Please see article below from Invesco received late on Friday afternoon – 18/06/2021

Don’t fear the singularity

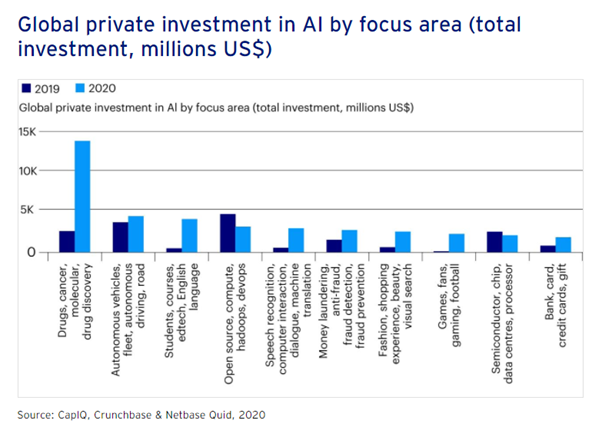

Technology is moving up the skill curve. As AI becomes more ‘I’, how far can it go? Invesco partnered with The Economist to explore the topic in more depth in their ‘The art of the possible’ series.

You can look at the revolution in artificial intelligence (AI) in two ways—as two alternate universes, almost. One, where machines support and enhance the human. Star Trek, if you will. The other, where access to technology has created an impassable divide between the haves and have-nots, more like the dystopian film Elysium.

Technology is certainly taking us closer to an automated future, whatever that may be. AI may have started by replacing low-skilled call centre jobs with rather clunky bots, but things are becoming more sophisticated.

Take the field of medicine, for example. To qualify as a diagnostician takes people years of training, and is often an arduous, time-consuming process. What’s more, in many areas, demand for this expertise outstrips supply, putting the healthcare system under strain. But where diagnostic information can be digitised, machines can step in to take the load. “AI is being used to help solve complex societal challenges, such as climate change, healthcare and food poverty,” says Robert Troy, Ireland’s minister for trade promotion, digital and company regulation. The advantage of an algorithm is that it can draw conclusions from the data in a fraction of a second. And, unlike a flesh-and-blood expert, machine-learning expertise can be reproduced potentially infinitely.

Mr Troy is optimistic about the wider ability of AI to transform society. “Globally, it is estimated that the application of AI could double economic growth by 2035,” he says. One study estimates that AI could contribute up to $15.7trn globally in 2030, more than the current output of China and India combined.1

Kevin Roose, author of Futureproof: 9 Rules for Humans in the Age of Automation, highlights the ways that AI is shaping work, such as “labour displacement that we traditionally think of when we think about automation”, although he says this is happening in a broader swath of industries than it traditionally has, through to white-collar workplaces. What’s less recognised is the supplanting of management functions: “There’s now a whole industry of worker surveillance and performance tracking software, and in some cases automatically making decisions about hiring and firing.” Overall, this could lead to the replacement of 47% of current job functions by 2034.2

Data curators

Where does this leave work, as we traditionally conceive it? Two centuries ago, England’s Luddites destroyed the emergent machinery of the first industrial revolution, as a way of combating what they saw as the replacement of manual jobs. Are human workers becoming a thing of the past?

Not really, says Mr Troy, as “much of the disruption caused by AI will result in changes to job roles, tasks and distribution”. Your doctor, for instance, won’t necessarily be replaced by a robot. “AI-based systems will augment physicians and are unlikely to replace the traditional physician–patient relationship,” according to one recent study published in PeerJ.

Marcus du Sautoy, Oxford Simonyi Professor for the Public Understanding of Science, agrees with Mr Troy: “We are going to see AI encroach on an increasing number of white-collar jobs, but as with all these revolutions, new jobs appear.”

The abilities of machines can enhance what it means to be human, not constrain it. Professor du Sautoy gives the example of the data curator, calling it “almost a new type of artist”. “Algorithms learn from data,” he says. “You give it data, it will go in one direction, you give it different data, it goes in another.” The still central role of human agency is to understand that process, and how to manipulate it to make it do what you want it to do—something that is a new and very human skill set. So, although AI can mimic artistic styles, from poetry to painting, it functions mostly in an assistant role, rather than replacing the human genius in the loop. The ghost in the machine has yet to become the machine.

Says Professor du Sautoy: “We thought the one thing that will be left to do is to write our symphonies and our novels, and now AI is going to be able to do that as well.” He sees a positive aspect to this, as the imperative to be creative can be terrifying. It’s a high entry level to taking that leap into writing or painting. “There’s something quite exciting about the power of these tools to democratise something that before was quite an elitist activity,” he adds. AI banishes the terror of the blank page. It’s an interesting idea.

Towards a two-tier economy?

Mr Roose predicts the rise of a two-tier economy: the machine economy and the human economy. The products of the former will become very cheap. “AI will enable the people who run those companies to strip out all the inefficiency and waste,” he says.

Conversely, the human economy will consist of people who are not so much making things and providing services as they are creating feelings and experiences, examples being healthcare workers, teachers and artists. And why stop there? Even people you wouldn’t think of as being irreplaceable, such as bartenders, baristas and flight attendants, fit the bill because they’re about making people feel comfortable. It’s the human touch that is so important.

Mr Roose reckons that this will increasingly see hyper-scale tech companies create higher-touch versions of their services: for example, a luxury version of Netflix, where film curators pick out movies for you. “There will be layers within these companies where users pay for human interaction on top of the base layer,” says Mr Roose. He predicts a new generation of companies that scale human connection without dehumanising it.

Does this mean that the tech leviathans will dominate everything? Professor du Sautoy doesn’t think so—but he does believe changes need to be made to ensure an open field. “You don’t need huge companies to analyse this data,” he says. “It’s about having clever algorithms to search data allowing smaller players to come into the field.”

However, he cautions, “If you don’t have access to data, you’re completely stuffed, frankly.” There are already examples of this in open source data—for instance, open banking regulation, which compels large banks to share their customer financial information. This has enabled disruptors in fintech, such as UK challenger banks Starling and Monzo, each now valued at more than £1bn, to enter the playing field.

There are, of course, strong vested interests with this. But that’s also true of ‘traditional’ financial services, and yet the field was still opened. Could the same be done with AI?

Please continue to check back for our regular blog posts and updates.

Please see below a comprehensive and insightful investment article received from JP Morgan, which provides educated predictions for the second half of the year and considers what might lie in store for global economies.

THEME 1 – INFLATION SIMMERING BUT NOT YET BOILING OVER

Developed economies are expected to continue their strong post-lockdown bounceback in the second half of the year. Vaccine rollout is well advanced in the US and UK, and continental Europe is quickly catching up. Despite recent spending, we estimate that households still have considerable excess savings as we head into the second half of the year, amounting to about 12% of GDP in the US, 7% in the eurozone and 10% in the UK.

Not all sectors of the economy are returning to normality: travel restrictions are likely to remain in place until governments are more confident that vaccination levels can cope with new strains of the virus. However, consumers are spending where they can and tourism’s loss appears to be home renovation and construction’s gain. Housing markets are booming in much of the developed world.

For now, it is rising consumer prices, rather than house prices, that central banks are monitoring. After over a year of pandemic-related disruptions, supply is struggling to keep pace with surging demand. Alongside soaring global commodity prices, input costs are on the up, with many companies passing cost increases on to end consumers. US CPI inflation is likely to remain above 3% into next year, and eurozone and UK inflation also looks set to rise in the coming months (see On the Minds of Investors: Monetary and fiscal coordination and the inflation risks).

Central banks believe these inflationary pressures will prove transitory. Whether this turns out to be the case depends in large part on the behaviour of labour markets. If workers are able to bargain for higher pay, inflationary pressures will become more entrenched.

Unfortunately, labour markets are as hard to predict as goods markets at this point. For example, in the UK, the unemployment rate has risen to 4.7%, but is well below the 8.5% peak it reached following the Global Financial Crisis. But 8% of the workforce are still on furlough, making it hard to gauge the true degree of labour market slack. In the US, the unemployment rate did rise sharply and, at 5.8%, still sits 2.3 percentage points above the pre-pandemic low. And yet firms are saying they are having more difficulty recruiting than at any point on record.

Inflation is likely to create market jitters in the second half of the year, but ultimately we believe it will take a lot to shift the central banks away from their current preference for tightening too late, rather than too early. Talk of tapering by the Federal Reserve (Fed) will no doubt become louder over the summer, but our base case sees a reduction in asset purchases beginning only at the start of 2022, with rate hikes not until at least the following year. In the eurozone, large asset purchases are set to continue for a long time in the context of still subdued inflationary pressures, even if we see some shuffling of purchases among the European Central Bank’s (ECB’s) various purchase programmes. Recent commentary from the Bank of England (BoE) suggests that policymakers may be open to tightening policy a little more quickly in the UK, but it should still be a debate for next year rather than this.

This new, more patient reaction function from the central banks is not without risks. A willingness to let the economy run hot sets up a strong near-term rebound. Yet, once the time for rate hikes arrives, we see a risk that central banks (especially the Fed) will have to tighten policy more quickly than the market currently expects.

Supportive policy from developed world central banks will help emerging economies catch up. While some economies, such as China, came through the pandemic relatively quickly, others are still struggling to contain the virus. However, we expect the vaccine delay in key parts of the emerging world to be a matter of quarters rather than years and believe economic activity should prove relatively resilient given the strength of global goods demand and commodity prices.

Overall, we think the outlook for near-term global growth remains strong. As the bounce from pent-up consumer spending fades, we expect government and business spending to pick up the baton. Focused on ‘building back better,’ governments are lining up multi-year infrastructure projects. This marks a stark contrast to the last cycle, in which government austerity proved a consistent drag on activity and inflation.

It is also remarkable to see how quickly investment is bouncing back, again in stark contrast to the last cycle. Indeed, if inflation is the greatest downside risk for investors to monitor, investment spending is the key upside risk, since it could potentially herald the start of a new era for productivity growth and help alleviate inflationary pressures.

Overall, the macro backdrop for the second half of the year remains strong. Growth in the developed world may slow by year end, but is likely to remain above trend, broadening out to investment spending and becoming more evenly distributed across geographies. Inflation concerns are likely to linger, but ultimately we think it will take a lot of bad news for central banks to meaningfully alter their current plans for a glacial removal of stimulus. While this approach may create further risks down the road, economic activity and corporate earnings look well supported for now.

THEME 2 – STICK WITH ROTATION INTO VALUE

The key question for equity investors is how moderately higher inflation and bond yields will affect corporate profits and valuations. Given significant pent-up consumer savings and elevated capex intentions, sales growth will likely be strong. When sales are strong, profits tend to rise, even if input costs are rising.

Higher bond yields could raise borrowing costs but this can also be offset by higher sales, while higher wages tend to boost sales as well as costs. Meanwhile, any additional taxes that hit the corporate sector are likely to be at least partially offset by the demand boost from additional government spending.

So, against the current economic backdrop, it seems unlikely that rising costs will fully offset the anticipated benefit from strong sales growth. Higher inflation is therefore likely to coincide with higher profits, as is normally the case.

The bigger concern for investors is whether higher bond yields will hurt equity valuations, since it raises the discount rate on companies’ future earnings. However if bond yields are rising because growth expectations are rising, then valuations don’t have to decline. Indeed, it is common for valuations to rise (and fall) at the same time as bond yields. Even if rising bond yields do lead to lower valuations, then as long as profits rise by more than valuations decline, stocks can still rise. Our base case is that rising corporate profits, driven by strong demand, will offset any decline in valuations for most stocks.

Growth versus value is another key debate as we head towards 2022. So far in 2021, last year’s losers have outperformed last year’s winners, with value stocks significantly outperforming growth stocks. Despite this, growth stocks still trade on high valuations compared with history and relative to value stocks.

Given that we believe 12-month forward earnings expectations are likely to keep rising for most stocks, the biggest risk to our continued optimism on equities is that valuations on the more expensive growth stocks decline by enough to offset the earnings upside.

However, our base case is that any further compression in the valuations of growth stocks will just limit the extent of their upside, rather than fully offset the expected increase in earnings. While we do not expect further price/earnings (P/E) expansion on value stocks, valuation compression seems less likely than for growth stocks, given much lower starting valuations.

For example, consensus expects 12-month forward earnings on the Russell 1000 growth index to be 19% higher by the end of next year, compared with 17% higher for the Russell 1000 value. Both indices should therefore rise, but even a modest decline in growth stock valuations relative to value stocks could lead growth stocks to underperform.

At the very least, it is worth being aware that a large part of the reason for the outperformance of growth stocks since 2009 has been the substantial increase in their valuations. A repeat of that tailwind seems unlikely from this starting point, and it is possible that it could now become a headwind, if valuations on growth stocks continue to decline. Value stocks, by contrast, are unlikely to see P/E compression, given valuations remain relatively modest.

It is also worth noting that financials are by far the largest part of value indices globally. Over the last decade, their relative performance has been highly correlated with 10-year bond yields. We therefore expect financials – and hence probably broader value indices – to outperform, if we’re right that bond yields will rise further from here.

Overall, we believe equities will move higher but at a slower pace, and with the potential for the usual bumps in the road. We also have a moderate preference for value over growth stocks, based on relative valuations and our view that bond yields will continue to rise.

At the index level, this means the US could underperform other regions, because of its large weighting to more expensive growth stocks. US value stocks could continue to perform well though, while more value-oriented markets such as Europe and the UK could outperform. For investors keen to avoid putting all their eggs in the value basket, we believe emerging markets offer long-term growth opportunities at a more reasonable price than some other markets.

THEME 3 – RETAIN FOCUS ON ASIA’S DECADE

Asian equities began 2021 with a lot of promise. Favourable longterm trends in demographics and technology, in combination with better containment of the pandemic, provided a strong tailwind for the region (see On the Minds of Investors: Asia’s decade: Getting ahead of the growth opportunity).

Since February, it seems that the tide has turned. Absolute performance stalled, while US and European equities stormed ahead. While part of the story relates to better developed market prospects following President Biden’s massive fiscal stimulus, the relatively poor performance of China since February has been a significant source of the underperformance of Asian equities.

This may seem surprising given that China’s economic outlook for the year appears compelling. Due to its early success in containing the pandemic, China looks on track to achieve more than 8% GDP growth in 2021.

However, three near-term challenges have investors concerned. First, Beijing has begun tightening policy after an expansion during the crisis amounting to growth in credit stock of over 30% of GDP. Second, a number of new announcements about tech regulation have generated worries about Beijing’s reform agenda. And third, in Asia the vaccination programme has been slower than those of many developed economies leading to lingering virus concerns.

We are not overly worried that these headwinds will provide a lasting drag on either economic or market performance. Any tightening of credit will be gradual and measured. Consumer inflation is currently contained, giving China’s central bank little reason to raise policy rates in the coming months. Therefore, current policy measures should be understood as normalising and not as outright tightening.

While not overly worried about tightening, neither do we believe China’s reform efforts should deter international investors. Faced with monopoly concerns, worries about financial stability and changing public sentiment, regulators are taking a more hawkish approach towards leading tech and financial companies. Recent high-profile fines for companies breaking competition laws, as well as the closing of regulatory loopholes, may signal the end of the highly supportive environment that these firms have enjoyed in recent history.

Given the weight these firms have in both Chinese and broader Asian indices, their underperformance has had a significant impact on overall returns. While the market leaders might be constrained by potential new rules in the short term, we believe their long-term growth outlook remains compelling, and valuations are now more attractive.

And on vaccinations, China is now making significant headway in catching up on vaccinating its population (EXHIBIT 7). In India, meanwhile, only 19% of the population are over the age of 50, so while the current outbreak is taking a heavy toll, it shouldn’t be too long before the most vulnerable have been vaccinated. In some smaller Asian countries, the slower pace of vaccine rollout may lead to ongoing problems with local outbreaks, delaying a full economic recovery this year.

In summary, while we acknowledge that President Biden’s stimulus has provided a near-term turbo boost to the US economy, we do not think developed market outperformance will last over the medium term. US and European policymakers will soon face the very same tough questions as their Chinese counterparts today – when and how to normalise the enormous amount of stimulus. So in 2022 and the following years, dynamics are likely to change as the distortions in corporate earnings caused by the pandemic and the policy responses recede. In this environment of more moderate growth, structural themes such as rising household incomes and technology adoption in Asia should gain importance relative to the cyclical stories that dominate today’s market performance. Since we are already in the middle of the year, it will be just a matter of time before investors shift their focus to the earnings outlook for next year, which should be beneficial for Chinese as well as broad Asian equities.

In the second half of the year, the outlook for Chinese local bond markets continues to be compelling. Moderate consumer inflation, solid corporate earnings and a low probability of rate hikes are supportive for the asset class. However, after the 10% appreciation of the renminbi in the past 12 months, we think that investors should expect a reduced tailwind from currency effects.

THEME 4 – CONSIDER PORTFOLIO IMPLICATIONS OF COP26

In early November, major nations will reconvene to discuss global plans to tackle climate change. COP26 (the 26th UN Climate Change Conference of Parties) will see leaders revisit the commitments that were made under the Paris Agreement in 2015, assess the progress to date and set a roadmap for the future. The legally-binding commitment made in 2015 was to limit global warming to well below two degrees Celsius, compared to pre-industrial levels, by the end of the century.

What is different about this annual meeting is that the US is back at the table, providing renewed momentum. Top of the agenda will be to compare national greenhouse gas emissions outcomes to those planned, and assess whether they are sufficient to achieve global climate objectives.

The conclusion is likely to be that greater efforts are required – though many governments have already accelerated their plans. The EU plans to reduce its emissions by 55% by 2030, while achieving net zero emissions by 2050 has recently become the new benchmark. In 2020, the UK and France were the first major economies to write their net zero emissions targets into law, and many other countries, including the US, are now following their example. China has given itself an additional decade with net zero emissions targeted for 2060.

The realignment of the US with global climate initiatives is a gamechanger. Having organised a global climate summit on Earth Day and supported a G7 announcement to end fossil fuel subsidies by 2025, the US will probably support a new Grand Climate Accord during COP26.

With the major economies already aligning behind the goal, reaching net zero emissions may well become the new official global target. This will require dramatic changes to the global economy, and we expect a wave of new policy and major investments in green infrastructure to be announced at COP26. However, to reach net zero emissions, policymakers will also need to increase private sector incentives to reduce carbon emissions, so carbon pricing initiatives such as emissions trading schemes (ETS), and carbon taxes are also likely to be key topics of conversation at COP26 (see On the Minds of Investors: The implications of carbon pricing initiatives for investors).

However, such discussions could lead to trade tensions as countries try to lay blame – and the need to change – at others’ doors. By country, China is the biggest emitter of greenhouse gases (EXHIBIT 8). But looking at the data by capita suggests the US has the most work to do. Others will argue the most appropriate comparison takes into account stages of economic development or reliance on manufacturing for GDP. This may hinder the group’s ability to agree on a common solution.

Obstacles to progress may prove particularly frustrating for Europe, which is far more advanced in this area, and keen to ensure that its own high regulatory standards are matched elsewhere, so that measures such as higher carbon prices in the EU don’t damage the profitability or competitiveness of the region’s companies (EXHIBIT 9). If the EU, China and the US cannot agree on a path towards a common carbon price, the EU may need to find a short-term solution to ensure that its climate efforts do not disadvantage European businesses.

One solution that appears to be growing in appeal in Europe is a carbon border adjustment mechanism (CBAM). This import tariff would be designed to ensure that the environmental footprint of a product was priced the same whether it was manufactured locally or imported.

Investors should be aware of how announcements at and after COP26 might influence their portfolios. Some companies will benefit from new green infrastructure investments, or from being relatively well prepared for the transition compared with their peers. Others may lose out – particularly firms that will face higher costs due to higher carbon prices, and especially if they are unable to pass these costs on in higher prices.

THEME 5 – SEEK PROTECTION FROM CHOPPY WATERS

As economies continue to open up, we are expecting a strong rebound in growth, with potentially sticky inflation. When central banks take their foot off the pedal and begin to apply the brakes, bond market returns suffer. The first quarter, which saw a loss of over 4% for US Treasuries – their largest quarterly drawdown since 1980 – is a case in point. With this backdrop, clients are wondering what role bonds should play in a balanced portfolio in the coming years (see On the Minds of Investors: Why and how to re-think the 60:40 portfolio).

There is no doubt that the return outlook for fixed income is challenging. In the past, the coupons that bonds paid at least cushioned the blow of rising rates. For example, during the Fed’s last hiking cycle (December 2015-December 2018), the price of US Treasuries fell by around 2% but the coupon paid over the period more than made up for that loss, such that total returns were still positive at around 4% over that period. Over the same period, global investment grade government bonds managed to return roughly 12%. Today, with starting yields and spreads so low, there is very little income to cushion against rising rates (EXHIBIT 10).

It might be tempting then to exclude bonds from portfolios altogether. However, that would lead to much higher portfolio volatility and little protection against unforeseen downside risks. For example, should the virus mutate to the extent that vaccines are no longer effective, government bonds would likely be one of the few assets generating positive returns.

In our view, investors should consider fixed income strategies that have the ability to invest globally in search of greater income protection, and which can move flexibly in the event of changing economic winds.

One global solution that, in our view, looks particularly attractive today is Chinese government bonds, which currently yield over 3% and benefit from a strong credit rating. A relatively low average duration also makes them less vulnerable to rising yields. Chinese bonds have proved to have a low correlation to both global bond and equity markets, making the market a good source of portfolio diversification (EXHIBIT 11). The Chinese onshore fixed income market is the second largest after the US Treasury market, but its representation in global benchmarks is still small. As its weighting grows, investors should benefit from the rising demand.

Beyond fixed income, investors can look to other alternatives for diversification. Macro strategies can adjust their correlation to equities and other asset classes and move dynamically according to changing market conditions. In periods of uncertainty – in which investors need portfolio protection – macro funds have historically outperformed equities (EXHIBIT 12).

The real market jitters would occur if a disorderly rise in inflation were to be realised. We view this as a tail risk, but given it would be unlikely to be good for either stocks or bonds, it’s one we should not be complacent about. Real estate and core infrastructure have low correlations to equity markets but their income streams are often tied to inflation, so can serve as a good inflation hedge. Of course, there are no free lunches, and such assets usually come with liquidity constraints, but those who can invest for the longer term may benefit from the inflation protection they can provide.

THEME 6 – CENTRAL PROJECTIONS AND RISKS FOR THE NEXT 6–12 MONTHS

Our core scenario is a continued recovery that broadens out and becomes more synchronised. Inflation worries provide some bumps, but monetary policy normalisation is slow. However, we remain in an unusual environment, and it’s as important as ever to keep an eye on the risks to our central view. On the positive side, inflation concerns could recede more quickly than we think as supply bottlenecks unstick, allowing central banks to remain accommodative for even longer. On the negative side, if those supply bottlenecks become more entrenched and vaccine progress falters, we could find ourselves dealing with stagflation.

Please check in again with us soon for further market updates and relevant content.

Please see the below piece from Invesco received late yesterday afternoon:

Key Points

As demonstrated by environmental protests against asset managers accused of “funding destruction”, the investment industry remains broadly perceived as uninterested in the existential challenges facing humanity.

Contrary to such perceptions, asset managers have taken a lead in promoting sustainable policies and practices – especially through active ownership of and engagement with the companies in which they invest.

It is vital that this “quiet revolution”, as the University of Cambridge has described it, builds wider recognition and that stakeholders of all kinds appreciate that their interests may be aligned with those of asset managers.

More than a decade on from the global financial crisis, the investment industry is still popularly perceived as a self-serving entity with little or no regard for the greater good. Before the COVID-19 pandemic curtailed mass gatherings, environmental activists’ demonstrations – including several against financial services companies said to have “funded destruction” – provided a clear reminder of how negatively this sphere is viewed by many of those outside it.

Former President of Ireland Mary Robinson, now a UN Special Envoy on El Niño and Climate, even suggested that Extinction Rebellion protesters should specifically target asset management firms. This tactic, she said, would lessen the likelihood of the group alienating members of the public.

Such a sentiment underscores the degree to which asset managers, routinely cast as essential cogs in the machinery of “big business”, are deemed complicit in many of the world’s ills. Yet it also implies that they can bring about positive change; and what appears to be consistently overlooked, at least in the mainstream narrative, is that this is exactly what they are doing.

The first decade of the 21st century exposed the limits of capitalism as we long knew it. There is no disputing this, just as there is no disputing that the resulting backlash against sections of the investment industry was deserved. Yet capitalism always has been and still is a work in progress: it has evolved substantively in seeking to avoid the errors of the past, and asset managers have been at the heart of the unfolding shift.

This is because responsibility, sustainability and long-term thinking are becoming norms for the sector. Asset managers are spearheading what the University of Cambridge has described as a “quiet revolution”, and the reality – unlikely though it might seem to some critics – is that many investment professionals have a deep and even long-held commitment to the future of the planet and its inhabitants.

A passion for the environment is not some sort of obligatory extension of work for such individuals. Quite the opposite: work is a potent augmentation of their passion for the environment. This should be acknowledged far beyond the industry – not because asset managers yearn to be loved or are tired of being harangued by climate campaigners but because stakeholders of every kind need to comprehend that there is a massively important alignment of interests here.

Contrary to widespread assumptions, asset managers are not fiercely determined to thwart efforts to make the world a better place. In fact, many want to be central to such endeavours. In this paper, drawing both on our own experiences and on insights from leading researchers, we seek to show that the quiet revolution is well under way; we attempt to highlight a more “human” side to the people behind it; and we try to explain why it merits much broader recognition.

Along with the investment industry in general, asset managers have attracted considerable criticism in recent years. With past sins still largely informing mainstream opinion, the scorn of the broader public – from environmental protesters to media commentators to the proverbial man and woman in the street – seemingly remains as strong as ever. Overturning such firmly entrenched disdain and distrust will not be straightforward. The investment industry as a whole has often made headlines for the wrong reasons, and the popular realisation that it has a much more admirable side will unquestionably take time to emerge.

The quiet revolution has been under way for several years. Maybe now is the time to make more noise about it – not for the sake of asset managers’ self-esteem, not because we demand due recognition, but because how we and our efforts are regarded and understood is likely to determine our effectiveness in helping plot a truly responsible course for the future.

This article is another indicator of the direction of travel within the industry. ‘Ethical’ and ‘Socially Responsible’ investment themes have always been there in the background, but over the past two years and especially since the onset of the pandemic, it no longer seems to be in the background.

Almost every fund manager now has to take into account ESG factors within their investments and portfolios whether they are doing so because they believe its right or because they now see that they have to in order to keep up, either way, its still a good push in the right direction.

People are waking up to making the world a better place, be it via social issues or climate issues.

Investors now seem to take comfort in the fact that they can help and ‘do their bit’ to help make the world a better place.

Please see below ‘Markets in a Minute’ article received from Brewin Dolphin yesterday evening, which provides a global update on markets and economic recovery as we strive towards a ‘new normal’ in a post-pandemic world.

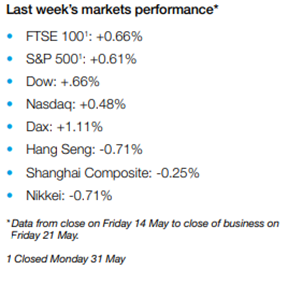

Most major stock markets rose last week despite figures showing US inflation surged in May to its highest level in 13 years.

The S&P 500 gained 0.4% to reach a new record high of 4,247, with healthcare stocks among the strongest performers. The technology-heavy Nasdaq added 1.9% as a sharp decrease in longer-term bond yields supported growth stocks.

The European Central Bank’s announcement that it would increase its pace of asset purchases boosted the pan-European STOXX 600, which ended the week up 1.1%. The UK’s FTSE 100 added 0.9% following encouraging GDP data, whereas Germany’s Dax was flat after figures revealed an unexpected decline in industrial production and factory orders.

Over in Asia, Japan’s Nikkei was largely unchanged after GDP shrank by an annualised 3.9% in the first quarter, better than the preliminary reading of a 5.1% contraction. China’s Shanghai Composite was also flat as investors weighed a fresh outbreak of Covid-19 cases in Guangzhou against renewed talks with the US on trade and investment links.

Investors shrug off lockdown easing delay

UK and European stocks continued to rise yesterday (14 June) despite reports that the UK was due to delay the final phase of lockdown easing. Prime minister Boris Johnson confirmed the reports in a briefing held after the market closed, saying restrictions would now be lifted on 19 July – four weeks later than originally planned.

The FTSE 100 added 0.2% on Monday, with strong oil prices helping the likes of Royal Dutch Shell, while travel and leisure stocks underperformed. The pan-European STOXX 600 also gained 0.2% to trade just off record highs. Most indices remained in the green at Tuesday’s open, with the FTSE 100 adding 0.3% amid a drop in the UK unemployment rate to 4.7%.

Over in the US, investors are turning their attention to the Federal Reserve’s upcoming policy decision and press conference on Wednesday. With inflation rising and the economy improving from its pandemic-era lows, investors will be closely monitoring Fed officials’ comments for any sign that it will begin easing its monetary and fiscal stimulus.

US inflation highest since 2008

Last week’s news was dominated by the latest US inflation figures, which revealed the headline consumer prices index (CPI) accelerated to an annual rate of 5.0% in May. This was higher than the 4.7% reading expected by economists and above April’s 4.2% figure. It marked the highest reading since August 2008 and partly reflected low base effects from last year when the coronavirus pandemic was at its peak.

Core inflation, which excludes volatile items like food and energy, leaped to 3.8% year-on-year, the highest level since 1992. On a monthly basis, consumer prices rose by 0.7% in May – well above the consensus forecast of 0.4%.

US stocks rallied despite the rise, suggesting investors agreed with the Federal Reserve’s stance that the current inflationary spike is transitory in nature. Indeed, the University of Michigan’s survey of consumer sentiment revealed Americans expect prices to rise by 4.0% in 2021, down from 4.6% in the previous month’s survey. The five-toten-year inflation outlook also fell to 2.8% from 3.0%.

Stock prices were also supported by an increase in the preliminary consumer sentiment index to 86.4 in the first half of June from a final reading of 82.9 in May. The gauge of current economic conditions edged up to 90.6 from 89.4, and the measure of consumer expectations rose to 83.8, the highest since February 2020.

UK GDP rises for third month in a row

Over in the UK, investors were cheered by the latest gross domestic product (GDP) data from the Office for National Statistics. GDP is estimated to have grown by 2.3% in April, marking the fastest monthly growth since July 2020. The service sector grew by 3.4% as consumer-facing services reopened in line with the easing of Covid-19 restrictions.

GDP remains 3.7% below the pre-pandemic levels seen in February 2020, but is now 1.2% above its initial recovery peak in October 2020. Compared with April 2020, the worst month of the pandemic, monthly GDP in April 2021 is estimated to have grown by a huge 27.6%.

ECB hikes inflation forecast

Elsewhere, the European Central Bank (ECB) announced it would increase the pace of its asset purchase programme over the coming weeks, despite calls from some policymakers to start reining in its monetary stimulus. It said bond purchases would continue at a ‘significantly higher’ pace than during the first few months of the year.

“Such a tightening would be premature and would pose a risk to the ongoing economic recovery,” said ECB president Christine Lagarde, adding it was too early to discuss when the emergency programme would end.

At the same time, the central bank increased its forecast for the harmonised index of consumer prices in the eurozone from 1.5% to 1.9% for 2021 but said the index would fall to 1.4% in 2023 as energy price rises evaporated. It also increased its forecast for economic growth in the euro area to 4.6% for 2021 and 4.7% for 2022. This comes amid falling Covid-19 infections, the lifting of lockdown restrictions, and a bounce back in business activity and consumer confidence.

Please check in with us again soon for further updates and relevant content.

Please see below for one of Invesco’s latest Investment Intelligence Updates, received by us yesterday 14/06/2021:

After April’s US CPI upside surprise, last week’s May reading was eagerly anticipated, albeit with a degree of trepidation. It didn’t disappoint. Headline CPI came in at 0.6%mom and 5%yoy, its highest level since 2008 (inflation peaked at 5.6%yoy then), while Core CPI rose even more at 0.7%mom, leaving it at 3.8%yoy, its highest since 1993. Both were 30bp above consensus expectations on a year-on-year basis. Strength was largely led by what are seen as “transitory” components, such as used cars (7.3%), car and truck rental (12.1%) and airfares (7%), even if there are other elements of consumer prices, such as shelter costs, that show more sustainable price pressures. Notwithstanding that we are probably close or at peak inflation as the impact of the lockdown starts to fall out of the calculation. How quickly and how far it will drop will be a function of whether rising costs, corporate pricing power and rising wages in a stimulus fuelled economy translate into more persistent inflation. For now, the Federal Reserve and increasing numbers of investors, witness a 10yr UST that is at its lowest level since early March, appear unconcerned about this risk. Time will tell whether this complacency is warranted or not, but it clearly remains a significant tail risk for financial markets.

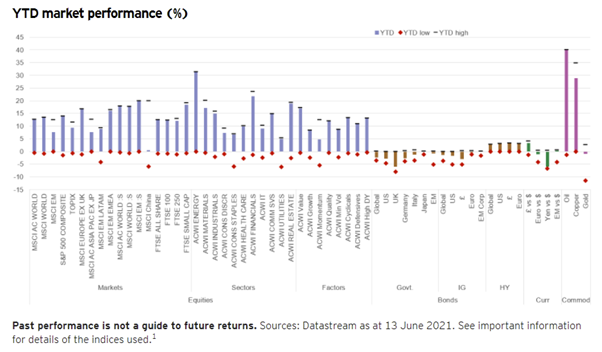

Global equity markets finished the week at a fresh all-time high, with a rise of 0.6% for MSCI ACWI. It is now up 12.7% YTD. DM (0.6%) led EM (flat), with both the US and Europe ex UK hitting new all-time highs, up 13.8% and 16.7% respectively YTD, with the latter the strongest major market of the week (1.2%). Small Caps (1.3%) outperformed again, hitting new all-time highs, with DM (1.3%) ahead of EM (1.1%). It was a rare week of Tech and tech-related sector outperformance, led by IT (1.6%). HealthCare (2.8%) was the best performing sector. Real Estate also had a good week (2.1%) and is now the third best performing sector YTD, up 18.8%, behind Energy and Financials. Lower bond yields weighed on Financial sector performance, while commodity sectors also lagged. Sector performance underpinned a strong relative performance week for Growth (1.4%) versus Value (-0.3%), while Quality (1%) had a good week too. UK equities were slightly ahead (All Share 0.9%) on the back of a good week for large caps (FTSE 100 0.9%) on strength in HealthCare, Telecoms and Energy.

Government bonds had a strong week with yields pushed lower by the belief that US inflationary pressures are transitory and a dovish stance at the latest ECB meeting. 10yr USTs and Gilts fell 10bp and 8bp respectively, taking them to their lowest levels since early March. They are now down 28bp and 18bp below their YTD highs, but are still higher than their starting level, hence the negative returns YTD from the asset class. Bunds and BTPs fell 6bp and 12bp. The better tone in government bond markets supported a good week for credit markets, where IG outperformed HY globally. IG yields fell 5bp with spreads narrowing by 2bp. The latter at 91bp are within touching distance of their post-GFC low (87bp). In HY a decline of 5bp in yields took them to all-time record lows (4.54%), but spreads at 353bp remain somewhat above their post-GFC lows (311bp).

The US$ edged higher over the week with the US Dollar Index up 0.5%, its third weekly gain, leaving it up 0.7% for the year. The Euro and £ were down -0.4% and -0.3% respectively.

Commodities overall were down slightly on the week with a -0.6% loss for the Bloomberg Commodity Spot Index, which is up just under 22% YTD. Brent, up 0.9%, hit its highest level ($73) in two years. In its latest monthly report, the IEA said that OPEC+ would need to boost output to meet demand that is set to recover to pre-pandemic levels by the end of 2022. Copper was up marginally too, 0.4% on the week, after a late rally on Friday as investors bet that China’s sales of strategic reserves would have a muted impact on demand. Gold edged lower (-0.6%) as it continued to consolidate around the $1900 level.

Andy Haldane, the Bank of England’s outgoing Chief Economist, described the UK’s housing market as being “on fire” last week. Recent House Price indices from the Halifax and Nationwide, the two biggest mortgage lenders, showed annual price growth of 9.6%yoy and 10.9%yoy respectively. These were the fastest rates of growth since 2007 and 2014 respectively and a lot faster than the rates of growth (3% and 3.5% CAGR respectively) seen in the decade leading up to the pandemic, described by another senior BoE official as housing’s “Quiet Decade”. And last Thursday’s RICS House Price Net Balance reading, which measures the breadth rather than magnitude of price falls or rises over the previous 3 months, hit +83% – its highest level since the housing boom of the late 1980s. Regionally it hit +100% in the N, NW and SW of England and Wales, while London was the standout laggard at just +46%.

All in all, a very uncharacteristic housing market, which typically fall and only recover slowly in severe economic contractions. This time around a combination of factors have delivered a very different market outturn: easing of lockdown restrictions have released pent-up demand. The government has supported the market through the Stamp Duty holiday (due to finish at the end of September), although it may not be as big a motivator for moving as some think. A recent survey by Rightmove shows that it is not the biggest motivation, with only 4% saying that they would abandon purchase plans if they missed the Stamp Duty deadline. Mortgage availability has improved, particularly for first-time buyers. Borrowing costs are low. Excess savings built up during the pandemic have provided cash for larger deposits. Finally, lifestyle factors (more space, relocating from large metropolitan areas) are at play. This has created an excess of demand over supply (the gap between new buyer enquiries and new instructions in the RICS survey was the widest since 2013) and, as with any commodity, when these imbalances occur prices tend to rise.

So, will the market remain “on fire”? In the RICS survey a national net balance of +45% envisage higher prices in the short-term (3m), while a greater +64% see them higher over 12m, although prices are only seen rising between 2-3%. Halifax and Nationwide also see the potential for further price rises in the coming months as most of the current demand drivers remain in place against a backdrop of a continued shortage of properties for sale. So, the fire may rage for a bit longer. Longer-term the RICS survey sees house prices appreciating by between 4-5% over the next 5 years. A still robust market, but certainly not to the same degree that we’re seeing currently. That would be a positive outturn for the economy.

Key economic data in the week ahead

The Federal Reserve and Bank of Japan meet this week to set their respective policy rates. Inflation data is a feature in both Japan and the UK this week, with the UK also publishing its latest employment report. In China economic activity for May is also released. Finally, there will be a number of post-G7 meetings in Europe next week, which may stir some interest, particularly those between the US and EU and Biden’s meeting with Putin.

In the US Retail Sales data for May is released on Tuesday. A decline of -0.6%mom is expected after no growth the previous month as the impact of pandemic-relief cheques faded. On Wednesday the Federal Reserve’s FOMC meets. While no change in policy is expected, market focus will be on its update of its economic projections, particularly any changes to the rates dot plot, employment and inflation projections (after two strong prints recently), as well as any clues on the future tapering of QE. Last week’s Initial Jobless Claims fell to a new pandemic low of 376k as the number of job openings has surged. On Thursday a further decline to 360k is expected.

There are a number of important data points this week in the UK. April’s Unemployment figures are published on Tuesday. A small decline to 4.7% from 4.8% is forecast. This compares to a recent high of 5.1% and 3.8% before the pandemic struck. On Wednesday May’s CPI will come out. Headline inflation is estimated to have increased 0.3%mom to 1.8%yoy mainly due to higher fuel prices. This will take inflation back to the levels seen immediately pre-pandemic. Core is also expected higher at 1.5%yoy from 1.3%yoy. So, both measures remain below the Bank of England’s 2% target. Retail Sales for May are released on Friday. After the non-essential shops re-opening bounce last month, a more sedate 1.6%mom is expected this month for sales ex Auto Fuel.

In Japan the Bank of Japan meets on Friday and is expected to keep its policy unchanged. CPI on the same day is forecast to have increased in May, but the Headline rate is still expected to be negative at -0.2%yoy, while Core is seen as flat, having fallen 0.1%yoy in April.

Chinese activity data for May is released on Wednesday. Industrial Production is forecast to have risen 9.2%yoy, slightly lower than 9.8%yoy in April. Retail Sales are also expected lower, but still strong at 14%yoy compared to 17.7%yoy in April. Fixed Asset Investment is seen up 17%yoy from 19.9%yoy last month.

There is no significant data coming from the EZ this week.

Please continue to utilise these blogs and expert insights to keep your own holistic view of the market up to date.

Please see the below article from AJ Bell received over the weekend:

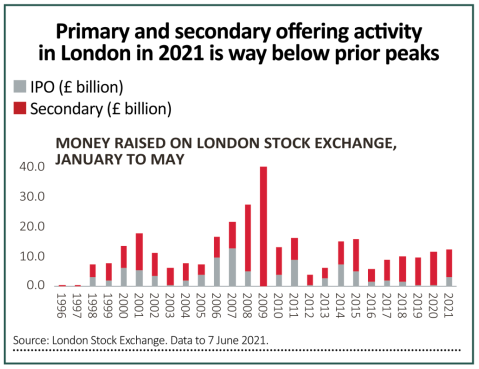

Fresh market listings raise questions about the risks of a downturn for equities.

The plunge into bankruptcy of the Softbank-backed, self-styled ‘construction industry disruptor’ Katerra spares investors in US equities the decision over whether to buy into what would have doubtless been an eventual IPO (initial public offering).

Katerra had been given ‘Unicorn’ status – a valuation in excess of $1 billion – before it ran out of cash, so investors may have ducked one there, although another Softbank firm, WeWork, is still seeking a US listing, albeit via a deal with a SPAC (special purpose acquisition company), rather than the more traditional flotation route.

This stuff really matters. As John Brooks wrote in his book The Go-Go Years: The Drama and Crashing Finale of Wall Street’s Bullish 60s: ‘If one fact is glaringly obvious in stock market history, it is that a new issues craze is the last stage of a dangerous boom.’

This is because sellers see their chance to cash out at inflated prices as buyers are lured in by rising markets and prevailing bullish sentiment.

The way in which multi-billion-dollar valuations at both WeWork and Katerra just melted away is perhaps confirmation of that warning and investors in UK equities might like to therefore keep a close eye on trends in the new listings market in London.

Hot and cold

The bad press surrounding the initial poor performance of both the Deliveroo (ROO) and Alphawave IP (AWE) flotations may suggest that the London market is far from overheating when it comes to new issues and that, as a result, such concerns may not be warranted.

If anything, the 43 IPOs to have taken place on the London Stock Exchange so far in 2021 appear to have struck a good balance. The average gain provided to those who were able to buy at the listing price is 24, although this column accepts the difficulties that private investors face in accessing IPOs is a major bugbear of many portfolio builders.

Nor does the amount of capital raised seem excessive, at £3.3 billion, according to data from the London Stock Exchange. This is the highest figure since 2015 but it pales compared to the £10 billion and £13 billion raised in the first five months of 2006 and 2007 respectively, after which trouble arrived in no uncertain terms, to again back up Brooks’ analysis of how the US equity boom of the 1960s came unstuck in the early 1970s.

The first five-month tally for 2021 also lags the boom of 2000 and 2001 as tech, media and telecom (TMT) companies rushed to list and sell stock to the unwary enthusiast.

Round two

Better still, the flow of secondary deals so far seems digestible, as companies whose shares are already listed have raised £9.5 billion in the year to date. It may be the highest figure since 2015 but again it lags the peaks of 2008-09 and 2000-02.

Even though share prices and valuations were collapsing, backers of technology firms were still willing sellers on the latter occasion because they knew the game was up. Perhaps therefore the real warning sign is not so much a rush of (potentially) dud IPOs but a string of secondary offerings that come regardless of how well – or badly – the IPO went.

Investors in Deliveroo and Alphawave IP should take particular note in this case, although this column was intrigued by commodities broker Marex Spectron’s decision to list on the London Stock Exchange. This could have been a good test of the current surge in commodity prices.

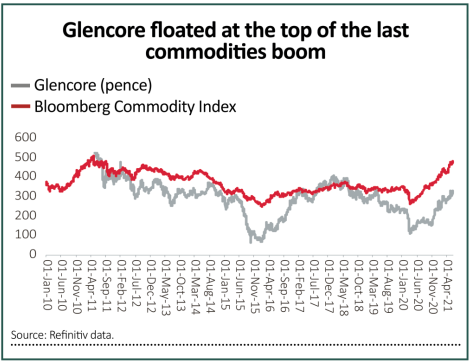

If anyone should know a good time to buy – or sell – it is surely a broker who is an expert in their field, so Marex’s move to give existing investors a chance to liquidate some of their investment now did look intriguing, given that the Bloomberg Commodity index is trading very close to its all-time highs of 2008 and 2011.

Smart money

Investors – and thus would-be buyers of the stock – could have be forgiven for asking themselves whether the sellers may know anything they do not and, as Shares went to press, the IPO was quietly pulled.

The last big commodity trader who came to market in London was Glencore (GLEN). It did so in 2011 – barely a month after the Bloomberg Commodity index peaked that April at 513, a level to which it is yet to return.

The aggregate amount of money raised by IPOs and secondary placings in 2021 to date is £12.8 billion. Investors have received over £8 billion from share buybacks and some £30 billion in dividends. Bull markets tend to wither when the money runs out and it does not look like we are reaching that stage, at least just yet.

Please continue to check back for further updates.

Please see article below from Invesco received late on Wednesday afternoon – 09/06/2021

Meet biodiversity: the next big thing?

Last week, on the 30th of May, the global conference on Biological Diversity (known as “COP15”) concluded in Kunming, China, with the aspiration to set global targets that would have become the “Net Zero for Nature”. Despite the postponement of the conference due to COVID, the urgency regarding the need to halt and reverse biodiversity loss is growing more acute.

The destruction of natural habitats, shrinking animal populations and even species extinctions are now widely regarded as part of a global crisis. The World Economic Forum’s Global Risks Report 2021 placed the loss of biodiversity in its top five existential risks, alongside global pandemics, climate change and weapons of mass destruction.

Inevitably, and rightly, the issue of biodiversity is set to play an important role in finance and investment, as regulation and public awareness require investment funds to take account of this vital issue in investment decisions.

Statistics on biodiversity tell their own story. The World Wildlife Fund’s (WWF) Living Planet Report 2020 catalogued the scale of the issue. Between 1970 and 2016 the planet experienced:

A 68% average decline in global vertebrate species populations.

An 84% decline in freshwater wildlife populations.

17% of the Amazon rainforest has been lost to deforestation.

Biodiversity is vital for the stability of the environment. Agricultural production and food security depend upon the wider ecology of plant and animal life. Biodiversity also plays a role in resisting disease and 25% of medicines are derived from rainforest plants.

Loss of biodiversity may force animals to live in closer proximity to both each other and humans, enabling the emergence and spread of disease. Water supplies, soil fertility and countless livelihoods depend upon biodiversity – there is a lot riding on its protection.

The clock is ticking on disclosure

While biodiversity is an issue across all business and industry, certain sectors and activities are on the front line. The United Nations’ 2019 Global Resources Outlook concluded the extraction and processing of natural resources – largely mining and farming – are responsible for 90% of global biodiversity loss. The deforestation of the Amazon to make way for beef farming is the most notorious example.

Within the broad issue of environmental protection, biodiversity is increasingly recognised as a key issue alongside climate change. For that reason, the role of the financial services sector in protecting and financing biodiversity is coming under the spotlight. Regulators are increasingly including biodiversity as a topic for financial firms to disclose on. For example, the European Union’s Sustainable Finance Directive Regulations (SFDR) specifically identifies biodiversity as one of the Principle Adverse Impacts (PAIs) the financial sector must address. Beyond disclosure, the issue increasingly being raised by regulators as a potential financial stability risk, with the Network for Greening the Financial System, comprised of global central banks and financial regulators, recently announced a work programme to study the financial stability risks arising from biodiversity.

How can investment be measured for biodiversity?

The effect of business activities on biodiversity is a complex matter to assess and hard data is in short supply. Numerous initiatives are currently underway to try to bridge this gap, by identifying appropriate metrics for measure biodiversity and natural capital. This includes the Taskforce on Nature-related Disclosures (TNFD), which, it is hoped will do for biodiversity what the Taskforce on Climate-related Disclosures (TCFD) did for climate change.

One pioneering organisation has been the FAIRR (Farm Animal Investment Risk & Return) Initiative that carries out research into environmental impacts and provides best practice tools for investors. The initiative is backed by a network of investment groups including Invesco.

FAIRR’s Protein Producer Index assesses the effect of industrial scale farming on the environment and biodiversity. Its latest report, in November last year, assessed 60 of the world’s largest food producers and found that more than 80% of land-based food producers posed a high risk of deforestation and loss of biodiversity1.

Its report also identified the links between major food producers and those companies closer to the consumer, such as McDonald’s and a range of supermarkets including Tesco, Sainsbury and Walmart.

As formal regulations and disclosures become part of the investment landscape over the coming years, assessments on biodiversity, such as those by FAIRR, TNFD, CDP (formerly the Carbon Disclosure Project) and others, are likely to become crucial in shaping investment strategies. Consumer awareness is also likely to rise, particularly as the links between production and consumer brands are made more transparent.

As governments and industry increasingly agree, the loss of biodiversity poses a grave risk to the global ecology and to the global economy. Consumer concern and rigorous regulation on impacts and disclosures are set to make biodiversity an important factor in sustainability and in company valuations. They will also become an essential theme for the investment strategies of the future.

The interconnectedness of existential threats means that the ripple effects can encompass concerns including deforestation, biodiversity loss, waste pollution, climate change and our own health.

Please continue to check back for more on ESG and socially responsible investing along with our latest blog posts and market updates.

Please see below an article on Divorce Law reforms from FT Adviser, which caught my eye as this is an area of advice we get involved in and I think helps highlight just how long it can this process can take:

Couples seeking a no fault divorce under new legislation will now have to wait until 2022, the government has confirmed.

The implementation of the Divorce, Dissolution and Separation Act will now come into force on April 6, 2022, not in October as the government had originally planned.

In a written answer to a question posed by Conservative MP Jane Stevenson, published yesterday (June 7), Chris Philp, parliamentary under secretary of state at the Ministry of Justice, said the original implementation date had been “ambitious”, although the bill received Royal Assent in June 2020.

He said the government had started work to identify, design and build the necessary amendments to court forms and also to amend the online digital divorce service while rules are being finalised.

But he admitted these amendments will not be finished before the end of the year.

Philp said: “The Ministry of Justice is committed to ensuring that the amended digital service allows for a smooth transition from the existing service which has reformed the way divorce is administered in the courts and improved the service received by divorcing couples at a traumatic point in their lives.

“Following detailed design work, it is now clear that these amendments, along with the full and rigorous testing of the new system ahead of implementation, will not conclude before the end of the year.

“While this delay is unfortunate it is essential that we take the time to get this right.”

The no-fault law will require divorcing couples to provide a statement of irretrievable breakdown and replace the need for evidence of conduct, such as adultery or unreasonable behaviour, or proof of separation.

According to the government, the act provides for the biggest reform of divorce law in 50 years and will reduce conflict between couples legally ending a marriage or civil partnership as they will no longer have to blame each other for the breakdown.

A Ministry of Justice spokesperson said: “Our changes will help divorcing couples to resolve their issues amicably by ending the needless ‘blame game’ that can exacerbate conflict and damage a child’s upbringing.

“These measures represent the biggest reform to divorce laws in 50 years, so it is right that we take time to ensure they are implemented as smoothly as possible.”

Alongside the no fault rules, the Divorce, Dissolution and Separation Act will remove the possibility of contesting the decision to divorce, as a statement will be conclusive evidence that the marriage has irretrievably broken down.

It also introduces a minimum period of 20 weeks from the start of proceedings to confirmation to the court that a conditional order of divorce may be made.

Kate Daly, co founder of divorce service Amicable, said: “We’re disappointed to hear the no fault divorce bill is due to be delayed until 2022. It’s the biggest reform to UK divorce law in 50 years, so we cannot afford to rush it, but we see first-hand the emotional toll that divorce proceedings can cause when conducted in an acrimonious, fault-finding manner.”

She added: “At Amicable, we have helped thousands of people untie the knot harmoniously, and many of people we have spoken to are holding off until the new laws come into place. Waiting longer could prove incredibly challenging emotionally, and has additional implications such as not being able to finalise financial arrangements.

“The Ministry of Justice should solve these technical issues as a priority to help people reach productive agreements.”

This latest deferral frustrates those awaiting amendments to what is already a lengthy and emotional process. This deferral doesn’t help reaching a financial settlement, including what assets, such as Pensions, that need to be included and what split is appropriate.

This is a complicated subject matter and something I will be writing about in greater detail via additional blogs over the coming weeks to show where we can add value and how we can help once the divorce is finalised.

Please continue to check our Blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.

Please see below ‘Markets in a Minute’ article received from Brewin Dolphin yesterday evening, which provides an overview of current market behaviour in reaction to global economic developments.

Most global stock markets edged higher last week as oil prices surged and data pointed to strong economic growth in the months ahead.

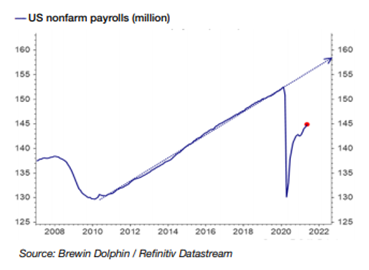

In the US, the S&P 500 ended its four-day week up 0.6% after crude oil prices climbed to their highest level for more than two years, boosting energy stocks. Share prices were also lifted by Friday’s weaker-than-expected US nonfarm payrolls report, which helped to alleviate fears of a shift in the Federal Reserve’s policy stance.

Over in Europe, the STOXX 600 added 0.8%, Germany’s Dax rose 1.1% and France’s CAC 40 gained 0.5% after the final purchasing managers’ survey for the eurozone suggested GDP would rise strongly in the second and third quarters. The UK’s FTSE 100, which was closed last Monday for the spring bank holiday, rose 0.7% despite concerns that the Delta variant of Covid-19 would delay the final lifting of lockdown restrictions.

The extension of the Covid-19 state of emergency in several prefectures in Japan weighed on the Nikkei 225, which declined 0.7%. China’s Shanghai Composite slipped 0.2%, ending a three-week run of gains.

Investors shrug off weak Chinese data

Most indices managed to hold on to gains yesterday (Monday 7 June) despite weaker-than-expected Chinese trade data. China’s imports grew by 51.1% in May from a year earlier, below the 54.5% growth predicted by analysts in a Bloomberg poll. Exports slowed to 27.9% in May from 32.3% in April, missing analysts’ forecasts of 32.1% growth.

Nevertheless, Asian markets closed in the black on Monday, with the Shanghai Composite and Nikkei 225 advancing 0.2% and 0.3%, respectively. The panEuropean STOXX 600 also erased earlier losses to close up 0.2%. News that UK house prices rose to a new peak in May boosted housebuilders, helping the FTSE 100 finish Monday’s session 0.1% higher.

UK and European shares were broadly higher at Tuesday’s open, although a fall in German factory output knocked 0.1% off the Dax.

US adds fewer jobs than expected

Last week saw the release of the closely watched US nonfarm payrolls report, which revealed the US added 559,000 jobs in May – fewer than the 675,000 extra jobs that economists were expecting. Economists had already lowered their forecasts following the huge miss in April when 278,000 jobs were added versus an expected one million jobs.

Labour participation in May was also lower than expected at 61.6%, below the pre-pandemic level of 63.4%. The number of unemployed stood at 9.3m, far higher than the pre-pandemic level of 5.7m.

However, the report wasn’t all doom and gloom. Job growth in May was driven by the services sector, with leisure and hospitality adding 292,000 new jobs, which is a further sign that the economy is normalising as vaccines are rolled out. In addition, the unemployment rate fell from 6.1% to 5.8%, and the number of permanent and temporary layoffs declined.

Overall, the report showed that while the US jobs market is improving it isn’t ‘overheating’, which would likely be the trigger for the Fed to tighten its monetary policy.

Eurozone services sector growth surges

Growth in the eurozone’s services sector hit a three-year high in May as lockdown restrictions eased. IHS Markit’s eurozone services PMI rose to 55.2 from 50.5 in April, marking the third successive month of expansion. Ireland and Spain saw the fastest growth, while Germany saw the slowest.

The composite PMI, which also includes manufacturing, surged to 57.1 in May from 53.8 in April, while business optimism for the year ahead hit the highest level for more than 17 years.

Chris Williamson, chief business economist at IHS Markit, said: “The service sector revival accompanies a booming manufacturing sector, meaning GDP should rise strongly in the second quarter. With a survey record build-up of work-in-hand to be followed by the further loosening of Covid restrictions in the coming months, growth is likely to be even more impressive in the third quarter.”

UK house price growth hits double digits UK annual house price growth rose to 10.9% in May – the highest level in nearly seven years. On a monthly basis, prices rose by 1.8% following a 2.3% rise in April. The average house price is now £242,832, an increase of £23,930 over the past 12 months, according to Nationwide.

The lender said the UK’s housing market has achieved a complete turnaround over the past 12 months. A year ago, activity collapsed in the wake of the first lockdown with housing transactions falling to a record low of 42,000 in April 2020. Activity surged towards the end of last year and into 2021, reaching a record high of 183,000 in March.

Robert Gardner, Nationwide’s chief economist, said the extension to the stamp duty holiday isn’t the key factor behind the spike in transactions, although it is impacting the timing.

“Amongst homeowners surveyed at the end of April that were either moving home or considering a move, three quarters (68%) said this would have been the case even if the stamp duty holiday had not been extended,” he stated. “It is shifting housing preferences which is continuing to drive activity, with people reassessing their needs in the wake of the pandemic.”

We will continue to publish relevant content and news as the vaccination drive in the UK is extended to include those aged 25 or over.

Please see below for Brooks MacDonald’s latest market update, received by us yesterday evening 07/06/2021:

Last Friday’s US jobs report missed expectations but the figures were welcomed by markets

With the EU vaccination programme progressing well, this week’s European Central Bank (ECB) meeting will be closely watched

US Consumer Price Index (CPI) on Thursday is arguably the most important data release so far in 2021

Last Friday’s US jobs report missed expectations but the figures were welcomed by markets

Equities ended the week strongly, despite the US jobs report coming in behind expectations. Growth equities were a particular beneficiary after the non-farm payroll report was released on Friday.

The May US employment report missed expectations but only mildly compared to the miss in April’s figures. May saw c.559,000 new jobs created on a headline basis and c.496,000 of those within the private sector1. Describing the gain, Federal Reserve Bank of Cleveland President Mester said that while the figures were positive, they fell short of substantial further progress which is the bar set by the Federal Reserve to consider tapering2. Beneath the numbers, the labour force participation rate fell, which may suggest that there is some hesitancy to return to workplaces or that stimulus measures have reduced the need to return to the workforce short term. The jobs report saw US 10-year Treasury yields fall as market participants priced in a slightly slower than expected recovery, which is showing fewer signs of acute labour shortages. It is those labour shortages that are particularly relevant given their role in driving supply side inflation as employers compete for workers.

With the EU vaccination programme progressing well, this week’s European Central Bank (ECB) meeting will be closely watched

This week’s main event is undoubtedly the US CPI number on Thursday, and this arguably represents the most important data release so far in 2021. Consensus estimates point to a 0.4% month-on-month increase in both the headline and core inflation rate, which would mean that core US inflation would move to 3.4% year-on-year3. This would be the highest level of core inflation since 19934. Of course, the massive reduction in economic activity last year skews these figures and this release, alongside June’s, sees a substantial uptick in inflation due to this ‘base effect’ alone. Thursday also sees the ECB’s meeting where the central bank, under less inflation pressure than the US, is likely to continue with its faster pace of asset purchases, for the short term at least. As the EU vaccination drive continues to gain momentum, an exit of this pandemic quantitative easing programme may be on the cards but probably not until the last quarter of this year.

US Consumer Price Index (CPI) on Thursday is arguably the most important data release so far in 2021

The US CPI number will be very closely watched by markets, not only for the core inflation figure but also what is driving the subcomponents. Last month, used cars were an outsized contributor to the figures but investors will be looking for signs of a broader increase in price pressures.

Please continue to utilise these blogs and expert insights to keep your own holistic view of the market up to date.