Please see below for the latest Brooks MacDonald Daily Investment Bulletin received by us today 21/01/2021:

What has happened

Markets greeted the inauguration of Joe Biden with a rally driven by the tech heavyweights. Some markets concerns remained around the final handover of Presidential power from Trump to Biden so there will be an element of welcoming the calmer tone of the new President as well as removing a transition risk premium.

President Biden

Yesterday’s inaugural Presidential address saw President Biden attempt to change the tone in Washington by encouraging bipartisan debate rather than absolutism. This speech was followed by a series of executive orders as expected. This included the US re-joining the Paris climate agreement, ceasing the withdrawal from the WHO, ending the travel ban on a number of Muslin countries and a federal mask rule on interstate travel and within federal buildings. As a sign of the focus for the new administration’s economic goals, there were also some specific COVID support measures such as pausing federal student loan repayments and extending the federal eviction moratorium. Yesterday’s speech, coupled with that of Janet Yellen earlier this week, paints a market friendly picture where near term support remains the focus. Of course, the sting in the tail could be higher taxes down the line but we need to remind ourselves of the thin Senate majority and the fact the midterms are in November next year and this could change the power balance in Congress yet again.

Central bank decisions

Yesterday we heard from the Bank of Japan which left monetary policy unchanged whilst predicting economic challenges over the course of 2021. Today is the turn of the ECB and given the central bank announced a further easing package in December, little dramatic change is expected. The central bank meets under the cloud of Euro Area CPI estimates that showed the region in deflation (-0.3%) compared to the year before. Whilst forward looking CPI estimates have been rising, in line with the broad global market reflation narrative, even these future estimates remain well below the ECB’s 2% target. The central bank therefore likely has room to increase stimulus but it isn’t clear that simply doing more of what has been tried before (bank lending, negative rates and quantitative easing) will have the desired effect.

What does Brooks Macdonald think

Equities rose and volatility fell as power transitioned peacefully between President Trump and President Biden. It is interesting that yesterday’s rally was so tech focused given fears over regulation under a Democrat White House and Congress. The rally yesterday implies that investors are confident the new administration has its hands full with the COVID response and is unlikely to look towards market unfriendly reform within that context.

Daily investment bulletins like this could prove to be very useful in the near future. Yesterday’s Presidential Inauguration is sure to cause ripples in the markets globally and keeping up to date with developments as they happen can, as ever, be very beneficial to your own views of the markets.

Please utilise our blogs in keeping your own views of the market holistic and up to date.

Please see the below update from Brewin Dolphin received late last night:

Most global markets fell back slightly over the past week, retreating from record highs set in the first trading week of the year. The falls came after a strong run for global markets that has, unsurprisingly, led to some profit taking. Also weighing on markets has been some disappointing economic data caused by new or expanded lockdowns.

For example, UK retail sales figures released last week saw the worst annual growth since 1955. US initial jobless claims increased sharply last Thursday, hitting their highest level in five months. US retail sales declined for a third straight month and manufacturing activity in the New York state slowed. Then the University of Michigan consumer sentiment index was weaker than had been expected. It is no surprise that markets have adopted a little more of a ‘risk off’ tone.

Last week’s markets performance*

FTSE100: -2%

S&P500: -1.47%

Dow: -0.91%

Nasdaq: -1.54%

Dax: -1.86

Hang Seng: +2.49%

Shanghai Composite: -0.10%

Nikkei: +1.35%**

*Data from close on 8 January to close of business on Friday 15 January.

Inauguration week starts on a cautious note

It was a quiet start to the week yesterday, as US markets were closed for Martin Luther King Jr Day. In Europe, markets were mostly higher; the pan-European STOXX 600 rose by 0.20%, France’s CAC 40 closed 0.44% higher at 13,848.35 and the Italy’s FTSE Mib gained 0.53% to 22,498.89.

In Asia, most markets lost ground, but China was the exception. The Shanghai Composite and Hang Seng indices both rose after China reported robust GDP data that confirmed it was the only major economy to expand in 2020.

In the UK, the FTSE100 closed down 0.22% at 6,720.65, while the FTSE250 eked out a gain of 0.12%.

China leads global recovery

China’s ongoing recovery continued apace at the end of last year. It recorded GDP growth of 2.3% for 2020 as a whole but growth accelerated in the fourth quarter, with its economy expanding by 6.5% compared to a year earlier. It was its fastest rate of growth in two years.

China’s growth was largely export driven, although government support for infrastructure projects also gave the economy a boost.

But even China is showing signs of pain during these difficult days. Retail sales came in below expectations, rising by 4.6% in December from a year earlier. While this is impressive by global standards, it was below expectations for 5.5% growth.

We expect China to continue to lead the global recovery in 2021, although growth should be more evenly spread around the world, assuming the roll out of vaccines proceeds smoothly.

Bond yields rising

Yields were a little lower on the back of this news, but not much. That is despite the very sharp increase in yields we have seen so far this year. This has been a topic of much speculation as the prevailing narrative had been that rates will stay low for the foreseeable future. However, very recently the market has begun to anticipate that monetary policy cannot remain this accommodative forever.

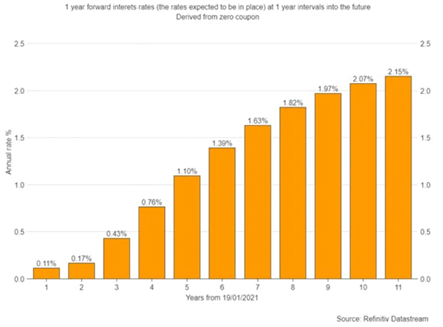

Currently forward interest rates presume that rates stay on hold for the next two years, but then begin to steadily rise. Implied rates have increased significantly over the beginning of the year, mainly in the US. Now those expectations have nudged outside the upper end of the Fed’s forecast range. The chart below shows the market implied interest rate for each year into the future.

Adding to the pressure on bond yields recently has been the fact that some forecasters have brought forward their expectations around the timing of the Fed beginning to slow down its bond purchases, or quantitative easing (QE).

Atlanta Fed president Raphael Bostic, who is about to become a voter on the FOMC, recently said that if the economy bounces back quickly, the Fed may be able to start paring back QE later this year. During the so-called ‘taper tantrum’ of 2013, the 10-year Treasury shot up around 130 basis points in just a few months. There are certainly some parallels between then and the backdrop today, so the bond market is highly sensitive to any discussion about the Fed altering the pace of its bond buying, which is currently at $120 billion per month.

Biden’s stimulus proposal

One of the factors weighing on the bond market is the prospect of extra fiscal stimulus. President-elect Biden announced his plan for spending, and it is eye-watering, at $1.9trn.

He has said he wants $2,000 stimulus cheques for individuals in addition to the $600 cheques already passed by Congress. It also includes $400 a week in emergency unemployment benefits, payable until September, and preventing a cliff-edge cut-off for jobless payments previously scheduled for March.

More controversially he also wants to more than double the minimum wage. This probably isn’t a serious proposition. It’s more of an effort to establish an anchor from which he can give a little ground and still be left with something meaningful at the end of the negotiation.

Inflation expectations on the up

Fundamentally, it has been rising inflation expectations that have been the driving force behind higher yields. Inflation is likely to look as if it is increasing over the coming months, but appearances will be misleading. Year-on-year energy prices will appear to have risen sharply in March when current oil prices are compared to those from a year ago, when prices actually went negative! But this is just a base effect.

There will also be some inflation caused by the reimposition of VAT in some jurisdictions. Statistical factors even imply that there is wage inflation in the current market because job losses in a large number of low-paid roles means that average wages are higher now than they were in 2019. None of these are real inflation, and policy makers will be able to safely ignore them – although headline writers may not.

Overall core inflation remains subdued, but it would be very unusual for it not to rise a little given the increase in manufacturing activity we have seen. In the longer term, more inflationary pressures may build, but for now a gentle increase in inflation gives us a preference for inflation-linked bonds over conventional bonds and reinforces the importance of having some precious metals exposure as a useful hedge.

Brief market updates like this help us get a quick overview of the markets and we share them in the aim of keeping our readers informed.

Today will be a historic day given that, across the pond, it is President Biden and Vice President, Kamala Harris’ Inauguration. VP Kamala Harris will today make history as the first female, first black and first Asian-American US Vice President, a great step towards a more inclusive and diverse future!

Hopefully, we could see positive market movements on the back of this, however, the markets are unpredictable (as have been the events of the world over the past 12 months).

Keep checking back with us for more updates like this.