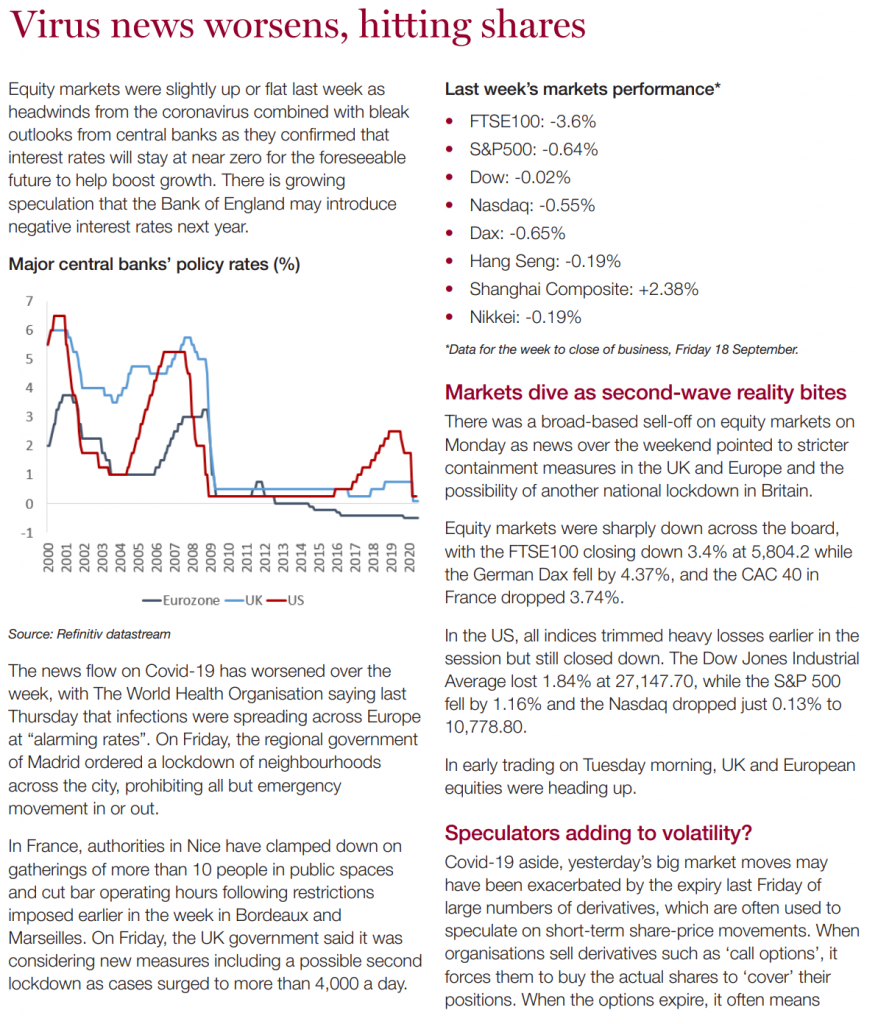

Please see below for the latest blog from Legal and General’s Investment Management Team regarding their ‘key beliefs’ regarding the markets:

Forward looking

It may seem difficult when faced with the latest political developments and a second wave of COVID-19, but investors need to be forward looking. If markets are indeed relatively efficient pricing mechanisms, we shouldn’t focus too much on what’s happening today; instead we need to think about what could happen tomorrow and beyond.

As with all Key Beliefs emails, this email represents solely the investment views of LGIM’s Asset Allocation team.

Pent-up demand unleashed

From an equity perspective, the losers from social distancing have been hit hardest by the pandemic. But if and when consumer behaviour normalises, these stocks should also benefit disproportionately.

In the spring and summer, such a recovery felt too distant for the travel and leisure sector, so we preferred other laggards like autos and small-caps. But as time has passed, we now expect generally positive macro news over the coming three to nine months (on vaccines, rapid testing and regulatory decisions) to start becoming a tailwind for this sector as well.

While we have no edge on the specific events, market expectations do not look excessive: sentiment is still bearish on the sector and performance has remained underwhelming and stuck in the middle of the post-pandemic range.

A vaccine should help these stocks in two ways: through de-risking the future path of their earnings, and through upgrades to earnings estimates if consumers resume their past behaviours faster than expected. This has already happened for other sectors, perhaps helped by some pent-up demand after the lockdown.

That’s not to say there are no risks to this trade. A greater-than-expected second wave could further delay a restart, customers could reject the changes made to the travel and leisure experience, or outbreaks on cruises could set back the wider sector.

But we believe that being closer to a potential turning point in the news flow, without having seen any meaningful outperformance for the sector, makes the risk/reward dynamics attractive enough for a first step.

Powerful gambit

European Commission President Ursula von der Leyen gave her annual State of the Union address last week. Invoking Margaret Thatcher in an argument with a Conservative British Prime Minister was a bold but powerful gambit. In the words of the original Iron Lady back in 1975, “Britain does not break treaties. It would be bad for Britain, bad for relations with the rest of the world, and bad for any future treaty on trade.” The sense of frustration with the shenanigans in Westminster is obvious.

It is tempting to think that the latest dispute is terminal for the prospect of a successful conclusion to trade talks. But the nature of brinkmanship is that it drives matters to the brink. Almost all European negotiations go to the 11th hour or beyond, so it is pretty hard to infer anything definitive at this stage.

If forced to pick a direction for sterling from here, we think appreciation is more likely than further depreciation. Portfolios naturally heavy on foreign currency therefore need to be increasingly mindful of a “rabbit out of the hat” moment driving the pound higher.

For non-Brexit obsessives, von der Leyen also had some interesting things to say about green bonds and carbon objectives. The EU is set to embark on an unprecedented issuance spree to finance the recently agreed Recovery Fund. Up to 30% of the planned €750 billion will be raised via green bonds. In the short term, we think the surge of EU issuance risks driving up yields in ‘semi-core’ European nations like France. Over the longer term, given that the green-bond market totals around $400 billion outstanding today, this will really bring the asset class into the mainstream.

Off the charts

We have highlighted the TIM Monitor a few times in previous Key Beliefs as one of a number of quantitative risk environment indicators that we use. The monitor aims to provide a characterisation of the current market environment and the likelihood of extreme losses going forward based on the combined information from two indicators: the Systemic Risk Index, which measures equity market fragility, and the Turbulence Index, a measure of ‘unusualness’ in global equity returns.

Needless to say, equity markets proved to be both fragile and extremely unusual in the first quarter, so much so that the TIM Monitor was quite literally off the charts. The monitor moved into ‘Alert’ territory on 25 February, with the S&P 500 down by around 7.5% from its peak at that point. After that, the S&P 500 fell a further 30% to its low on 23 March. The monitor remained in ‘Alert’, with the Systemic Risk Index remaining uncomfortably high, until 17th August when it finally switched back to ‘Warning’, almost exactly at the time that US equities returned to their previous highs. So, it was a timely indicator to get out of equities, but a bit slow to get back in again.

The length of its tenure in ‘Alert’ territory in part reflects the fact that a small number of key drivers propelled the market back up again – swift and comprehensive monetary policy responses over the past decade have had a tendency to do exactly that in times of stress. But we must also acknowledge that it is partly down to how the Systemic Risk Index is constructed, as it is an intentionally (sometimes painfully) slow-moving indicator.

Within an investment process involving judgement, these types of frameworks can be extremely useful in providing a different lens through which to view the world. Each one comes with its own nuances, however, and hence we believe they are best used in combination with other metrics rather than in isolation.

Detailed and focussed opinions from market leading investment managers such as Legal and General can be a useful addition to your overall view of the markets.

Please keep reading our blogs to ensure your holistic view of the markets is well informed, diversified and up to date.

Keep safe and well

Paul Green

23/09/2020

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}