Please see the below article from AJ Bell received over the weekend:

Inflation has soared to a 10-year high and everyone is feeling the pinch, whether it’s in their weekly shop, their energy bills or when they’re heading out to buy a new car. But not everything has risen in price and some areas of our lives are getting pricier than others.

“The single biggest price rise of the year will dismay DIY fans or anyone working on a home renovation: MDF (or Medium-density fibreboard). The man-made wood has got 63% more expensive since the start of the year, as supply chain issues and a surge of people doing up their homes has put it in strong demand. And the biggest faller of the year? Computer games, which are a third cheaper than the start of the year, following a boom in demand during the pandemic that has died away now.”

Travel and transport

Car hire has soared in price, rising by 30% this year, shortly followed by air fares which have risen by 28% as more people hopped on a plane to get some sun. And anyone thinking of going on a jaunt to France will be shocked that EuroTunnel prices have risen 21% this year.

But if you’re willing to travel in the UK you’ll find costs haven’t risen that much, with coach fares actually falling by 24% and rail fares only rising by 3%, meaning a UK holiday could be much more affordable than setting your sights abroad.

Everyone knows that second-hand cars have been among the biggest risers this year, increasing by by almost 25% since January. But electric or hybrid cars haven’t seen the same increases, staying the same price across the year, meaning now could be a good time to go green. Adding literal fuel to this argument is that petrol prices have risen by more than 18% this year, while diesel prices have risen 17%.

Clothing

Now is not the time to be buying formal clothing and workwear, as it’s shot up in price after everyone realised they needed to upgrade their work wardrobes for the return to the office. If you’re pondering a new coat for Christmas you’ll need to dig deeper as a men’s coat has risen in price by more than a third, while a woman’s coat has risen by a more modest 15%.

But those still working from home and who didn’t max out on comfy clothing in the pandemic will find their clothes shopping is less pricey, as men’s jogging bottoms are 5% cheaper than at the start of the year, while women’s exercise leggings are 2% cheaper.

The food shop

The biggest price rise of all food items is fruit drink bottles, so things like Fruit Shoots, which are a staple in many parents’ weekly shop. A pack of them has risen 32% this year. The other biggest risers are a pack of yogurts, which is up 19%, and low-fat spread, which has risen 18%. It’s going to cost more to make a spag bol now, as tinned tomatoes have risen in price by 17%. As it’s not summer people might not be too disappointed that Magnums and other ‘chocolate-covered ice creams’ have risen by 13% in the year.

And the food item that’s fallen the most in price? Prepared mashed potato, which is down 13% on the year, followed by self-raising flour, which was hugely in demand during the pandemic, but people have now ditched their home-baking causing it to be more than 10% cheaper than the start of the year.

As for booze, wine drinkers have found the cost of their tipple increase, with new world red wine and European white wine up by 5% on the year, while a glass of plonk in the pub is up 4%. Beer drinkers haven’t been spared, with a pint of draught bitter or lager both up by 4%. But if you’re willing to ditch the pub for a beer at home, you’ll find a pack of lager has actually dropped in price by around 2%.

Christmas presents

Anyone wanting to buy the bookworm in their life some new material will find costs have shot up, with ebooks costing 23% more than last Christmas and hard-cover books rising by more than 20%. Even children’s books have shot up in price, up by 12%.

If you’re thinking of getting a new TV to watch the Christmas specials you’ll find they cost around 10% more than the start of the year, while the family Christmas board game is around 5% more expensive. But jigsaw fans can rejoice as they are 15% cheaper – once the hot ticket item to have in lockdown it appears their favour has waned a little. The same is true for smart speakers, which are 14% cheaper than the start of the year.

And sports fans will have found their weekly golf trip has got pricier, with golf balls getting 3% more expensive while green fees have shot up 19% in the year. But football players have fared better, with football boots staying the same price and the cost of an actual football rising by around 3%. But those wanting to get the new kit for Christmas will find prices have shot up, with official shirts being 19% more expensive than the start of the year.

Our Comment

These views should be taken in context. Please look at our other blogs that cover inflation as this is a topic we have been regularly posting about.

Rising inflation is currently a global trend due to high demand and issues with supply chains. These supply and demand issues along with rising energy prices are pushing prices up globally.

It may continue to rise in the short term before falling back but it is important to note that inflation is still viewed as transitory by Central Banks.

Please keep checking back for more updates on the current inflation situation, along with our regular content, including our ESG related content and economic updates from some of the world’s leading investment houses.

Please see below for Brooks MacDonald’s Daily Investment Bulletin, received by us late yesterday 21/10/2021:

What has happened

US and European equities continued their recent run of positive days with a small gain in the US leaving the index only a fraction away from its all-time high set in September. US earnings were, again, the driver of this upswing with around two-thirds of companies reporting yesterday beating expectations.

COVID-19

With the recent pickup in cases, headlines filtered through yesterday from across the globe. In Russia, President Putin has mandated a ‘non-working’ firebreak between the 31st October and 7th November whilst the Czech Republic has mandated the wearing of masks in indoor spaces. In New York City, municipal workers will need to show proof of vaccination to continue in their roles with the option of showing a negative test no longer available. Global governments appear to be taking one of two paths as cases increase in the northern hemisphere, either enacting restrictions now or doubling down on their vaccination/booster strategy. In the UK, weekly average cases have now risen to 45k per day with the Health Secretary yesterday urging citizens to register for vaccinations and for booster jabs ahead of the winter period.

Inflationary pressures

Whilst equities recorded another strong day yesterday, sovereign bonds remained under siege due to inflationary concerns. Oil prices hit another high for the year after reports from the US EIA pointed to falling inventories of both crude oil and gasoline. US 10 year inflation breakevens are now sitting at 2.6%, their highest level since 2012. Fed Speakers have been keen to push back against market expectations for interest rates, which are now running far ahead of the latest Fed dot plot from September. Fed Governor Quarles said yesterday that whilst he sees ‘significant upside risks’ to inflation, that his base case sees US inflation heading towards 2% next year. Quarles also addressed the elephant in the central bank room, saying that a demand/supply imbalance is not best addressed by curtailing demand via tighter monetary policy, describing such an approach as ‘premature’.

What does Brooks Macdonald think The market has fully priced in one rate hike in the US in 2022 with a second hike three-quarters priced in. The first step on the Fed’s monetary normalisation process will be the tapering of pandemic quantitative easing programmes so this will buy some time for the Fed to settle on the exact timing and pace of rate hikers, in the interim the Fed wants to avoid the market pricing in too rapid a tightening.

Please continue to utilise these blogs and expert insights to keep your own holistic view of the market up to date.

Please see the below article from Invesco received yesterday evening:

Key takeaways

Structural changes post-Covid are diminishing the global deflationary narrative

At the same time, a combination of fiscal and monetary largesse are providing a new inflationary force

We believe cyclically sensitive stocks and European stocks in particular could benefit from this new regime

One of the most significant top-down discussions impacting asset prices (bonds and equities) today is inflation: are we heading into a period of inflation or not? The debate has been rumbling since the policy reaction to the Covid pandemic but is now reaching fever pitch as we’ve seen the first above trend inflation data.

As European equity investors, we believe we must have a view. While it would be nice to simply claim that we’re ‘bottom-up’ and ‘fundamental’, the fact is we can’t ignore the polarisation in markets of the last decade, underpinned by monetary dominance and fiscal repression.

Duration (defensive/Quality) assets have benefitted from the low inflation period and short duration assets (cyclical/Value) have suffered. This part is straightforward to understand: medium-term inflation influences the risk-free rate (RFR) and it’s the RFR that the market uses to discount future cash flows. If expectations are for sustained low inflation, then the discount rate is low and asset prices rise and vice versa.

The problem is that forecasting medium-term inflation isn’t straightforward. Nothing causes normally amiable economists to become more tribal than asking them to explain the causes of inflation. In this article, we explain why we believe the arguments for transitory inflation are something of a distraction and point to areas of the market that could do well as mid-term inflation emerges.

Monetarists vs Keynesians and the case for transitory inflation

Monetarists can ‘prove’ inflation is a consequence of broad money growth while Keynesians will eloquently explain that as the demand curve shifts (to the right) faster than the supply curve, then prices rise.

Given we can’t even agree on the definitive cause of price moves then it’s not surprising there’s debate at any moment in time as to what the price moves might be.

The Monetarist vs Keynesian arm wrestle has, we believe, become more visceral since the global financial crisis (GFC) because excess money supply hasn’t led to significant inflation1. This has empowered the Keynesians to look for other rational reasoning of deflationary forces such as demographic trends (declining workforce), technology (increased productivity and labour marginalised) and globalisation (lower cost supply) with post crisis austerity the final straw.

Accordingly, when looking at the post-Covid world, Monetarists have less voice and the Keynesians argue these same three structural trends persist and, hence, any inflation we are seeing today is purely transitory.

This transitory narrative is a function of the severity of the enforced downturn which has impeded but, importantly, not destroyed supply (capital still exists). Therefore, as demand has recovered (surprisingly) fast, supply is temporarily struggling to cope and prices have risen, if only temporarily.

The effects have been exacerbated by the Suez blockage, lack of belly capacity in air transport, low inventories and even the weather in Texas.

If one believes that inflation is ‘only transitory’, logic dictates that it won’t impact the discount rates and therefore duration assets aren’t at risk and short duration cyclicality assets remain value traps….

Time to address the long-term deflationary narrative

The irony is that transitory inflation believers would likely claim to be long term and not worry about the short-term noise. However, we believe they’re perhaps missing the more fundamental structural changes happening post Covid.

We will try to outline why and in doing so will intertwine both economic theories, which we appreciate may anger more purist economists.

Firstly, we need to address some of the structural deflationary points:

Demographics. These are hard to argue with. European demographic trends are unhelpful albeit, net of migration, the data to 2019 suggest population is broadly stable. An aging population likewise doesn’t help. To us it remains an ongoing pressure but not incrementally so.

Technology. Often touted as a deflationary force. It increases productivity and hence pushes the supply curve to the right (we can produce more for lower prices). However, importantly, this is nothing new, innovation has been a relative constant over time. We also wonder if, in the post-GFC period, dominated by monetary policy, corporates were rewarded for ramping shareholder returns (dividends and buybacks) at the expense of investment and so exaggerated the deflationary impact.

Globalisation. We believe this is most contestable as a structural cause of deflation. Transferring production to Asia has undoubtedly been a key deflationary force for at least the past 20 years. China has been both a source of cheap labour and then, through policy, a source of excess production assets. In addition, at times of stress, China has devalued its currency, thereby easing inflationary pressures.

We strongly believe that it’s no longer so obvious. Reaction against the offshoring of US manufacturing jobs to China was a key source of Trump’s appeal. His firmly anti-China policy is one of the few policies the Biden administration has continued to pursue and, with China GDP set to rival the US by 2030, it is unlikely to stop being a vote winner. Within China itself, policy has shifted from emphasising the producer economy towards the consumer with some producing assets being forced to close.

This has been aided by Environmentalism being part of the domestic policy agenda. Lastly, it’s perhaps notable that despite strong domestic wage inflation, and the recent Renminbi appreciation, there’s been no talk of China devaluing – could China actually be exporting inflation?

We should also be aware of emerging market monetary policy setting being more traditional than developed markets currently – it’s developed markets running the largest ever deficits, while China tightens.

Figure 1. The Covid crisis will lead to further de-globalisation

The key point is that these structural deflationary forces, while still present, are a less powerful backdrop than we’ve become accustomed to. Meanwhile, there is the incremental risk from emerging inflationary trends.

Inflationary structural trends – are they here to stay?

Covid has changed voter tolerances, which in turn affects policy. This then has an impact on the economic backdrop and, ultimately, inflation risk.

We believe the true impact of the pandemic goes beyond headline fiscal payments, which are only as inflationary as the next cheque/infrastructure project, and more towards a change in what people truly care about and will vote for.

The post-Covid regime shift is happening to address the issues of Inequality and Climate Change. The vulnerability exacerbated by the health crisis is creating tolerance of big government. Unlike after the GFC, when the response to a financial crisis was fiscal austerity, today the electorate want fiscal dominance. The newly created EU recovery fund, worth €750 billion, is such an example.

Figure 2. Grants and loans from the EU recovery fund (in 2018 prices)

These, we believe, are inflationary forces. Big government is historically a poor allocator of resources compared to the private sector – it curtails supply (the British auto industry in the 1970s is a good example of this).Addressing inequality at a micro level means a greater share of stakeholder profits going to wages rather than to shareholders and management. This would direct resources to lower income earners who have a greater propensity to spend and therefore drive demand.

Inequality at a macro level means infrastructure projects and providing incentives to invest, thereby driving full employment and reducing social scarcity. Full employment as a policy is inflationary.

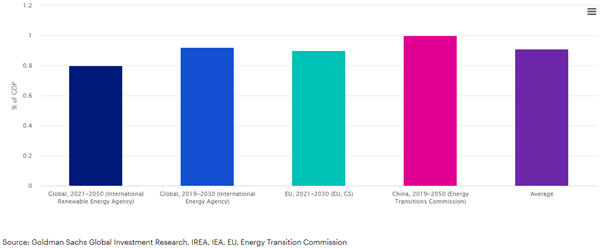

The climate agenda is a wrapper to digest the fiscal shift but it is also inflationary in its own right. Net neutrality requires capital investment: we need to build turbines, solar parks and transmission networks, which creates demand for physical assets.

Figure 3. A rise in green investment demand worth nearly 1% of GDP

However, we also need to build the infrastructure with renewable commodities meaning cement needs to be ‘green’ and steel needs to be low carbon. Some commodity producers will invest and take advantage, but others, previously running for cash, will be forced to close and hence we will finally see capacity come out of the market.

Consumers will be affected too with tolerance for higher prices (especially if wages are increasing) for greener products and replacement demand driven by policy – think replacing vehicles for hybrid or electric alternatives as internal combustion engine (ICE) cars are being banned from urban areas. This is inflationary.

Environmental policy is affecting capital availability already. Financial regulation means asset allocators need to disclose environmental data with the fastest growing asset class being ESG compliant funds.

These fund flows impact corporate capital allocation with environmental projects getting cheaper funding than brown projects. There simply isn’t cheap money available for coal, new oil or other environmentally challenging industries and, hence, over time, there will be a squeeze of supply. We know we are approaching peak oil at some point, however, what happens if peak supply comes first: prices rise – inflationary.

We believe there are some incremental inflationary forces at play, absorbing output gaps. These, combined with the perhaps abating ‘structurally’ deflationary forces will lead to net inflation, but on the condition of monetary complicity.

Monetarists believe money growth is key and MV=PT (or Money Supply times Velocity of money (rate of exchange)) is equal to Prices times Transactions. What does seem to be true is that without money growth, there’s no inflation. Simply because without new money, increased demand growth from, say, Government crowds out private sector demand and so net there’s no growth.

Importantly then, post-Covid, we have both fiscal dominance and monetary accommodation. Post-pandemic, broad money growth has been far greater than following the GFC and we also have a banking system that’s fully functional, i.e. neither deleveraging nor working out bad loans.

Monetary policy makers are shifting their mandate to remain accommodative for longer with targets of full employment and average “synchronised” inflation. This allows developed market central banks to stay ‘behind the curve’, meaning they do not feel the need to address the current inflation scenario.

There’s also consensus that central banks want fiscal cooperation in support of their tired monetary bazookas and will manage the interest costs through yield curve controls if required.

As per the Fischer equation, MV=PT, with ‘V’, the velocity of money, as the balancing item. The ‘V’ is probably best understood as how much the money in the economy changes hands. It has fallen over many years and fell more drastically post Covid as the saving rate has increased. However, we believe ‘V’ will increase as economies unlock, the savings rate falls and inequality falls (lower incomes have a lower propensity to save).

With abundant liquidity meaning banks will be able to lend (even as savings are reduced), central banks printing money and velocity increasing, then prices will rise: inflation.

Transitory inflation is just a distraction – cyclical stocks and Europe set to benefit

We believe that arguing about the short-term transitory inflation numbers misses the key point. Yes, short-term inflation is spiking because of bottle necks. However, asset prices are based on mid-term inflation forecasts, not crisis-related data. Therefore, it’s mid-term inflation we need to think about.

It’s our strong belief that mid-term inflation will be sustained at above central bank targets, albeit not rampant. Indeed, inflation-linked bonds are signalling as much. Yet, the ongoing polarisation of the equity market with preference for long duration and growth equities would suggest something different.

In our view, from a top-down perspective, the types of companies that could benefit from nominal growth are the short duration equities and these are the cheapest parts of the market. We believe they are cheap hedges to the mid-term inflation risk that we have argued for above.

In addition, from a bottom-up perspective, it’s the same sectors and companies that will be a direct beneficiary of the political shifts we’ve mentioned. The environmental agenda is pro-investment; it’s pro-cyclicality.

Companies in industries exposed to construction materials, utilities, automotive OEMs and even banks through volume growth, all might benefit. These are also where currently the most compelling valuations are.

Likewise, the impact from more re-balancing of stakeholder profit shares and fairer taxes with bigger government are less onerous on European companies. This is simply because they have been operating under a more egalitarian environment for longer than other global regions.

Generally, equities are owned with the aim of protecting you from inflation. However, many portfolios that have outperformed over the last decade, and more, have been ones that have benefited primarily from a lack of inflation – so one composed of bonds and long-duration/growth equities.

As we move into a new regime of inflation for the reasons argued, in our view, this type of portfolio is unlikely to do so well. On the contrary, our valuation discipline has resulted in our fund ranges being exposed to short duration or cyclical stocks, which we believe are well positioned in the more inflationary backdrop we have outlined.

Please see the below article from Invesco received late yesterday afternoon:

Key takeaways

The Fed does not have a trigger finger

Just because the Fed reacts negatively to a data point doesn’t mean it’s going to tighten monetary policy at its next meeting.

Some inflation is expected

Time and again, Fed officials have warned that a spike in inflation is likely as the US economy re-opens.

The Fed’s approach has changed

The Fed has gone through a paradigm shift when it comes to inflation targeting.

Last week, investors shuddered as data showed a big rise in prices in the US and a greater-than-expected rise in prices in the eurozone. Stocks sold off, US Treasury yields climbed higher, and market pundits obsessed over inflation. I feel it’s important at this juncture to remind investors of a few truths surrounding inflation and the Federal Reserve.

1. The Fed does not have a trigger finger

Just because the Fed reacts negatively or says it’s surprised by one or more data points doesn’t mean it’s going to tighten monetary policy at its next meeting. Some investors were taken aback by Fed Vice Chair Richard Clarida’s comments last week when he said he was surprised by some recent data points such as the Consumer Price Index, which was much higher than he expected. However, he was quick to reassure: “Honestly, we need to recognize that there’s a fair amount of noise right now, and it will be prudent and appropriate to gather more evidence…” Don’t forget that the Fed’s new catch phrase is “patiently accommodative.” In other words, the Fed is going to err on the side of accommodation and is likely to deliberate extensively before tightening.

2. The Fed anticipates a spike in inflation as the economy re-opens

At a Wall Street Journal conference in early March, Fed Chair Jay Powell explained that, “We expect that as the economy reopens and hopefully picks up, we will see inflation move up through base effects. That could create some upward pressure on prices.” In fact, time and again, Powell and other Fed officials have telegraphed that a spike in inflation is likely as the US economy re-opens. The Fed is ready and accepting of that rise in inflation.

3. We won’t know any time soon if the increase in inflation is temporary or persistent

A temporary rise in inflation is at least partially the result of base effects — in other words, the comparisons to a year ago look distorted given what poor shape the economy was in last spring as the pandemic took hold. In addition, there is currently a mismatch between supply and demand which can drive up prices — think of the supply chain issues that are being experienced right now in some industries and the pent-up demand that is now being exercised as economies re-open. However, these are likely to create only temporary inflation. After all, how many flights can you take and haircuts can you get once the economy re-opens? Clearly, the law of diminishing marginal utility suggests that at a certain point, satisfaction with each additional flight or haircut is reduced.

Now, there are forces that can lead to more persistent inflation. Typically wage increases lead to “stickier” inflation. We have not yet seen a significant rise in average hourly earnings in the United States, and it seems unlikely that will happen quickly given the very substantial amount of labor market slack.

Monetarists would argue that it all comes down to money supply; a significant increase in money supply can spur persistent inflation, and right now we have seen a very significant increase. However, one other key ingredient is usually present as well: an increase in the velocity of money, which we have not yet seen. The quantity theory of money posits that inflation is not just a function of money supply but also the velocity of money. As the St. Louis Fed explained in a brief research note, “If for some reason the money velocity declines rapidly during an expansionary monetary policy period, it can offset the increase in money supply and even lead to deflation instead of inflation.” But even if a money supply increase is enough to spur persistent inflation, this would not occur immediately — it usually occurs with an 18-24 month lag, suggesting we may not see it until late 2021 or early 2022.

4. The Fed’s inflation targeting policy represents a paradigm shift for the Fed

The Fed has gone through several paradigm shifts in the last several decades, and they’ve been transformational. I’m old enough to remember when the Fed didn’t believe in regular communication with the public, when the size of then-Fed Chair Alan Greenspan’s briefcase was the best indicator of what the Fed’s decision on rates would be at the next Federal Open Market Committee (FOMC) meeting. And now of course, the Fed is extremely transparent, working hard to telegraph its views and actions before taking them. Similarly, the Fed had a very different inflation targeting policy before last summer. Its current policy, called Average Inflation Targeting (AIT), means that the Fed’s objective is to push inflation enduringly above 2% and attain full employment before considering tightening. In other words, this new policy enables the Fed to be far more flexible and essentially tolerate economic overheating. This is NOT the Fed of yesteryear, which believed that its role was to take away the punch bowl just as the party was getting started. This Fed might leave out the punch bowl into the wee hours, even as partygoers get drunk.

What does this mean for investors?

This begs the question: what are investors afraid of? Are they afraid of inflation — or the Fed tightening in reaction to inflation? It seems to me that they are far more worried about the latter than the former. That would explain why last week’s negative reaction to signs of inflation was so very short-lived, as Fed officials provided reassurance. And so perhaps investors should be more concerned about the former, especially if the Fed remains “behind the curve” and is unable to easily tame inflation once it tries to. While I must stress that this is far from my base case scenario, it is a risk that needs to be considered since inflation can have a negative impact on some asset classes. If persistently higher inflation were to occur, investors could benefit from exposure to commodities, cyclical stocks, inflation-protected securities, emerging market assets and even dividend-paying stocks as part of a diversified portfolio.

This week there is more potential for volatility, as investors wait with bated breath for the FOMC minutes, which could offer more insight into what the Fed is thinking with regard to inflation and tightening.

Our Comments

The markets are still volatile at the moment but are generally on an upwards trend as you can see from the below chart of the FTSE 100 over the past year:

Source: Google, as at 16:35 BST 19/05/2021

Global markets are increasingly more interconnected and US inflation fears affects the UK markets (and vice versa).

Inflationary fears will continue as will the volatility however as we always state, its important to remain calm and ride the volatility out.