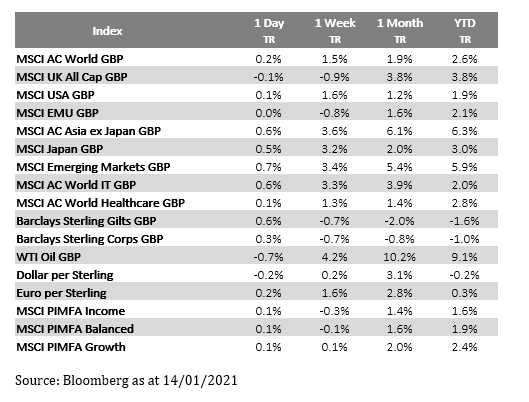

Please see below Daily Investment Bulletin received from Brooks MacDonald earlier this afternoon. The update provides analysis on the fall and rise of bond markets in response to political developments in the US and Italy over the past few days.

What has happened

Equity markets retained a constructive tone yesterday, but it was really bond markets that did the most travelling. Initially US Treasury bond yields fell as markets continued to digest the series of Fed governors who reassured bond investors that they would remain accommodative for the foreseeable future. Overnight however, Bloomberg reported that President-elect Biden’s administration would be seeking a bi-partisan $2 trillion bill which led the decline in yields to reverse. The interplay of the nascent economic recovery, fiscal stimulus and monetary stimulus will be a key theme of 2021.

Italian politics

As widely expected, Matteo Renzi announced yesterday that his party, Italy Alive, was quitting the government’s coalition. Matteo Renzi previously was Prime Minister as well as leader of Democratic Party however his new party has far fewer seats in Parliament. Those few seats are still enough to topple the delicate coalition, but investors are currently expecting an election to be avoided. Prime Minister Conte may now resign, or a vote of confidence may be called, regardless Conte will first seek to build a new coalition amongst the parties. Should this fail we may see a change of Prime Minister or a technocratic administration as an interim measure. Hope that Italy could avoid the destabilisation of fresh elections helped support Italian government bonds after a difficult start to the week.

US Politics

The major news story yesterday was the second impeachment of President Trump, a first in American history. The key question now is when the articles of impeachment will be reviewed by the Senate, commencing the trial. There is an active debate amongst Democrats over whether it is better to deal with the trial as the first order of business under a new White House or whether it is prudent to conclude other business first. There is certainly no urgency on the Senate trial given the trial will take place after President Trump leaves office however the political palatability of a delay is probably the key factor.

What does Brooks Macdonald think

With talk that President-elect Biden will seek a $2 trillion package, well ahead of expectations, cyclical equities are seeing another boost overnight and today. Today we hear from Fed Chair Powell who will be talking about the Fed’s policy framework. Investors will be scouring the speech for commitment to the mood music from recent Fed governor speeches which have sought to reassure markets that monetary accommodation is here to stay.

Please check in again with us soon for more relevant data and market analysis.

Stay safe.

Chloe

14/01/2021