Please see below for Blackfinch Group’s latest Monday Market Update Article, received by us yesterday 31/08/2021 due to the Bank Holiday:

UK COMMENTARY

Recruitment company Hays warned of “clear signs” of skills shortages worldwide and said hiring woes were pushing up wages in some hard-hit sectors. It also noted salaries are rising in certain industries as employers seek to attract and retain staff, particularly in the technology and life sciences sectors.

British car factories produced the fewest cars for any July since 1956 as they struggled with worker absences and the global shortage of computer chips. UK carmakers made 53,400 vehicles in July, a 37.6% drop when compared with July 2020, according to data from the Society of Motor Manufacturers and Traders (SMMT), the industry’s lobby group.

US COMMENTARY

The Chair of the US Federal Reserve (Fed), Jerome Powell, expressed concern about rocketing COVID-19 infections and was cautious on when it would start easing back on its stimulus programme. Powell’s remarks were far less hawkish than some Wall Street analysts had expected, and had a positive instant impact on the financial markets.

A new survey from the University of Michigan showed weakening US consumer confidence. Its consumer sentiment index fell from July’s final reading of 81.2 to 70.3 in August, the lowest recorded since December 2011.

EUROPE COMMENTARY

Rising prices, and the increase in COVID-19 cases, have knocked consumer confidence in Germany, the eurozone’s largest economy.

Figures released by Destatis showed that the German government’s efforts to fight the pandemic saw its budget deficit expand by €80.9bn in the first six months of 2021. That’s equal to 4.7% of GDP, and the highest reading since 1995.

ASIA COMMENTARY

Sentiment was weighed down by weaker-than-expected August Purchasing Managers’ Indices (PMIs) from China. The non-manufacturing PMI fell to 47.5, the first sub-50 reading since February 2020 (a sub-50 reading represents a contraction), which was below the 52.0 expected and down from 53.3 in July. Several factors were behind the slowdown, including further lockdowns to control the spread of the Delta variant, flooding in some regions, and ongoing regulatory changes that have impacted domestic wealth.

Please continue to utilise these blogs and expert insights to keep your own holistic view of the market up to date.

Please see below for Brooks MacDonald’s Daily Investment Bulletin received by us yesterday 19/08/2021:

What has happened

Markets spent much of Wednesday in a holding pattern ahead of the release of the Fed July meeting minutes. That changed when the minutes came out, as they showed that most officials looked to be favour of starting to taper bond purchases by the end of 2021. As a result, expectations around Fed Chair Powell’s speech next week at Jackson Hole will have gone up a notch or two, as investors await fresh clues on what a potential strategy for tapering might look like. After the release, US 10-year Treasury yields gave up the day’s gains of around 3bps to finish broadly flat at around 1.26%, but in early trade this morning, have traded lower, below 1.25%. US equities, already small down on the day, moved lower after the report was published, with cyclical and growth sectors falling in broadly equal measure. Overnight Asian markets are following Wall Street’s lead, trading lower this morning. Separately, Wednesday also saw the latest UK Consumer Price Index (CPI) data for July, which came in at 2% year on year, below June’s 2.5%, and below expectations of 2.3%. However, such is the ongoing distortion from base effects and reopening imbalances that neither the ‘transitory’ nor ‘sustained’ inflation camp was able to claim the advantage.

Fed releases its July meeting minutes

The release of Fed meeting minutes doesn’t normally get this much attention, but such is the focus around when the US Fed might look to start tapering its asset purchase programme. Regarding the subject of the taper, the minutes showed that ‘most participants noted that, provided that the economy were to evolve broadly as they anticipated, they judged that it could be appropriate to start reducing the pace of asset purchases this year.’ The committee also discussed the method by which to taper asset purchases, with most participants wanting to taper purchases of Treasury securities and Mortgage Backed Securities ‘proportionally in order to end both sets of purchases at the same time.’ Finally, the minutes showed members wanted to emphasise the decisions between tapering and rate hiking would be separate and not dependent on each other, saying that ‘participants indicated that the standards for raising the target range for the federal funds rate were distinct from those associated with tapering asset purchases’. This last point seemed to fit with comments earlier in the day on Wednesday from St Louis Fed President Bullard, who said that he preferred that tapering were finished by Q1 2022, and that Q4 2022 was a ‘logical place’ for interest rate hikes to commence.

US health officials announce plan for widescale COVID vaccine booster shots

US health officials including Dr Fauci, Biden’s Chief Medical Advisor, came out with a joint statement on Wednesday, saying that subject to final FDA (Food and Drug Administration) and CDC (Centers for Disease Control and Prevention) approvals, the US would recommend booster shots to all Americans who had received the Pfizer or Moderna vaccines. The outlined plan on Wednesday suggested an booster dose should follow eight months after the second dose, and that the booster doses could begin during the week of 20th September. The drive to offer booster shots has come because of the rise in delta variant cases, as well as signs that the vaccines’ effectiveness is falling over time. According to CDC Director Walensky on Wednesday, ‘our plan is to protect the American people, to stay ahead of this virus’. As for those who had received the single-dose Johnson & Johnson (J&J) vaccine, health officials suggested they might also need booster shots, but that they were awaiting more data, principally because the J&J vaccine rollout had started much later than the other vaccines.

What does Brooks Macdonald think

Vaccines remain the ultimate game-changer in the fight against the pandemic. With concerns of falling protection over time, booster shots have been expected, but the fact that the US has formalised a widescale plan around this should be positive for markets. The flip-side is that for every Pfizer or Moderna vaccine given as a booster, it is potentially one-less shot available for those in poorer economies who have yet to get their first or second shots. Reiterating this point, the WHO (World Health Organization) on Wednesday objected to the US plan on the grounds that it could exacerbate vaccine-inequality especially for relatively poorer countries globally. If that assessment is right, then it probably lengthens the odds of seeing a synchronised economic recovery globally.

Please continue to utilise these blogs and expert insights to keep your own holistic view of the market up to date.

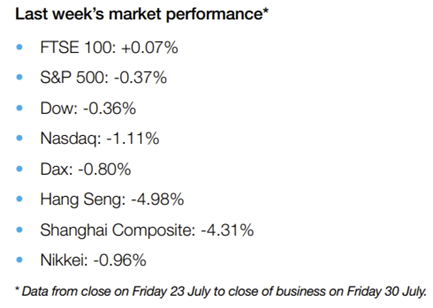

Please see below for Brewin Dolphin’s latest ‘Markets in a Minute’ article, received by us yesterday evening 03/08/2021:

Global equities were mixed last week as weaker-thanexpected US economic data offset strong corporate earnings reports.

In the US, the S&P 500 and the Nasdaq slipped 0.4% and 1.1%, respectively, after gross domestic product (GDP) growth and durable goods orders missed expectations. Amazon’s warning of slower growth in the months ahead weighed on the consumer discretionary sector, whereas utilities and real estate stocks outperformed.

The pan-European STOXX 600 ended the week flat amid ongoing concerns about the spread of Covid-19. The UK’s FTSE 100 was also little changed after a spike in the number of people told to self-isolate continued to disrupt production.

Over in Asia, Japan’s Nikkei 225 lost 1.0% as new Covid-19 cases reached record levels, resulting in Tokyo’s state of emergency being extended until the end of August. China’s Shanghai Composite slumped 4.3% following the country’s regulatory crackdown on the technology and education industries.

Delta woes weigh on markets

US stocks closed slightly lower on Monday as concerns about the Delta variant were compounded by softer-than expected manufacturing growth. The Institute for Supply Management’s index of national factory activity fell from 60.6 in June to 59.5 in July, the lowest reading since January and the second consecutive month of slowing growth.

Asian markets followed Wall Street lower on Tuesday, with the Nikkei 225 and Hang Seng tumbling 0.5% and 0.4%, respectively, as fears about the spread of coronavirus overshadowed strong US corporate earnings.

In contrast, the FTSE 100 and the STOXX 600 added 0.7% and 0.6%, respectively, on Monday, following news that British engineering firm Meggitt has agreed a £6.3bn takeover by US company Parker-Hannifin. Shares in Meggitt surged 56.7% from Friday’s close.

Market gains continued into Tuesday, with the FTSE 100 and the STOXX 600 up 0.4% and 0.3%, respectively, at the start of trading.

US economic data misses estimates

Last week’s headlines were dominated by the latest GDP figures from the US. According to preliminary data from the Commerce Department, the US economy expanded by an annualised rate of 6.5% in the second quarter. This was better than the 6.3% increase seen in the first quarter but was significantly below forecasts of 8.5% growth.

Personal consumption was the biggest driver of growth, as the stimulus cheques issued between mid-March and April fuelled an 11.8% year-on-year increase in household spending. This was partially offset by lagging property investments and inventory drawdowns.

Separate data from the US Census Bureau showed orders for cars, appliances and other durable goods in June were also weaker than expected. Orders rose by 0.8% from the previous month versus estimates of 2.2% growth, although May’s reading was revised up to 3.2% from 2.3%. It came amid continued shortages of parts and labour as well as higher material costs.

Meanwhile, the Labor Department reported that 400,000 people filed initial claims for unemployment benefits for the week ending 24 July, above the Dow Jones estimate of 380,000 and nearly double the pre-pandemic norm.

More positively, US consumer confidence was little changed in July, hovering at a 17-month high of 129.1. Economists polled by Reuters had forecast a decline to 123.9.

Inflation picks up in Europe

Over in the eurozone, inflation accelerated to 2.2% in July from 1.9% in June, according to figures from Eurostat. This was the highest rate since October 2018 and above the 2.0% reading forecast by economists. Higher inflation came amid faster-than-expected monthly GDP growth of 2.0% in the April to June period. Compared with the same period a year ago, GDP surged by 13.7%. The eurozone economy is still around 3% smaller than at the end of 2019, but the expansion marked a strong rebound from the 0.3% contraction seen in the first quarter of 2021.

Germany missed expectations with a quarterly expansion of 1.5%, as supply constraints left manufacturers short of materials such as semiconductors.

Half a million come off furlough

Here in the UK, more than half a million people came off furlough in June. The gradual reopening of the hospitality sector drove more than half the total fall in jobs supported by wage subsidies, according to data from HM Revenue & Customs.

Shortages of labour and materials and problems recruiting staff meant manufacturing output and order book growth slowed to its weakest level in four months in July. The manufacturing PMI stood at 60.4, down from 63.9 in June. IHS Markit said July’s performance was still among the best on record but would have been even better had it not been for supply constraints.

Nevertheless, the International Monetary Fund (IMF) upgraded its 2021 growth forecast for the UK to 7%, meaning that together with the US it would have the joint fastest growth of the G7 countries this year. In 2020, the UK’s economic contraction was the deepest in the group.

Please continue to utilise these blogs and expert insights to keep your own holistic view of the market up to date.

Please see below for Legal & General’s latest Asset Allocation Team Key Beliefs Article, received by us yesterday afternoon 19/07/2021:

Bearish sentiments

This week, we look at investor sentiment, Peru, and China – can you guess the obvious link between them?

Bulls and bears

The latest AAII Bull/Bear spread, which is based on a survey of investors’ outlooks, has started to drift lower again. The number of bullish investors has now declined to a year-to-date low.

Overall, there are still more bulls out there than bears, but the dampening of excessively positive sentiment can be seen in other indicators too. For us, this is a positive, as it reduces the risk that frothy sentiment quickly unwinds, prompting investors to pull positions and cause a market slump of their own creation.

Yet the overall bullish tone does still remain. Yields are low, policy conditions are generally supportive, and inflation – although high – is not seen as problematic. The vaccine story is also generally good, although we are aware of the risks.

In our own scenario analysis, the conclusions look similar – and that in itself acts as a red flag. Both our most likely scenario of a healthy recovery and the weighted average scenario in our analysis suggest above-trend growth and modestly above-target inflation ahead.

Given the positive sentiment, we think that is pretty well priced by markets too, so return expectations shouldn’t be too lavish from here if that scenario plays out. The upside is a ‘Roaring 20s’ type recovery; the downside is a COVID-19 variant or vaccine failure inducing a deflationary slump or rapid cycle compression, although neither attracts a particularly high probability in our view.

It’s fine to be in the crowd for a while – indeed, some of us may look forward to being in actual crowds again – but as investors we don’t want to stay there for too long. Consensus thinking can be dangerous.

Change at Paddington’s home

There is a new Paddington Bear movie in the pipeline, a Paddington exhibition at the British Library has opened, and Gareth Southgate’s management style has been juxtaposed against Paddington Bear.

Our reason for bringing him up, though, is his origins in “deepest darkest Peru”. Our economist Erik has had his spectacles on to look at Peru and other Latin American economies recently.

Peru now has a decidedly leftist government, but we believe it is a country with enviable fundamentals and China-like growth rates. In the run up to the recent elections, the currency sold off in anticipation of a hard-left candidate winning the vote.

Pedro Castillo did indeed win the presidency, and has vowed to overhaul the country’s economic model. But while his party is socialist, Castillo has drawn up more neutral policies since his victory, including central-bank independence and not nationalising the mining sector.

While we are wary of Castillo and will continue to monitor his policies and cabinet appointments closely, our view is that he may not be as negative for the country as the media are making out. With strong economic fundamentals, the risk event of the election behind us, and attractive valuations after the recent selloff, we have moved in on the currency, looking for negative sentiment to moderate.

Panda pop

This month has brought news that giant pandas are no longer endangered in the wild, according to China. The species is native to South Central China and, thanks to conservation areas, its outlook has been improving. Our view is that the Chinese economy is on a good footing too.

Much of the economic data looks solid and second-quarter growth came in stronger than expected. This made us a little surprised to see a cut in the reserve requirement ratio (RRR), one of the tools used to manage the economy, last week.

GDP is broadly back to its pre-pandemic trend, so if anything is responsible for the RRR cut it could be that growth remains a little unbalanced, with retail sales remaining depressed.

We added Chinese bonds to a number of portfolios in the early parts of the year as we believe the highly rated securities still offer an attractive yield and can play a role as an interesting diversifier in our portfolios. We still think that holds. The downside risk of a vaccine failure causing an economic slump in the country also makes us think these bonds could help should a bear market prevail.

Please continue to utilise these blogs and expert insights to keep your own holistic view of the market up to date.

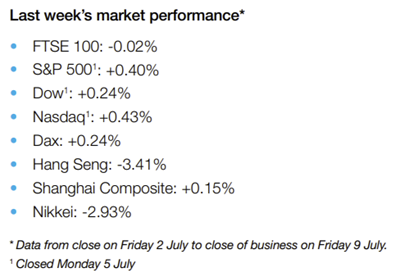

Please see below for Brewin Dolphin’s latest ‘Markets in a Minute’ article, received by us yesterday evening 13/07/2021:

Equities mixed as US Treasury yields slide

Stock markets were mixed last week as fears about a slowdown in global economic growth led to a steep decline in longer-term bond yields. US indices suffered heavy losses on Thursday as the yield on the benchmark ten-year Treasury note slid to a near five-month low. Although falling bond yields usually increase the relative appeal of equities, investors feared it signalled expectations of a slower recovery from the pandemic. The S&P 500 and the Dow managed to claw back losses on Friday to end the holiday-shortened week up 0.4% and 0.2%, respectively.

The spread of the Delta variant of Covid-19 also weighed on investor sentiment, particularly in Asia where Japan’s Nikkei 225 plunged by nearly 3.0%. Tokyo is being placed under a fourth state of emergency to try to curb the rise in infections. In Europe, the STOXX 600 recovered from Thursday’s sharp pullback to end the week up 0.2%. Germany’s Dax also added 0.2%, whereas France’s CAC 40 slipped 0.4%. The UK’s FTSE 100 was flat as the government confirmed it would ease quarantine rules for fully vaccinated adults and under-18s from mid-August, despite the surge in infections.

Stocks rise ahead of Q2 earnings season

Wall Street stocks were in the green on Monday (12 July) ahead of the start of the second quarter earnings season. Analysts expect strong results from banks such as JP Morgan Chase and Bank of America. The Dow, S&P 500 and Nasdaq all closed at fresh record highs, with the Dow narrowly missing the 35,000 mark. The FTSE 100 edged up 0.1%, with insurer Admiral leading the way on news its first half profits are likely to be higher than expected. Travel-related stocks underperformed amid data showing passenger numbers at Heathrow Airport in June were almost 90% lower than pre-pandemic levels. The FTSE 100 was up 0.3% at Tuesday’s market open, after the Bank of England said it was lifting Covid-19 restrictions on dividends from lenders. Shares in NatWest, HSBC and Lloyds all rose by around 2% following the announcement.

US economic data miss forecasts

A raft of worse-than-expected US economic data weighed on equities and bond yields last week. The Institute for Supply Management’s gauge of service sector activity fell to 60.1 in June, lower than the 63.5 figure forecast by economists in a Reuters poll and down from 64.0 in May. It came amid labour and raw material shortages, which resulted in the survey’s measure of backlog orders rising to 65.8 from 61.1 in May. The IBD / TIPP economic optimism index also slipped from 56.4 in June to 54.3 for July, its lowest reading since February. Elsewhere, figures from the Labor Department showed US weekly jobless claims rose to 373,000 for the week ending 3 July, worse than the 350,000 Dow Jones estimate. Job openings hit a record high of 9.2m in May, which was up 1.7% on the previous month but lower than the expected 9.3m.

UK economic rebound slows

Here in the UK, gross domestic product (GDP) expanded by 0.8% in May from a month ago, down from April’s 2.0% increase and weaker than the 1.5% expansion predicted in a Reuters poll. The Office for National Statistics said GDP growth remained 3.1% below its level in February 2020, just before the pandemic struck. The services sector rose by a weaker-than-expected 0.9% between April and May, as the huge surge in accommodation and food services output failed to offset slower increases elsewhere. Services growth was 3.4% below its February 2020 level. Meanwhile, manufacturing output slipped by 0.1% as the ongoing microchip shortage disrupted car production, leading to the steepest fall in the manufacture of transport equipment since April 2020. Construction output fell for a second consecutive month, down 0.8%, but remained the only sector to have output levels at above its pre pandemic level.

Eurozone retail sales rebound

There was more positive economic data from the eurozone, where monthly retail sales rose more than expected in May following a decline the previous month. According to Eurostat, retail sales rose by 4.6% monthon-month and by 9.0% from a year ago. This was above consensus forecasts of a 4.4% monthly rise and an 8.2% annual increase. The surge was driven by purchases of non-food products and car fuel as several countries lifted coronavirus restrictions. However, the rapid spread of the Delta variant has cast doubt over the speed of Europe’s economic recovery. On Friday, Germany and France warned people against travelling to Spain, where the infection rate is the highest in mainland Europe. The Netherlands said it would reintroduce restrictions on hospitality venues just two weeks after lifting them. Figures from the European Centre for Disease Prevention and Control, reported by the Financial Times, showed the weekly Covid-19 infection rate for the EU and European Economic Area rose to 51.6 per 100,000 people on Friday, from 38.6 the week before. The infection rate is expected to exceed 90 per 100,000 people in four weeks’ time.

Please continue to utilise these blogs and expert insights to keep your own holistic view of the market up to date.

Please see below for one of AJ Bell’s latest Investment Insight articles, received by us yesterday 09/05/2021:

In many ways right now, it looks like business as usual for the financial markets. Blow-out quarterly numbers from Google’s parent Alphabet, Apple and Facebook are taking their share prices to new highs and carrying the NASDAQ index along with them; the FTSE 100 is having another crack at breaking through the 7,000 barrier; and central banks seem in no rush to switch off the hose of cheap liquidity with which they are dowsing markets (unintentionally or otherwise).

And yet, as discussed last week, bonds are trying to rally, as is gold. This move in haven assets seems at odds with the prevailing optimism regarding global vaccination programmes, an economic upturn and higher corporate profits and dividends.

It can be too easy to read too much into such short-term moves, as nothing goes up (or down) in a straight line. One way to test the market mood is to check out what is going on at the periphery, as that is where advisers and clients are probably taking the most risk and therefore the asset classes and holdings they are most likely to liquidate first in the event that bullish sentiment starts to ebb.

Another is to look at the market darlings: the areas that are doing (or have done) best and are garnering the most coverage from analysts, press and commentators alike. If they are keeping on running, then all may still be well. If not, this may be the first inkling of trouble ahead, or at least a shift in the market mood.

Cryptic message

Both the Archegos hedge fund and Greensill Capital went down in March, despite the bullish market backdrop and expectations that the global economy is on the mend (see Shares, 29 March 2021). That still feels odd. Markets have so far done a good job of shrugging off those failures, however advisers and clients will remember markets kept rising after the first two Bear Stearns property funds collapsed in June 2008, but it did not take long for deeper problems to appear – so everyone must remain vigilant, especially as there are some signs that some of the hottest areas are starting to cool.

This can, for example, be seen in the fortunes of both Bitcoin and Special Purpose Acquisition Companies (SPACs), a phenomenon that has gripped the US market in particular. The Next Gen Defiance SPAC Derived Exchange-Traded Fund (ETF), which tracks a basket of over 200 SPACs, is down by more than a third from its high. This is perhaps less of a surprise when you consider the data from SPACinsider.com, which shows how 308 SPACs are looking for a target even though 263 have already floated. In the end, supply may be outstripping demand.

Setbacks in Bitcoin are nothing new and cryptocurrency supporters will be unperturbed, but the way the performance of Initial Public Offerings (IPOs) is tailing off around the world is worthy of note. Perhaps the quality of deals is going down as the prices are going up, or, again, supply is starting to catch up with demand.

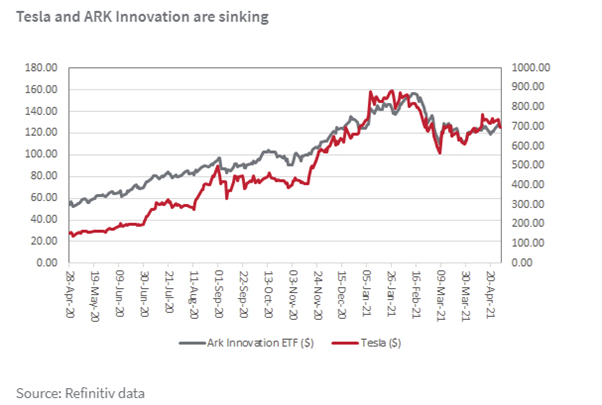

Electric shock

Advisers and clients are unlikely to have the time for, or interest in, the intricacies of stock-specific issues, but there can surely be no better proxy for the current bull market than Tesla. Yet even Elon Musk’s charge is, well, losing a bit of its power to impress and that is weighing on another momentum favourite, Cathie Wood’s ARK Innovation ETF, a $22 billion actively-managed tracker which aims to deliver the performance of 58 tech and growth stocks.

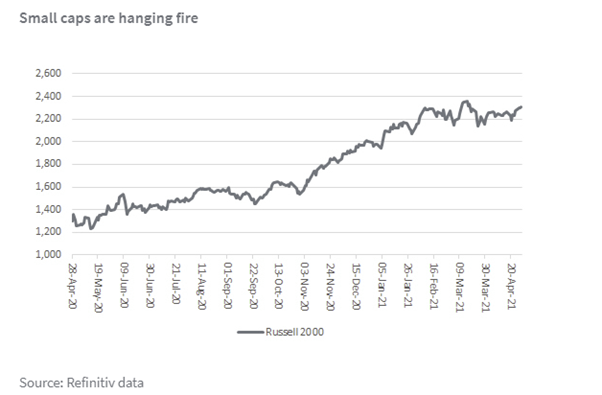

Even that classic gauge of both market sentiment and economic activity small-cap stocks are pausing for breath, although America’s Russell 2000 is yet to roll over.

All of this could be healthy. Again, nothing goes up in a straight line and some of these assets and securities were looking bubbly, at least in the eyes of some. A cooling-off may be no bad thing.

Equally, it could be just a sign that markets are moving on. Frontier and emerging equity markets still look to be showing upward momentum, a trend that would fit with the narrative of a global economic recovery and bullish investor sentiment – few areas are more peripheral than frontier arenas such as Vietnam, Morocco, Kenya and Romania.

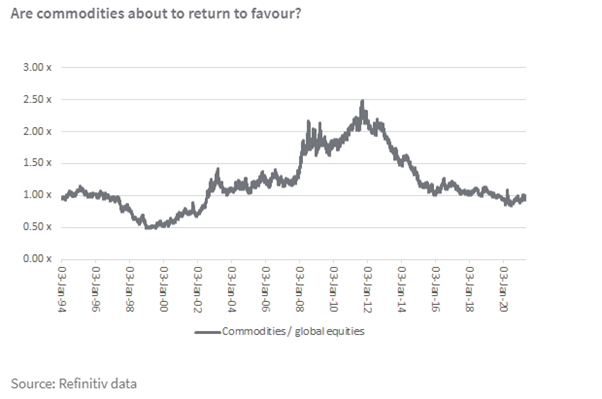

As such, we could just be seeing the next leg of the switch from defensives and growth to cyclicals and value. And if the upturn does prove inflationary, then there is a further trend to watch, one to which this column will return. This final chart shows the relative performance of commodities, as benchmarked by the Bloomberg index, against the FTSE All-World Equities index. Maybe real assets are on the verge of ending a decade’s worth of underperformance relative to paper assets, or at least paper claims on them?

Please continue to utilise these blogs and expert insights to keep your own holistic view of the market up to date.

Please see below for the Daily Investment Bulletin from Brooks McDonald, received by us today 05/01/2021:

What has happened

Markets started the day positively but the New Year jubilance faded as the US COVID outlook worsened and a tight Georgia run-off today could go either way. The US index started the day in positive territory before falling as much as 2.5% then settling 1.5% down at the close.

COVID’s new variant and restrictions

The new COVID variant has been responsible for a large quantum of the surge in the South East of England and news that it had now been detected in New York, Colorado, California and Florida did little to help the mood. Whilst there is no evidence that the new strain is more deadly it does appear to be transmitting aggressively, causing strain on the healthcare system. It is this strain that led to UK PM Johnson announcing that England would move into its third Lockdown with the new stay at home rules far more reminiscent of March 2020’s with schools closed and only essential journeys allowed. UK Chancellor Sunak is expected to unveil a fresh support package for UK companies in light of these new tough restrictions which are expected to produce a similar economic impact to that seen in March and April last year.

Georgia run-off

The other event keeping New Year optimism in check is the Georgia Senate run-off. This is clearly key in determining which party has control of the Senate and therefore whether a blue sweep can be achieved. Back in November the market’s base case was that the Democrats would win every race and this would give them the flexibility to launch substantial stimulus in Q1 2021. Once this didn’t immediately materialise, investors warmed to the idea of a split Congress as this would curb the chances of tax rises, tougher regulation and other less economically positive reforms. As we approach today’s election, the Democrats are ahead in both seats, albeit it narrowly, and investors are not entirely sure which side of the coin they want the race to land.

What does Brooks Macdonald think

A Democrat clean sweep or a split Congress both have benefits and negatives but our instinct is that a split Congress would be more market friendly as it retains the status quo and financial assets will look through the positives of US Fiscal Stimulus quite quickly as compared to broader reforms. Even if the Democrats do take both seats, and VP-Elect Harris is left with the deciding vote in the Senate, the current filibuster rules will stop contentious legislation. If we do see a blue sweep, markets will look very closely at any suggestions from the Democrats that they would look to remove the Filibuster from the next Senate session.

Regular daily updates like these are a useful method of frequently updating your holistic view of the markets, especially given the way the world is rapidly changing by the day with Coronavirus.

Please continue to utilise these blogs to help inform your own views of the markets.

Please see below for the latest Markets in a Minute update from Brewin Dolphin, received yesterday evening 22/12/2020:

Global equity markets moved mostly higher over the past week, as the vaccines programme boosted optimism and an agreement on the US stimulus package edged closer. Eternal hope of a Brexit deal helped the more UK-centric shares and European markets. The FTSE100 has been an underperformer, however, as the dollar has been weakening relative to sterling, squeezing the earnings of FTSE’S multinationals, which gather most of their revenue in dollars. The ongoing dollar slide helped push commodity prices higher, and bitcoin briefly hit a record $23,000 amid a flurry of speculation, although nobody can really gauge its true value.

Last week’s markets performance*

• FTSE100: -0.26%

• S&P500: +1.25%

• Dow: +0.44%

• Nasdaq: +3.05%

• Dax: +3.93%

• Hang Seng: -0.02%

• Shanghai Composite: +1.42%

• Nikkei: +0.41%

*Data for week to close of business on Friday 18 December

Equity markets pull back at start of week

News of the virus mutation in the UK, and resulting restrictions on the movement of people and goods to numerous countries led to a sell off in many markets around the world on Monday. The FTSE100 closed down by 1.73% at 6,416.32, and the FTSE250 ended 2.11% lower at 19,962.11. In Europe, the pan-European STOXX 600 index fell 2.3% after the UK announced its tougher restrictions in response to the vaccine, and the EU’s largest market, the German Dax, fell by 2.82%. Reaction was more muted in the US, where the S&P500 lost just 0.4%, while the Nasdaq lost 0.10%. The Dow closed up by 0.12%.

US stimulus bill passed

The long-awaited US stimulus package to extend unemployment benefits and fund a range of other pandemic-related expenditure was passed on Monday night after nearly six months of wrangling. The package, worth $900bn in total, will send one-off cheques worth $600 to households, with extra payments for children. It will also extend unemployment benefit payments worth $300 a week for those who are out of work due to Covid-19. These payments will last until March and give the vaccination programme time to take effect. However, President-elect Joe Biden has signalled he will look to pass a larger bill once he takes office in January.

Markets sensitive to risk

There is a lack of liquidity in the market at the moment, as many traders have started their Christmas breaks and there is less money flowing into shares and bonds. This can make markets quite volatile, and there is no denying that the newsflow right now is quite alarming. We heard of the new strain of Covid-19 emerging from the UK, prompting Tier 4 containment measures in London, the south east and parts of eastern England over the weekend. In Europe, there are concerns surrounding movement of people and goods which has led to travel constraints. This could have an impact on the economy – and our lives – unless some resolution is reached quite quickly.

This bad news linked with a lack of progress on Brexit, with travel restrictions making negotiations harder, led to weakness in UK and European markets at the start of the week. However, the pound has recovered its losses, indicating that investors are perhaps taking stock and realising that this is probably not as frightening as the headlines first seemed. There were hopeful headlines on Tuesday morning about a compromise on fishing quotas, but there is no firm news of progress. We must wait to see how this plays out in the coming days, but markets will be jittery until the end of the year at least; even if a deal is agreed, it needs to be cleared by the EU member states which will not happen until the new year. The US, meanwhile, was far calmer, with the Dow even closing with a small gain, as the US stimulus bill was passed.

Economic resilience Taking a broader view, the global economy is holding up better than expected given such challenging circumstances. Many UK businesses had reported activity improving in December. The IHS/Markit flash composite purchasing managers index, which measures business levels compared to the previous month, rose to 50.7 in December from 49 in November. A reading above 50 indicates business is expanding. The services element of the index, which covers leisure and hospitality, rose to 49.9 in December from 47.6 in the previous month, suggesting business levels are still falling. Yet the data was still better than anticipated and shows the economy holding up relatively well. PMIs in the US were even stronger, with the businesses saying that activity levels were improving, especially in the manufacturing sector.

All in all, there is a sense of confidence that the global economy will get through this very challenging period and emerge to recover next year, as things return to normal. On a 12-month view, we remain optimistic on equities, although it could be a bumpy ride until as sentiment rises and falls along with the headlines.

Brewin Dolphin regularly give us their insight of the markets. Updates in this efficient manner are a quick but well-informed way to update your consensus view of the global markets.

Please keep using these blogs to regularly update your knowledge of current market affairs from around the world.

Please see below for the latest Blackfinch Group Monday Market Update received by us today 21/12/2020:

UK COMMENTARY

Talks continued in the hope of finding a solution in the Brexit negotiations.

Data showed redundancies hit a record 370,000 in the third quarter of the year, with the unemployment rate rising to 4.9%.

UK inflation slowed again in November, to 0.3% from 0.7%, with prices weighed down by retailers cutting prices during ‘Black Friday’ sales.

The Bank of England voted to leave interest rates on hold and revised its expectations for the decline in gross domestic product in the fourth quarter, from 2.0% to a “little over 1%”.

UK retail sales fell 3.8% month on month in November, although economists had predicted a decline of more than 4%.

US COMMENTARY

Talks continued over a further stimulus package, with the deadline fast approaching.

The Electoral College ratified the November presidential election result, with each state voting in line with their electorate to confirm the upcoming inauguration of Joe Biden and Kamala Harris.

US retail sales fell further than expected in December, declining 1.1% month on month.

The US Federal Reserve announced it will buy at least $120bn of bonds each month until substantial further progress is made towards its maximum employment and price stability goals.

First-time jobless claims data came in above expectations in the week to 12th December, climbing to 885,000.

ASIA COMMENTARY

The Bank of Japan extended its virus-related corporate lending programme by six months to September 2021, while making no changes to its monetary policy.

COVID-19 COMMENTARY

The US began its vaccination programme, with the first three million doses of the Pfizer/BioNTech vaccine distributed for use across all states.

The US Food and Drug Administration approved the vaccine developed by Moderna for emergency use.

News broke of a new variant strain of COVID-19 that has become prominent in London, the South East and Eastern England.

These articles provide concise well-informed views that cover the whole of the market and are useful to maintain your up to date view of the markets globally.

Please keep reading our blogs regularly to give yourself a holistic and up to date view of the markets.

Please see below for the Daily Investment Bulletin from Brooks McDonald, received by us today 17/12/2020:

What has happened

The Federal Reserve had their final rate setting meeting of the year and were eager to reassure markets that quantitative easing would remain until the economy had improved substantially. Whilst markets initially wavered over the lack of further measures they eventually settled largely unchanged.

Last Fed meeting of 2020

The Federal Reserve has been responsible for a large number of the blockbuster stimulus headlines over 2020 but those hoping for another round of accommodation were disappointed. The committee stressed that it would continue with the current pace of quantitative easing until ‘substantial further progress’ had been achieved towards their inflation and employment targets. There was some change to the 2023 interest rate expectations with one member showing a hike that year and also to the 2023 inflation level expectations where 4 members pointed to a small overshoot of the 2% target. Of course, a small overshoot would not pose a problem for the bank given it has unveiled average inflation rate targeting earlier in the year which will give them additional room if needed.

Update on unfinished business

The tone around Brexit talks improved again yesterday with sterling seeing further strength but remaining in the 1.09-1.11 band versus the Euro that it has been maintaining despite the high jinks of recent weeks. EC President von der Leyen said yesterday that ‘there is a path to an agreement now’ but reports suggest that fisheries remain a stumbling block. Rumours are circulating that Parliament is readying to return early next week to vote on a deal which is also supporting the UK currency. Meanwhile US Fiscal Stimulus talks continue amidst a positive tone, but the spectre of Christmas is nearing so there is a narrowing path to pass through Congress. The more contentious $160bn bill appears to have been predictably side-lined but the more substantial package seems to have the support of both sides.

What does Brooks Macdonald think

Economic data over the last few days has seen beats in Europe (specifically the compositive PMIs) and misses from the US on retail sales. This highlights how difficult it is for economists to calculate activity during periods where restrictions are gradually tightening, and consumer behaviour is shifting. The miss in US retail sales does provide further impetus for fiscal stimulus however and markets shrugging this off reflects hope that this may provide a catalyst for support rather than be a sign of things to come.

Regular daily updates like these are a useful method of frequently updating your holistic view of the markets, especially given the way the market is rapidly changing by the day with Coronavirus and Brexit.

Please continue to utilise these blogs to help inform your own views of the markets.