|

|

Please see below article received from EPIC Investment Partners this morning which provides an economic update for the UK ahead of the Autumn Budget on the 26th of November.

The UK economy is misfiring, posing a severe challenge for Chancellor Rachel Reeves ahead of the Autumn Budget. Latest data shows that growth slowed sharply to just 0.1% in Q3, with real GDP per head flat, confirming that the recovery remains weak and uneven. This sluggish performance leaves the UK lagging behind its G7 peers as it struggles with stubborn inflation, weak investment, and strained public finances.

The weakness is broad-based. Business investment fell by 0.3%, while consumer spending remains subdued amid the ongoing erosion of household purchasing power. The lingering effects of last year’s employers’ National Insurance rise continue to weigh on firms, while a temporary cyber-attack on Jaguar Land Rover significantly dragged down Q3 output, suggesting a one-off shock but not disguising the underlying fragility of the economy.

With unemployment now at a four-year high (5.0% in September) and inflation still running at 3.8%, nearly double the Bank of England’s 2% target, the BoE has held rates at 4.00% to maintain a tight stance against inflation. However, expectations are mounting for a December rate cut, with markets pricing in an ~86% probability following the latest weak GDP figures, contributing to renewed Sterling weakness against major currencies.

Amid this slowdown, the fiscal backdrop has darkened. Government borrowing reached roughly £100 billion in the first half of FY2025/26, pushing public sector net debt to around 95% of GDP. The Office for Budget Responsibility (OBR) is expected to downgrade productivity and fiscal headroom estimates, creating a “fiscal hole” of around £30 billion, and prompting warnings of a potential “doom loop”: the risk that fiscal consolidation to satisfy bond markets and control debt could further choke off already weak growth.

Faced with this dilemma, the Autumn Budget on 26 November will be a high-stakes balancing act. Reeves is boxed in by the need to restore fiscal credibility while supporting a faltering economy. While headline tax rates such as National Insurance, and VAT may remain unchanged, additional revenue could be raised through “fiscal drag”, the freezing of thresholds that quietly lifts the tax take as wages rise, and potential increases to income tax. Targeted spending cuts and the reprofiling of investment may also feature as the Treasury seeks to plug the shortfall.

The Budget’s success will depend on Reeves’s ability to rebuild confidence without stifling activity. With growth stagnating, inflation still elevated, and fiscal space narrowing, the UK finds itself on a tight policy tightrope, one misstep away from a deeper slowdown.

Please check in again with us soon for further relevant content and market news.

Chloe

13/11/2025

Please see below article received from Brooks Macdonald this morning, which provides a global market update for your perusal.

What has happened?

Yesterday, global markets faced headwinds, with the S&P 500 declining by 0.53% after three consecutive gains. Key pressures included escalating US-China trade tensions, disappointing corporate earnings, and concerns over a prolonged US government shutdown. The S&P 500 fell -0.53% with chip stocks leading the underperformance. The tech sector also faced scrutiny as Tesla kicked off the Mag-7 earnings season. Despite beating revenue expectations, Tesla’s earnings per share fell 31% year-over-year to $0.50, missing estimates due to rising operating expenses. Shares dropped 3.95% in after-hours trading. In Europe, the STOXX 600 fell 0.18%, reflecting a cautious mood. Meanwhile, oil prices surged, with Brent Crude climbing above $64/bbl following new US sanctions on Russia’s largest oil companies, marking a sharper tone in US-Russia relations since President Trump’s return to office.

US-China trade tensions continue

US-China trade concerns dominated market sentiment, driven by reports that the Trump administration is considering export restrictions on goods containing US software in response to China’s limits on rare earth exports. This news hit trade-sensitive sectors hard, with the Philadelphia Semiconductor Index dropping 2.36%. Despite the rhetoric, optimism flickered as Trump hinted at a potential comprehensive deal with China’s President Xi, suggesting negotiations remain fluid ahead of a possible summit.

UK markets shine

In contrast to global unease, UK markets rallied after a surprising drop in inflation. Headline CPI held steady at 3.8% (below the expected 4.0%), while core CPI fell to 3.5% (against forecasts of 3.7%). This fuelled expectations for a Bank of England rate cut, with the probability of a December cut rising from 42% to 72%. Gilts surged, with 2-year yields dropping 8.8bps to their lowest since August 2024, and 10-year yields falling 6.0bps. UK equities also gained, with the FTSE 100 up 0.93% and the FTSE 250 soaring 1.47%, its strongest performance in over six months.

What does Brooks Macdonald think?

The ongoing US government shutdown, now in its 23rd day, continues to cloud the outlook. The record for the longest shutdown was set in 2018-19, and Polymarket odds now indicating a 75% chance of surpassing that record. The lack of a resolution between Republicans and Democrats is stifling the flow of US economic data, leaving investors navigating in the dark. We remain vigilant, preferring opportunities in markets like the UK, where positive inflation data could point to improving outlook.

| Index | 1 Day | 1 Week | 1 Month | YTD | |

| TR | TR | TR | TR | ||

| MSCI AC World GBP | -0.39% | 0.70% | 1.70% | 11.61% | |

| MSCI UK GBP | 0.92% | 1.01% | 3.32% | 19.78% | |

| MSCI USA GBP | -0.56% | 0.55% | 1.03% | 7.52% | |

| MSCI EMU GBP | -0.49% | 0.70% | 3.15% | 26.21% | |

| MSCI AC Asia Pacific ex Japan GBP | -0.45% | 1.31% | 3.54% | 20.03% | |

| MSCI Japan GBP | 0.40% | 2.58% | 3.34% | 15.45% | |

| MSCI Emerging Markets GBP | -0.24% | 1.22% | 3.84% | 22.47% | |

| Bloomberg Sterling Gilts GBP | 0.53% | 1.08% | 2.76% | 4.36% | |

| Bloomberg Sterling Corps GBP | 0.41% | 0.71% | 1.99% | 6.11% | |

| WTI Oil GBP | 1.19% | 0.54% | -5.65% | -23.63% | |

| Dollar per Sterling | -0.11% | -0.35% | -1.17% | 6.71% | |

| Euro per Sterling | -0.19% | -0.03% | 0.47% | -4.81% | |

| MSCI PIMFA Income GBP | 0.19% | 0.63% | 1.83% | 9.89% | |

| MSCI PIMFA Balanced GBP | 0.15% | 0.64% | 1.87% | 10.81% | |

| MSCI PIMFA Growth GBP | 0.10% | 0.68% | 1.94% | 11.99% | |

| Index | 1 Day | 1 Week | 1 Month | YTD | |

| TR | TR | TR | TR | ||

| MSCI AC World USD | -0.41% | 0.55% | 0.67% | 19.21% | |

| MSCI UK USD | 0.91% | 0.86% | 2.28% | 27.94% | |

| MSCI USA USD | -0.57% | 0.40% | 0.00% | 14.84% | |

| MSCI EMU USD | -0.50% | 0.55% | 2.11% | 34.80% | |

| MSCI AC Asia Pacific ex Japan USD | -0.47% | 1.16% | 2.49% | 28.20% | |

| MSCI Japan USD | 0.39% | 2.43% | 2.29% | 23.30% | |

| MSCI Emerging Markets USD | -0.26% | 1.07% | 2.79% | 30.81% | |

| Bloomberg Sterling Gilts USD | 0.39% | 1.01% | 1.70% | 11.29% | |

| Bloomberg Sterling Corps USD | 0.27% | 0.64% | 0.93% | 13.16% | |

| WTI Oil USD | 1.18% | 0.39% | -6.61% | -18.43% | |

| Dollar per Sterling | -0.11% | -0.35% | -1.17% | 6.71% | |

| Euro per Sterling | -0.19% | -0.03% | 0.47% | -4.81% | |

| MSCI PIMFA Income USD | 0.18% | 0.48% | 0.80% | 17.37% | |

| MSCI PIMFA Balanced USD | 0.13% | 0.49% | 0.83% | 18.35% | |

| MSCI PIMFA Growth USD | 0.09% | 0.53% | 0.91% | 19.61% | |

Bloomberg as at 23/10/2025. TR denotes Net Total Return.

Please check in with us again soon for further relevant content and market news.

Chloe

23/10/2025

Please see below article received from EPIC Investment Partners this morning, which provides an update on emerging markets.

Investors are increasingly questioning whether ‘emerging markets’ should continue to be treated as an asset class. The term was coined by the World Bank back in 1981 as a more polite, or modern, term than The Third World.

From distant memory a country needed a per capita income below $10,000 to be considered emerging. Later frontier markets were identified, defined loosely as ‘generally smaller, less liquid, and less accessible than emerging markets.’

The question is whether it is appropriate to lump, say, Chile with Egypt or the UAE with Thailand or Vietnam with Argentina. The bland traditional definition seems outdated and arguably not fit for purpose. Greece was infamously downgraded to emerging market status in 2013.

Taiwan’s nominal GDP per capita for 2024 was $34,000 while GDP per capita in Purchasing Power Parity (PPP) terms is estimated to be around $82,600. Why is Taiwan still an emerging market? The only reasonable excuse is that foreign investors need to register and obtain a licence to trade local stocks.

The same applies to South Kora where GDP per capital is $36,000 while GDP per capita in PPP terms is estimated to be around $63,000. China remains an emerging market although nominal and PPP GDP per capita income stand at $13,000 and $25,000 respectively. The numbers for India are $2,700 and $12,100.

Local licences are required for all four markets.

The largest five markets in the MSCI Emerging Market Index are as follows: China 31.2%, Taiwan 19.4%, India 15.2%, South Korea 11.0%, and Brazil, 4.3%. Total 81.1%. Only Brazil and India more or less qualify within the traditional GDP per capita definition.

As investors, we are happy to run with the Asia ex Japan asset class which is also dominated by the four markets listed above.

Unfortunately, the markets across ASEAN (The Association of South East Asian Nations) have a tiny index weight – less than 1.5% each (with the notable exception of Singapore). These markets are not uninvestible by any means but passively managed products have little incentive to invest in the region.

Please check in again with us soon for further relevant content and market news.

Chloe

23/10/2025

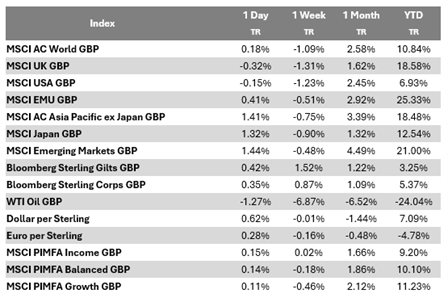

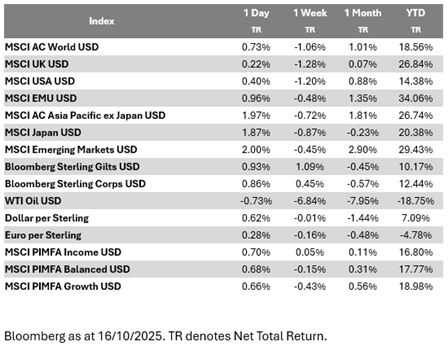

Please see below article received from Brooks Macdonald this morning, which provides a global market update for your perusal.

What has happened?

US equities closed mostly higher on Wednesday. The S&P 500 gained +0.40% and Nasdaq gained +0.66%. Banks and semiconductors led as the outperformers, while the big techs were mixed. Treasuries weakened slightly, contributing to some curve steepening. The dollar index dipped -0.3%, gold climbed +0.9% to surpass $4,200 per ounce, and WTI crude oil declined -0.7%. In Europe, markets were slightly positive with the STOXX 600 edging up +0.1%. The FTSE 100 and DAX both gained +0.2%.

Trump continues hawkish tone on trade

US Trade Representative Greer labelled China’s new rare earth export restrictions as a ‘global supply chain power grab’ and a breach of prior agreements. Treasury Secretary Bessent dismissed reports that Beijing is banking on Trump’s stock market focus to force concessions, emphasising that the US won’t negotiate under market pressure. He branded Chinese Vice Commerce Minister Li Chenggang as ‘unhinged,’ accused China of questionable supply chain practices, and announced plans for price floors in various industries to counter market manipulation. However, Bessent offered a glimmer of compromise: a longer pause on high US tariffs if Beijing delays its rare earth limits, potentially negotiable in the coming weeks. Trump has questioned the need for a meeting with Xi at the upcoming Asia-Pacific Economic Cooperation summit in South Korea, but Bessent indicated it’s still likely on.

Fed’s Beige Book reveals stagnant economy

The Federal Reserve’s latest Beige Book reported minimal change in economic activity since the prior period, with three Districts showing slight to modest growth, five unchanged, and four experiencing a slight slowdown. Employment remained stable, but labour demand was subdued, with more firms reporting layoffs. Prices continued to rise, accelerated by higher input costs, which are often linked to tariffs. Wages increased modestly. Consumer spending dipped slightly, especially on retail goods, though electric vehicle sales boosted auto demand. Lower- and middle-income households hunted for discounts, while high-income luxury spending stayed robust. District outlooks varied, blending improved sentiment with persistent uncertainty.

What does Brooks Macdonald think?

US-China trade frictions show no signs of easing. But there were some positive trade developments elsewhere, US-South Korea talks signal headway on a $350 billion investment pledge, while US-India relations warm with Trump’s praise for PM Modi and claims of Delhi halting Russian crude purchase. Closer to home, UK monthly activity expanded marginally in August as expected, though July’s figure was revised to a 0.1% contraction. In France, political drama unfolds with PM Lecornu facing two no-confidence votes—one from the far-right (likely to fail) and one from the left-wing bloc, whose outcome hinges on a few votes despite offered compromises to Socialists.

Please check in again with us soon for further relevant content and market news.

Chloe

16/10/2025

Please see below article received from EPIC Investment Partners yesterday, which provides an update on the US economy.

Concerns over the health of the US economy are mounting, driven by a sharp decline in sentiment, a softening labour market, and the disruptive reality of a government shutdown. These compounding headwinds suggest a period of economic caution, making a compelling case for defensive, undervalued, fixed income issued by the wealthy nations.

Recent data paints a clear picture of deterioration. The Conference Board’s US Consumer Confidence Index fell to a five-month low in September. Crucially, the measure of expectations for the next six months remains below the 80 threshold that has historically signalled a recession. This weak sentiment is rooted in job worries, with the gauge of present conditions dropping to a year-low and the difference between “jobs plentiful” and “jobs hard to get” narrowing to the smallest since early 2021.

The labour market is displaying notable weakness. The ADP National Employment Report for September was a major setback, showing private employers shed 32,000 jobs, with job creation losing momentum across most sectors. Furthermore, for the first time since the start of the pandemic, there are now more unemployed people in the US than there are job vacancies (job openings), suggesting that labour demand is cooling off. Compounding this, the grim official jobs report for August showed a mere 22,000 gain, with June being revised down to a loss of 13,000. These figures strongly suggest the economy is cooling rapidly.

Adding to the instability is the government shutdown, which introduces immediate economic drag. The Congressional Budget Office estimated the 2018/2019 partial shutdown reduced annualised real GDP growth by 0.4% in Q1 2019, while the 2013 lapse lowered growth by as much as 0.6%. The current shutdown, with threats of mass federal layoffs and disruption to services like E-Verify, will further erode confidence and hit private businesses; the 2013 shutdown cut an estimated 120,000 private-sector jobs.

This combination of weak consumer confidence, a softening labour market, and government instability creates an environment of elevated risk and uncertainty. In times like these, investors typically seek safety. Undervalued, high-quality sovereign and quasi-sovereign bonds like those held in the EPIC Fixed Income Strategy, become attractive. These assets offer capital preservation and predictable income in the face of economic turbulence, acting as a crucial defensive counterbalance to potential volatility in other asset classes.

Please check in again with us soon for further relevant content and market news.

Chloe

03/10/2025

Please see below article received from EPIC Investment Partners this morning, which explains the link between defense spending and the bond market.

The size of militaries

According to the World Population review China has the largest military with 2m people. India has 1.5m, the US and North Korea each with 1.3m, Russia 1.1m and Ukraine 730,000. When it comes to military spending power the US is dominant, accounting for 37% of the world total, three times the amount of China in second place.

Ukraine has the largest military in Europe because it is fighting a war. Russia is on a war footing. Both these economies are spending large proportions of their budgets on defence equipment and are increasing their weapon making capacities. China is building a large military capability to be able to intervene widely, with figures that may be understated. Germany, France, Italy, UK and Canada are all under pressure to increase spending as NATO members whilst Japan and South Korea are raising their budgets as allies of the US seeking to deter Chinese expansion.

In 2024 the US spent $1 trillion on defence, followed by China at $314bn and Russia at $149bn. All others were each under 9% of the US total spend. The US continues to lead in technology and development of new weapons, though China is now a serious rival with her own ability to innovate.

Defence shares have boomed on the back of planned expansion of budgets, with companies now needing to translate the increased order books into higher turnover and profits to justify the advances. Meanwhile bond markets are factoring in substantial increases in some defence budgets at a time when most countries need to cut their high deficits to reassure savers lending them money.

Defence budgets

The US, EU and UK are all embarking on further growth in their defence budgets. NATO has set a new target of 3.5% of GDP by 2035, with related expenditures on relevant national infrastructure at an extra 1.5%. Most countries will struggle with hitting these new targets.

The US President is seeking a 13% budget increase for 2026 over 2025. He wishes to strengthen US industrial capabilities to make weapons, improve US defences against missile and drone attack (Golden Dome), start the F-47 new fighter plane and improve nuclear capabilities. He is also scaling back the F-35 programme and demanding various efficiency improvements.

Germany is doing the most to increase its spending, starting from a low base and with a lower stock of state debt to GDP. The German government set up a €500bn fund to supplement annual defence spending over a period of years. The current German government removed the debt brake from borrowing needed to boost defence spending. As a result, it plans to raise spending to 3.5% by 2029, when it was only 1.4% in 2022. It plans €649bn over 5 years, ramping up from €86bn this year. It will continue to provide weapons to Ukraine.

France is very constrained by its excessive debts and large deficit. The President has recently announced his wish to increase the spending set out by the Loi de programmation militaire in 2026 and 2027. The budget allows modest growth in defence against a background of the last PM seeking overall budget cuts of Euro 43.8bn hitting welfare and the civil service. The defence increase is not helping get the budget through as the government seeks to confront the Parliament with the need to cut the deficit. Given the budget pressures there is not going to be much increase in the €53bn budget for defence, keeping it around 2% of GDP.

The UK has always stayed above the 2%. 23 out of 32 NATO states have now got to that level or above. The UK government plans to increase spend to 2.4% of GDP this year and 2.5% next year. It is leaving it until the next decade to get to 3% and above. Current plans see the £56.9bn budget of last year rising to £59.8bn this.

Deficits and bond issuance

The UK and US have to pay more interest on new borrowings than the Europeans or Japanese.

The UK has the highest long term borrowing rates as fears are more pronounced over the state of the national finances. The Chancellor raised substantial money in extra taxes last year in the budget, only to see the deficit go up again as a result of growth slowing and spending on welfare and public services rising by far more than the tax increases. With a policy for growth that depends on increased defence work, and a foreign policy based around the European wing of NATO taking on more responsibility for European defence and for assisting Ukraine, the government is having to look at other areas to cut back.

Germany with a lower debt to GDP is able to borrow more to pay for the shells. The USA continues to get away with a very high debt and deficit, and will be adding to it with extra defence, though seeking big cuts in some other areas like net zero policy. France is the most stressed of the major European economies, with a high debt and deficit. France has to pay considerably more to borrow than the Euro average given the budget risks. France will do the least to increase defence as a result.

Conclusion

The bond markets will continue to warn the UK and France that their governments need to take more action to rein in deficits. Both countries will find it is difficult to cut spending and will be looking to see what extra taxes they can impose without too much more damage to growth. Share markets have adjusted to the improved relative outlook for defence companies, whilst bond markets have made an understandable assessment of different levels of risk of budget strains. Both France and the UK have work to do to reassure more; while the US economy is slowing so it does allow rate cuts.

Please check in again with us soon for further relevant content and market news.

Chloe

25/09/2025

Please see below article received from EPIC Investment Partners this afternoon, which provides a global market update for your perusal.

“If you see a dam leaking, do not wait for it to burst,” goes an old engineer’s maxim. In financial markets, policy uncertainty often begins as a trickle such as minor skirmishes over tariffs or election rhetoric. But it can quickly flood asset prices. Recent research from the European Central Bank highlights how measures of economic policy uncertainty (EPU), drawn from news sentiment, spiked this spring following the US tariff announcement back in April. Yet volatility in both equities and bonds only rose sharply once that uncertainty fed through to weak equity market momentum.

This disconnect between policy noise and market choppiness is not new. Studies have documented long stretches (such as after the 2016 US election or during the energy crisis) when EPU surged but volatility stayed muted. ECB authors show that in Germany, EPU rose steadily into early 2025, driven by domestic fiscal questions and global trade tensions, yet equity‐market volatility diverged until the sudden sell‐off in April realigned the two. Additional academic work suggests that strong prior equity gains lull investors into complacency, suppressing implied volatility even as policy risk mounts.

Today, with autumn under way, policy uncertainty remains elevated on both sides of the Atlantic, from looming US elections to fractious EU budget talks. Yet headline VIX and VSTOXX readings trade near multi‐month lows, suggesting another potential mismatch. The danger is that a fresh shock arising from a market comment by a central bank governor or a sudden credit‐rating downgrade could trigger volatility clustering, where initial jitters cascade across asset classes.

For advisers, the lesson is twofold. First, recognise that EPU indices and realised volatility often co‐move only when equity momentum fades. Monitoring both news‐based uncertainty measures and market breadth indicators can flag when the dam’s wall is weakening. Second, tilt portfolios towards assets with negative sensitivity to broad volatility spikes. Low‐beta equities, inflation‐linked bonds and select investment‐grade credit historically outperform during clustered sell‐offs. A modest allocation to defensive sectors such as utilities or consumer staples can also cushion portfolio drawdowns when policy noise turns into market turbulence.

Ultimately, markets adapt by repricing risk. The real flood comes when leaks become uncontrollable, and those who built windmills rather than walls long before, will weather the storm more easily.

Please check in again with us soon for further relevant content and market news.

Chloe

09/09/2025

Please see below article received from Brooks Macdonald this morning, which provides a global market update for your perusal.

What has happened?

Markets delivered a robust performance over the past 24 hours, fuelled by soft US labour data that bolstered expectations for a Federal Reserve rate cut this month. Weaker labour market signals, including a disappointing ADP private payrolls report of +54k (vs. +68k expected) and initial jobless claims hitting a 10-week high of 237k (vs. 230k expected), underscored concerns following last month’s unexpectedly poor jobs report. The August ISM Services Index rose to 52.0 (from 50.1 in July). Prices paid component dipped slightly from 69.9 to 69.2, signalling persistent cost pressures. This backdrop drove a bond rally, with the 2y Treasury yield dropping to an 11-month low and the 10-year yield falling to a 5-month low. The S&P 500 gained +0.83% and the Magnificent 7 gained +1.31% hitting record highs, led by Amazon’s +4.29% surge after news of its AI-powered workspace software testing.

Fed independence under scrutiny

The Federal Reserve’s independence took centre stage yesterday during Stephen Miran’s Senate confirmation hearing for the Fed’s Board of Governors. Miran emphasised, ‘If confirmed, I will act independently, as the Federal Reserve always does.’ Questioned about retaining his CEA Chair role while serving as Governor until January, he clarified he would resign from the CEA if nominated for a longer-term Fed position. Meanwhile, news of a US Justice Department investigation into Fed Governor Lisa Cook for alleged mortgage fraud added uncertainty, as markets await updates on her bid for a court order to block potential dismissal.

Europe steadies ahead of French confidence vote

Across the Atlantic, French markets steadied as fears over Monday’s National Assembly confidence vote subsided. With a defeat widely expected, investor concerns about prolonged instability eased. French OATs outperformed, with the 10-year yield dropping 5.0bps to 3.49%, narrowing the Franco-German spread to 77bps, a recent low. The STOXX 600 rose +0.61%, reflecting cautious optimism in European markets.

What does Brooks Macdonald think?

As markets ride the wave of Fed rate cut optimism, today’s US Payrolls report marks the start of a pivotal two-week period that could shape global markets for the rest of 2025. Expectations are for August nonfarm payrolls to slightly outperform July’s figures, with the unemployment rate holding at 4.2%. However, revisions to prior months’ data will be crucial after last month’s significant downward adjustments (+19k for May, +14k for June), the largest in over five years, which led to the ousting of BLS chief Erika McEntarfer. The presumptive nominee, E.J. Antoni, awaits Senate confirmation this month. With US CPI next Thursday and the FOMC decision the following Wednesday, the labour market’s trajectory and inflation data will be pivotal in guiding the Fed’s next moves.

Please check in again with us soon for further relevant content and market news.

Chloe

05/09/2025

Please see below article received from EPIC Investment Partners this morning, which provides an interesting insight into potential investment opportunities in Chile.

Chile’s Atacama Desert, known for its extreme landscape and copper mining, is becoming a key location for green hydrogen production. The region’s high solar radiation provides an ideal resource for this clean fuel, which is made by using renewable energy to split water. This development could help Chile reduce its dependence on fossil fuel imports and create a new economic sector.

One significant development is the technology used to address the region’s dryness. While most green hydrogen projects use water-intensive electrolysis, some pilot projects are exploring different methods. For instance, the H2Atacama facility is testing a process that uses thermocatalytic solar reactors to extract atmospheric moisture and convert it into green hydrogen. This approach could reduce the need for large external water supplies or energy intensive desalination, which would be a practical advantage in an arid environment like the Atacama.

The economic potential of this industry is considerable. Government projections suggest that green hydrogen exports could reach a value of $30 billion by 2050, potentially becoming a major contributor to the national economy alongside the existing mining sector. Chile’s National Green Hydrogen Strategy aims to establish the country as a competitive producer and a top exporter within the next two decades. This vision is drawing international investment, with multiple projects already underway.

The growth of this sector will have broader benefits. It could create new jobs in technology and engineering, helping to diversify the economy. The use of green hydrogen in domestic industries, particularly in mining, could also contribute to lowering carbon emissions. By using hydrogen to power heavy equipment and processes, Chile will make its copper and other exports more sustainable. This is a critical step for a country that is a major global copper producer, and it is a direction the industry is already embracing.

The state-owned copper giant Codelco is a prime example of this transition. The company is not just a major player in Chile’s economy, but a key driver of its green mining initiatives. Codelco has committed to a plan to become carbon-neutral by 2050 and is actively investing in new technologies to meet these goals. For instance, it has commissioned a prototype of a hydrogen-fuelled mining vehicle, a first for Chile, that operates with zero emissions and only emits water vapor. Codelco is also transitioning to a 100% clean energy matrix to power its operations, with an ambitious goal to reduce its overall carbon emissions by 70% by 2030.

These efforts to decarbonise and innovate make Codelco a strong candidate for investment. The company’s strategic importance to the government, coupled with its strong market position and extensive mineral reserves, offers an attractive profile for investors. This is why Codelco is a long-standing name across the EPIC Fixed Income product range, with the longer-end bonds offering attractive risk-adjusted value and credit notch cushion. Moreover, a commitment to sustainability not only supports Chile’s national goals but also reinforces its long-term financial viability.

Please check in with us again soon for further relevant content and market news.

Chloe

02/09/2025