Please see below for the latest Blackfinch Group Monday Market Update:

UK COMMENTARY

Boris Johnson unveiled a three-tier lockdown system to help control the spread of a second wave of infections

A lack of progress on a Brexit trade agreement saw Johnson suggest that the country should prepare for a ‘no-deal’ outcome

The three months to the end of August saw Britain’s unemployment rate rise to 4.5%, the Office for National Statistics (ONS) said, versus expectations of 4.3%

After a record low of 343,000 vacancies in April to June, there has been an estimated quarterly increase to 488,000 vacancies in July to September 2020. Vacancies, however, remain below pre-pandemic levels and are 332,000 less than a year ago.

The latest grocery market share figures from Kantar for the four weeks to October 4th show that sales growth rose by 10.6%, which is expected to be a result of the threat of another national lockdown. Shoppers spent an additional £261mln on alcohol as the 10pm curfew came into effect and the Eat Out to Help Out scheme concluded.

ONS data suggested that labour productivity, as measured by output per hour, fell 1.8% year-on-year. Output per worker fell by 21.1%, but it is expected that this is a result of the furlough scheme allowing employers to retain workers even though they are working no hours.

US COMMENTARY

The market continues to wait patiently for any news on a further government stimulus package. However some solace can be taken in the fact that no matter who wins the presidential election next month, there will likely be a sizeable fiscal stimulus package announced.

Third quarter earnings season started, giving investors much to digest, with the main area of focus being the level of recovery that companies have seen since the depths of the economic fallout from the pandemic

First time jobless claims increased to 898,000, the consensus forecast had been for a drop to 825,000. Continuing claims fell from 10.98mln to 10.02mln, a greater fall than had been anticipated by the market.

Retail sales rose 1.9%, well ahead of estimates, although industrial production showed a 0.6% decline in September.

ASIA COMMENTARY

On Tuesday 13th, Hong Kong’s stock market was unexpectedly closed as a tropical storm prompted authorities to shutter businesses and close schools

GLOBAL COMMENTARY

The International Monetary Fund has upgraded its GDP forecasts for this year. In its latest World Economic Outlook it predicts that global output will fall by 4.4% in 2020, better than the 5.2% slump forecast in June.

The largest shift was in the prediction for the US, with GDP seen shrinking by 4.3%, not the 8% previously anticipated

Improvements are also seen in the forecasts for Europe, the UK and China, with the fund saying that these changes are due to a “somewhat less dire” slump in the April-June quarter, and a stronger than expected recovery in July-September

Emerging markets saw their forecast fall, with a prediction for a 5.7% contraction, worse than the previously suggested 5% slump

The report also suggests that as a result of the pandemic 80-90mln more people will be pushed into extreme poverty globally.

COVID-19 COMMENTARY

Johnson & Johnson are forced to pause their COVID-19 vaccine trial due to ‘an unexplained illness in a study participant’

Pfizer and BioNTech have indicated that they could file for emergency use authorisation from the US Food and Drug Administration by late November for their jointly developed vaccine.

These articles provide concise well-informed views that cover the whole of the market and are useful to maintain your up to date view of the markets globally.

Please keep reading our blogs regularly to give yourself a holistic and up to date view of the markets.

Please see below for the latest blog from Legal and General’s Investment Management Team regarding their ‘key beliefs’ regarding the markets:

Forward looking

It may seem difficult when faced with the latest political developments and a second wave of COVID-19, but investors need to be forward looking. If markets are indeed relatively efficient pricing mechanisms, we shouldn’t focus too much on what’s happening today; instead we need to think about what could happen tomorrow and beyond.

As with all Key Beliefs emails, this email represents solely the investment views of LGIM’s Asset Allocation team.

Pent-up demand unleashed

From an equity perspective, the losers from social distancing have been hit hardest by the pandemic. But if and when consumer behaviour normalises, these stocks should also benefit disproportionately.

In the spring and summer, such a recovery felt too distant for the travel and leisure sector, so we preferred other laggards like autos and small-caps. But as time has passed, we now expect generally positive macro news over the coming three to nine months (on vaccines, rapid testing and regulatory decisions) to start becoming a tailwind for this sector as well.

While we have no edge on the specific events, market expectations do not look excessive: sentiment is still bearish on the sector and performance has remained underwhelming and stuck in the middle of the post-pandemic range.

A vaccine should help these stocks in two ways: through de-risking the future path of their earnings, and through upgrades to earnings estimates if consumers resume their past behaviours faster than expected. This has already happened for other sectors, perhaps helped by some pent-up demand after the lockdown.

That’s not to say there are no risks to this trade. A greater-than-expected second wave could further delay a restart, customers could reject the changes made to the travel and leisure experience, or outbreaks on cruises could set back the wider sector.

But we believe that being closer to a potential turning point in the news flow, without having seen any meaningful outperformance for the sector, makes the risk/reward dynamics attractive enough for a first step.

Powerful gambit

European Commission President Ursula von der Leyen gave her annual State of the Union address last week. Invoking Margaret Thatcher in an argument with a Conservative British Prime Minister was a bold but powerful gambit. In the words of the original Iron Lady back in 1975, “Britain does not break treaties. It would be bad for Britain, bad for relations with the rest of the world, and bad for any future treaty on trade.” The sense of frustration with the shenanigans in Westminster is obvious.

It is tempting to think that the latest dispute is terminal for the prospect of a successful conclusion to trade talks. But the nature of brinkmanship is that it drives matters to the brink. Almost all European negotiations go to the 11th hour or beyond, so it is pretty hard to infer anything definitive at this stage.

If forced to pick a direction for sterling from here, we think appreciation is more likely than further depreciation. Portfolios naturally heavy on foreign currency therefore need to be increasingly mindful of a “rabbit out of the hat” moment driving the pound higher.

For non-Brexit obsessives, von der Leyen also had some interesting things to say about green bonds and carbon objectives. The EU is set to embark on an unprecedented issuance spree to finance the recently agreed Recovery Fund. Up to 30% of the planned €750 billion will be raised via green bonds. In the short term, we think the surge of EU issuance risks driving up yields in ‘semi-core’ European nations like France. Over the longer term, given that the green-bond market totals around $400 billion outstanding today, this will really bring the asset class into the mainstream.

Off the charts

We have highlighted the TIM Monitor a few times in previous Key Beliefs as one of a number of quantitative risk environment indicators that we use. The monitor aims to provide a characterisation of the current market environment and the likelihood of extreme losses going forward based on the combined information from two indicators: the Systemic Risk Index, which measures equity market fragility, and the Turbulence Index, a measure of ‘unusualness’ in global equity returns.

Needless to say, equity markets proved to be both fragile and extremely unusual in the first quarter, so much so that the TIM Monitor was quite literally off the charts. The monitor moved into ‘Alert’ territory on 25 February, with the S&P 500 down by around 7.5% from its peak at that point. After that, the S&P 500 fell a further 30% to its low on 23 March. The monitor remained in ‘Alert’, with the Systemic Risk Index remaining uncomfortably high, until 17th August when it finally switched back to ‘Warning’, almost exactly at the time that US equities returned to their previous highs. So, it was a timely indicator to get out of equities, but a bit slow to get back in again.

The length of its tenure in ‘Alert’ territory in part reflects the fact that a small number of key drivers propelled the market back up again – swift and comprehensive monetary policy responses over the past decade have had a tendency to do exactly that in times of stress. But we must also acknowledge that it is partly down to how the Systemic Risk Index is constructed, as it is an intentionally (sometimes painfully) slow-moving indicator.

Within an investment process involving judgement, these types of frameworks can be extremely useful in providing a different lens through which to view the world. Each one comes with its own nuances, however, and hence we believe they are best used in combination with other metrics rather than in isolation.

Detailed and focussed opinions from market leading investment managers such as Legal and General can be a useful addition to your overall view of the markets.

Please keep reading our blogs to ensure your holistic view of the markets is well informed, diversified and up to date.

Please see below for this week’s market update received from Blackfinch Asset Management earlier today:

In the ever-changing world that we live in, we recognise the importance of regular and current communication. This weekly news update from our MPS Portfolio Managers provides you with a short summary of events around the world which we hope you will find useful.

Issue 5 | 24th August, 2020

UK COMMENTARY

The IHS Markit UK Household Finance Index fell to 40.8 in August from 41.5 in July.

UK retail sales increased by 3.6% in July and are now 3% above the pre-pandemic levels seen in February. Online sales numbers fell by 7.0%, but remain 50.4% higher than in February.

The IHS Markit Composite Purchasing Managers’ Index (PMI) for August rose to 60.3 from 57.0 in July, the fastest rate of business activity expansion since October 2013.

UK retail footfall showed a weekly increase of 0.8%, following a 3.8% increase the week before. Market research group Springboard suggest the slowdown in growth could be attributable to the hot weather.

Market research group Kantar released data showing that the grocery market grew by 14.4% in the 12 weeks to the 9th August, with households averaging 14 shopping trips per month.

Inflation, measured by the Consumer Price Index (CPI), rose unexpectedly to 1.1% in July, driven by an increase in culture and recreation costs, analysts had predicted a reading of 0.7%.

A Reuters survey of economists suggests that the UK economy will take at least two years to recover from the impact of COVID-19.

US COMMENTARY

US/China trade talks are cancelled, President Trump signs an executive order forcing TikTok developer ByteDance to sell off its US operations within 90 days and announces further tightening of restrictions on Huawei.

The S&P 500 reached record levels, stopping just short of closing above the 3,400 level.

Apple becomes the first company to reach a market capitalisation of US$2trn.

News on the next tranche of stimulus from the US government fails to materialise for another week.

Minutes from the Federal Reserve offer little encouragement, stating that the pandemic could have a ‘considerable’ impact on the US economic outlook for the medium term. The Federal Reserve also offer no further guidance on interest rates, reiterating that they will remain low for ‘a very long time’.

First-time unemployment claims rise by 135,000, counteracting the previous week’s fall.

ASIA COMMENTARY

The Chinese Central Bank added 700bn Yuan (c.£76bn) to their medium-term lending facility for commercial lenders in order to help liquidity, helping to boost sentiment.

Japanese Gross Domestic Product (GDP) shrinks at 7.8% on a seasonally-adjusted quarterly basis, the third consecutive quarter of negative growth.

These articles are useful for breaking down market input into sectors. This facilitates an all-round view of the markets from the experts in a quick and efficient format.

Please use these blogs to keep your own view of the markets up to date from a variety of different sources.

Please see below for Jupiter Asset management’s latest ‘Active Minds’ article received by us late on the 22nd July 2020:

Jason Pidcock

Head of Strategy, Asian Income

China’s recovery drives Asian bull market

The bull market in Asia continues, noted Jason Pidcock, Head of Strategy, Asian Income. We’ve seen lots of large index constituents in China and Hong Kong rallying sharply, with some reaching all-time highs. Some people may find this a bit ironic given the negative political news coming out of China and Hong Kong, but this hasn’t prevented capital from flowing into those markets. Jason highlighted that this isn’t just in terms of domestic inflows – foreign capital is also buying Chinese and Hong Kong stocks.

What’s really driving Asian equities is the V-shaped recovery in China’s economy, said Jason. China is in a better position than many other economies, with second-quarter GDP up 3.2% year on year, following a contraction of 6.8% in the first quarter. So, it’s on track with expectations for a full recovery from the decline sometime in the second half of the year. Lots of Chinese businesses are doing well, too. Companies are forecasting profit growth and they’ve got strong balance sheets. While many parts of the world are seeing dividend cuts, many Chinese companies are not cutting dividends, and furthermore, many are actually growing their dividends, partly because of their net cash positions.

There’s been minimum impact from recent geopolitical tensions on Hong Kong, too. The UK symbolically suspended its extradition treaty with Hong Kong and placed it under an arms embargo, and the US has officially removed Hong Kong’s special trade status. Economic impact will be quite minimal though, as it should only affect about 1% of Hong Kong’s total exports. The Hong Kong dollar peg is unlikely (and technically difficult) to change, and capital flows into Hong Kong have gone up sharply since the announcement of the drafting of the National Security Law at the end of May. Hong Kong has had to lock down the economy to a degree because of a new flare up in virus cases, but most people are seeing this as temporary; it’s not having a big impact on most of the larger-weighted stocks listed there.

Overall, Jason expects to see Asia Pacific equities continue to trend higher; within the region, it’s Northeast Asia that’s driving growth.

Chris Smith

Fund Manager, UK Growth

Why aren’t supermarkets making more profit?

The UK has been the worst performing major developed market year to date, said Chris Smith, Fund Manager, UK Growth. That in itself isn’t so remarkable, as the UK has lagged behind major global peers for much of the last five years, but Chris said that the magnitude of the underperformance has accelerated in 2020. The reason for this is partly because the UK stock market has a larger exposure to structurally challenged or cyclical sectors, such as oil majors and financials, than many of its peers, and not much of a technology sector.

So, if the UK market faces so many challenges, where can a stock picker investing in UK stocks look for opportunities? Chris used a couple of examples to illustrate where he does, and does not, find attractive stock ideas in this environment.

At first glance, supermarkets seem like one of the winners from the Covid-19 pandemic, registering record like-for-like sale growth in many cases as shoppers stockpiled ahead of lockdown. Chris, however, sees them as structurally challenged ‘old world’ businesses. Despite that record sales growth, supermarket profits are forecast to be broadly flat year-on-year in the UK. This is because the increased sales were focused on low margin staples, and office workers, tourists etc staying at home means supermarkets are selling far fewer high margin items such as ‘on the go’ convenience food and drink. Online deliveries have gone up significantly, but this also has a dilutive effect on margins, as purchases are again focused on low margin items and the costs of fulfilling orders are higher than for in-store purchases.

Ultimately, Chris doesn’t see supermarkets as an attractive long-term investment for a growth investor like him. More attractive, however, is the testing and certification industry. It is essentially an oligopoly, with three major players all experiencing strong organic growth across the cycle from 2006-2019. The industry is also exposed to a lot of long-term structural growth trends, such as more regulation, higher safety standards, ESG in the supply chain, and cybersecurity, among others.

Richard Watts

Head of Strategy, UK Small & Mid Caps

UK midcaps – go where the growth is

Richard Watts, Head of Strategy, UK Small & Mid Caps, also discussed the UK’s recent underperformance, noting that the domestically-biased FTSE 250 Index is down around 25% year to date, which is significantly worse than the 16% decline of the more international FTSE 100 Index.

In turn, the UK stock market is trading at a 25% discount to its long-term average against the broad global equity market as represented by the MSCI World Index. This valuation trough is at its lowest since World War II, so it does look cheap. The UK market has also hugely underperformed relative to where government bond yields are so, in Richard’s view, the market looks very good value.

Part of the malaise is down to the weakness of the pound and its volatility against a backdrop of Brexit uncertainty in particular hurting many midcap stocks, which collectively are more exposed to the economically-sensitive parts of the economy (housebuilders, engineers, travel companies, pubs and restaurants) than the FTSE 100 Index. More recently it has also reflected the outlook for dividends, as many companies had to cut dividends or cancel them to access government support schemes.

In the small and midcap strategy, Richard and the team have been overweight in structural growth for some time – it’s been clear that the pandemic has greatly accelerated the shift towards online retailing, pulling forward some two to three years of growth. This is having a very positive impact on the earnings of such companies and the strategy. And it’s no surprise that the team is underweight in travel, store-based retailers, pubs and restaurants, as they think consumers are still very nervous. This can be seen in the number of restaurant table bookings (not) being made. The team expects pub like-for-like sales to be down around 40% year-on-year, so they are wary of having too much exposure to these areas. Instead, they are seeking economically-sensitive exposure through those businesses that they believe will emerge from the crisis in better shape and which are not reliant on consumer spending where, in their view, it will take time for confidence to recover.

Joel Ojdana

Credit Analyst, Fixed Income

Don’t miss the double-B boat

Double-B credit offers great opportunities in today’s US high yield market, said Joel Ojdana, Credit Analyst, Fixed Income. Classed as the better-quality end of high yield credit, these businesses are well suited to the ‘new normal.’ In a world where negative real rates imply a slow global recovery, and with enormous debt at both the corporate and sovereign level likely to dampen productivity, these better-quality balance sheets and businesses should benefit.

Unprecedented support from the Federal Reserve also continues to drive spreads tighter, said Joel, and has opened up a financing window to corporate borrowers that is not at all typical during a ‘normal’ recession. With more monetary support expected by the market, BB-credit spreads are likely to further compress, in Joel’s view, offering a great opportunity. That said, it’s important to discriminate, because the pandemic has created both winners and losers within the US high yield segment – the Technology and Utilities sectors have outperformed year to date, while the Energy and Transport sectors have plummeted, for example. Finally, BB-rated corporates also frequently issue 10-year bonds, which is typically the longest duration in the high yield market and therefore should offer the most potential upside if spreads do tighten further.

These articles are useful for breaking down input into sectors, allowing experts of their particular sectors to offer insight within their specified field. This facilitates an all-round view of the markets.

Please keep reading these blogs to keep your own view of the markets up to date.

Please see article below from Brewin Dolphin’s ‘Markets in a Minute’ update received 15/07/2020.

China shares rally as state media declares bull market

Global share markets were mixed over the past week, although China has been a standout performer after investors piled in, encouraged by a state-owned newspaper that effectively declared a “healthy” bull market was on the way in Chinese equities.

Investors took the message to heart, and Chinese shares surged by almost 6% at the start of last week on trade volumes roughly double the average.

In the UK, a rally late in the week lifted the FTSE100 comfortably above the 6,000 level but performance in most markets was fairly muted due to the ongoing downbeat news around the coronavirus, worries about tensions between the US and China, and uncertainty around stimulus packages.

Last week’s markets performance*

FTSE100: -1%

Dow Jones: 0.95%**

S&P500: 1.75%**

Dax: 0.84%

Nikkei: -0.07%

Hang Seng: 1.4%

Shanghai Composite: 7.3%

*Performance in the week to Friday 10 July **Performance from close of business on 2 July to Friday 10 July due to Independence Day holiday.

A mixed start to this week…

Share markets largely continued their bullish run on Monday, with the FTSE100 gaining 1.33% and European markets hitting their best levels in almost a month as reports suggested progress on two vaccine candidates in the US. China and other Asian markets continued their strong run.

However, the S&P500 and the Nasdaq in the US both closed down yesterday amid worries about the rolling back of reopening plans in some states due to rising coronavirus cases. That led to Asian markets falling sharply today.

Chinese policymakers have also become uneasy about the rapid rise in Chinese stocks, leading to two state-backed funds to begin offloading equities in a bid to cool the overheating market. The Chinese government has also sought to dissuade investors from accessing unauthorised sources of margin financing. The Shanghai Composite closed down by 0.8% today. In early trading in the UK and Europe, shares were heading down.

Stimulus cliff-edge in US, knife-edge summit in Europe

There can be no doubt that both the US and Europe need more stimulus to maintain their recovery, or at least prevent a sharp deterioration. In the US, a central plank of March’s $2trn stimulus package is being debated; the extra $600-a-week in unemployment benefits, which is paid on top of each state’s existing unemployment benefits, is due to end on July 31. This means a potential cliff-edge income drop for around 20m unemployed Americans that would cause average unemployment payments to fall by about 60%. Also, cash payments to households have already been received, and probably spent.

Fortunately, both the Democrats and Republicans want the extra stimulus to keep flowing, so it is more than likely we will see these benefits extended.

This coming Friday the EU will debate the €750bn coronavirus recovery package at a special summit, and it is far from certain the fund, dubbed Next Generation EU, will pass in its current size or format – the current proposal is that the fund is made up of grants and loans, and more fiscally conservative states, particularly the Netherlands, are objecting to the grants element and also, reportedly, the size of the package.

Virus news

While the headline figures from case growth around the world, and particularly the US, still make dire reading, a glimmer of hope can be seen in the decline in Swedish cases, although this could be for any number of reasons (less testing, some more lockdown measures). Crucially, however, there was an important suggestion that immunity may have spread more widely than believed, which has global implications.

Marcus Buggert of The Centre for Infectious Medicine at Karolinska Institutet, Sweden, said: “Our results indicate that roughly twice as many people have developed T-cell immunity compared with those who we can detect antibodies in.”

Apparently, this could mean herd immunity is achievable with far lower infection rates of, say, 20% rather than the 60% suggested more commonly.

Overall the trends in Covid cases may be improving but it is hard to say due to fluctuations in testing and the distortion of the Independence Day holiday in the US. Even outside Sweden, European cases seem to have been suppressed for now. The case growth rate in Brazil could be peaking but there is little sign of any improvement in Mexico, South Africa or India.

In Asia, after a week in which Tokyo recorded 100 new cases per day, they subsequently jumped more than 200 on Thursday. Hong Kong will close its schools early for the summer holidays after finding 34 new locally transmitted cases on Thursday.

On the vaccine front, research into T-cell immunity is now being incorporated into vaccine development, in addition to the focus on antibodies we have seen so far. If successful, this could significantly boost any vaccination’s efficacy and the duration of immunity, though it is still very early days.

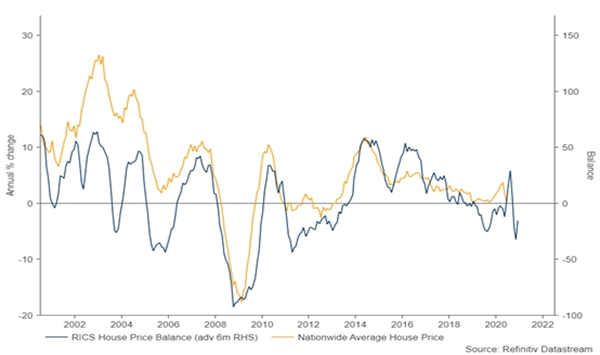

Summer statement boosts housing sector

In his summer statement last week, Chancellor Rishi Sunak refused to extend the government’s furlough scheme past October as widely expected, but he announced a stamp duty holiday until next March for properties worth up to £500,000. That boosted shares in housebuilders, and it may prompt an uptick in housing transactions. New buyer enquiries at estate agents were close to record levels in June, according to last week’s survey from the Royal Institution of Chartered Surveyors. Its survey, which questions surveyors around the country, suggested a slight recovery in prices and a big increase in properties being listed for sale. But looking ahead, views were a little more negative, implying price declines of 5% over the remainder of the year.

New buyer enquiries vs Nationwide average house price

RICS House price balance vs Nationwide average house price

Make the most of higher-rate tax relief in your pension while you can

Sunak hinted that efforts to address the dire situation that is the national finances will begin in November’s Budget. This may finally sound the death knell for one of the most attractive tax breaks in the UK, namely higher-rate tax relief on pension contributions.

It’s hard to see any more obvious revenue-raising step that would be so effective, and it has been speculated about for a decade. It would suggest anybody who hasn’t taken advantage of this year’s allowance should seriously consider doing so before the autumn.

One of the main focuses of this update are the views on potential monetary and fiscal policy actions from governments, particularly the UK, EU, China and US. It now seems that market analysts have turned their attention to how governments will act to deal with the financial consequences of this pandemic in the long term and how that will affect the markets as they begin to recover.

Please see below for Royal London’s latest market update received 29/06/2020. They provide an update on the impact of recent market events:

RLAM Economic Viewpoint

Survey data, high frequency data and now increasingly the hard data too, continue to show that developed economies are in the ‘recovery phase’ of this crisis. Albeit this is the somewhat mechanical bit as economies are allowed to open up and you get a bit of pent-up demand set loose as well. Some of the recent data points have shown much stronger than expected improvements. This, however, doesn’t tell us much about the next stage of the recovery that economists generally expect to be much slower. Social distancing, scarring (including permanent job losses, business closures and balance sheet damage) and residual fear of the virus (including as it relates to job security) will all influence the strength of that recovery and government policy still has a crucial role to play in all of them.

June business surveys improve substantially: Data in the past week or two has included several June business surveys and these have mostly seen solid improvements, with some notable upside surprises in European business surveys and US regional business surveys. However, the headline composite PMI business survey indicators for the US, eurozone, Japan and the UK remain below 50. Taken at face value, remaining below 50.0 would normally signal that these economies are still shrinking. However, mapping PMIs accurately to economic activity levels is somewhat hazardous after such a big shock to GDP (the survey asks whether things are better/worse, rather than by how much). Nevertheless, if you look at the commentary in the PMI surveys – social distancing has eased, helping many firms reopen and firms are more optimistic, but many companies also report weak demand as customers remain cautious. That is – so far – consistent with economies taking time (likely, several quarters) to get back to ‘normal’ levels of activity after a sharp initial recovery phase.

US data continue to suggest a strong start to the early stage recovery, but virus data more worrying: May retail sales, durable goods orders and some housing data have bounced significantly more than expected. However, US COVID-19 numbers have, in the meantime, become more worrying. The increase in virus cases in some states is likely to worry consumers, including the prospects of social distancing being reversed and the impact on job security. Meanwhile, Congress and the White House have still not agreed a package of economic support measures to replace those set to roll off this summer. US government policy interventions have so far done a good job in shielding household balance sheets (and therefore spending power) from the crisis. Reduced/disrupted fiscal support and the progression of the virus both have the potential to curb US recovery momentum.

Here in the UK, data also signal a solid start to the recovery phase but also a weak underlying labour market and an economy still in need of policy support: May retail sales were also an upside surprise, rising 12% in May. They are still 13.1% below February levels, but that’s a solid start to the recovery phase, especially since it was only mid-June that saw ‘non-essential’ retail stores reopen. Just as in the US, however, the UK’s early stage recovery has needed – and still needs – plenty of policy support. Government borrowing was also somewhat higher than expected in May and the levels of government debt as a percent of GDP, on the headline measure, moved above 100% for the first time since 1963. PAYE data meanwhile show the number of paid employees fell by 449K March to April. Early May estimates indicate another drop of 163K. Job vacancies in May fell to a record low. The furlough scheme is set to start unwinding from August, but this is a labour market that is far from out of the woods yet. That was recognised by the Bank of England who extended their asset purchase programme, though reduced the pace. They have become more concerned about long-term damage from the crisis. How the labour market evolves from here will be a key driver of their decisions going forward including, potentially, a decision around negative rates.

Market view from Piers Hillier, CIO, RLAM

The upwards trend in global equity markets was met with some resistance this week, resulting in sideways equity trading and moderate credit spread widening. Investors were perturbed by a sharp increase in Covid-19 cases in the US as the country reported a record number of new cases on Thursday. While the coronavirus appears to be under control in most developed countries at this stage, global new case numbers are at record highs; driven by the US, Brazil and India. In an effort to mitigate the damage of a second wave, US regulators gave in to a long-sought demand for a relaxation of the Volcker Rule as they allowed banks to invest in hedge funds and private equity funds.

Markets have also been rocked by increased global trading tensions. There have been signs of further difficulties in the trade negotiations between the US and China. Meanwhile the US threatened to impose tariffs on $3.1bn of European products, prompting an angry response from the European Commission.

On a more positive note, numerous key economic data releases have been far stronger than anticipated recently. There have been strong improvements in US and UK retail sales and in the European and US business surveys. While activity surveys are still consistent with contractions in many economies, possibly reflecting the elevated corporate debt and unemployment levels, they show that businesses are markedly more upbeat as they emerge from the worst of the lockdowns.

Reflecting a perception that the UK economy is somewhat stronger than expected, the Bank of England surprised investors at its latest meeting. While it announced an additional £100bn of bond buying, as had been expected, it slowed the pace of its purchases. The Bank said it would spend the £100bn by the end of the year, rather than by the end of August as the market had hoped. Of course, the very fact that spending was increased reveals the fragile state that the Bank considers the economy to be in, with serious concerns over the unemployment outlook.

The focus for many in the UK has been on further opening of businesses – both non-essential retail in mid June, and with the prospects of pubs, restaurants and others opening from early July. As investors we are pleased to see this – we are under no illusions that we as a society will return to prior habits in terms of spending; many of us will feel differently about being on a train, plane or in a restaurant for some time. And with other countries seeing flare-ups in the virus, it is clear that this road will have a number of bumps in it. However, it does appear that we are now through the first phase of this crisis, and returning to a more normal cycle of data and market reaction.

Royal London is the UK’s largest mutual life, pensions and investment company. This in-depth market outlook by a market leading financial services organisation adds valuable insight to our consensus view of the markets. It is evident that in recent times these views have been dominated by the Coronavirus Pandemic, but we have also now been offered insight into the socio-political tensions that have recently risen, particularly in the US, and how they in turn are effecting the economy. This is an example of how frequently reviewing these updates gives us a better view of the ‘bigger picture’.

The opinions of market leaders are key to keeping our understanding of the markets up to date. A wide variety of these views from different sources help us paint a more accurate picture on the events of the world and how they are influencing market behaviours.

Please see the below investment outlook received from J.P. Morgan today (Tuesday 23rd June):

In Brief

In early June the market was pricing in a V-shaped recovery from the pandemic-driven economic contraction. We expect the recovery to be more gradual, with a few stop-starts along the way. Extremely low interest rates will help, but unemployment and corporate deleveraging could be a drag on growth.

The extent of near-term uncertainty, as well as the potential for political risk to mount as we approach the US election, could generate more market volatility.

For individual market sectors, the outlook depends on the path of the pandemic. If a full and sustainable reopening of the economy becomes possible, we may see a further rally for the most beaten-up sectors, coupled with a style rotation. For now, we believe it makes sense to maintain a nimble approach, with a focus on quality and an eye to ESG risks.

Low-risk options for income seekers are increasingly scarce. Rather than stretching for yield, investors may be better off being selective within fixed income and using a wider range of income-providing asset classes, including real assets for those who can accept lower liquidity.

Developed market government bonds look less and less likely to play their traditional roles of providing income and protecting portfolios in periods of market stress. Investors may need to look beyond the traditional 60:40 portfolio, with a greater role for alternatives and flexible fixed income strategies.

No one predicted that in the first half of 2020 the world’s economies would be brought to a virtual standstill by a global pandemic. Even had we have known the virus was coming, we would not have predicted that by mid-year the S&P 500 would have managed to climb back above 3000 (EXHIBIT 1).

We have global policymakers to thank for the market’s resilience. According to current analysts’ expectations, the policy response has helped one-year forward earnings expectations to find a floor and start to improve. In the sharp rally since 23 March, markets looked to be pricing that the combined actions of governments and central banks in recent months will have successfully absorbed the economic losses of Covid-19 to engineer the perfect V-shaped recovery (EXHIBIT 2).

While the policy response has been commendable, we believe the market’s expectation of the recovery in early June was too optimistic. It’s not that we believe people will permanently change their behaviour – we are social animals, after all. We just think it will take a little longer to get back to full normality.

Chief among our concerns is that the virus itself may linger and some need for social distancing will remain, in countries such as the US and UK, at least. In addition, high unemployment and a dramatic increase in public and private debt may serve to restrain spending in the recovery. We may also be at the beginning of a period of difficult political fallout as politicians seek to apportion blame for the crisis. The US election of 3 November could have important market implications. With the UK having left the EU but not yet having secured a new trade deal, Brexit might also – once again – generate volatility.

In summary, we acknowledge that the commitment from governments and central banks shouldn’t be underestimated. And, if more stimulus is needed, it will come. This makes us cautious about being underweight risk assets. But we need to see that policy action is influencing fundamentals. Valuations and uncertainty around the economic and earnings outlook make us cautious about advocating an overweight position in equities. We therefore think investors may benefit from having more than one toe in this rally, but not from jumping in with two feet.

In what follows, we provide greater information on our view of the shape of the recovery. We then consider three investment themes for the second half of the year:

1) Considerations for investors in the near term, given uncertainties and potential volatility

2) Options for investors in need of income

3) Rethinking a 60:40 portfolio in a world of zero bond yields

WHAT SHAPE WILL THE RECOVERY TAKE?

As shutdowns are eased around the world, forecasters are debating the likely shape of the recovery. The optimists point to a V-shaped recovery, the pessimists L-shaped, and the cautious look for something less linear, such as W, U or √.

In truth, it is very difficult to know at this stage. The risks aren’t black swans, they are known unknowns, but we simply don’t have enough information at this stage to form our judgment.

The first set of known unknowns relates to the virus itself. As the economic and fiscal costs have become apparent, politicians have hurried to ease shutdowns, whether the infection is under control or not. It is possible that the combination of a degree of ongoing social distancing, track and trace systems, and better hygiene practices will mean that the reopening happens without a reacceleration in infections. But there is also a risk that the infection rate will pick back up. Governments may be reluctant to re-impose shutdowns in such a scenario, but there will still be economic costs if people choose to socially distance voluntarily (EXHIBIT 3).

We are closely tracking how the virus progresses as well as using high frequency data to gauge the extent to which economic activity is normalising (EXHIBIT 4). To find the latest statistics on these, please refer to our On the Minds of Investors piece, Monitoring the global impact of Covid-19, which is updated twice a week.

As the weeks and months drag on, the more lasting consequences of the recession will become more evident. Policymakers globally have made a gallant attempt to limit the impact and absorb the losses of Covid-19. Grants and subsidies aimed to shift the losses on to government balance sheets. These, in turn, were shifted to central bank balance sheets as asset purchase programmes were expanded to absorb the additional issuance. Governments have been able to issue record high levels of government bonds, at record low interest rates.

Furlough, or short-shift schemes have been the cornerstone of the policy response in Europe (EXHIBIT 5). However, unemployment has still risen in the UK. The moves on the continent of Europe have been more moderate, but we suspect this is flattered by people not categorising themselves as unemployed because they are not actively looking for work due to either a need to look after children or a choice to remain socially isolated.

In the US – which hasn’t adopted widespread furlough schemes – unemployment rose to 14.7% in April though came down slightly in May to 13.3%. We would be considerably more worried about a double-digit unemployment rate were it not for the fact that the US social safety net has been made considerably more generous. Indeed, estimates suggest that 75% of those that have lost work are in fact better off given the additional USD 600 a week that has been added to unemployment benefits. This boost to benefits is set to expire on 31 July and, though an extension of some sort looks likely, it is likely to be less generous. We are therefore monitoring labour market data closely to gauge any shift in unemployment from those currently classified as temporary to permanent (EXHIBIT 5).

What will be the lasting consequence of higher levels of public debt? Is a new wave of austerity ahead? Public sector pay and benefit freezes – which were an important component of the spending restraint in the last expansion – seem unlikely given the degree of austerity fatigue in the population. Wealth taxes may be appealing given the resilience of asset prices, but these policies run into the practical problem that much of people’s wealth is stored in housing assets and held by individuals that are asset rich and income poor. One off ‘Pigouvian’ income taxes on higher earners are also being touted. We see it as more likely that finance ministers will forge ahead with plans to tax the large multi-nationals that obtain tax advantages by choosing favourable domiciles.

There is one global debt-reducing strategy we see as almost inevitable: interest rates will be held down for the foreseeable future. One suspects that policymakers are hoping for a repeat of the post-war period, in which a combination of yield curve control and financial repression kept the interest rate below nominal growth and helped erode government debt as a percent of GDP (EXHIBIT 6).

Lower interest rates will help corporates, which, on aggregate, have also experienced a significant rise in debt as a result of Covid-19. While we don’t expect governments to focus on deleveraging, the same may not be said for the corporate sector. Corporate deleveraging may constrain investment spending and employment growth and, in turn, the economic recovery.

So what is the letter most apt to describe the economic recovery? Our standard alphabet might not suffice but, in our view, expecting a symmetrical V is too optimistic. The recovery is likely to be more gradual, with a few stop-starts along the way. All the while, investors should be mindful of some sizeable tail risks lurking.

One such risk is China’s relationship with the world in the wake of Covid-19. Our opinion is that de-globalisation is easier (politically) said than done. China is highly integrated in global supply chains. As the 2019 trade war demonstrated, it is very hard to reduce trade links without causing significant economic harm in western economies. However, it does seem likely that China will come under scrutiny for regulatory standards, which may in turn raise inflationary pressures. Despite the economic realities, rhetoric towards China may intensify for short-term political reasons.

Nowhere is this more evident than in the US, which enters full election mode in the coming months. At this stage it is still difficult to say anything definitive about who will win, whether the victor will have full control of Congress, or the impact on markets.

The top priority for whoever emerges successful will be to manage the recovery as the economy restarts in earnest in 2021. Tough choices will need to be made about whether to push on with further stimulus or to try to tighten the purse strings as the recovery takes hold. President Trump had already flagged his desire for a second round of tax cuts prior to Covid19, but with US national debt-to-GDP now set to rise above 100% this year, further corporate tax cuts could face greater opposition. While Trump is yet to lay out a clear agenda for a second term, the tough-on-China and tough-on-trade stances that were at the core of the 2016 Republican campaign will remain a key tenet of his approach.

For the Democrats, as the most left-leaning candidates exited the primary race, so did their policies. Yet it is clear that presumptive nominee Joe Biden’s vision for corporate America is still very different to that of President Trump. Two topics that investors will need to monitor closely are a proposal to use anti-trust legislation to clamp down on ‘Big Tech’ and plans for corporate tax changes. Biden’s campaign team has also been keen to emphasise its candidate’s tough-on-China credentials. Historically, escalating trade tensions have favoured the higherquality US stock market relative to other regions, but a ramp-up in pressure on the tech titans would pose risks to US market leadership given the high weights to the technology and communication services sectors in US indices.

The second half of the year may therefore put us in the unusual position in which the political risk premium may be higher on US assets than on those of continental Europe, where the signs look increasingly positive. Though it still needs to be ratified by all EU member states, the European Recovery Fund is a significant step forward. Not only will it provide invaluable short-term help for countries like Italy but it provides a strong signal for the long term with regards to the fiscal integration that is much needed to complement the monetary union.

If the recovery in the US lags due to lingering Covid risks, and perceptions of political risk change, we could see downward pressure on the dollar.

CONSIDERATIONS FOR INVESTORS IN THE NEAR-TERM GIVEN UNCERTAINTIES

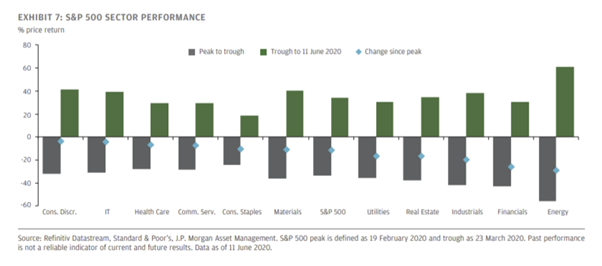

While the S&P 500 suggests a V-shaped recovery is priced in, at the sector level the narrative is more nuanced. From the start of the year to the S&P 500 trough in March, some of the most obviously affected sectors were hardest hit. Meanwhile, the likely winners from people remaining at home, other than for their food shop, outperformed.

The bounce-back since March has included some of the worst performers during the sell-off (EXHIBIT 7). For example, energy, autos, clothing retailers and restaurants have all outperformed during the rally, presumably on hopes of a partial rebound in activity as the economy starts to reopen. But some of the perceived beneficiaries of a world with more working and shopping from home, such as home improvement retailers, tech companies and industrial (including warehouse) properties have also rallied strongly. Meanwhile, despite improvement from their lows, airlines, hotels, department stores and retail properties remain among the weakest performers year to date.

What are the risks and opportunities from here under different potential scenarios:

Scenario 1: A full and sustainable reopening of the economy with social distancing no longer required. The most beaten-up sectors could rally further, while the sectors that have gained the most could be vulnerable to profit taking and rotation into cheaper companies as it becomes clear we won’t all work and shop from home forever. This would also likely coincide with a style rotation from large cap to small.

Scenario 2: An acceleration in infection rates leading to renewed shutdowns. At least part of the rally since March could reverse for most sectors, but those most exposed to further shutdowns could suffer the most as solvency concerns increase.

Scenario 3: Partial reopening of the economy but with some social distancing remaining in place. Sectors that might be able to reopen with some social distancing, such as department stores, autos and energy, could benefit further. Airlines, hotels and dine-in restaurants could struggle as solvency concerns increase. The most expensive stocks among the current winners could also suffer from valuation deratings and earnings disappointments, as unemployment remains elevated.

Which scenario plays out depends largely on the path of the virus itself, which is unknown. Given this uncertainty, we think it makes sense to avoid potential value traps, where solvency concerns could increase further. But we also think it makes sense to avoid the most expensive companies, where there is a lot of good news already in the price.

We also think this recession will increase the momentum behind sustainable investing. Robust ESG screening processes should capture the risks to corporate earnings from potential changes to taxes and other political interventions. The crisis has underscored the benefits of screening companies on nonfinancial metrics such as corporate governance and human capital management. We believe companies will increasingly be rewarded for demonstrating responsible capitalism given that there are, unfortunately, likely to be more lasting consequences of this recession for lower income and minority groups. Finally, although governments will be strapped for cash coming out of this recession they will also been keen to support infrastructure projects that can fuel the recovery. We expect these projects to be focused on the shift to a zero-carbon economy. The European Green deal is one such example.

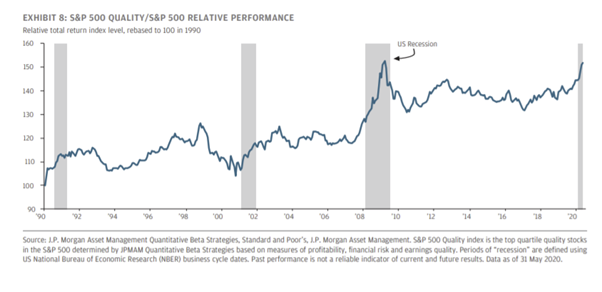

An active, nimble approach, with a current focus on quality companies (EXHIBIT 8), a keen eye on valuations, and consideration of ESG risks, therefore appears the best way of navigating the uncertainty facing investors.

SEEKING SUSTAINABLE INCOME

Central bank actions so far this year have performed the essential role of keeping government borrowing costs low but, for those seeking income, the negative side effect is that lowrisk income options are increasingly scarce.

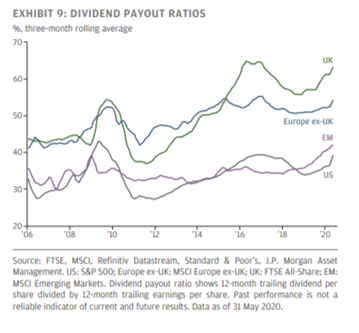

Investors have been turning to higher risk asset classes, including equities, for income over recent years, yet dividend cuts have become a hot topic as companies look to shore up balance sheets against the shock from Covid-19. While we acknowledge that many companies – particularly those who are receiving government support – may find it difficult to maintain payouts over the coming months, it is essential not to mistake what, for many firms, will be a cyclical issue for a structural one. On a regional basis, we see US dividends as most resilient. The lower dividend payout ratio of the US market provides companies with more flexibility to maintain dividends in periods of weaker earnings. Higher use of buybacks provides a buffer for companies to cut before dividends are hit. Regulatory pressure on banks, in particular, has also been lower so far in the US than in Europe.

Riskier parts of fixed income, such as corporate credit and emerging market debt, are other areas that may warrant attention when hunting for income. The Federal Reserve’s decision to buy both investment grade and high yield credit for the first time helped to pull spreads back from their widest levels in March, but credit spreads still sit significantly above their levels of the start of 2020. Central bank purchases in both the US and Europe should provide something of a backstop for corporate bond prices in the second half of the year, although we advocate an increasingly selective approach as investors move further down the quality spectrum and the need to differentiate between (more temporary) liquidity issues and (more permanent) solvency issues becomes more important.

Outside of fixed income, real assets may also have a larger role to play in portfolios as an alternative income source. While asset prices in areas such as infrastructure have not been immune to the pressures seen in public markets so far this year, income streams have broadly remained stable. But, of course, investors will need to be able to accept lower liquidity as the trade-off for moving into these types of asset classes.

The risks of overstretching for yield when hunting for income have been made very clear by the market volatility so far in 2020. Higher levels of income can only be achieved via higher levels of risk in some shape or form. Rather than ramping up risk to achieve a fixed yield target, income-seeking investors may be better off using a wide range of asset classes to build well-diversified portfolios that are in line with their risk appetite, and accepting the level of yield available as a result.

60:40 WHEN BOND YIELDS ARE NEAR ZERO

Perhaps the clearest investment challenge that will endure well beyond Covid-19 is that of how to construct a portfolio in a world of very low government bond yields.

Government bonds have traditionally played two roles in a portfolio. One is to provide a steady and stable source of income. The other is to protect a portfolio in times of market stress. Traditionally, recessions would coincide with central banks cutting interest rates, sending bond prices higher at a time when stock prices were falling. This reduced the overall scale of capital loss in bear markets.

As we look ahead, developed world government bonds don’t look like they will serve either purpose. Even long-duration government bonds provide very little – if any – income in much of Europe. And unless central banks entertain the idea of taking interest rates into negative territory (or deeper negative territory, for those already deploying negative interest rates) then bond prices cannot rise much in periods of market stress.

Meanwhile, shifting to, say, a 90:10 allocation or substituting government bonds for high yield bonds would help boost return prospects but result in a portfolio that was far less able to weather bouts of volatility.

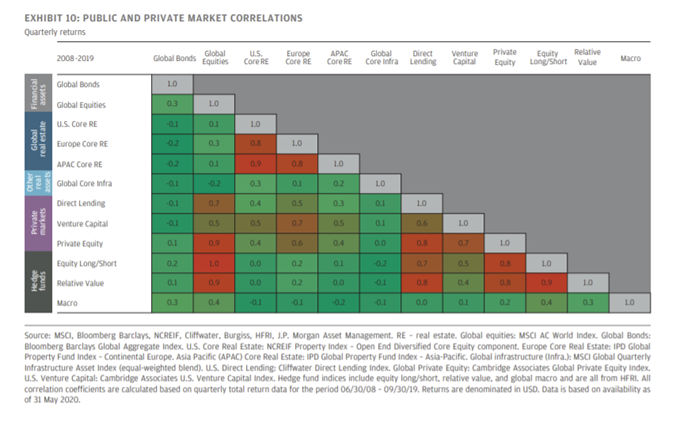

The challenge is therefore to find assets that have low correlation to stocks and ideally provide income along the way. While there are still highly rated government bonds – such as Chinese government bonds – that offer modest positive yields, in our view it may be better to look to the alternative markets. EXHIBIT 10, taken from our Guide to Alternatives, shows the asset correlations. Within liquid strategies, macro funds have tended to do a good job of providing downside protection. Less liquid options include direct real estate and core infrastructure, which both have relatively low correlations to stock markets and offer relatively strong income.

J.P. Morgan is a global leader in financial services, offering solutions to the world’s most important corporations, governments, and institutions in more than 100 countries. This in-depth analysis of markets by a world leading financial services organisation can prove valuable as we venture into the unknown as Coronavirus restrictions are gradually loosened and we attempt to return to ‘normal’.

We still believe now as much as ever that gaining a consensus view of the markets by reviewing the opinions of a variety of market leaders is key. Market behaviour is very much on a knife edge right now, and it is important that we frequently review these views so that we are well informed and in turn can keep you up to date.