Please see below for Brewin Dolphin’s latest ‘Markets in a Minute’ article, received by us yesterday evening 13/07/2021:

Equities mixed as US Treasury yields slide

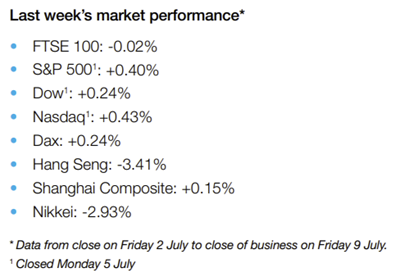

Stock markets were mixed last week as fears about a slowdown in global economic growth led to a steep decline in longer-term bond yields. US indices suffered heavy losses on Thursday as the yield on the benchmark ten-year Treasury note slid to a near five-month low. Although falling bond yields usually increase the relative appeal of equities, investors feared it signalled expectations of a slower recovery from the pandemic. The S&P 500 and the Dow managed to claw back losses on Friday to end the holiday-shortened week up 0.4% and 0.2%, respectively.

The spread of the Delta variant of Covid-19 also weighed on investor sentiment, particularly in Asia where Japan’s Nikkei 225 plunged by nearly 3.0%. Tokyo is being placed under a fourth state of emergency to try to curb the rise in infections. In Europe, the STOXX 600 recovered from Thursday’s sharp pullback to end the week up 0.2%. Germany’s Dax also added 0.2%, whereas France’s CAC 40 slipped 0.4%. The UK’s FTSE 100 was flat as the government confirmed it would ease quarantine rules for fully vaccinated adults and under-18s from mid-August, despite the surge in infections.

Stocks rise ahead of Q2 earnings season

Wall Street stocks were in the green on Monday (12 July) ahead of the start of the second quarter earnings season. Analysts expect strong results from banks such as JP Morgan Chase and Bank of America. The Dow, S&P 500 and Nasdaq all closed at fresh record highs, with the Dow narrowly missing the 35,000 mark. The FTSE 100 edged up 0.1%, with insurer Admiral leading the way on news its first half profits are likely to be higher than expected. Travel-related stocks underperformed amid data showing passenger numbers at Heathrow Airport in June were almost 90% lower than pre-pandemic levels. The FTSE 100 was up 0.3% at Tuesday’s market open, after the Bank of England said it was lifting Covid-19 restrictions on dividends from lenders. Shares in NatWest, HSBC and Lloyds all rose by around 2% following the announcement.

US economic data miss forecasts

A raft of worse-than-expected US economic data weighed on equities and bond yields last week. The Institute for Supply Management’s gauge of service sector activity fell to 60.1 in June, lower than the 63.5 figure forecast by economists in a Reuters poll and down from 64.0 in May. It came amid labour and raw material shortages, which resulted in the survey’s measure of backlog orders rising to 65.8 from 61.1 in May. The IBD / TIPP economic optimism index also slipped from 56.4 in June to 54.3 for July, its lowest reading since February. Elsewhere, figures from the Labor Department showed US weekly jobless claims rose to 373,000 for the week ending 3 July, worse than the 350,000 Dow Jones estimate. Job openings hit a record high of 9.2m in May, which was up 1.7% on the previous month but lower than the expected 9.3m.

UK economic rebound slows

Here in the UK, gross domestic product (GDP) expanded by 0.8% in May from a month ago, down from April’s 2.0% increase and weaker than the 1.5% expansion predicted in a Reuters poll. The Office for National Statistics said GDP growth remained 3.1% below its level in February 2020, just before the pandemic struck. The services sector rose by a weaker-than-expected 0.9% between April and May, as the huge surge in accommodation and food services output failed to offset slower increases elsewhere. Services growth was 3.4% below its February 2020 level. Meanwhile, manufacturing output slipped by 0.1% as the ongoing microchip shortage disrupted car production, leading to the steepest fall in the manufacture of transport equipment since April 2020. Construction output fell for a second consecutive month, down 0.8%, but remained the only sector to have output levels at above its pre pandemic level.

Eurozone retail sales rebound

There was more positive economic data from the eurozone, where monthly retail sales rose more than expected in May following a decline the previous month. According to Eurostat, retail sales rose by 4.6% monthon-month and by 9.0% from a year ago. This was above consensus forecasts of a 4.4% monthly rise and an 8.2% annual increase. The surge was driven by purchases of non-food products and car fuel as several countries lifted coronavirus restrictions. However, the rapid spread of the Delta variant has cast doubt over the speed of Europe’s economic recovery. On Friday, Germany and France warned people against travelling to Spain, where the infection rate is the highest in mainland Europe. The Netherlands said it would reintroduce restrictions on hospitality venues just two weeks after lifting them. Figures from the European Centre for Disease Prevention and Control, reported by the Financial Times, showed the weekly Covid-19 infection rate for the EU and European Economic Area rose to 51.6 per 100,000 people on Friday, from 38.6 the week before. The infection rate is expected to exceed 90 per 100,000 people in four weeks’ time.

Please continue to utilise these blogs and expert insights to keep your own holistic view of the market up to date.

Please see below this week’s article from Brooks Macdonald which was received late yesterday afternoon (12/07) and details their thoughts on markets:

Please continue to check our Blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.

Please see the below article from Invesco received over the weekend:

Key takeaways

Innovation is not just about technology

Not a one size fits all approach to finding opportunities

ESG and innovation are both driving change

Innovation in emerging markets is no longer about applying technologies and techniques from developed economies to play catch to the levels of productivity, income and wealth that took centuries to achieve in the United States or Europe.

Instead accelerating innovating is becoming a driver of growth. Our panellists in the ‘Emerging Markets: Innovation Unleashed’ webinar discuss what is underpinning the fast pace of innovation and how it is evolving.

Many emerging markets countries have a strong track record when it comes to innovation. China has overtaken both the United States and Japan in the number of patents being awarded and for many years, Russia has exceeded the number of patents won by Germany and the UK, while India has recently surpassed them as well.

“Innovation has also shaped consumption patterns in Asia and China,” said William Yuen, associate director of investment at Invesco in the Asia Pacific region.

Yuen has put this down to the rapid adoption of the Internet across Asia. Enormous opportunities have opened up for companies wanting to create innovative products for a digital consumer audience.

On the back of this wave small social media platforms, digital payment platforms and entertainment companies have been turned into mega companies.

But the concept of innovation expands much wider than technology and the Internet. Yuen explained companies are not just innovating for digitalisation, rather research and development has evolved and other consumer broad themes have emerged that are driving change and creating investment opportunities. These include premiumisation, experience, urbanisation and wellness.

“A lot of the spending nowadays is no longer just about getting things done or day-to-day survival,” said Yuen. “It is a lot about experiences.”

As consumers demand more, companies are converting existing products into more sophisticated ones to get a higher margin for the return on their businesses.

To find the companies disrupting the market, Bhvatosh Vajpayee, director of equity research at Invesco specialising in emerging market equities, pointed out there are four major ways investors could do this.

First is to look at the scale of the market. For example, India, South East Asia and Latin America have large pools of consumers. Second is to understand how user adoption and developmental gaps can create leapfrog opportunities.

Third is to find localised solutions as countries differ widely on adoption curves and regulations. Lastly is examining local talent and ecosystems. In China, India and Russia local talent pools in science and engineering are particularly strong.

“Every country, every region is very idiosyncratic,” said Vajpayee. “The one lesson that we have learned over the last few years is do not take the template from one country and try to fit it in some other country.”

Innovations were also driving the adoption of ESG principles at the country level and at a sector level.

“These address decarbonisation, clean water and sanitation, climate change mitigation and digitalisation of course,” said Claudia Castro, director of fixed income research in the Invesco global debt team.

For example, as gas demand fades over the next decade, Russia will potentially have a problem as its pipeline capacity becomes redundant, pointed out Castro. Carbon capture and storage facilities have been looked into as a solution to this.

Speaking about the trend of ESG related innovation, Castro said: “We will not see it reversing, but accelerating.” Climate change is a global issue and countries need to recognise it at a local level.

“You have issues of infrastructure damage, displacement of people, food insecurity from disruptions from climate,” said Castro. “It is really important you have local solutions as well.”

This article again highlights what we have been talking about for the past year, ESG innovation is accelerating.

Emerging Markets is a section of the global markets that can offer the potential for real growth. These markets and the developing countries also have an opportunity to be ahead of the curve when it comes to ESG too by each playing to their own strengths, whether this be market size or technology advances.

Emerging Markets is definitely a sector to watch and include in your portfolio for the potential for some good long term returns.

Keep checking back for our usual market updates, insights and ESG related content.

Please see article below from AJ Bell – received yesterday afternoon 08/07/2021

Cash is being drained from the banking system: why this matters

Is the Federal Reserve reversing course after all?

US journalist Edward R. Murrow may be known for the line which he used to end his broadcasts – ‘Good night, and good luck’ – but this column’s favourite comment of his goes ‘Anyone who isn’t confused really doesn’t understand the situation’.

There is one particularly confusing situation in financial markets right now, and that is the US overnight (reverse) repo market.

A reverse repo is the direct opposite of quantitative easing, in that it drains cash from the banking system. The US Federal Reserve is using reverse repos in vast quantities even as it continues to run QE at $120 billion a month.

That programme means the US central bank’s asset base now exceeds $8 trillion, or more than a third of US GDP, for the first time ever. But as fast as the Fed is pumping liquidity into the system it is taking it away with another. Confused? You should be.

A repo or repurchase agreement sees a financial institution sell government bonds to a bank or central bank on an overnight basis. It then buys them back the next day, usually at a slightly higher price.

The idea is the seller can raise immediate liquidity if required. It also enables the counterparty to make a financial return pretty much without risk, given the short time horizon involved and the collateral backing the trade.

The repo rate spiked suddenly in the US in autumn 2019 in a sign that the Fed’s then-quantitative tightening plan of raising rates and withdrawing quantitative easing was working well – so well that banks were scrambling for cash as the financial system began to creak.

Under Jay Powell, the US central bank backtracked on quantitative tightening and – as the pandemic hit – cranked up quantitative easing to ever-more dizzying levels in 2020. That tidal wave of liquidity means the US overnight repo rate is now 0.07%, down from a panicky 6.9% one-day spike two Septembers ago.

WHAT IS A REVERSE REPO?

A reverse repo or reverse repurchase agreement is when a bank or central bank sells government bonds in exchange for cash to a range of counterparties, over a pre-determined timeframe.

This drains cash out of the financial system, at least if a central bank is doing it and the Federal Reserve is hard at work here right now. At the last count, the Fed’s outstanding reverse repo liabilities were $791 billion, the equivalent to six and a half months of quantitative easing.

POLICY SHIFT

Perhaps the US Federal Reserve is laying the groundwork for tightening monetary policy after all and taking these initial steps to test how financial markets and the economy will react.

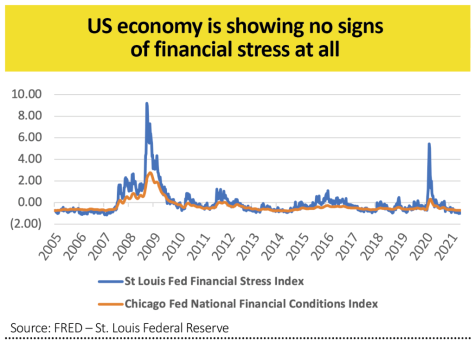

The answer appears to be ‘so far, so good’ on both counts. The S&P 500 index of US shares trades at record highs while there is no sign of financial stress anywhere in the system, at least according to the tried-and-tested St. Louis Fed Financial Stress and Chicago Fed National Financial Conditions indices. Both are trading close to their all-time lows.

As US equity markets trade at all-time highs, American unemployment ticks lower and wage growth reaches 5.7% on an annualised basis and US house prices rise at the fastest rate in nearly 30 years. Perhaps the Fed is getting nervous that there is too much cheap liquidity around.

This initial foray into tightening policy could be seen by Fed officials as a success since neither financial markets nor the economy appears to be wavering.

This is in stark contrast to autumn 2019’s repo rate spike, as that was when WeWork’s much-hyped stock market flotation fell apart, bitcoin sank 25% in a month and wider equity and bond markets both got the jitters, albeit very briefly.

It would surely be a good thing if financial markets could break their addiction to cheap Fed liquidity.

Any business model or asset valuation that is being goosed by zero interest rate policies and quantitative easing will face biggest tests if the Fed really is going to surprise the markets and tighten monetary policy, no matter how gently.

This ranges from loss-making so-called unicorns and equity growth stocks to private equity firms which are feasting off cheap money to make acquisitions.

In theory, tighter money could have negative implications for gold and other real assets. Equally, a fresh backtracking by the Fed and an end to the reverse repo scheme, while quantitative easing keeps running at $120 billion a month, could stoke fresh interest in precious metals and other perceived stores of value.

Gold did well when investors felt central banks were losing control (2007-11 and 2019-2020) and less well when they took the view the authorities had matters in hand (2012-18 and 2021).

Please continue to check back for our regular blog posts and updates.

Please see below for one of Invesco’s latest investment articles, received by us yesterday 07/07/2021:

A year and a half after the first reported cases of a new SARS-like virus in Wuhan, China, we can now look back with greater clarity on a period of some of the most dramatic volatility since the Asian and global financial crises. Here, we assess what this volatility and the associated policy responses have meant for China and emerging markets and plot a dotted line for the road ahead.

Looking up after locking down

At the time the pandemic hit, the unresolved US-China trade war loomed large and global manufacturing was in the early stages of restructuring to accommodate new trade patterns. Despite this, China stood out from other countries in terms of its fiscal, monetary and industrial policy response.

Beijing’s policy decisions focused on maintaining domestic productivity and employment with as little disruption on the demand side as possible. Manufacturers were given liberal access to capital to maintain operations, and refunds on social security tax and unemployment insurance incentivised businesses to retain staff without layoffs.

At the same time, the central bank lowered its reserve requirements and removed blocks on certain loan extensions and renewals. Investments were made in traditional infrastructure projects like housing and transportation, and spending on the nationwide 5G network was accelerated.

As a result, China moved from having a GDP contraction of almost 6% for the first quarter of 2020 to being the only major world economy to print a positive GDP growth number for the year.

A dolorous relationship?

While China’s growth in 2020 is unmatched, the road ahead is not unwinding, particularly when we consider the impact that US policy decisions could have on the US dollar.

The growth of the US fiscal balance sheet in 2020 (accommodated via easy monetary policy) appears to have stimulated real inflation in the US economy – an outcome which has led to talk of tightening. If asset purchase programmes are tapered or rates increased, the likely outcome is a stronger dollar.

Historically, a strong dollar has been negative for emerging markets, as it increases the burden of US dollar-denominated debt. This is less of a factor today than it was prior to the Asian and global financial crises. However, the fact remains that this could dampen growth prospects in some emerging market economies.

Commodities buck the trend

In spite of the observation noted above, it is likely that a stronger dollar will benefit firms selling commodities into US dollar-denominated markets, as long as there is global demand for these products. This factors into the dramatic outperformance we have seen from steelmakers, iron miners, commodity chemical companies, and even coal producers.

The demand behind this outperformance is not part of the same super-cycle seen after China’s admission to the World Trade Organisation, when investment in capacity and infrastructure facilitated the country’s transition to the so-called ‘world’s factory’.

Even when we account for the fact that some of this capacity has moved to other countries in the context of trade realignment, the overall demand for commodity materials is not in the same league as two decades ago.

Instead of a broad, sustainable growth in demand, we are seeing a short-term build-up of inventories that reflects ‘new normal’ uncertainties about tariffs and pandemic lockdowns. This goes all the way through the product cycle, from raw materials to finished goods.

Although these dynamics are almost certainly near-term and should subside in the medium-term, they do attract speculation that disrupts the market.

The road ahead

What does this disruption mean for emerging markets? In the absence of significant inflows, there is a conservation of capital within the asset class. The sharp and transitory shifts described above get funded by parts of the market that have outperformed — in this case growth companies, in particular those in China. In this sense, China has been a victim of its own success as far as its response to the pandemic is concerned, as some investors look to lock-in potential gains.

That said, in our opinion, these sharp transitions do not signify a change in the long-term view for emerging markets. The types of firms that create and capture value for shareholders remain the same.

Even with an ageing population, China remains a large economy with an outlook for sustained, high-speed growth. The growing middle class offers opportunities for investment in education, real estate services, and world-leading innovative technology platforms that facilitate consumption.

It is worth adding that the size and scale of the domestic market should make it less susceptible to external volatility than other markets in the asset class.

What these transitions offer, then, is the potential to invest in the best long-term opportunities at more attractive valuations than normal market conditions afford.

Please continue to utilise these blogs and expert insights to keep your own holistic view of the market up to date.

Please see below ‘Markets in a Minute’ article received from Brewin Dolphin yesterday evening, which provides an update on the markets’ response to the ongoing coronavirus pandemic, the rising UK housing market and economic developments in the US.

Stock markets were mixed last week as the spread of the Covid-19 Delta variant dented optimism about the global economic recovery.

In the US, the S&P 500 and the Nasdaq recorded a fifth consecutive week of gains, rising 1.7% and 2.0%, respectively. Investor sentiment was boosted by betterthan-expected labour market data and a surge in consumer confidence.

In contrast, the pan-European STOXX 600 slipped 0.2% amid concerns about inflation and a spike in coronavirus cases. The UK’s FTSE 100 also fell 0.2%, while France’s CAC 40 declined 1.1% and Germany’s Dax managed a 0.3% gain.

Fears about the rebound in infections spilled over to Asia, where Japan’s Nikkei 225 declined by 1.0%. The Japanese government is considering extending Covid-19 restrictions beyond 11 July, which could affect how many spectators are allowed in Olympic venues.

Morrisons bidding war boosts FTSE

The FTSE 100 rose 0.6% on Monday (5 July), led by an 11.6% surge in Wm Morrison shares after US buyout firm Apollo Global said it was considering making an offer for the supermarket chain. It came after Fortress Investment Group made a £6.3bn takeover bid over the weekend.

UK stocks were also buoyed by the latest IHS Markit / CIPS UK services PMI, which measured 62.4 in June, the second-highest reading since October 2013.

The pan-European STOXX 600 ended Monday’s trading session up 0.3% after figures showed eurozone business activity expanded at the fastest rate in 15 years in June. In contrast, markets in Asia were mixed after the latest Caixin / Markit services PMI showed a sharp decline from 55.1 in May to 50.3 in June.

Stock markets in the US were closed on Monday for the Independence Day public holiday.

The FTSE 100 started Tuesday’s trading session 0.1% lower after the pound rallied against the dollar on news the lifting of Covid-19 restrictions in England will go ahead on 19 July.

Cases rise in Europe for first time in ten weeks

A surge in coronavirus cases weighed on major European indices and bond yields last week. The World Health Organization (WHO) confirmed the number of new Covid-19 cases in Europe had risen for the first time in ten weeks because of increased mixing, summer travel and the rapid spread of the Delta variant.

Hans Kluge, the WHO’s regional director for Europe, said new infections had jumped by 10% and the variant was already causing increased hospitalisations and deaths. At least 63% of people in Europe are still waiting for a first dose of a coronavirus vaccine. Christine Lagarde, president of the European Central Bank, warned of the threat posed by virus variants to the economy, stating: “A Delta variant that spreads quickly is an uncertainty, and it is an uncertainty that will weigh on the balance of risks today.”

In the UK, where vaccination rates are higher, the number of daily deaths remains low despite a surge in infections. On Sunday, there were 24,248 coronavirus cases and 15 deaths, according to UK government figures reported by Sky News.

US consumer confidence at 16-month high

Over in the US, The Conference Board’s index of consumer confidence rose to 127.3 in June – the highest level since the onset of the pandemic in March 2020.

The present situation index, based on consumers’ assessment of current business and labour market conditions, rose from 148.7 to 157.7. The expectations index, based on consumers’ short-term outlook for income, business and labour market conditions, improved to 107.0 from 100.9.

“While short-term inflation expectations increased, this had little impact on consumers’ confidence or purchasing intentions,” said Lynn Franco, senior director of economic indicators at The Conference Board. “In fact, the proportion of consumers planning to purchase homes, automobiles and major appliances all rose – a sign that consumer spending will continue to support economic growth in the short term.”

US consumer confidence

US stock markets were also supported by stronger-thanexpected labour market data. According to the Labor Department, employers added 850,000 nonfarm jobs in June – the most since August 2020. Meanwhile, weekly jobless claims fell to a pandemic-era low of 364,000 for the week ending 26 June, a decline of 51,000 from the previous week.

UK house prices rise at fastest pace since 2004

House prices in the UK grew at the fastest annual rate in 17 years in June, according to the latest figures from Nationwide. The average price of a UK home rose by 13.4% from a year ago to £245,432. On a monthly basis, prices increased by 0.7%.

Northern Ireland and Wales saw the largest gains, up by 14.0% and 13.4% from a year ago. Scotland saw the weakest rate of annual growth at 7.1%, followed by London at 7.3%.

Robert Gardner, Nationwide’s chief economist, said some of the annual increase was due to base effects as June 2020 was unusually weak because of the first lockdown. However, the market continues to show momentum, with prices in June almost 5% higher than in March.

“Activity will almost inevitably soften for a period after the stamp duty holiday expires at the end of September, given the strong incentive for people to bring forward their purchases to avoid the additional tax,” said Gardner. “Nevertheless, underlying demand is likely to soften around the turn of the year if unemployment rises as most analysts expect, as government support schemes wind down. But even this is far from assured.”

We will continue to publish relevant content and news, so please check in again with us shortly.

Please see below the latest article from the Legal & General Asset Allocation Team which was received yesterday (06/07) and details their thoughts on markets:

Please continue to check our Blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.

Investors are often forced to divest when a stock fails their ESG criteria

This can be avoided through active and positive engagement with management

Greater engagement can sometimes lead to better outcomes and returns for investors

Selling a stock because it fails to comply with ESG criteria is not the only tool available to portfolio managers when encouraging companies to change for the better.

Ownership of a stock can give portfolio managers a certain amount of say in how a company is run. This is particularly important when investing for environmental, social and governance (ESG) themes or goals.

If a company fails to resolve significant ESG issues, should managers divest and abandon the company?

Oğuzhan Karakaş of Cambridge University’s Judge Business School said the decision to divest was not the only option available to ESG managers. Highlighting renowned economist Albert Hirschmann’s ‘Exit, Voice, and Loyalty’, Karakaş said investors were typically forced into one of two options – exit or voice – when faced with a difficult situation.

While divestment was an ‘exit’ option, engagement was one of ‘voice’, said the academic, and could be considered more of an art than a science.

“Divestment may look like an easy and obvious option, but it may have some unintended consequences,” he explained. “When we look at ‘sin’ stocks – companies that are involved in alcohol, tobacco or gambling – research shows those companies may outperform.

“One of the reasons is that [if] ‘sin’ stocks are shunned or divested by investors, their prices get depressed and hence offer much higher [potential] returns. In addition, once these companies are divested they are bought by investors that care much less about ESG and could therefore be counterproductive.”

Karakaş said successful engagement could also create value for investors.

“There are some sceptics that [believe] dealing with ESG may cause companies to lose value,” he said. He further noted that, while it could be costly, solving ESG issues could also lead to greater efficiencies and help attract longer-term investors.

Erik Esselink, an Invesco portfolio manager and co-manager of one of our European strategies, said engagement was crucial in the investment process and helped improve the sustainability of portfolio companies.

Using in-house data from Invesco’s proprietary tool – Invesco ESGintel – portfolio managers have access to many data points, insights, metrics, an internal rating and ‘direction of change’, and sector ranking from which they can take a view on ESG risks and opportunities.

Esselink said Invesco managers use ESGintel to engage with companies on issues, to aid their understanding of the magnitude and momentum of any problem, and to ascertain how likely the company is to engage with them.

“We set our price targets three years out based on certain earnings assumptions,” he said. “If we, through engagement, can improve the durability or sustainability of this company, the rating at which we can sell the security in three years’ time will be higher. And our shareholders will benefit in this case.”

According to Esselink, this is particularly true of the small-cap space where data quality is poor, which can lead to some companies with considerable valuation uplift being overlooked.

As an active owner, Esselink votes on every stock in the portfolios he oversees. His ability to put pressure on a company may be limited in some circumstances. However, this is where an asset manager like Invesco can use its considerable passive investment business to bring about positive ESG outcomes.

Matthew Tagliani, head of EMEA ETF product and sales strategy at Invesco, said while passive asset managers may have the scale to influence companies, they often don’t have the in-depth ESG knowledge of an active investment firm.

“We own a large portion of many companies, and we want to wield that strength in a responsible way,” he said. “If there is an active manager in the firm that also owns [a security] we effectively leverage the active portion of the business. It’s called echo voting.”

Despite this internal collaboration, there will still be occasions when divestment is the only option left available to portfolio managers.

“Most companies know when we ask something we want to have a dialogue,” Esselink said. “‘This is not me telling you what to do. This is me wanting to understand why it is you do what you do and to discuss if there is a better way’.”

However, if both parties are at opposites with little room for engagement, then it could mean divestment, he acknowledged.

Passive funds have little choice in this regard, said Tagliani, but they can decide to change the methodology to ensure that companies not meeting investor requirements are not held in the portfolio.

As such, portfolio managers must think carefully before wielding the divest option and consider whether engagement could yield better outcomes, for both the companies they invest in and their investors.

Please continue to check back for more blogs from us.

Please see below article recently received from AJ Bell, which warns of the potential impact that tax relief reform could have on pensions and investors.

Recent press reports suggest the Treasury is eyeing cuts to pension tax incentives to help pay the cost of COVID. Reforms said to be under consideration include introducing a flat rate of pension tax relief, cutting the lifetime allowance or taxing employer contributions.

Beyond the political fire and brimstone a pensions tax raid would cause among Conservative backbenchers and voters, there would be significant practical implications for any of the proposals floated by the Treasury.

Cutting tax relief for individuals risks undoing the groundwork laid by automatic enrolment and sowing mistrust in the stability of the retirement savings framework.

Hitting employers, meanwhile, might raise a fast buck for the Chancellor but would risk strangling off the UK’s pandemic recovery.

There were always going to be tough fiscal choices as the country slowly shifts away from dealing with the health emergency of Coronavirus and focuses on the financial hole blown in the Exchequer’s balance sheet.

It is critical any proposals for pension tax reform consider both short and long-term priorities, and in particular the challenge of ensuring current and future generations’ retirement prospects are not fatally damaged.

Introducing a flat rate of pension tax relief

Given the priority of the Government is to raise cash for the post-COVID economic recovery, a flat rate of pension tax relief would likely need to be set well below 30% to achieve this.

In fact, analysis carried out by the respected Pensions Policy Institute* suggested setting a flat rate of pension tax relief at 30% would actually cost the Government money, while a rate of 25% might save between £2-£3billion a year and 20% around £6-£8 billion a year.

Such huge savings would clearly come at a cost to individuals. For example, if a flat rate of 20% was introduced, a 35-year-old earning £60,000 and paying 4% of salary into a pension could miss out on £50,000 of retirement income by the time they are 67. Those earning more or making larger contributions would face an even bigger hit to their plans.

However, the big challenge in going down this road – both practically and politically – lies in the public sector, where some workers continue to enjoy generous guaranteed defined benefit pensions.

In order to apply a flat rate of relief to these pensions a tax charge would need to be calculated and applied directly to employees by HMRC.

Doctors and senior NHS staff who have been on the front line dealing with the pandemic would likely end up with tax bills running into thousands of pounds as a result.

Reduce the pensions lifetime allowance from £1,073,100 to £900,000 or £800,000

The lifetime allowance has been tinkered with relentlessly by successive Governments, reducing from £1.8 million a decade ago to just £1 million by 2016/17. Two years later it was pegged to CPI inflation – but this link was removed for the rest of this Parliament by Rishi Sunak in March. This constant tinkering has led to huge complexity and uncertainty for retirement savers.

If we were to get yet another cut to the lifetime allowance to £900,000 or even £800,000, as has been suggested, more diligent savers would be at risk of breaching the limit.

To put this in context, reducing the lifetime allowance to £800,000 would mean after tax-free cash has been taken the retirement income someone could take at age 66 would be well below the average salary in the UK.**

This would feel like an extremely low bar to set for people’s retirement aspirations.

Tax employer pension contributions

Of the pension tax proposals floated this was the one with the least amount of detail attached – which is saying something.

At the moment employer pension contributions are exempt from National Insurance, so it is theoretically possible the Treasury could reverse this position – or perhaps apply a limited charge – in a bid to raise revenue.

However, going down this road would cause uproar among businesses already struggling to deal with the fallout from the pandemic. It could also be counterproductive if landing these firms with extra costs forced them to hold off on investment.

Over the long-term, any increase in the costs of providing pensions would likely see a damaging levelling down of provision.

Comment

Pension tax reliefs have been under review since Gordon Brown was the Chancellor in 1997, remember his tax raid? Every government looks at them.

Whilst changing tax reliefs could save money for the State, we need to look at the bigger picture. What would be the impact on pension savings? If people save less in pensions, they will rely more on the State. This is not what any government wants.

I think tinkering with employer pension contributions tax relief would be particularly damaging. Employers need to help fund employee’s pensions.

Hopefully, we won’t see any change in this area, but we also know that we need money now too to support the country in key areas, covid debt interest payments (long term repayment?), to re-build the NHS/Social Services/Residential Care etc., and to help kick start the economy in the UK.

The other issue is timing, Rishi Sunak needs all of us to go out and spend money now to help the economy recover. He can’t scare us into not spending, we will fall back into recession.

Please see the below article from Invesco received yesterday evening:

Key takeaways

Structural changes post-Covid are diminishing the global deflationary narrative

At the same time, a combination of fiscal and monetary largesse are providing a new inflationary force

We believe cyclically sensitive stocks and European stocks in particular could benefit from this new regime

One of the most significant top-down discussions impacting asset prices (bonds and equities) today is inflation: are we heading into a period of inflation or not? The debate has been rumbling since the policy reaction to the Covid pandemic but is now reaching fever pitch as we’ve seen the first above trend inflation data.

As European equity investors, we believe we must have a view. While it would be nice to simply claim that we’re ‘bottom-up’ and ‘fundamental’, the fact is we can’t ignore the polarisation in markets of the last decade, underpinned by monetary dominance and fiscal repression.

Duration (defensive/Quality) assets have benefitted from the low inflation period and short duration assets (cyclical/Value) have suffered. This part is straightforward to understand: medium-term inflation influences the risk-free rate (RFR) and it’s the RFR that the market uses to discount future cash flows. If expectations are for sustained low inflation, then the discount rate is low and asset prices rise and vice versa.

The problem is that forecasting medium-term inflation isn’t straightforward. Nothing causes normally amiable economists to become more tribal than asking them to explain the causes of inflation. In this article, we explain why we believe the arguments for transitory inflation are something of a distraction and point to areas of the market that could do well as mid-term inflation emerges.

Monetarists vs Keynesians and the case for transitory inflation

Monetarists can ‘prove’ inflation is a consequence of broad money growth while Keynesians will eloquently explain that as the demand curve shifts (to the right) faster than the supply curve, then prices rise.

Given we can’t even agree on the definitive cause of price moves then it’s not surprising there’s debate at any moment in time as to what the price moves might be.

The Monetarist vs Keynesian arm wrestle has, we believe, become more visceral since the global financial crisis (GFC) because excess money supply hasn’t led to significant inflation1. This has empowered the Keynesians to look for other rational reasoning of deflationary forces such as demographic trends (declining workforce), technology (increased productivity and labour marginalised) and globalisation (lower cost supply) with post crisis austerity the final straw.

Accordingly, when looking at the post-Covid world, Monetarists have less voice and the Keynesians argue these same three structural trends persist and, hence, any inflation we are seeing today is purely transitory.

This transitory narrative is a function of the severity of the enforced downturn which has impeded but, importantly, not destroyed supply (capital still exists). Therefore, as demand has recovered (surprisingly) fast, supply is temporarily struggling to cope and prices have risen, if only temporarily.

The effects have been exacerbated by the Suez blockage, lack of belly capacity in air transport, low inventories and even the weather in Texas.

If one believes that inflation is ‘only transitory’, logic dictates that it won’t impact the discount rates and therefore duration assets aren’t at risk and short duration cyclicality assets remain value traps….

Time to address the long-term deflationary narrative

The irony is that transitory inflation believers would likely claim to be long term and not worry about the short-term noise. However, we believe they’re perhaps missing the more fundamental structural changes happening post Covid.

We will try to outline why and in doing so will intertwine both economic theories, which we appreciate may anger more purist economists.

Firstly, we need to address some of the structural deflationary points:

Demographics. These are hard to argue with. European demographic trends are unhelpful albeit, net of migration, the data to 2019 suggest population is broadly stable. An aging population likewise doesn’t help. To us it remains an ongoing pressure but not incrementally so.

Technology. Often touted as a deflationary force. It increases productivity and hence pushes the supply curve to the right (we can produce more for lower prices). However, importantly, this is nothing new, innovation has been a relative constant over time. We also wonder if, in the post-GFC period, dominated by monetary policy, corporates were rewarded for ramping shareholder returns (dividends and buybacks) at the expense of investment and so exaggerated the deflationary impact.

Globalisation. We believe this is most contestable as a structural cause of deflation. Transferring production to Asia has undoubtedly been a key deflationary force for at least the past 20 years. China has been both a source of cheap labour and then, through policy, a source of excess production assets. In addition, at times of stress, China has devalued its currency, thereby easing inflationary pressures.

We strongly believe that it’s no longer so obvious. Reaction against the offshoring of US manufacturing jobs to China was a key source of Trump’s appeal. His firmly anti-China policy is one of the few policies the Biden administration has continued to pursue and, with China GDP set to rival the US by 2030, it is unlikely to stop being a vote winner. Within China itself, policy has shifted from emphasising the producer economy towards the consumer with some producing assets being forced to close.

This has been aided by Environmentalism being part of the domestic policy agenda. Lastly, it’s perhaps notable that despite strong domestic wage inflation, and the recent Renminbi appreciation, there’s been no talk of China devaluing – could China actually be exporting inflation?

We should also be aware of emerging market monetary policy setting being more traditional than developed markets currently – it’s developed markets running the largest ever deficits, while China tightens.

Figure 1. The Covid crisis will lead to further de-globalisation

The key point is that these structural deflationary forces, while still present, are a less powerful backdrop than we’ve become accustomed to. Meanwhile, there is the incremental risk from emerging inflationary trends.

Inflationary structural trends – are they here to stay?

Covid has changed voter tolerances, which in turn affects policy. This then has an impact on the economic backdrop and, ultimately, inflation risk.

We believe the true impact of the pandemic goes beyond headline fiscal payments, which are only as inflationary as the next cheque/infrastructure project, and more towards a change in what people truly care about and will vote for.

The post-Covid regime shift is happening to address the issues of Inequality and Climate Change. The vulnerability exacerbated by the health crisis is creating tolerance of big government. Unlike after the GFC, when the response to a financial crisis was fiscal austerity, today the electorate want fiscal dominance. The newly created EU recovery fund, worth €750 billion, is such an example.

Figure 2. Grants and loans from the EU recovery fund (in 2018 prices)

These, we believe, are inflationary forces. Big government is historically a poor allocator of resources compared to the private sector – it curtails supply (the British auto industry in the 1970s is a good example of this).Addressing inequality at a micro level means a greater share of stakeholder profits going to wages rather than to shareholders and management. This would direct resources to lower income earners who have a greater propensity to spend and therefore drive demand.

Inequality at a macro level means infrastructure projects and providing incentives to invest, thereby driving full employment and reducing social scarcity. Full employment as a policy is inflationary.

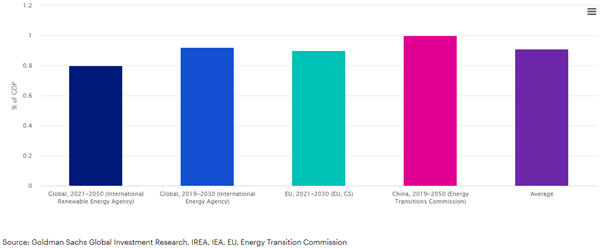

The climate agenda is a wrapper to digest the fiscal shift but it is also inflationary in its own right. Net neutrality requires capital investment: we need to build turbines, solar parks and transmission networks, which creates demand for physical assets.

Figure 3. A rise in green investment demand worth nearly 1% of GDP

However, we also need to build the infrastructure with renewable commodities meaning cement needs to be ‘green’ and steel needs to be low carbon. Some commodity producers will invest and take advantage, but others, previously running for cash, will be forced to close and hence we will finally see capacity come out of the market.

Consumers will be affected too with tolerance for higher prices (especially if wages are increasing) for greener products and replacement demand driven by policy – think replacing vehicles for hybrid or electric alternatives as internal combustion engine (ICE) cars are being banned from urban areas. This is inflationary.

Environmental policy is affecting capital availability already. Financial regulation means asset allocators need to disclose environmental data with the fastest growing asset class being ESG compliant funds.

These fund flows impact corporate capital allocation with environmental projects getting cheaper funding than brown projects. There simply isn’t cheap money available for coal, new oil or other environmentally challenging industries and, hence, over time, there will be a squeeze of supply. We know we are approaching peak oil at some point, however, what happens if peak supply comes first: prices rise – inflationary.

We believe there are some incremental inflationary forces at play, absorbing output gaps. These, combined with the perhaps abating ‘structurally’ deflationary forces will lead to net inflation, but on the condition of monetary complicity.

Monetarists believe money growth is key and MV=PT (or Money Supply times Velocity of money (rate of exchange)) is equal to Prices times Transactions. What does seem to be true is that without money growth, there’s no inflation. Simply because without new money, increased demand growth from, say, Government crowds out private sector demand and so net there’s no growth.

Importantly then, post-Covid, we have both fiscal dominance and monetary accommodation. Post-pandemic, broad money growth has been far greater than following the GFC and we also have a banking system that’s fully functional, i.e. neither deleveraging nor working out bad loans.

Monetary policy makers are shifting their mandate to remain accommodative for longer with targets of full employment and average “synchronised” inflation. This allows developed market central banks to stay ‘behind the curve’, meaning they do not feel the need to address the current inflation scenario.

There’s also consensus that central banks want fiscal cooperation in support of their tired monetary bazookas and will manage the interest costs through yield curve controls if required.

As per the Fischer equation, MV=PT, with ‘V’, the velocity of money, as the balancing item. The ‘V’ is probably best understood as how much the money in the economy changes hands. It has fallen over many years and fell more drastically post Covid as the saving rate has increased. However, we believe ‘V’ will increase as economies unlock, the savings rate falls and inequality falls (lower incomes have a lower propensity to save).

With abundant liquidity meaning banks will be able to lend (even as savings are reduced), central banks printing money and velocity increasing, then prices will rise: inflation.

Transitory inflation is just a distraction – cyclical stocks and Europe set to benefit

We believe that arguing about the short-term transitory inflation numbers misses the key point. Yes, short-term inflation is spiking because of bottle necks. However, asset prices are based on mid-term inflation forecasts, not crisis-related data. Therefore, it’s mid-term inflation we need to think about.

It’s our strong belief that mid-term inflation will be sustained at above central bank targets, albeit not rampant. Indeed, inflation-linked bonds are signalling as much. Yet, the ongoing polarisation of the equity market with preference for long duration and growth equities would suggest something different.

In our view, from a top-down perspective, the types of companies that could benefit from nominal growth are the short duration equities and these are the cheapest parts of the market. We believe they are cheap hedges to the mid-term inflation risk that we have argued for above.

In addition, from a bottom-up perspective, it’s the same sectors and companies that will be a direct beneficiary of the political shifts we’ve mentioned. The environmental agenda is pro-investment; it’s pro-cyclicality.

Companies in industries exposed to construction materials, utilities, automotive OEMs and even banks through volume growth, all might benefit. These are also where currently the most compelling valuations are.

Likewise, the impact from more re-balancing of stakeholder profit shares and fairer taxes with bigger government are less onerous on European companies. This is simply because they have been operating under a more egalitarian environment for longer than other global regions.

Generally, equities are owned with the aim of protecting you from inflation. However, many portfolios that have outperformed over the last decade, and more, have been ones that have benefited primarily from a lack of inflation – so one composed of bonds and long-duration/growth equities.

As we move into a new regime of inflation for the reasons argued, in our view, this type of portfolio is unlikely to do so well. On the contrary, our valuation discipline has resulted in our fund ranges being exposed to short duration or cyclical stocks, which we believe are well positioned in the more inflationary backdrop we have outlined.