for five to ten years, then you should start to think about putting at least some of it in the stock market. If you’re putting cash away for more than ten years, then an approach that invests more heavily in the stock market is likely to yield significantly better results.

Cash ISA inertia

Cash ISA savers aren’t paying a great deal of attention to the rate they’re getting, and who can blame them, seeing as picking cash products right now is about selecting the least worst option. Our survey found that on average Cash ISA holders hadn’t reviewed their rate for two and a half years, over which time the average Cash ISA interest rate has more than halved, from 0.9% to 0.4%, according to Bank of England data. Worryingly, almost a quarter of Cash ISA savers (23%) said they hadn’t reviewed their cash ISA rate for 5 years or more. This goes some way to explaining why 25% of Cash ISA savers reported getting over 1% interest, which looks unrealistically high in today’s market.

Despite holding a Cash ISA for an average of 8.5 years, 45% of Cash ISA savers said they have never switched provider. Half of these savers said it was because rates were so low, it didn’t seem worth it. That’s perfectly understandable, though for those with large sums in Cash ISAs offering poor rates, the difference can still be significant.

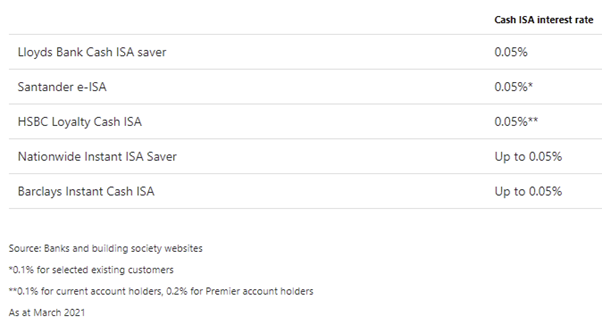

20% of Cash ISA savers said they held £50,000 or more in their Cash ISA. If they were picking up a high street rate of 0.1% (see table below) on £50,000, simply by moving to an account providing the average rate of 0.4% they could make an extra £150 a year. Not a king’s ransom, but worth having in your pocket rather than the bank’s. Particularly when you consider that at a rate of 0.1%, the total interest you are receiving is £50, and by moving to an account paying 0.4%, you would be quadrupling that amount to £200.

Selected high street instant access Cash ISA rates

Switching to a Stocks & Shares ISA

Half of Cash ISA savers surveyed (51%) said they had considered switching to a Stocks & Shares ISA. It used to be the case that you couldn’t cross the streams, but since 2014 you have been allowed transfer money from a Stocks and Shares ISA to a Cash ISA, and vice versa.

Doing so may be worthwhile if you feel you’ve got too much sitting in cash, earning next to nothing, and you’re willing to keep your money invested for the long term. You must be willing to tolerate falls in the value of your capital however, but the reward should be higher returns in the long run.

It’s important to always maintain a cash buffer for emergencies, three to six months of expenditure is the rough rule of thumb, but beyond this, you can start to think about investing in the market. Instead of transferring you might consider funnelling some of your new savings into a Stocks and Shares ISA, thereby gradually reducing your reliance on cash. Investing in the stock market bit by bit also helps to take the edge off the inevitable bumps in the road.

Please continue to utilise these blogs and expert insights to keep your own holistic view of the market up to date and for advice and planning tips.

Please see below up-to-date commentary from Brewin Dolphin, received late yesterday. The article provides insight into mixed market performance with Covid-19 and Brexit developments noted as current contributing factors.

Equity markets were mixed last week as markets struggled to gain traction amid a flow of (mostly) worrying news. There was the worsening second wave of Covid-19 in Europe and the announcement of tighter restrictions on socialising in the UK. Then, a potential hitch with the AstraZeneca vaccine, added to increasing worries of a no-deal Brexit. On the financial front, perhaps the most remarkable development was the 3.5% fall in sterling which likely helped the FTSE100 outperform its international peers over the past week.

Last week’s markets performance*

• FTSE100: 4%

• S&P500: -2.5%

• Dow: -1.66%

• Nasdaq: -4%

• Dax: +2.8%

• Hang Seng: -0.77%

• Shanghai Composite: -2.83%

• Nikkei: +0.86%

*Data for the week to close of business, Friday 11 September.

A mixed start to the week

Equity markets in the UK and Europe turned in a mixed performance on Monday despite encouraging news about the resumption of the AstraZeneca/Oxford University vaccine trials in the UK.

The FTSE100 closed 0.1% down on Monday and the more domestically focused FTSE250 rose by 0.7%. Sterling rose 0.76% against the dollar to $1.289, and by 0.42% against the euro to €1.085.

In Europe, the pan-European Stoxx600 gained 0.15%, the German Dax fell by 0.07% while France’s CAC-40 closed up by 0.35%.

In the US, however, the positive vaccine news from the UK helped boost sentiment, as the Dow closed up by 1.2%, the S&P500 rose by 1.27% and the Nasdaq rebounded by 1.87% to 11,056.65.

Analysts said hopes about an early vaccine were tempered by concerns about rising Covid-19 cases in the UK and Europe leading to tighter suppression measures, with a consequent dampening of economic activity.

In early trading on Tuesday morning, UK shares were heading up.

Brexit is back

The developments over the last week have suggested an increased risk of a no-deal departure. And just as in previous bouts of Brexit-related stress, the worse things go, the greater the pressure is on the pound. The fortunate thing from an investment perspective is that this tends to be supportive of UK bonds (which perform inversely to the UK economy), and also UK equities, because of their inverse sensitivity to the level of the pound. In other words, when the pound falls, all other things being equal, most UK equities rise.

This might seem counterintuitive, but the reality is that the sensitivity of even UK equities to the UK economy is generally low and mostly limited to a small number of sectors, such as retail, real estate, home construction and banks. More broadly, the overall market tends to be more exposed to the overseas currencies in which its revenues are denominated. For example, around 75% of the earnings for companies in the FTSE100 come from overseas and so are denominated in foreign currencies. Therefore, when the pound falls, these earnings are worth more in sterling terms and this helps UK equities.

Overseas equities, unsurprisingly, are even more inversely sensitive to the level of the pound as they are both denominated in foreign currency and economically linked to revenues received in other currencies.

Below we show the % change in trade weighted currency, the top graph shows 2015 to present and the bottom chart shows the period from 15 May 2020 to present.

What this means

All of which means that, ultimately, we don’t see Brexit as a material investment risk. Paradoxically, the greater issue for us is how to protect wealth when Brexit risks subside because, under those circumstances, we would expect to see the pound rise and bonds (and possibly equities) fall – again, all other things being equal.

So how do we see Brexit developing? It seems likely that the current standoff is another episode of the brinksmanship that has been exhibited throughout the last four years. The intention of the government is to pressure the EU into making some concessions on fishing and, most notably, state aid. Most outstanding issues between the EU and the UK seem reconcilable, but the state aid point is one the UK government seems to want to push. Why? It seems like the government wants to ensure it can do everything it can to support strategically sensitive industries such as technology and renewables. This idea of a “Made in UK” strategy to match the “Made in China 2025” strategy is what the European’s are afraid of. It seems likely that, when push comes to shove, the UK will be forced to find a way of discreetly backing down – but we can’t be sure.

Covid-19 developments

This also comes with an adverse trend in relative Covid-19 performance as well. America’s renewed surge in cases which began in the Midwest has failed to gather pace while some large states are seeing further improvement. Progress is not universal, however, and as we can see from Europe, a true second wave is likely in the US at some point. But for now, the US case growth numbers are improving which is helpful for Donald Trump as we approach the election in November.

Case growth in the UK, on the other hand, has accelerated. This prompted the government to impose new restrictions that came into effect from Monday to great consternation from the back benches. Evidence continues to point to Covid-19 as a continuing threat with the low rate of hospitalisations during France’s second wave now beginning to pick up. The concern here is that young people are spreading the virus amongst themselves and then introducing it to older generations of their families.

Covid-19 and your investments

Regarding the investment risks of a second wave of Covid-19, we believe that investors already expect successive waves until such time as there is a widely available vaccine. The question from an investor’s perspective therefore is not so much whether further waves come, but what the impact is on perceived valuations.

Understanding how the market reacts to that is not trivial. However, we should distinguish between what we saw in the early part of 2020 which was a shock, from what we might see in future periods, which will be more of an evolution of a known risk.

When we had the shock in March it was largely because the structure of the policy environment and the market were both set up for late-stage economic expansion. That is quite typical for the entry into a recession and is the reason that equity markets react so poorly to the onset of recessions.

On a valuation basis, the loss of a year or two’s worth of earnings is bad news but would not justify the falls seen earlier in the year – hence markets were able to rebound substantially.

With Covid-19 much more of a known-unknown, and with market expectations of ebbing and flowing regional measures to try and slow those waves, we acknowledge that Covid-19 remains an important factor for the market, but it should form part of the ‘wall of worry’ that markets often find themselves climbing.

Wall of worry

The cliché about climbing the ‘wall of worry’ describes the way in which markets are often resilient in the face of known risks. It assumes investors gradually become resigned to the fact that these issues will be resolved in due course and reflects the way in which the overly cautious gradually get sucked into the improving narrative. It is helped by such circumstances also tending to coincide with periods when monetary policy is very supportive.

One more handhold on that wall came from the news that the testing of AstraZeneca’s vaccine has been paused. Although one of the front runners, this was not the only candidate. However, over the weekend it emerged that the trial would resume in the UK and India, but it remains paused in the US.

Also providing a great deal of angst is the planned end to the furlough scheme next month. Chancellor Rishi Sunak is under a great deal of pressure from lobbyists and trade unions to extend the scheme further to prevent a “tsunami” of job losses this autumn.

An extension would not be without international precedent. Germany has announced an extension to its Kurzarbeit scheme, which gives financial aid to employers while allowing them to reduce employees’ hours. It had been scheduled to finish in March 2021 but has been extended for another year. France has also extended its version of the furlough scheme but has tweaked the rules so that employers must reduce hours for workers rather than keep them off work altogether. If the British government is going to follow suit, it is leaving it late.

We strive to update our blog content regularly in order to provide the most relevant and accurate data so please check in again with us soon.

Please see below for Invesco’s latest Investment Intelligence Update:

News flow last week, such as Non-Farm Payrolls and the ISM surveys in the US, was generally supportive of a positive tone in financial markets. “V” looks the shape of the recovery, for now at least. The virus news, however, remains mixed. New confirmed cases continue to roll over in the US, albeit still at elevated levels, while in Europe and DM Asia case growth remains relatively low, although it has risen in recent weeks. Case growth continues at elevated levels in Latin America. Central Bank dovishness remains very much the order of the day, with the Bank of England last week reiterating the uncertain outlook and the preparedness to do more if needed. Geo-political strains between the US and China refuse to go away, and in fact look as if they are escalating, while progress towards further US fiscal stimulus continues to frustrate.

Global equities hit their highest level since the bear market low during the week and are now back into positive territory for the year, now just 3% from their all-time high. Small caps and value/cyclical sectors led the way. In the UK further £ strength weighed on FTSE 100 relative performance, which dragged the All Share lower.

There was mixed performance in fixed income, with government bonds weaker at the margin, with the odd exception (Italy, EM). IG and HY continue to make progress. A new record low for yields for the former, while further declines in yields for the latter returned the asset class to positive territory for the year. Spreads for both still remain well above the lows seen earlier in the year.

The US$ halted its decline (see Chart of the week). Economic optimism helped boost economically sensitive commodity prices. China, the world’s biggest consumer of copper, saw record imports for the second straight month. Gold pushed to new highs as real yields declined to record lows and investor demand remained elevated.

Market performance last week (%)

Past performance is not a guide to future returns. Sources: Datastream as at 9 August 2020. See important information for details of the indices used.1

YTD market performance and YTD low (%)

Past performance is not a guide to future returns. Sources: Datastream as at 9 August 2020. See important information for details of the indices used.1

Chart of the week: US$ Index

Source: Datastream as at 8 August 2020.

One of the features of financial markets since the peak of the pandemic crisis dislocation in late March has been the weakness in the US$. In this chart we use the US$ Index (DXY) as a proxy for the currency’s performance (Fixed currency weights for DXY are Euro 57.6%, Yen 13.6%, £ 11.9%, Canadian $ 9.1%, Swedish Krona (SEK) 4.2% and Swiss Franc 3.6%).

At its YTD peak (late March) it had risen just under 7% on the back of its safe-haven, reserve currency characteristics and a shortage of US$ liquidity. Since then it has given up all those gains and more, declining 9.1% and now down just over 3% YTD. It is now at levels last seen in May 2018 and its 100-day decline has been the worst since November 2010. The major contributor to this weakness has been strength in the Euro (10.3%), given its high index weight, but other currencies have been stronger (SEK +18.7%, £ +11.1%). The Yen has been the weakest on a relative basis, but has still risen 4.6%.

Why has the US$ been so weak? A number of factors have contributed: the global rebound in growth has favoured more cyclical currencies, such as the Euro; an unwinding of safe-haven flows into the US$ on the back of this; real and nominal interest rate differentials between the US and another major markets have collapsed; aggressive Federal Reserve policy has alleviated US$ funding issues; fiscal and structural optimism in Europe on the back of agreement on the European Recovery Fund; the Federal Reserve and US government is happy to see a weaker currency; and finally, idiosyncratic US political and fiscal risk. All have weighed on a currency that on most measures was overvalued and where investor positioning was extended.

Can the US$ weaken further? Fundamentals are currently stacked up against the currency for now, but this is in the context where the DXY has moved from its most overbought level ever (relative to its 12m average) to its most oversold level since 1978. At the same time investor positioning (based on CFTC data) is now at a record short.

What does US$ weakness mean for financial markets? Historically it has benefitted global equites (and non-US stocks in particular), cyclical sectors, EM assets in general and commodity prices, such as Gold and Copper.

Key economic data in the week ahead:

A relatively quiet week ahead on the data front.

In the US there is July’s CPI reading on Wednesday. Headline inflation is expected to rise slightly to 0.7%yoy, off the pandemic lows, but still at the lowest level since 2015. Core inflation is expected to see a marginal decline to 1.1%yoy, its lowest level since 2011. The pandemic has been disinflationary. Initial jobless claims out on Thursday are forecast to show another 1.4m people receiving unemployment benefits, despite the better than expected Non-Farm Payroll data last Friday. Data on the strength of the US consumer is also out, with US retail sales for July published Friday and forecast to show a slowing recovery (1.9%mom vs 7.5%mom in June), while the preliminary reading of the University of Michigan Sentiment Index is expected to fall further and continue to hover around pandemic lows.

In the UK the most anticipated datapoint next week is the Q2 GDP release on Wednesday. If the forecasts of -20.5% prove right it would be the worst quarterly contraction of the UK economy on record. Broad-based weakness is expected, with the increase in government spending the only positive, depending on your point of view. Monthly GDP for June will also be released at the same time, which should show an underlying improving trend in the economy not seen in the quarterly numbers, with 8%mom forecast compared to May’s 1.8%mom. The latest UK unemployment report is published on Tuesday. The unemployment rate is expected to rise only slightly to 4.2% from 3.9% as the labour market continues to be underpinned by the government’s job retention scheme. The true health of the labour market will be seen away from the headline data in areas such as the number who are now economically inactive, hours worked and vacancy levels. These all point to higher levels of unemployment by year end, with the Bank of England’s Monetary Policy Report last week seeing it at 7.5%. Finally, there is July’s RICS house price data on Friday, which is expected to show a -5% drop in July, but up from -15% last month, highlighting the gradual improvement in the housing market in England and Wales.

China’s July data pipeline started last week and will continue throughout this week with figures on CPI (Monday) industrial production, fixed investment, retail sales, house price inflation and unemployment (all on Friday). Most indicators are forecast to post better readings than they did in June, suggesting that the third quarter is off to a relatively firm start.

Nothing of note during the week from either the EZ or Japan.

An insightful look into the markets by the experts at Invesco. These weekly updates are useful in terms of providing a regular overall view of the market.

Please use Invesco’s Investment Intelligence updates as well as our other blogs to refresh your view of current goings on in the global markets.