Please see below articles received yesterday afternoon, written by the Head of Sustainable Investing at Jupiter and Head of Strategy at UK Alpha. The first commentary offers tips on investment opportunities for the year ahead and the second provides an update on the UK’s economic recovery.

Abbie Llewellyn-Waters, Head of Sustainable Investing, noted that in recent months the largest impact on sustainable investing, including her own strategy, was the value rotation. Abbie believes that the most attractive sustainability investment opportunities are to be found in high quality stocks. Reporting season is starting soon, and that will provide more context about how these quality stocks are navigating this environment.

From a broader perspective, Abbie doesn’t share the optimism in the market based on an economic reopening, which has been in full swing since the first vaccine announcements in November last year. She’s concerned that a normalisation is further away than the market is currently pricing in. In recent discussions with a world-leading company in the field of viral vaccines, they pointed to more prolonged timeframes, with normalisation closer to years rather than months away.

As such, Abbie believes it is important for investors to be disciplined and focused on businesses that can survive and prosper through this period and into the longer term, especially in defensive sectors such as healthcare and consumer goods. Among the more cyclical parts of the market, Abbie continues to see strong sustainable investing opportunities within the digitalisation theme.

Fundamentally, however, Abbie sees sustainable investing as a structural theme and many of the drivers that emerged in 2020 (including addressing climate change, where Biden’s appointment of John Kerry as special climate envoy shouldn’t be underestimated, in her view) will continue throughout 2021 and beyond.

Market whipsaws as recovery optimism weakens

At the start of the year, the market trusted in the post-vaccine recovery trade and expected that by the summer the economy would be getting back to normal, noted Richard Buxton, Head of Strategy, UK Alpha. That view has been undermined by a complicated pandemic with new virus variants and data suggesting some people are reluctant to be vaccinated, he said.

Now the market is whipsawing daily, he said. He cited a company that operates concessions in airports and train stations that said two weeks ago it was expecting a strong summer of trading as consumers rush back to travel after the lockdown. That outlook now seems overly optimistic, he said, noting that testing requirements would complicate a family of four’s holiday to Spain, for example.

Richard said he is following closely the debate about reopening UK schools. The government will be forced to make a political judgement about when to ease the lockdown and let students return to the classroom in order to end potential long-term damage to young people, especially those in disadvantaged areas, whose education has been disrupted, he said.

While a return to normal will take longer, it makes sense on a 2-year view to invest in companies that will benefit from the economy reopening, Richard said. In the meantime, his investment team is looking at adding to defensive holdings, such as including pharmaceutical companies, he said.

The recovery will happen, but like in comedy, it’s all about the timing, Richard said.

It will be interesting to see where opportunity presents itself as we make positive strides to achieve mass vaccination in the UK and worldwide.

Please see the below market update from Invesco received late yesterday afternoon:

Overview

Europe: Europe is clearly at risk of a double-dip recession, albeit a modest one.

The UK: The UK appears to be at even greater risk than the eurozone of a double-dip recession in the current quarter.

The US: US markets seem to have focused recently on the potential for additional fiscal stimulus.

What a week — both the S&P 500 and NASDAQ Composite Indexes reached all-time highs last Thursday, but we also saw a reversal of the rotation from growth/defensives to cyclicals in both European and US markets. Markets are clearly reacting to the problems that many economies are facing as COVID-19 continues to impact growth. Recent data shows evidence of these problems.

Europe may face a modest recession

Europe is clearly at risk of a double-dip recession, albeit a modest one. The IHS Markit Flash Eurozone Composite PMI (Purchasing Managers Index) clocked in at 47.5, down from December’s 49.1.1 And it’s not just services that drug down that number; there was also a decline in manufacturing PMI, which actually fell to a seven-month low. And the weakness was spread throughout Europe.

This should come as no surprise. The Oxford Blavatnik Stringency Index, which tracks the level of economic lockdowns in various countries, indicates that stringency in many European countries is at or near the highest levels that have been experienced since the start of the pandemic. In other words, first-quarter economic activity could contract again, although if it does, I would expect this to be a very shallow contraction. More fiscal support is coming, and I expect the European Central Bank to remain supportive.

And so Europe just needs to get through this “fifth quarter of 2020,” and then I expect the situation to improve. I think that by later in the second quarter we will see improvement in economic activity as vaccine distribution becomes widespread.

The UK get more bad news

The UK is in a worse situation, at an even greater risk than the eurozone of a double-dip recession in the current quarter. The preliminary reading of the IHS Markit/CIPS UK Composite PMI fell like a lead balloon, dropping from 50.4 in December to 40.6 in January.1 Chris Williamson, chief economist at IHS Markit, explained the drop in the composite: “Services have once again been especially hard hit, but manufacturing has seen growth almost stall, blamed on a cocktail of COVID-19 and Brexit, which has led to increasingly widespread supply delays, rising costs and falling exports.”

What’s more, on Friday UK Prime Minister Boris Johnson shared more bad news: 1) the UK strain of the virus is not only more contagious but appears to be more deadly; 2) lockdowns might last until this summer. And so we should not expect economic strength in the near term, although I maintain that the economy is very likely to rebound substantially as vaccines are distributed.

Japan suffering too

Flash PMI readings for January indicate Japan is facing some headwinds too. Also last week the Bank of Japan warned of increasing risks to the economic outlook for Japan, and that efforts to control the virus could have impact beyond just the services sector. And while COVID-19 has been well-controlled in Japan relative to many Western countries, Japan has not yet rolled out any vaccines. They are still in clinical trials, but rollout is expected to start by late February

The US awaits the fate of fiscal stimulus

The US is also facing serious economic headwinds due to COVID. US markets seem to have focused recently on the potential for additional fiscal stimulus. Janet Yellen, President Joe Biden’s nominee to be US Treasury Secretary, made a strong case for more fiscal stimulus last week. She recognized concerns about growing debt levels, but also argued that there’s no time like the present to borrow since rates are so low. However, by the end of the week there was concern that President Biden would not have enough support to get his proposed $1.9 trillion package passed.

On days when markets are encouraged by the likelihood of more stimulus and a stronger rebound, cyclical stocks have outperformed. But when markets are worried that no more stimulus is forthcoming, or when economic data disappoints, secular growth stocks — especially tech — have outperformed.

Key takeaways

I expect this “seesaw” stock market behavior to continue in the near term. While I still believe a strong economic rebound is in the offing later in 2021, there are likely to be glitches before we get there, as I have warned before. The tech sector has recently exhibited defensive qualities that I expect to continue and which I believe could be valuable in the next few months as we slog through what is likely to be a difficult time for the economy. Low interest rates help this situation given that tech valuations are admittedly stretched; investors have historically been more forgiving of valuations with rates so low.

The other side of the seesaw is exposure to cyclicals. I am most excited about one sector in particular: consumer discretionary. I think the global economic recovery will be robust and inclusive, creating and restoring jobs — and spurring consumers to spend. And in many countries, consumers have built up impressive savings because of a lack of spending during the pandemic. This could be deployed rather quickly once vaccines are distributed broadly and there is a return to something akin to “normalcy.”

I expect that, in a world awash in monetary stimulus, with significant fiscal stimulus as well, there will continue to be an upward bias for stocks. That doesn’t mean we won’t see a stock sell-off in 2021. It could be triggered by the 10-year US Treasury yield rising (we could see a sell-off if it rises too quickly) or fears about inflation increasing — even though I expect the Federal Reserve to reiterate this week its commitment to remain very accommodative and tolerant of a spike in inflation over its target. There could be other triggers — a continued rise in infections, especially more serious strains, or a slowdown in vaccine rollouts. We don’t know when this could occur — and while I believe it would be short-lived, I also believe it’s very important to be broadly diversified both across and within stocks, bonds and alternatives.

While broad diversification is critical, investors could consider overweighting both the technology and consumer discretionary sectors within their equity sleeve. Both could serve different purposes in a portfolio — one offering some defensive qualities while the other offering the potential to participate in the recovery.

Please keep checking back for more market updates, investment commentary and a range of different blog content from us.

Please see below the latest ‘Markets in a Minute’ article from Brewin Dolphin received yesterday – 26/01/2021

US equities strengthen on stimulus plans

Global equities performed relatively strongly last week, as fresh hopes of US stimulus outweighed concerns about extended lockdowns in Europe.

The Nasdaq was the strongest performer among the main markets, rising by an impressive 4.19% thanks to a comeback from the FAANGs. The S&P 500 and the Dow also recorded gains, with investors celebrating Joe Biden’s inauguration and Janet Yellen’s call for Congress to ‘act big’ on stimulus measures.

Renewed coronavirus concerns weighed on the UK’s FTSE 100 as well as several European indices. Over in Asia, hopes of better relations between China and the US boosted the Shanghai Composite by 1.13%, while the Nikkei remained relatively flat.

Last week’s markets performance*

FTSE100: -0.60%

S&P500: +1.94%

Dow: +0.59%

Nasdaq: +4.19%

Dax: +0.63%

Hang Seng: +3.06%

Shanghai Composite: +1.13%

Nikkei: +0.39%

*Data from close on Friday 15 January to close of business on Friday 22 January.

Merck abandons vaccine

News that pharmaceutical giant Merck is abandoning its vaccine development efforts have dampened last week’s gains. The FTSE 100 slipped a further 0.8% yesterday amid fears that Merck’s decision could delay the global rebound from the pandemic. Airlines, who could face severe travel restrictions, struggled the most, with shares in International Consolidated Airlines 7.2% lower.

In the US, the S&P 500 and the Nasdaq briefly turned negative yesterday, but the Nasdaq ended up closing at a record high, gaining 0.69% ahead of quarterly results from Apple, Microsoft and Facebook this week. The Dow, in which Merck is a component, ended yesterday 0.12% lower.

US celebrates Biden and the FAANGs

Following his inauguration last Wednesday, Joe Biden wasted no time in unveiling details of how he intends to support the US through the pandemic. His proposed $1.9 trillion Covid-19 fiscal package includes another round of direct payments, an increase in the federal weekly unemployment insurance benefit and, somewhat controversially, a hike in the national minimum wage to $15 per hour.

Biden also repeated his goal of one million vaccinations a day for the first 100 days of his presidency, and reversed Trump’s decision to withdraw from the World Health Organization and Paris Agreement on climate change.

The fact that Biden’s inauguration took place without any significant violence helped to calm nerves, as did strong provisional services PMI and better-than-expected housing data.

Although Biden’s election has brought some comfort to investors, it is worth noting that his Cabinet appointments are less market-friendly than Trump’s were. His appointments for the head of the Securities and Exchange Commission, the Consumer Financial Protection Bureau and the Senate Banking Committee could result in tougher regulations for the financial sector.

Last week also saw the return of big mega-caps in the US, which helped to drive up the Nasdaq and S&P 500. Netflix, which reported robust earnings, gained 13.5%, while Apple, Google and Facebook all rose 9%. A strong start to the US reporting season added to investor optimism for the new president.

Lockdowns extended in Europe

Over in Europe, investor sentiment was more subdued as renewed coronavirus concerns took hold. Germany’s Xetra DAX Index edged up by 0.63%, whereas France’s CAC 40 and Italy’s FTSE MIB both declined by 0.93% and 1.31%, respectively. The UK’s FTSE 100 Index fell 0.60%.

There are growing concerns that social distancing restrictions in the UK could last until the middle of the year, after Boris Johnson announced it is ‘too early’ to say when the national lockdown will end. Germany extended its restrictions until 14 February, and The Netherlands introduced its first nationwide curfew since World War II.

Disappointing economic data did not help matters. A Purchasing Managers’ Index revealed business activity in the eurozone contracted at a faster rate in January, while the UK’s quarterly CBI business optimism index plunged from 0 to -22, largely driven by fears about the impact of Covid-19 on British businesses.

Q1 is shaping up to be a bad quarter for the UK economy

In contrast, gilt yields increased after Bank of England governor Andrew Bailey said he anticipated a pronounced economic recovery in the UK later in the year as vaccines are rolled out.

Japan trims GDP forecast

In Japan, the Nikkei rose 0.39% following the country’s first positive exports data since November 2018. The government also announced it has agreed to buy additional vaccines for 12 million people, meaning it will have enough to vaccinate more than half of the country’s population.

On the flipside, Japan’s monetary policy committee lowered its gross domestic product (GDP) growth forecast for the current fiscal year from -5.5% to -5.6%. Although it increased its growth target for 2021 from 3.6% to 3.9%, it warned that the outlook was highly uncertain.

In China, where stocks rallied following Biden’s election, forecasts revealed the economy grew by 2.3% in 2020 – a clear sign that, unlike much of the rest of the world, it has largely recovered from coronavirus lockdowns. Fourth quarter real GDP growth increased to 6.5%.

Markets show impressive resilience

Overall, global stock markets are showing remarkable resilience during the pandemic, underscoring the case for exposure to risk assets. Markets are on course for a third consecutive month of gains, and more stocks are hitting their 52-week highs.

Now, all eyes are on this week’s raft of US corporate earnings figures. Investors will be looking for insight into whether tech stocks can continue their strong growth trajectory over the coming year.

Please continue to check back for our regular blog posts and updates.

Please see below for Legal and General’s latest Asset Allocation Team’s Key Beliefs article received by us the afternoon of 25/01/2021:

Bubble trouble?

Never have more people searched for the term ‘stock market bubble’ on Google. Data stretching back to 2004 show that January 2021 is set to eclipse January 2018, when searches for the term both preceded and followed a 10% drop in the S&P 500 over nine trading days. As we have highlighted before, investor optimism is pretty well inflated and, while most sentiment indicators don’t look stretched, many are elevated.

Burst case scenario

Not everyone is optimistic, though. One scholar of market bubbles, Jeremy Grantham, opened his new outlook: “The long, long bull market since 2009 has finally matured into a fully-fledged epic bubble.” Grantham has a good track record in predicting the moments when bubbles burst, so should we be worried? We think the famed investor may be right but, as he concedes, we believe the market could still run a lot further. Our own bubble index shows that the probability of a market bubble has indeed been rising. In fact, it is now the highest it has been since 2008.

What has driven this? We have seen an increase in capital raising through IPOs and SPACs, some of which echo the tech bubble of the late 1990s. US retail investor activity has also taken off, with easier access through investment platforms and, for some, new money to play with from stimulus cheques. However, we are just emerging from the COVID-driven economic recession. This means many macroeconomic indicators have improved, policy is supportive, and there is plenty more cash on the side lines ready to be deployed, regardless of further fiscal stimulus.

So while the market is definitely reminiscent of a bubble forming, it could easily still get much stronger from here. We therefore believe it’s too early to call a bubble now.

The moderates yield

If you weren’t able to watch any of the US presidential inauguration, I recommend viewing US National Youth Poet Laureate Amanda Gorman’s recital of “The Hill We Climb”, a powerful and gritty poem of hope for the future of the US, from a self-proclaimed presidential candidate for 2036.

In the more immediate future, the most relevant aspect of the new Biden administration to financial markets will be the prospect of more fiscal stimulus. The central case is for another virus relief package worth $1 trillion to be passed in the coming months, with an additional $1 trillion recovery package potentially following later. The quicker the economy recovers, of course, the smaller later packages will be.

Politically, though, we see the path of least resistance actually being for more fiscal spending rather than less. With a razor-thin majority, power accrues to the moderates, which means only consensus policies can pass. We expect it will be easier to build such a consensus on extra spending (giving things away) than on extra revenues (taking things away). While Democratic moderates have supported virus relief and the current package so far, several are not on record as supporting Biden’s tax proposals. Finally, voters don’t appear to care as much about deficits anymore, so senators probably won’t either.

Treasury yields could be the place where changing fiscal dynamics are priced, and indeed US yields have risen more than others in recent weeks after the Georgia runoffs, but as it stands we are comfortable with an overall neutral position on duration. In fact, we prefer US markets to UK gilts, which have only seen more modest yield rises despite the so-far successful vaccine rollout and expectations for a fiscally conservative budget.

Flexible recipe for fixed income

Multi-asset portfolios are like giant cakes, baked with multiple ingredients. We have decided to add a new ingredient to our cake: Chinese bonds. Technically it’s not new, as they are a growing part of emerging-market bond allocations in portfolios, but we have moved to an explicitly positive view.

We believe Chinese bonds add a lot of diversification to our fixed income holdings as China hums to a slightly different economic tune from the rest of the world, with a different monetary policy framework too. Historically, Chinese bonds have had a low correlation to other bonds. Their yields are relatively high, and we are particularly interested in bonds that could continue to provide protection in macro downturns as we believe many traditional bond markets will struggle to provide the defence they offered in the past.

This is just one of the steps we have been taking in portfolios to try to manage investor outcomes in a low interest-rate environment, with greater roles for non-traditional fixed income assets as well as defensive currencies and other strategies.

Regularly ‘picking the brains’ of investment managers and experts by reading articles like these can help update your own view of the markets and current global affairs.

Please keep reading these blogs to keep your view of the market well informed and up to date.

Yesterday afternoon Prudential announced ‘upwards’ Unit Price Adjustments, details cut and pasted as follows:

PruFund Series E fund announcement

Today we announced there’s six upward UPAs for the Series E PruFund range of funds at this month’s PruFund Investment Date.

Fund

UPA applied

Prudential PruFund Growth Pension – Retirement Account Series E

+3.18%

Prudential PruFund Cautious Pension – Retirement Account Series E

+2.16%

Prudential PruFund Risk Managed 2 – Retirement Account Series E

+2.24%

Prudential PruFund Risk Managed 3 – Retirement Account Series E

+2.93%

Prudential PruFund Risk Managed 4 – Retirement Account Series E

+3.41%

Prudential PruFund Risk Managed 5 – Retirement Account Series E

+3.97%

This is good news and I had hoped for this following positive recent developments for markets, the US election outcome, the last-minute Brexit trade deal and the approval of vaccines and the start of distribution and vaccination.

President Biden has laid out his plans, revoked quite a few of Trump’s policies and appears to be on a mission to change the USA. This should help the world and global trade although the USA will still be struggling with China and trade with them, but relationships should be more diplomatic. President Biden is after all, a career public servant.

A cautionary note, whilst we still have headwinds in the market, (the end of furlough, rising unemployment and business failure in the UK to name a few), markets are still volatile as the vaccine battles the virus and economies struggle to build momentum, we could see further UPAs down as well as up. However, over the long term I would expect returns to be reasonable and for all PruFund investors to benefit from a truly diversified multi asset approach. This is what we need when asset values over the next decade in ‘standard’ investment assets are forecast to be lower for longer.

J. P. Morgan’s Long Term Capital Markets Assumptions Report for 2021 (25th anniversary edition) details the lower longer term returns from standard asset classes. Multi Asset diversification will be key. Prudential have long term experience in this area of fund management and have the scale, expertise and leverage to access non standard higher returning assets that will help sustain higher returns than standard portfolios of assets will offer at a similar risk profile over the long term.

As ever, our key advice is for you to remain invested, we are not out of the woods yet, but things look a lot brighter in comparison to just a few months ago. Funding investments now whether it is on a single/ad-hoc basis or on a regular monthly basis should be good value over the long term too.

Please see below the ‘A step-by-step guide to the PruFund smoothing process’, which aims to show the long-term characteristics and how the PruFund series of funds function:

Please see below commentary received from Blackfinch Group this morning, which provides market analysis as Lockdown 3.0 continues in the UK and Joe Biden is inaugurated as 46th President of the United States.

UK COMMENTARY

The Office for National Statistics released labour productivity data showing that output per hour, the UK’s headline measure of labour productivity, increased 4.0% year-on-year in the third quarter of 2020, the largest increase since the fourth quarter of 2005. The Coronavirus Job Retention Scheme continued to impact output per worker productivity, which fell 7.9%.

Inflation, measured by the Consumer Price Index, rose 0.6% in November, pushed higher by transport and clothing costs.

Average house prices in the UK jumped 7.6% in the year to November 2020, to reach a record high of £250,000.

Retail footfall fell 10.9% in the week to the 16th of January, with year-on-year footfall down 67.5%.

Retail sales data showed volumes fell 1.9% in 2020, with clothing sales the hardest hit, falling by a quarter from the previous year.

IHS Markit/CIPS flash UK composite purchasing managers’ index (PMI) in January fell to an eight-month low of 40.6, down from 50.4 in December.

US COMMENTARY

Joe Biden was inaugurated as 46th President of the United States and got straight to work, using executive orders to reverse some of Donald Trump’s more controversial actions, including returning the US to the Paris Climate Agreement.

President Biden also moved forward with his plans to launch a further stimulus package, but investors await final confirmation of the deal.

Incoming Treasury Secretary Janet Yellen called on Republicans to back the stimulus package and urged the US to “act big” to revive the economy.

US initial jobless claims fell to 900,000 last week, but remain at elevated levels. Continuing claims also fell marginally by 127,000 to 5.18mn.

ASIA COMMENTARY

Official data showed Chinese gross domestic product was 2.3% in 2020, having expanded by a better-than-expected 6.5% in the fourth quarter.

COVID-19 COMMENTARY

New research by BioNTech found that its vaccine, jointly produced with Pfizer, is effective against the new variant of COVID-19 originally identified in the UK. The results echo those from a previous Pfizer study that showed the vaccine was effective against virus mutations identified in the UK and South Africa.

The ever-changing world we live in reinforces the importance of regular up-to-date communication. Please check in again with us soon for further market updates and news.

Please see the below article from JP Morgan received this morning:

The election of Joe Biden has fueled expectations of an increase in global momentum on tackling climate change. Climate action was one of Biden’s key campaign promises and, according to exit polls, the main reason that 74% of his voters voted for him. Having control of the Senate gives the Democrats more scope to deploy their (climate) programme, but they will still need to compromise given that they fall well short of the 60 seats required to easily pass major legislation. Business groups will also be active in lobbying Congress to oppose the pieces of legislation they find the least acceptable.

Biden’s climate proposals

In his Plan for a Clean Energy Revolution and Environmental Justice, President Biden set out his central ambitions on climate, including:

“Rally the rest of the world to meet the threat of climate change”: The president has stated that rejoining the Paris Climate Agreement will be a day one priority. He also wants to fully integrate climate change into US foreign and trade policies in order to get every major country to further ramp up their domestic climate targets. From a global climate policy perspective, greater US support could be a game changer, as the US is the second-largest CO2 emitter in the world and the carbon intensity of its economy is three times higher than the global average. Quite how the president intends to work with the international community should become clearer following COP 26, the United Nations Climate Conference due to take place in Glasgow in November. At that point, we could see a new Grand Climate Accord. One possibility investors should look out for is that Biden makes climate policy central to ongoing trade tensions with China.

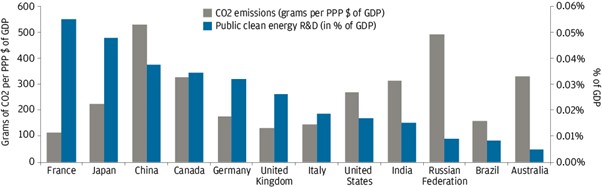

“Ensure the US achieves a 100% clean energy economy and reaches net-zero emissions no later than 2050”: Biden’s pledge to achieve net-zero emissions by 2050 has already been made by more than 110 countries, accounting for more than 50% of global GDP and carbon dioxide emissions. To achieve the net-zero goal and ensure that the US becomes a 100% clean energy economy, Biden plans, among other policy measures, massive public investments (USD 400 billion) in energy- and climate-related research and development (R&D), an area where the US is lagging compared to Europe and China (see Exhibit 1).

“Build a stronger, more resilient nation”: In addition to supporting R&D, Biden has promised significant investments in low-carbon infrastructure, committing to “a federal investment of USD 1.7 trillion over the next ten years, leveraging additional private sector and state and local investments to total to more than USD5 trillion”. This is probably the aspect of Biden’s climate plan that has generated the most enthusiasm in the US as there is a bipartisan consensus about the need to invest in infrastructure. The American Association of Civil Engineers estimates that to close its investment gap, the US “must increase investment from all levels of government and the private sector from 2.5% to 3.5% of US GDP by 2025”. Infrastructure spending will be part of a broader agenda of easy fiscal policy to promote the post-Covid 19 recovery.

As well as these key climate commitments, other parts of Biden’s programme could further support the sustainability agenda. For example, changes to the Employment Retirement Income Security Act could redirect pension capital flows to encourage private capital to be part of the climate solution.

Exhibit 1: Government investment in greening the economy and level of CO2 emissions

Source: IEA, OECD, World Bank, Mission Innovation, J.P. Morgan Asset Management. R&D budgets for Brazil, Russia, India and China are estimates. Note: R&D numbers from public sector data and may not reflect private sector or joint venture research initiatives. Data as of 2019 or latest available.

Implications of climate policy initiatives for the (global) economy

The economic impact of the transition to a low carbon economy generally depends on whether it is “sticks-based”, with private businesses bearing the bulk of the cost of the transition, or “carrots-based”, with governments supporting the transition through subsidies and other forms of fiscal stimulus.

The carrots-based approach, on which Biden focused in his campaign, is of course the most popular in the current economic environment as it could support the recovery while also addressing the longer-term threat of climate change. Even though he inherits the highest debt/GDP ratio since the second world war, Biden aims to maximise the fiscal impulse of his policies by leveraging public-private partnerships. Similar approaches, such as the European Fund for Strategic Investments, launched in 2015, have delivered strong results in terms of economic growth and energy transition while also generating opportunities for private investors.

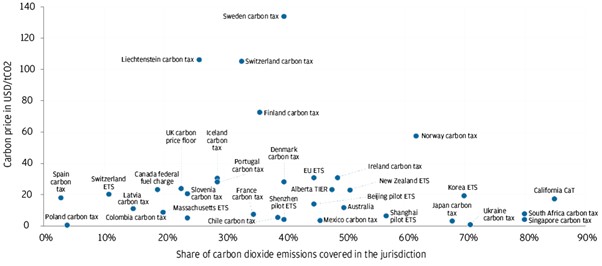

However, to be most effective from a climate perspective, this approach should be combined with a sticks-based approach. The most common such approach is the implementation of a carbon tax, or more generally of a carbon price that can be set either through taxes or preferably through Emissions Trading Schemes (ETSs) to incentivise carbon producers to reduce their carbon intensity.

Although Biden has refrained from formally mentioning carbon pricing in his programme, his Treasury Secretary, Janet Yellen, has made clear in the past that she sees carbon pricing as a key element of any climate policy package. Yellen has also advocated so-called “carbon border tax adjustments”, which would ensure that ambitious carbon pricing does not undermine a level playing field globally. As already discussed, this may contribute to ongoing trade tensions with China.

Conviction in the need for border tax adjustments is shared by many countries that have already launched their ETSs, but so far emissions coverage and price levels remain heterogeneous, and too low to reach our climate goals (Exhibit 2). The US could be tempted to leverage its experience with state-level ETSs, such as those in California and Massachusetts, to support the creation of a global level playing field for carbon prices.

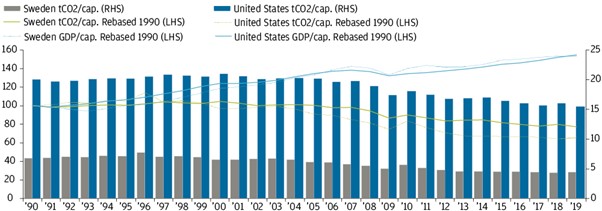

Contrary to the general belief, moving towards a fairer carbon price globally should not necessarily be negative for the global economy. The example of Sweden is striking in this respect. Although Sweden introduced the world’s highest carbon tax (Exhibit 2) in 1991 and joined the EU ETS in 2005, its GDP per capita grew by 53.5% between 1990 and 2019, or slightly less than the 54.6% posted by the US. In the meantime, Sweden’s carbon intensity has dropped from 6.8 tonnes of CO2 per capita (tCO2/cap) in 1990 to 4.45, a third of US carbon intensity (Exhibit 3).

Exhibit 2: Carbon pricing initiatives around the world

Carbon prices in USD (as of 1 November 2020) and % share of carbon dioxide emissions covered in the jurisdiction.

Source: World Bank Carbon Pricing Dashboard, National Bank of Belgium, J.P. Morgan Asset Management. Data as of 20 January 2021.

Exhibit 3: Economic and carbon performances of Sweden compared to the US, 1990-2019

Economic and carbon performances of Sweden compared to the USA 1990-2019

Source: National Bank of Belgium, Refinitiv Datastream, Emission Database for Global Atmospheric Research, Crippa, M., Guizzardi, D., Muntean, M., Schaaf, E., Solazzo, E., Monforti- Ferrario, F., Olivier, J.G.J., Vignati, E., Fossil CO2 emissions of all world countries – 2020 Report, EUR 30358 EN, Publications Office of the European Union, Luxembourg, 2020, ISBN 978-92-76-21515-8, doi:10.2760/143674, JRC121460. , J.P. Morgan Asset Management. GDP per capita based on purchasing power parity (PPP), 2011 international dollars. Data as of 20 January 2021.

Investment implications

Biden’s climate policy is likely to be part of a package of broader fiscal measures to support growth and speed up the energy transition of the country. It should also generate opportunities for investors in asset classes including real assets and global renewables, all of which have rallied over the last couple of weeks.

Internationally, the US is likely to re-embrace a more multilateral approach, after rejoining the Paris Climate agreement and committing to net zero carbon emissions by 2050. While US support for global carbon pricing initiatives remains uncertain, Biden’s administration may support carbon border tax adjustments, which could lead to a level playing field globally for carbon prices.

This is not necessarily negative from an economic perspective, as shown by the Swedish example, but carbon policy will need to be monitored by investors as carbon intensity is going to be an important non-financial parameter of economic and corporate performance.

Its good to see President Biden’s positive impact already showing through, from re-joining the Paris Climate Agreement to his recent repeal of Trump’s former transgender military ban. These are all elements which come under the heading of ESG.

Along with his more pro-active efforts to tackle the coronavirus, hopefully these positive moves will all help the markets move in the right direction.

Please keep checking back for more ESG related content along with a range of investment and market updates.

Please see investment bulletin below from Brooks Macdonald received this morning – 22/01/2021

Brooks Macdonald Investment Bulletin

What has happened

A tech fuelled rally drove the US index marginally higher yesterday. Interestingly the cyclical stocks, which outperformed at the start of the month are losing some momentum. One of the explanations for this is the disconnect between market expectations around demand, i.e. the oil price and forward looking equities, i.e. oil majors – until expectations of a cyclical rebound is reflected across the board, cyclical equities may have bouts of weakness. That said, the reflation narrative remains alive in fixed income with US inflation expectations picking up yet again yesterday.

ECB

Whilst there were no changes to policy levels at the ECB meeting yesterday, investors were left feeling more uncomfortable as the bank stressed the ‘symmetrical’ nature of the pandemic quantitative easing programme. Specifically, this means that if the bank feels that it does not need to use all of the QE budget it will not do so. This is fairly logical and reiterates what was said in the December meeting but the fact there was a new section in the statement to reiterate this, concerned markets. Central bank watchers pore over the specific words in a statement so the inclusion of a full section is a strong emphasis from the ECB. Investors decreased their expectations of monetary policy accommodation as a result which saw the Euro rise against the dollar and sovereign bond yields rise amidst fears that the major buyer of sovereign bonds would be less active in purchases going forwards.

US COVID response

With President Biden’s first full day in office we saw a series of executive orders in relation to vaccine supply chains and vaccine deployment. The President did note however that stimulus was required to change the trajectory of the vaccine rollout, but the administration remains committed to the 100m vaccines in the first 100 days. Dr Fauci, Chief Medical Advisor to the President, welcomed news that Johnson & Johnson’s vaccine expected to have early stage results during the start of February and would have data available for an emergency use review during that month.

What does Brooks Macdonald think

The ECB is in a tough spot as financial markets want to hear that tapering is off the table however more fiscally conservative member states such as Germany, want the pandemic QE programme to slow as the economy recovers. Last year we saw the challenge by the German Constitutional Court over the ECB’s QE programme and the inclusion of a statement around the symmetrical nature of QE is probably principally designed to calm the fiscal hawks amongst member states.

Source: Bloomberg as at 22/01/2021

Please continue to check back for our latest updates and blog posts.

Please see below article received from AJ Bell yesterday afternoon, which provides an insight into what rising prices mean for value stocks and emerging markets.

One theme which continues to exercise financial markets is whether inflation is primed to make a comeback and – if so – what this could mean for asset allocation and portfolio strategies.

The five-year forward inflation expectation in the US now stands at 2.11%, its highest level since December 2018, and financial markets are beginning to react: bond yields are ticking higher, bitcoin is going bananas while gold holds relatively firm. Within equity markets cyclical growth (or ‘value,’ for want of a better word) is again trying to cast off a decade of underperformance relative to perceived secular growth sectors such as technology.

As this column has suggested before, the battle for portfolio style (and performance) supremacy within equities can be seen by comparing the returns provided by two exchange-traded funds (ETFs) in the US: the QQQ Invesco Trust, which follows the price of the biggest non-financial stocks on the NASDAQ, and the Russell 2000 Value ETF.

If the line on this chart goes up, ‘growth’ is outperforming. If it goes down, ‘value’ is outperforming. As can be seen, cyclical growth outperformance stretches to summer 2020.

But this trend can be seen in another way too, this time on a geographic basis. Over the past decade, investors have adapted to the low growth, low inflation, low interest rate environment by buying long-dated assets such as bonds and equity growth (such as technology stocks), and forgetting about commodities, cyclical equities (‘value’) and emerging markets.

Yet as inflation creeps back onto the radar, perhaps for the first time in 40 years since then Fed chairman Paul Volcker set about wiping it out, emerging markets are coming back into fashion too.

This can be seen using the same technique as before, this time by dividing the performance of America’s S&P 500 index by the MSCI Emerging Markets benchmark. American outperformance peaked in September, since when emerging arenas have done better.

Clear pattern

This return to form for emerging markets coincides with a period of strength for commodity prices and dollar weakness. Whether it lasts may hinge to a great degree on those two trends, which also tie into the inflation narrative.

If those three continue to coincide, then we could see a third major period of emerging market outperformance relative to the US (and by implication developed markets), to match those of 1988-1994 and then 2000-2010, so this EM resurgence must be monitored closely. If it proves to be no mere flash in the pan, then it could have profound portfolio implications.

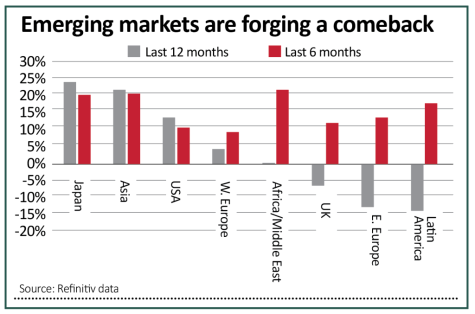

The resurgence of EMs can be seen by digging deeper into geographic performance trends, too.

Japan may be the best performer, in total return, sterling-denominated terms over the past 12 months, but Asia is a close second. The data from the past six months, when cyclical growth, or value, began to try and forge its latest comeback, show outperformance from not just Asia, but the Middle East and Africa, Latin America, and Eastern Europe, too.

East of Eden

Global export plays like South Korea and Taiwan have done well of late, but tourism and travel destinations like Thailand and Hong Kong are clear laggards. Perhaps South East Asia becomes the next leg of the post-vaccine, global upturn story.

There may be other reasons for the return to form of emerging markets, beyond commodity strength, dollar weakness and markets’ preoccupation with inflation and a near-term economic recovery, as this column hinted just under a year ago.

Perhaps Asia’s outperformance reflects the view that region was first in and first out when it comes to the global pandemic (even allowing for recent local flare-ups). Given the experience of SARS in 2002-03, Asia may have been better prepared and equipped to deal with such a situation.

In addition, Asian nations learned harsh lessons about debt during their currency crisis of 1997-98 and as a result aggregate government borrowing levels are generally much lower as a percentage of GDP than they are in the West.

Such facets could help to shape long-term outperformance too, especially as soundness of finances usually wins out in the end.

We will continue to publish news and market analysis. Please check in again with us soon.

Please see below for the latest Brooks MacDonald Daily Investment Bulletin received by us today 21/01/2021:

What has happened

Markets greeted the inauguration of Joe Biden with a rally driven by the tech heavyweights. Some markets concerns remained around the final handover of Presidential power from Trump to Biden so there will be an element of welcoming the calmer tone of the new President as well as removing a transition risk premium.

President Biden

Yesterday’s inaugural Presidential address saw President Biden attempt to change the tone in Washington by encouraging bipartisan debate rather than absolutism. This speech was followed by a series of executive orders as expected. This included the US re-joining the Paris climate agreement, ceasing the withdrawal from the WHO, ending the travel ban on a number of Muslin countries and a federal mask rule on interstate travel and within federal buildings. As a sign of the focus for the new administration’s economic goals, there were also some specific COVID support measures such as pausing federal student loan repayments and extending the federal eviction moratorium. Yesterday’s speech, coupled with that of Janet Yellen earlier this week, paints a market friendly picture where near term support remains the focus. Of course, the sting in the tail could be higher taxes down the line but we need to remind ourselves of the thin Senate majority and the fact the midterms are in November next year and this could change the power balance in Congress yet again.

Central bank decisions

Yesterday we heard from the Bank of Japan which left monetary policy unchanged whilst predicting economic challenges over the course of 2021. Today is the turn of the ECB and given the central bank announced a further easing package in December, little dramatic change is expected. The central bank meets under the cloud of Euro Area CPI estimates that showed the region in deflation (-0.3%) compared to the year before. Whilst forward looking CPI estimates have been rising, in line with the broad global market reflation narrative, even these future estimates remain well below the ECB’s 2% target. The central bank therefore likely has room to increase stimulus but it isn’t clear that simply doing more of what has been tried before (bank lending, negative rates and quantitative easing) will have the desired effect.

What does Brooks Macdonald think

Equities rose and volatility fell as power transitioned peacefully between President Trump and President Biden. It is interesting that yesterday’s rally was so tech focused given fears over regulation under a Democrat White House and Congress. The rally yesterday implies that investors are confident the new administration has its hands full with the COVID response and is unlikely to look towards market unfriendly reform within that context.

Daily investment bulletins like this could prove to be very useful in the near future. Yesterday’s Presidential Inauguration is sure to cause ripples in the markets globally and keeping up to date with developments as they happen can, as ever, be very beneficial to your own views of the markets.

Please utilise our blogs in keeping your own views of the market holistic and up to date.