Please see below an article received yesterday from Brooks Macdonald which provides a brief overview of the Biden Inauguration and what the transfer of power could mean for markets:

Please continue to check our Blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.

Please see the below update from Brewin Dolphin received late last night:

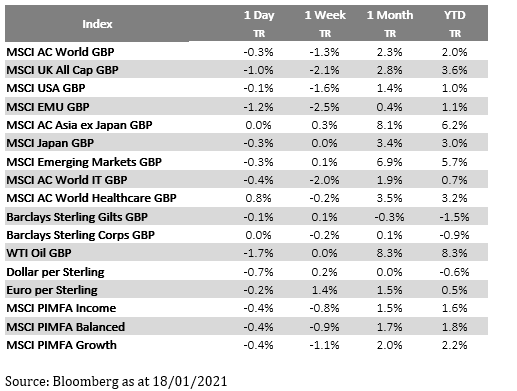

Most global markets fell back slightly over the past week, retreating from record highs set in the first trading week of the year. The falls came after a strong run for global markets that has, unsurprisingly, led to some profit taking. Also weighing on markets has been some disappointing economic data caused by new or expanded lockdowns.

For example, UK retail sales figures released last week saw the worst annual growth since 1955. US initial jobless claims increased sharply last Thursday, hitting their highest level in five months. US retail sales declined for a third straight month and manufacturing activity in the New York state slowed. Then the University of Michigan consumer sentiment index was weaker than had been expected. It is no surprise that markets have adopted a little more of a ‘risk off’ tone.

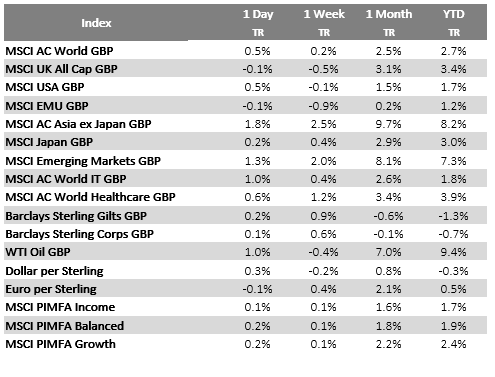

Last week’s markets performance*

FTSE100: -2%

S&P500: -1.47%

Dow: -0.91%

Nasdaq: -1.54%

Dax: -1.86

Hang Seng: +2.49%

Shanghai Composite: -0.10%

Nikkei: +1.35%**

*Data from close on 8 January to close of business on Friday 15 January.

Inauguration week starts on a cautious note

It was a quiet start to the week yesterday, as US markets were closed for Martin Luther King Jr Day. In Europe, markets were mostly higher; the pan-European STOXX 600 rose by 0.20%, France’s CAC 40 closed 0.44% higher at 13,848.35 and the Italy’s FTSE Mib gained 0.53% to 22,498.89.

In Asia, most markets lost ground, but China was the exception. The Shanghai Composite and Hang Seng indices both rose after China reported robust GDP data that confirmed it was the only major economy to expand in 2020.

In the UK, the FTSE100 closed down 0.22% at 6,720.65, while the FTSE250 eked out a gain of 0.12%.

China leads global recovery

China’s ongoing recovery continued apace at the end of last year. It recorded GDP growth of 2.3% for 2020 as a whole but growth accelerated in the fourth quarter, with its economy expanding by 6.5% compared to a year earlier. It was its fastest rate of growth in two years.

China’s growth was largely export driven, although government support for infrastructure projects also gave the economy a boost.

But even China is showing signs of pain during these difficult days. Retail sales came in below expectations, rising by 4.6% in December from a year earlier. While this is impressive by global standards, it was below expectations for 5.5% growth.

We expect China to continue to lead the global recovery in 2021, although growth should be more evenly spread around the world, assuming the roll out of vaccines proceeds smoothly.

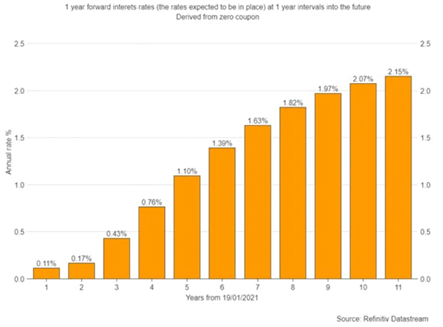

Bond yields rising

Yields were a little lower on the back of this news, but not much. That is despite the very sharp increase in yields we have seen so far this year. This has been a topic of much speculation as the prevailing narrative had been that rates will stay low for the foreseeable future. However, very recently the market has begun to anticipate that monetary policy cannot remain this accommodative forever.

Currently forward interest rates presume that rates stay on hold for the next two years, but then begin to steadily rise. Implied rates have increased significantly over the beginning of the year, mainly in the US. Now those expectations have nudged outside the upper end of the Fed’s forecast range. The chart below shows the market implied interest rate for each year into the future.

Adding to the pressure on bond yields recently has been the fact that some forecasters have brought forward their expectations around the timing of the Fed beginning to slow down its bond purchases, or quantitative easing (QE).

Atlanta Fed president Raphael Bostic, who is about to become a voter on the FOMC, recently said that if the economy bounces back quickly, the Fed may be able to start paring back QE later this year. During the so-called ‘taper tantrum’ of 2013, the 10-year Treasury shot up around 130 basis points in just a few months. There are certainly some parallels between then and the backdrop today, so the bond market is highly sensitive to any discussion about the Fed altering the pace of its bond buying, which is currently at $120 billion per month.

Biden’s stimulus proposal

One of the factors weighing on the bond market is the prospect of extra fiscal stimulus. President-elect Biden announced his plan for spending, and it is eye-watering, at $1.9trn.

He has said he wants $2,000 stimulus cheques for individuals in addition to the $600 cheques already passed by Congress. It also includes $400 a week in emergency unemployment benefits, payable until September, and preventing a cliff-edge cut-off for jobless payments previously scheduled for March.

More controversially he also wants to more than double the minimum wage. This probably isn’t a serious proposition. It’s more of an effort to establish an anchor from which he can give a little ground and still be left with something meaningful at the end of the negotiation.

Inflation expectations on the up

Fundamentally, it has been rising inflation expectations that have been the driving force behind higher yields. Inflation is likely to look as if it is increasing over the coming months, but appearances will be misleading. Year-on-year energy prices will appear to have risen sharply in March when current oil prices are compared to those from a year ago, when prices actually went negative! But this is just a base effect.

There will also be some inflation caused by the reimposition of VAT in some jurisdictions. Statistical factors even imply that there is wage inflation in the current market because job losses in a large number of low-paid roles means that average wages are higher now than they were in 2019. None of these are real inflation, and policy makers will be able to safely ignore them – although headline writers may not.

Overall core inflation remains subdued, but it would be very unusual for it not to rise a little given the increase in manufacturing activity we have seen. In the longer term, more inflationary pressures may build, but for now a gentle increase in inflation gives us a preference for inflation-linked bonds over conventional bonds and reinforces the importance of having some precious metals exposure as a useful hedge.

Brief market updates like this help us get a quick overview of the markets and we share them in the aim of keeping our readers informed.

Today will be a historic day given that, across the pond, it is President Biden and Vice President, Kamala Harris’ Inauguration. VP Kamala Harris will today make history as the first female, first black and first Asian-American US Vice President, a great step towards a more inclusive and diverse future!

Hopefully, we could see positive market movements on the back of this, however, the markets are unpredictable (as have been the events of the world over the past 12 months).

Keep checking back with us for more updates like this.

Please see below update received from Brooks MacDonald earlier today, which analyses global market performance over the past few days.

What has happened

With US markets closed yesterday, equity moves were fairly small and we saw more of a consolidation than any momentum one way or another. That said, European and Asian markets did gain ground with the latter helped by the strong Chinese GDP data at the start of the week.

Yellen’s confirmation hearing

Later today, Janet Yellen, former Fed Chair will set out her plan to the Senate finance committee ahead of her confirmation as Treasury secretary. The prepared remarks have already been leaked and the highest profile phrase is that ‘the smartest thing we can do is act big’. Yellen is expected to reiterate the need for fiscal spending saying that the downturn in the economy could lead to a ‘longer, more painful recession’ if stimulus bills such as that proposed by President-elect Biden falter. The first test for the new President will be the passing of $1.9 trillion of relief measures which may prove challenging given the tiniest of working majorities in the Senate. There will inevitably be questions about the longer-term funding of the deficit created by these measures and the interactions between the Fed and Treasury given Yellen’s former role.

COVID Update

Cases remain elevated across Europe but there are signs that the tougher restrictions are starting to work with Italy seeing its daily cases fall below 10,000 for the first time this year and the UK dipping below 40,000 as Lockdown 3.0 takes effect. Germany is also expected to extend its lockdown further due to concerns over the new variants after being in heightened restrictions for several months. On the vaccine there continue to be impressive numbers out of the UK which is one of the fastest moving of the major economies. The EU are also seeking 70% of the bloc’s population to have had the vaccine by the summer so signs of momentum, or at least ambition, building. In less positive news, California’s state epidemiologist has recommended the pause of the rollout of the Moderna vaccine after severe allergic reactions.

What does Brooks Macdonald think

Yesterday saw a brief lull in market activity after an eventful start to 2021, with central bank meetings, politics and earnings this is unlikely to last too long. Against this backdrop the vaccine rollout has begun in earnest which means that with each passing day the economic risk of reopening marginally reduces. Of course, the question for governments will be what proportion of the population needs to be vaccinated before the risk of the virus is ‘acceptable’, expect this to be a major debate in Q2 2021.

Please check in again with us soon for further relevant content and news.

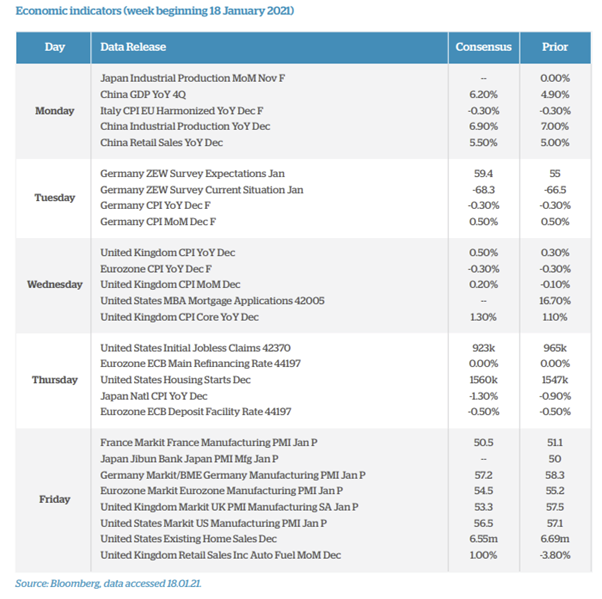

Please see below for the latest Weekly Investment Bulletin from Brooks MacDonald, received by us yesterday 19/01/2021:

US markets are closed on Monday ahead of a busy week of politics, earnings and central bank meetings

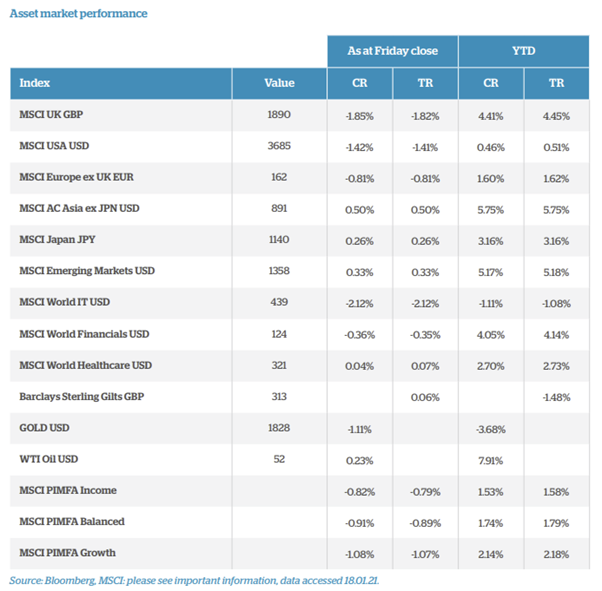

Last week saw most major equity indices decline as risk appetite waned after a strong start to 2021. The primary drivers of this were concerns over Federal Reserve tapering and fears that the new Biden administration may struggle to deliver the proposed fiscal stimulus. More positively, Chinese Q4 GDP showed a beat to the upside with the country growing by 2.3% year-on-year in 2020, a stark contrast to most other G20 nations which are expected to see significant declines.

Wednesday’s inauguration of Joe Biden as US President begins the politically important first 100 days in office

The week starts slowly with Martin Luther King Day meaning that US markets are closed. When they reopen however, politics in both the US and in Europe will dominate the headlines. On Wednesday, Joe Biden will be inaugurated as the next President of the United States and with it the politically important first 100 days will begin. The response to the coronavirus pandemic will be high on the new administration’s agenda with ambitious fiscal stimulus and vaccination goals being mentioned ahead of Wednesday. In February, the new President is expected to unveil a more comprehensive economic plan which will include infrastructure investment as well as policies to tackle climate change. Meanwhile in Europe, reports suggest that Italian Prime Minister Conte will survive a vote of no confidence today due to several abstentions. If these prove correct, this will reduce the near-term risk of fresh elections. Staying in Europe, the German Christian Democratic Union (CDU) have elected Armin Laschet as the new party leader, however it remains to be seen whether Laschet will be nominated as the chancellor candidate for the ruling CDU/CSU (Christian Social Union in Bavaria) coalition for September’s federal election.

Earnings season begins to gain traction this week with a string of banks and tech firms reporting

While we had a small number of earnings releases last week, including J.P. Morgan, this week sees a ramp up across both the US and Europe. The US tends to reach peak earnings momentum a little earlier than Europe so that region will be the focus for the rest of January. This week we have Bank of America, Netflix, Goldman Sachs, Morgan Stanley, Intel and IBM, so a range of sectors but a technology/bank focus. Coming into the season, large cap US equities are expected to see a year on year earnings decline for Q4 2020.

After a quieter start due to the US holiday, this week is likely to become far busier as US politics, European politics, earnings and central bank meetings all arrive. The European Central Bank is the major bank meeting this week and while no material change is expected, markets will be watching the rhetoric closely to see if there are any signs of tightening ahead.

Weekly updates like these are a useful method of frequently updating your holistic view of the markets, especially given the way the world is rapidly changing with Coronavirus.

Please continue to utilise these blogs to help inform your own views of the markets.

Please see below an article received within the hour from Brooks Macdonald which provides a brief recap of the last week and also what could impact on markets this week:

As you can see from the above, politics could have a big impact on markets this week, especially with President Elect Joe Biden’s Inauguration on Wednesday. Also, they will be keeping an eye on this week’s European Central Bank (ECB) meeting.

Please continue to check our Blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.

Please see article below from J.P. Morgan received this morning – 18/01/2021

When will the vaccines allow for a sustained economic recovery?

15-01-2021

For months, the question on everyone’s lips has been, ‘When can we start getting back to normal?’ The short answer is, ‘When the vulnerable have been vaccinated and the healthcare systems are comfortably coping with Covid-19 cases’. The more complete answer is a little more complex. Protecting the vulnerable will facilitate the process of a sustainable reopening but caution will still be required until a broader group are vaccinated, and the timetable will differ around the world. Our base case for major developed economies is that the process of sustainable reopening begins in the spring, and in the latter months of the year we see a meaningful bounce in economic activity as pent-up demand is unleashed.

The charts in this report will be updated twice a week in our tracker for readers to follow the progress of the vaccine rollout.

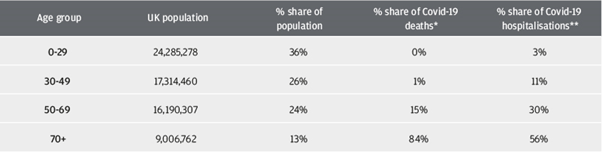

Vaccinating the vulnerable should drastically reduce mortality and hospitalisations from Covid-19

Governments around the world are adopting strategies to vaccinate the most vulnerable first, which should reduce mortality from the virus but also ease the burden on healthcare services. This approach makes sense given Covid-19 causes a disproportionate level of deaths and hospitalisations among older cohorts. In the UK, there are nine million people aged over 70, accounting for 13% of the total population, but 84% of the total Covid-19 deaths and over 50% of total hospitalisations (Exhibit 1).

Exhibit 1: Demographics and Covid-19 in the UK

Source: Office for National Statistics, British Medical Journal, J.P. Morgan Asset Management. *Based on deaths in England and Wales where Covid-19 is mentioned on the death certificate. **Based on an analysis of the first wave published in the British Medical Journal. Data as of 14 January 2021.

Throughout the Covid-19 pandemic we have seen how the health and economic crises have been inextricably linked. If vaccinating the vulnerable significantly reduces the number of new hospital admissions, then governments will feel more comfortable about relaxing restrictions, allowing economic activity to begin normalising.

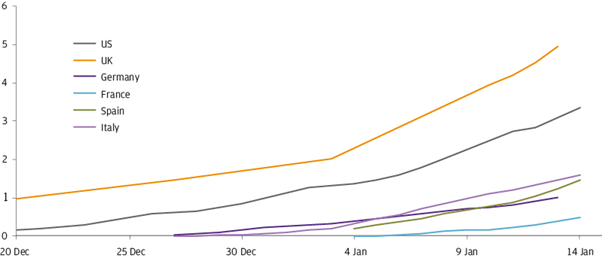

The pace of vaccine rollout is key

At the time of writing, the UK and US have made solid starts in vaccinating their populations, while the major European economies are off to a slower start (Exhibit 2).

Exhibit 2: Covid-19 vaccine rollout Cumulative doses administered per 100 people

Source: Our World in Data, J.P. Morgan Asset Management. Data as of 14 January 2021.

The UK government has announced an ambitious plan to offer vaccinations to its top four priority groups – amounting to 15 million people – by 15 February. These groups include those over the age of 70, frontline workers and those that are clinically vulnerable. The time between first and second dose of vaccines administered in the UK has been extended to 12 weeks to allow as many people as possible to receive at least the first dose, which the government’s advisers view as the best way to reduce mortality and the strain on the health system.

How feasible is it to vaccinate such a large group of people in such a short space of time? In the 2019-20 flu season, the UK vaccinated over 14 million people over a five-month period. The UK health system already has significant experience in vaccinating millions, but it needs to do it around five times as fast as normal. Several mass vaccination centres are planned around the country to meet this ambition, with some vaccinating 24/7. The government has expressed confidence that this will provide sufficient distributive capacity to allow it to meet its goal, and that distribution needs will be met by the supply of approved vaccines, of which the UK now has three.

We think the target is broadly achievable. Whether or not it is achieved exactly to the day is primarily a political concern, but the proposition of having the majority of the UK’s vulnerable with some protection by the beginning of March ought to be a game-changer (as Exhibit 1 suggests) and allow for a process of sustained economic recovery to begin in the second quarter.

The rollout in the US and EU is likely to continue to lag the UK, but both should still have vaccinated the most vulnerable in the first half of the year. Both the Pfizer and Moderna vaccines are approved in the US and the EU, and sufficient doses have been secured to vaccinate the vulnerable population.

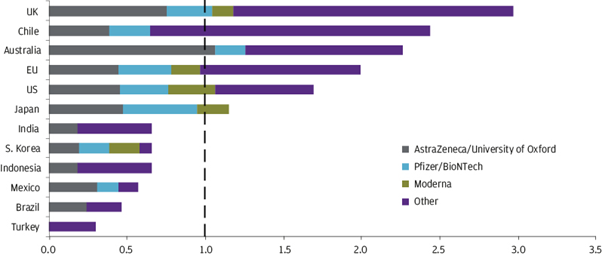

The EU, in particular, will benefit considerably if its regulators approve the AstraZeneca/University of Oxford vaccine in the coming weeks, since it has ordered doses to cover more than 40% of its population and this vaccine is logistically easier to handle (Exhibit 3).

Exhibit 3: Confirmed orders for vaccinations per head of population Complete vaccination courses per head of population

Source: Duke Global Health Innovation Center, World Bank, J.P. Morgan Asset Management. This chart shows the number of complete vaccination courses that a given country has confirmed orders for. Data as of 9 January 2021.

The success of the three pioneering Covid vaccines will have a huge impact in taming the pandemic, but there are also many other vaccine candidates that could be approved in the coming months that would bolster the world’s supply. Novavax and Johnson & Johnson (J&J) are two of 20 vaccine candidates currently in phase III trials, and have large orders confirmed.

However, it is clear that the vaccine rollout will be unequal. The deep pockets of developed governments have allowed them to secure vaccinations to more than cover their populations. Lower-income emerging market countries have order books that fall short of their populations, giving them less room for error in their rollout strategies. As a result, many will have to rely on the COVAX scheme – a consortium set up by the World Health Organisation and others to ensure that all countries have access to Covid-19 vaccines – and can expect a slower return to normality. COVAX has large orders for the AstraZeneca/University of Oxford and J&J vaccines.

One part of the emerging world is less reliant on vaccines for its economic recovery: North Asia. Through effective testing, contact tracing and strict border controls, the region has been able to recover quickly without the help of vaccines. For investors in emerging markets, this disparate outlook calls for a selective approach.

We are optimistic on the path of vaccine rollout, but mindful of tail risks

The rollout of vaccines in the developed world should allow economies to recover sharply in the second half of the year as normality returns and consumers are finally free to unleash their pent-up savings. We expect that the UK and US will have vaccinated over half their populations in the first half of the year, and the EU will reach that milestone during the summer.

The strong rebound in developed market activity should be supportive of risk assets, and in particular stocks that stand to benefit the most from a rotation from the Covid winners to those that lost out from the pandemic. Europe, the UK and the value style stand out in this respect. The emerging markets could also perform well in this environment, driven by continued strong economic performance in Asia and a gradual decline in the US dollar.

Of course, there remain risks. We are less concerned about the vaccine timetable slipping for logistical reasons, and think that plans could even be accelerated. Governments are under tremendous pressure to at least keep up with their neighbouring counterparts. And given the fiscal cost of maintaining economic restrictions, no expense will be spared in driving the rollout.

Uncertainty around take-up is a hurdle for all countries, and surveys suggest a significant degree of scepticism for the Covid-19 vaccine in Europe. Experience in the UK suggests that as the vaccine rollout is proceeding, public confidence is growing, and many may feel increasingly confident of taking up the vaccine as time progresses.

The key risk is that the virus mutates to a new variant that makes the currently approved vaccines ineffective. There is also the risk that vaccine efficacy is lower than initially reported, either among the older population, or across the population from altering the time between first and second doses. Data from trials hasn’t been completely comprehensive in these areas. Many of these risks could be addressed – and rather than derailing the recovery completely, could just provide a setback while new formulations are found. However, we think it prudent for investors to maintain tail-risk protection such as through long-duration government bonds or dynamic fixed income and macro strategies.

A good update from J.P. Morgan with more positive news on the vaccine roll out.

Vaccinating the most vulnerable should drastically reduce mortality and hospitalisations from Covid-19. Hopefully, once the most vulnerable are vaccinated, governments will feel more comfortable about relaxing restrictions, allowing economic activity to begin normalising.

Please continue to check back for our latest blog posts and updates.

Please see below article received from AJ Bell yesterday evening, written by their Investment Director, Russ Mould. The commentary indicates a positive start to 2021 in relation to UK equity markets and predicts market performance for the year ahead.

After a rotten showing in 2020, when the FTSE 100 ranked plumb last among major national indices on a local currency, total-return basis, the UK equity market is off to a flyer in 2021. Whether this is a simple case of every dog having its day or the start of a more fundamental turnaround will only become clear with the passage of time, but what is undeniable is that the FTSE 100 has just had its best start to a year in its history, using the capital return over the first five calendar days’ trading as a benchmark.

FTSE 100’s fast start looks promising for the rest of 2021, if history is any guide

“It is eye-catching to see how the FTSE 100 has generated positive capital returns on every occasion bar one when it has begun the year with an opening-week gain of 1% or more.”

The past is no guarantee for the future, as all advisers and clients know (and the numbers show that a bad start does not guarantee a bad overall outcome). Even so, it is eye-catching to see how the FTSE 100 has generated positive capital returns on every occasion bar one when it has begun the year with an opening-week gain of 1% or more. That exception was 1987 and even that year looked like plain sailing until October, although a nasty reckoning then followed with the Crash.

That episode shows that trouble can come when it is least expected and, as part of any risk-management review, advisers and clients will look at what can go wrong. There is a saying that “bull markets end when the money runs out” and, at the moment, there seems to be no shortage of cheap cash upon which financial markets can feast, as central banks continue to run ultra-loose monetary policy and governments around the world continue to provide fiscal support to their economies, racking up huge budget deficits in the process.

“Spotting misallocation of capital is important when it comes to market tops. In 1999–2000 and 2006–7, overpriced merger and acquisition deals had a role to play. So did a very active market for Initial Public Offerings (IPOs) and secondary sales of stock by either vendors or companies themselves.”

So perhaps advisers and clients need to start wondering where all of this money could go, or what could soak it up, to end the bull run. Spotting misallocation of capital is also key. In 1999–2000 and 2006–7, overpriced merger and acquisition deals had a role to play. So did a very active market for Initial Public Offerings (IPOs) and secondary sales of stock by either vendors or companies themselves. Many of those IPOs were in what turned out to be overpriced tech, media and telecoms stocks in 1999–2000, while miners and junior oil explorers, property stocks and financial investment vehicles took centre stage in 2006–7 (and more of the last-named in a moment), to eventual great cost to buyers of this new paper.

Some advisers’ and clients’ interest may therefore be piqued by the announcement of planned stock flotations by Moonpig, Foresight Group and Dr Martens at the start of 2021, even if the specifics of the individual companies will be left to their preferred UK equity managers to assess.

Functioning markets

In some ways, these new flotations could be a good sign.

They suggest that capital markets are working well and doing what they are supposed to do, which is provide capital that companies can use to invest and hire, create wealth and ultimately help the economy to grow.

Fund managers may also see them as a chance to buy into new, exciting stories that generate capital gains or welcome income over the long term for their clients, or at least offer the potential for a quick turn if a deal looks like it is going to be hot and the shares are going to spike.

However, a sudden flood of new market entrants might also be warning sign, on the grounds that you can have too much of a good thing.

“Not surprisingly given the circumstances, and especially last spring’s stock market rout, newcomers to the London market were relatively few and far between in 2020, although the pace did pick up in the second half and some deals, such as THG, proved to be absolute winners.”

Not surprisingly given the circumstances, and especially last spring’s stock market rout, newcomers to the London market were relatively few and far between in 2020, although the pace did pick up in the second half and some deals, such as THG, proved to be absolute winners.

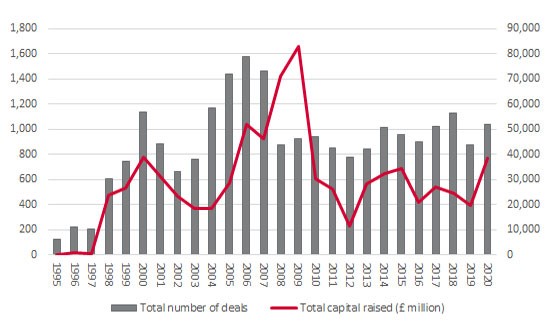

Overall, the number of new issues and IPOs in London last year was the second-lowest since 2009 and the end of the Great Financial Crisis, according to data from the London Stock Exchange (only 2019 was lower).

New issue activity has been relatively quiet in the UK for some time

Source: London Stock Exchange

Over £7 billion was raised by primary offerings, the highest figure since 2017, and that exceeded the sums generated by market newbies in 2009, 2012, 2015, 2018 and 2019.

And with only a select number of names announcing plans for an IPO so far in 2021, it is too early to be pressing the panic button about a deluge of new issues swamping investors and snuffing out the UK market’s attempt to forge a sustained bull run.

The £7.3 billion raised in 2020 came nowhere near the £31 billion of 2006 and £27 billion of 2007, right before trouble hit and the bear market began, or the £18.7 billion peak of the prior cycle in 2000.

Warming up

But advisers and clients need to be on their guard. The US market has shown signs of an overheated new offerings market, especially given the post-listing surges in names such as Airbnb and DoorDash, the coming to market and the lofty valuations at which many new entrants have gone public and the torrent of Special Purpose Acquisition Companies (SPACs) that have listed, in a manner that is eerily reminiscent of 2006–7 on both sides of the Atlantic.

“The US market has shown signs of an overheated new offerings market. The UK is showing no real signs of any of those, which is reassuring, although advisers and clients will also want to keep an eye on secondary offerings too, since they can also soak up cash that could otherwise be deployed elsewhere.”

The UK is showing no real signs of any of those, which is reassuring, although advisers and clients will also want to keep an eye on secondary offerings too, since they can also soak up cash that could otherwise be deployed elsewhere.

Over 950 secondary deals, including rights issues, placings for cash, open offers, subscriptions and further issues took place in 2020, perhaps understandably as many companies tapped their shareholders for fresh liquidity to help see them through the pandemic and the subsequent recession. London-listed and quoted firms raised over £31 billion, the highest figure since 2008–9 when companies were again in cash-raising, crisis-management mode.

Secondary issuance began to pick up in 2020 as many firms scrambled for cash

Source: London Stock Exchange

That meant the total cash raised across primary and secondary deals reached nearly £39 billion, again the highest mark since 2009. Couple that with hefty cuts to dividend payments and a collapse in share buyback activity and it is no surprise that the UK stock market’s headline indices struggled to make headway in 2020.

Total UK equity issuance picked up in 2020 just as dividends and buyback activity fell

Source: London Stock Exchange

Watch the flow

Dividend payments are expected to rebound this year and buyback activity could conceivably start to pick up, too, should the global economy really begin to gain traction in the wake of vaccination programmes.

This remains far from certain, however, and advisers and clients do need to be on their guard in case the steady flow of new deals becomes a flood, especially if deal quality starts to flag and certain hot or popular sectors witness very high levels of activity. This is not a problem in the UK, as Foresight Group, Dr Martens and Moonpig all come from different sectors and industries, but advisers and clients might like to make sure that their chosen fund managers bear in mind Warren Buffett’s warning, should copycat deals start to proliferate:

“First come the innovators, who see opportunities that others don’t. Then come the imitators who copy what the innovators have done. And then come the idiots, whose avarice undoes the very innovations they are trying to use to get rich.”

We will continue to publish relevant market analysis and news, so please check in again with us soon.

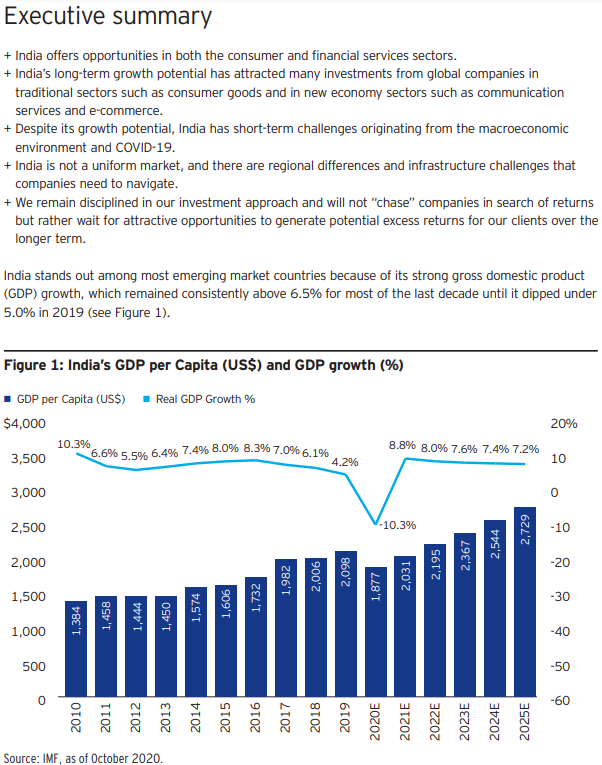

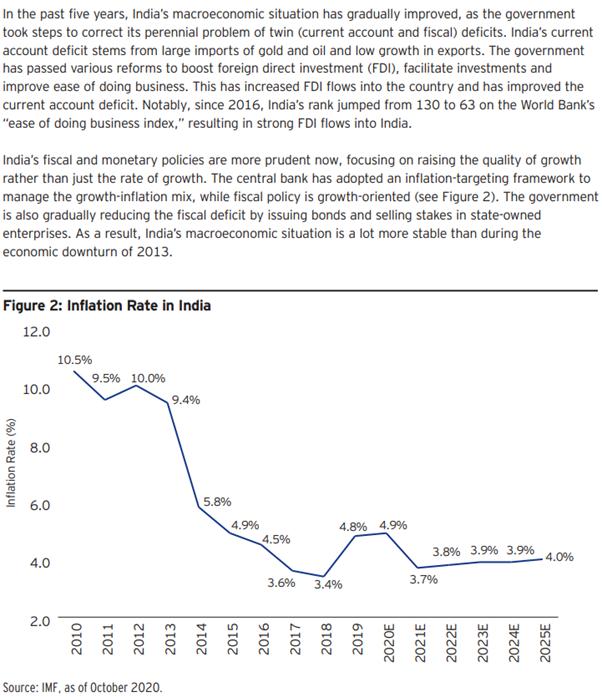

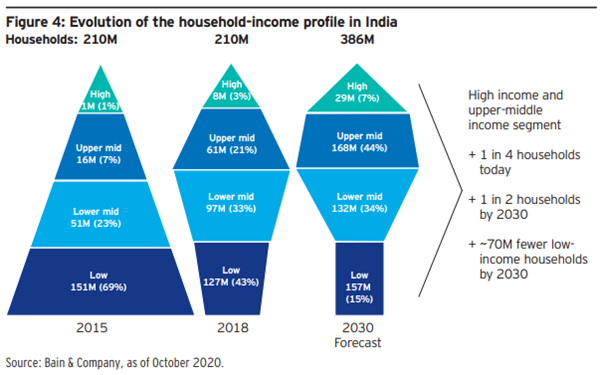

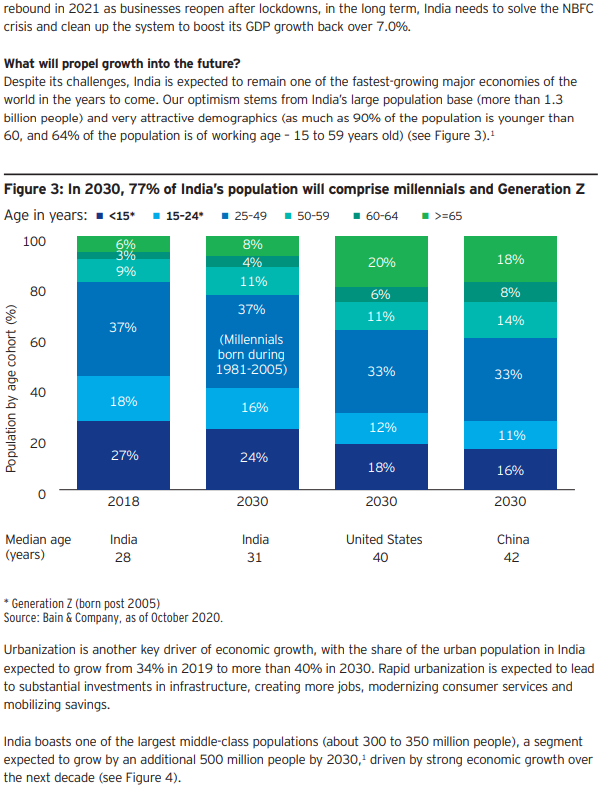

Please see below an article published by Invesco on 8th January and received today, which outlines the long-term growth potential of investing in India:

As you can see from the above, India has faced its issues recently, but the long-term growth prospects for this emerging market remains positive.

Please continue to check our Blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.

Please see article below from AJ Bell – received yesterday afternoon – 14/01/2021

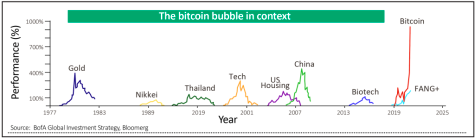

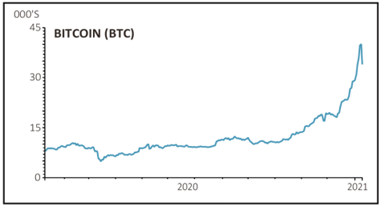

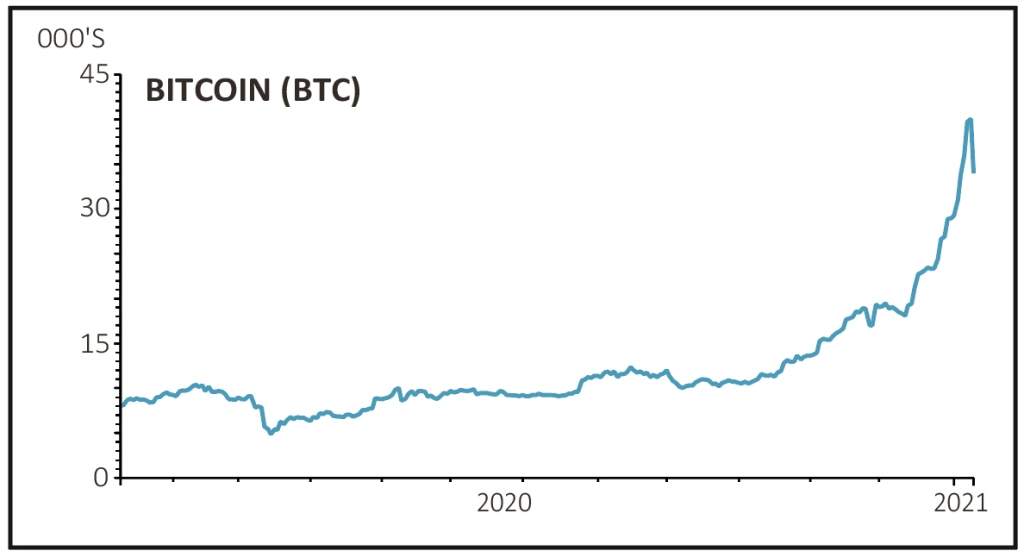

A history-making bubble in bitcoin

There is no reliable basis for valuing cryptocurrencies

Thursday 14 Jan 2021 Author: Martin Gamble

Bitcoin could turn out to be the ‘mother of all bubbles’ according to Bank of America’s Michael Hartnett who has compared the price action of the cryptocurrency to former bubbles in history including the 1979-to-1981 Gold bubble which took the price up 400% in around two years.

As the charts illustrate bitcoin’s gains have been spectacular and over the month to 8 January it had gained 10-fold (it has since lost 25% of its value).

This sort of volatility isn’t normally associated with ‘safe’ assets, but more institutions are taking the cryptocurrency seriously and adding exposure as an alternative to gold as a hedge against inflation.

This feels like a rehash of arguments made over the last 40 years for various assets.

With so much debt being issued since the start of the pandemic, some investors worry about future inflation and see bitcoin as an alternative to gold.

One such institution is asset manager Ruffer which recently purchased bitcoin saying: ‘Bitcoin diversifies the company’s (much larger) investments in gold and inflation-linked bonds, and acts as a hedge to some of the monetary and market risks that we see.’

Hedging a diversified portfolio with bitcoin after conducting thorough research may be appropriate for institutions, but the worry is that recent price momentum has been driven by individual investors looking to make a quick return with little regard for the risks.

As the Financial Conduct Authority (FCA) warned on 11 January, cryptocurrencies offering high returns generally involves taking high risks and investors should ‘be prepared to lose all their money.’

Since 10 January all UK crypto-asset firms must be registered with the FCA under regulations to tackle money laundering and operating without a registration is a criminal offence.

In the long run digital currencies like bitcoin may have a role to play with central banks looking very carefully at them and large companies like Starbucks trialling them as a form of payment.

However high-profile fraud cases like the Mt. Gox exchange in Japan, where bitcoin wallets were emptied, and the assets disappeared, and high price volatility means bitcoin’s entry into the mainstream may be delayed. [MG]

Please continue to check back for our latest updates and blog posts.

Please see below an article published by Brooks Macdonald earlier this week and received today, which details their views on markets in December 2020:

Please continue to check our Blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.

{kind=link}

{kind=link}