Please see article below from AJ Bell – received yesterday afternoon 08/07/2021

Cash is being drained from the banking system: why this matters

Is the Federal Reserve reversing course after all?

US journalist Edward R. Murrow may be known for the line which he used to end his broadcasts – ‘Good night, and good luck’ – but this column’s favourite comment of his goes ‘Anyone who isn’t confused really doesn’t understand the situation’.

There is one particularly confusing situation in financial markets right now, and that is the US overnight (reverse) repo market.

A reverse repo is the direct opposite of quantitative easing, in that it drains cash from the banking system. The US Federal Reserve is using reverse repos in vast quantities even as it continues to run QE at $120 billion a month.

That programme means the US central bank’s asset base now exceeds $8 trillion, or more than a third of US GDP, for the first time ever. But as fast as the Fed is pumping liquidity into the system it is taking it away with another. Confused? You should be.

A repo or repurchase agreement sees a financial institution sell government bonds to a bank or central bank on an overnight basis. It then buys them back the next day, usually at a slightly higher price.

The idea is the seller can raise immediate liquidity if required. It also enables the counterparty to make a financial return pretty much without risk, given the short time horizon involved and the collateral backing the trade.

The repo rate spiked suddenly in the US in autumn 2019 in a sign that the Fed’s then-quantitative tightening plan of raising rates and withdrawing quantitative easing was working well – so well that banks were scrambling for cash as the financial system began to creak.

Under Jay Powell, the US central bank backtracked on quantitative tightening and – as the pandemic hit – cranked up quantitative easing to ever-more dizzying levels in 2020. That tidal wave of liquidity means the US overnight repo rate is now 0.07%, down from a panicky 6.9% one-day spike two Septembers ago.

WHAT IS A REVERSE REPO?

A reverse repo or reverse repurchase agreement is when a bank or central bank sells government bonds in exchange for cash to a range of counterparties, over a pre-determined timeframe.

This drains cash out of the financial system, at least if a central bank is doing it and the Federal Reserve is hard at work here right now. At the last count, the Fed’s outstanding reverse repo liabilities were $791 billion, the equivalent to six and a half months of quantitative easing.

POLICY SHIFT

Perhaps the US Federal Reserve is laying the groundwork for tightening monetary policy after all and taking these initial steps to test how financial markets and the economy will react.

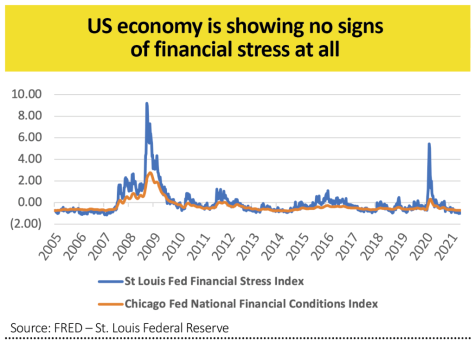

The answer appears to be ‘so far, so good’ on both counts. The S&P 500 index of US shares trades at record highs while there is no sign of financial stress anywhere in the system, at least according to the tried-and-tested St. Louis Fed Financial Stress and Chicago Fed National Financial Conditions indices. Both are trading close to their all-time lows.

As US equity markets trade at all-time highs, American unemployment ticks lower and wage growth reaches 5.7% on an annualised basis and US house prices rise at the fastest rate in nearly 30 years. Perhaps the Fed is getting nervous that there is too much cheap liquidity around.

This initial foray into tightening policy could be seen by Fed officials as a success since neither financial markets nor the economy appears to be wavering.

This is in stark contrast to autumn 2019’s repo rate spike, as that was when WeWork’s much-hyped stock market flotation fell apart, bitcoin sank 25% in a month and wider equity and bond markets both got the jitters, albeit very briefly.

It would surely be a good thing if financial markets could break their addiction to cheap Fed liquidity.

Any business model or asset valuation that is being goosed by zero interest rate policies and quantitative easing will face biggest tests if the Fed really is going to surprise the markets and tighten monetary policy, no matter how gently.

This ranges from loss-making so-called unicorns and equity growth stocks to private equity firms which are feasting off cheap money to make acquisitions.

In theory, tighter money could have negative implications for gold and other real assets. Equally, a fresh backtracking by the Fed and an end to the reverse repo scheme, while quantitative easing keeps running at $120 billion a month, could stoke fresh interest in precious metals and other perceived stores of value.

Gold did well when investors felt central banks were losing control (2007-11 and 2019-2020) and less well when they took the view the authorities had matters in hand (2012-18 and 2021).

Please continue to check back for our regular blog posts and updates.

Charlotte Ennis

09/07/2021