Please see below for the latest key beliefs article from Legal and General’s Asset Allocation team, received by us late afternoon 07/12/2020:

Festive spirits

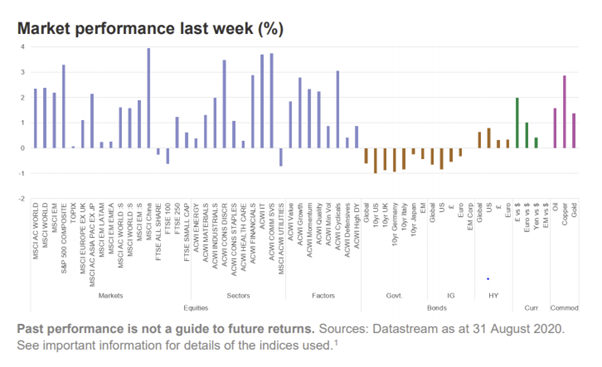

Markets don’t seem to be taking a holiday break yet. Last week, equities rose, the US dollar weakened, and rates and inflation climbed higher. It doesn’t look like we will be able to relax any time soon, either; the coming weeks could see the start of vaccine distributions, the Trump administration transferring power, the conclusion of Brexit’s game of ‘deal or no deal’, and potentially a fiscal deal in the US.

As with all Key Beliefs emails, this email represents solely the investment views of LGIM’s Asset Allocation team.

Could the last bull please switch off the lights?

Recent news on COVID-19 vaccines has generally been positive, but the immediate economic outlook remains challenging. Europe is already in a renewed contraction, following a significant increase in restrictions to get the virus under control. US economic data have held up well so far because restrictions had been relatively limited, but stricter measures are starting to be deployed amid a surge in cases.

Then there are the fading hopes for fiscal stimulus. US households are beginning to run out of savings from the income transfers received during the spring lockdown, while more unemployment benefits are set to expire at the end of this month. There are signs Congress is beginning to recognise this danger, and Friday’s weaker payrolls report was a clear warning as talks have resumed on passing some targeted measures in the $500-900 billion range. It is not clear a compromise can be reached in time for Christmas; failure to achieve one risks an outright contraction in activity over the festive period and a negative GDP print for the first quarter.

Does it matter? The outlook for 2021 is bullish and markets might be able to look through any weakness as temporary. The main headwind for markets at the moment is the very broad positive sentiment. Next year’s consensus outlooks are bullish and our sentiment indicators are exuberant. What could possibly go wrong?

We remain cautiously bullish for the medium term but tactically neutral. We will not chase the rally at this point, preferring to take our risk in relative-value trades.

Every hero needs a crisis

Central banks had no choice in either 2008 or March this year. The world needed to be saved from a financial meltdown and so they flushed liquidity into the world.

However, today’s monetary policy can contribute to tomorrow’s meltdown. Keeping interest rates low to provide a safety net for markets can induce corporations and households to take on more debt and more risk. This dynamic has also tended to stoke inequality, as asset prices have been boosted even though unemployment has spiked. Managed stability creates instability.

Global leverage has increased significantly this year, undoing much if not all of the deleveraging of recent years. In a normal world, increased leverage is often resolved by a credit crisis, massive defaults, forced liquidations, or massive inflation. But apparently this isn’t a normal world.

Most of the increase in debt during the pandemic has been in the public sector, and a large part of this has been absorbed by central banks via quantitative easing. This debt sits with central banks and is perpetually rolled over, effectively debt monetisation. Central banks could commit to never selling it or just write it off, which would improve debt-to-GDP ratios. Cancelling public debt like this is prohibited in some countries, due to the moral hazard it could create for politicians. For others, the only constraint is ultimately inflation.

But ballooning debt is also a symptom of other problems like weak productivity and inequality (encompassing poor health, low wage growth, and poor education). This could result in further political tensions and anti-globalisation, similar to the experience of the 1930s.

Given the current economic output gaps, we don’t see runaway inflation as a likely scenario but our head of economics does expect mildly higher inflation in the years to come. This would change if we saw continued broad global fiscal support financed by central banks.

Do you feel lucky?

Bitcoin reached a new all-time high last week. The crypto-currency has mostly seemed a private-investor phenomenon, but we have seen increased interest from institutions. There are many things for them to like: past returns have been stellar (an annualised return above 100% over the past five years); it has offered some diversifying properties with only a slight positive correlation with risk; and, contrary to many currencies, it has the attraction of limited supply at a time when central banks are printing money.

However, there are also plenty of downsides. Bitcoins have no intrinsic value (at least tulip bulbs could yield a beautiful flower); they are not widely recognised or regulated; it takes the energy of a medium-sized nation to mine a bitcoin so it isn’t very environmentally friendly; and it is very expensive and slow to use in day-to-day transactions.

The first is perhaps the most existential risk: at some point bitcoins could become worthless if a more popular or efficient alternative is found. Central banks could well develop their own crypto-currencies, especially if bitcoins and others become too big and interfere with efficient monetary policy.

It could easily be years before the next bitcoin selloff but we know how this story is likely to end. At the peak of the 17th century tulip trade in Amsterdam, those paying fortunes for a single bulb were surely speculators who understood that tulip prices had no link to bulbs’ intrinsic value and just hoped to sell them to someone else at an even higher price. Many were successful in the year before the crash in 1637; their quick gains were what drew in others and excited pundits. Does that sound familiar?

These articles provide concise well-informed views that cover the whole of the market and are useful to maintain your up to date view of the markets globally.

Please keep reading our blogs regularly to give yourself a holistic and up to date view of the markets.

Keep safe and well,

Paul Green

08/12/2020