Please see below for Brewin Dolphin’s latest markets in a minute article, received by us yesterday evening 27/04/2021:

Most major stock markets declined last week on fears that rising Covid-19 infections could hinder economic recovery.

With Europe firmly in the grip of the so-called ‘third wave’, the pan-European STOXX 600 ended the week down 0.8%, while Germany’s Dax fell 1.2% and France’s CAC 40 declined 0.5%. The UK’s FTSE 100 slid 1.2%, with positive economic data failing to lift investors’ spirits.

Rising infections also weighed on Japan’s Nikkei, which dropped 2.2% after the country reported nationwide daily infections of more than 5,000 for the first time in three months. This led to another state of emergency being declared in several prefectures.

US stock markets posted small declines last week after President Joe Biden announced proposals to nearly double taxes on capital gains for those earning more than $1m a year. In contrast, Chinese stock markets posted solid gains following strong inflows from Hong Kong via the Stock Connect trading programme.

Last week’s markets performance*

- FTSE 100: -1.2%

- S&P 500: -0.1%

- Dow: -0.5%

- Nasdaq: -0.3%

- Dax: -1.2%

- Hang Seng: +0.4%

- Shanghai Composite: +1.4%

- Nikkei: -2.2%

* Data from close on Friday 16 April to close of business on Friday 23 April.

European stocks gain on travel plans

UK and European stocks rose on Monday after European Commission president Ursula von der Leyen told the New York Times that inoculated Americans will be able to visit the EU in the summer. The STOXX 600 added 0.3% and the FTSE rose 0.4%, with shares in easyJet, Ryanair and TUI all posting strong gains.

In the US, the Dow slipped 0.2% whereas the S&P 500 and the Nasdaq rose 0.2% and 0.9%, respectively. Tesla started a busy week of corporate earnings statements, reporting a 74% surge in quarterly revenues. Apple, Microsoft, Amazon, Alphabet, Boeing and Ford are all due to release first quarter results this week.

HSBC and BP were in focus at the start of trading on Tuesday, with the former posting a 79% rise in first quarter pre-tax profit, and the latter receiving an earnings bump from higher oil prices and a surge in revenue from natural gas trading. The FTSE 100 opened flat ahead of the US Federal Reserve’s two-day policy meeting.

UK economy shows signs of rebound

Last week saw the release of several pieces of economic data that suggest the UK economy is starting to rebound from the Covid-19 crisis. Friday’s IHS Markit/CIPS flash composite PMI showed a strong revival in private sector output following the downturn seen at the start of 2021. The index rose to 60.0 in April from 56.4 in March – the strongest overall rise in private sector output since November 2013.

For the first time since the pandemic began, service activity growth outperformed manufacturing production growth. The service sub-index rose from 56.3 to 60.1, marking the fastest pace of expansion for more than sixand-a-half years. The manufacturing sub-index increased from 58.9 to 60.7, the highest since July 1994.

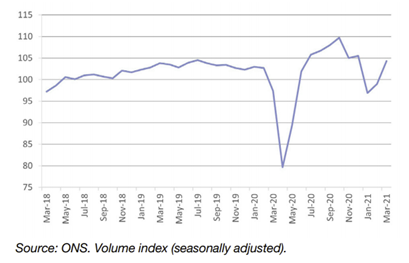

Separate data from the Office for National Statistics (ONS) showed UK retail sales volumes continued to recover in March, increasing by 5.4% from the previous month. This reflected the easing of Covid-19 restrictions on consumer spending. Sales were 1.6% higher than in February 2020 – the month before the pandemic struck.

UK retail sales surge 5.4% in March

Non-food stores provided the largest positive contribution to the monthly growth, with increases of 17.5% and 13.4% in clothing stores and other non-food stores, respectively. Fuel retailers reported monthly growth of 11.1%.

However, the ONS said retail sales for the quarter were subdued overall. In the three months to March, sales fell by 5.8% when compared with the previous three months because of tighter lockdown restrictions.

US economy moving to post-pandemic state

Last week’s flurry of US corporate earnings reports suggest the economy is starting to transition to life after the pandemic. Most notably, Netflix announced it had added just under four million subscribers in the first quarter – missing its forecast of six million. The company said it expected one million paid net additions for the second quarter – versus ten million in the second quarter of 2020, when it benefitted from a surge in demand at the beginning of the crisis.

Elsewhere, figures showed US weekly jobless claims fell to their lowest level since the onset of the pandemic, declining by 39,000 to 547,000 in the week ending 17 April. This was far better than the 617,000 figure. forecast by analysts.

US existing home sales declined by 3.7% between February and March to a seven-month low, largely because of the acute shortage of houses on the market. Compared with a year ago, when home sales first started to fall when the pandemic hit, sales were 12.3% higher. Limited supply and strong demand pushed the median existing home sales price by a record-breaking annual pace of 17.2% to an historic high of $329,100, the National Association of Realtors said.

Eurozone manufacturing enjoys record boom

Over in the eurozone, business activity in April experienced its fastest rate of increase since July 2020, thanks to record expansion in manufacturing output and a return to growth in the service sector. The composite PMI rose from 53.2 in March to 53.7 in April, according to IHS Markit’s preliminary ‘flash’ reading, which is based on around 85% of final responses to the survey.

Manufacturing output grew for a tenth straight month, expanding at a rate unsurpassed in more than two decades of survey history. The service sector continued to lag because of Covid-19 restrictions in many member states, but still reported the first expansion of activity since August 2020, rising from 49.6 in March to 50.3 in April.

Please continue to utilise these blogs and expert insights to keep your own holistic view of the market up to date.

Keep safe and well.

Paul Green DipFA

28/04/2021