Please see below this week’s Markets in a Minute update from Brewin Dolphin – received late yesterday afternoon – 29/06/2021

Stocks surge as US agrees $1trn infrastructure deal

Global equities rebounded last week after Republican and Democratic senators reached a bipartisan agreement on a huge US infrastructure package.

The S&P 500 and the Nasdaq reached new all-time highs, ending the week up 2.7% and 2.4%, respectively. Energy stocks outperformed as supply constraints pushed oil prices to their highest level since October 2018.

The UK’s FTSE 100 rose 1.7% after the Bank of England said that while inflation could reach 3% in the coming months, this would prove to be a temporary phenomenon. This sentiment was echoed by the European Central Bank, which helped to boost the pan-European STOXX 600 by 1.2%.

Over in Asia, Japan’s Nikkei 225 edged up 0.4% as the country’s vaccination drive helped to outweigh a decline in business activity. China’s Shanghai Composite gained 2.3% after the central bank increased its injection of shortterm cash into the financial system for the first time since March amid growing demand for liquidity.

Travel curbs weigh on European indices

UK and European stocks tumbled into the red on Monday (28 June) after Portugal, Spain and Germany introduced new travel restrictions in a bid to limit the spread of the Delta variant of Covid-19. Germany’s chancellor Angela Merkel reportedly urged the EU to designate the UK a ‘country of concern’ and introduce stricter quarantine measures for British travellers.

The FTSE 100 finished Monday’s trading session down 0.9%, with shares in British Airways owner IAG, travel company TUI and budget airline easyJet all falling by more than 5%. The pan-European STOXX 600 slipped 0.6% and Spain’s IBEX 35 lost 2.0%.

Over in the US, indices were mixed as technology stocks outperformed while some large energy stocks declined. The Dow slipped 0.4% whereas the S&P 500 and the Nasdaq gained 0.2% and 1.0%, respectively.

The FTSE 100 was up 0.3% at the start of trading on Tuesday, ahead of the release of the latest UK mortgage approvals and consumer credit data. The figures for May showed a record rise in mortgage approvals following the recent extension to the stamp duty holiday, and the first lending increase since August 2020.

Infrastructure bill passes first hurdle

Last week, US President Joe Biden and a group of Democratic and Republican senators agreed a $1trn bipartisan deal to upgrade the country’s infrastructure. The eight-year plan includes funding for roads, bridges, railways and public transport, as well as expanding access to broadband and upgrading the power grid.

The plan would be funded by $125bn in unused Covid-19 relief funds, returned state jobless benefits, and greater tax enforcement.

The deal is a significantly pared down version of Biden’s original proposal, however the Democrats hope to push through a separate spending bill worth around $6trn. This would tackle issues such as climate change, education and childcare benefits and potentially be funded by tax increases on corporations and the wealthy.

The announcement helped to boost industrial, energy and financial stocks and outweigh concerns about the most recent US inflation reading.

US core inflation hits 29-year high

The US core personal consumption expenditures price index, an important inflation gauge, rose by 3.4% in May from a year ago – the biggest increase since 1992. On a monthly basis, the index rose by 0.5%, which was slightly below expectations of a 0.6% increase. The Bureau of Economic Analysis said headline inflation, which includes volatile food and energy prices, rose by 3.9% from a year ago – the biggest increase since August 2008, just before the worst of the financial crisis hit.

The increase partly reflected base effects from a year ago, when prices were supressed by the pandemic, as well as supply chain disruptions and growing demand as the economy reopens.

Separate figures showed US house prices are also continuing to soar. The median existing home price rose by 23.6% in May from a year ago, with every region registering price increases, according to the National Association of Realtors. This was a record high and marked 111 consecutive months of year-over-year gains.

BoE views high inflation as temporary

Here in the UK, the Bank of England sought to calm fears about rising prices by stating that while inflation could exceed 3% in the coming months, the surge was temporary.

“The committee’s central expectation is that the economy will experience a temporary period of strong GDP growth and above-target CPI inflation, after which growth and inflation will fall back,” the Bank’s Monetary Policy Committee said.

The Bank said stronger demand, rising commodity prices, supply side constraints and transport bottlenecks were all factors that had driven increased inflationary pressures.

This was reflected in the latest input price component of the manufacturing PMI, published last Wednesday, which hit an all-time high.

Chris Williamson, chief business economist at IHS Markit, said record levels in the survey’s price gauges and further capacity constraints “hint strongly that consumer price inflation has much further to rise after already breaching the Bank of England’s 2% target in May”.

Weekly updates like this from Brewin Dolphin help us keep up to date with what is happening in the markets.

Please continue to check back for our latest blog posts and market updates.

Please see below for Legal & General’s latest ‘Asset Allocation Team’s Key Beliefs’ article, received by us late yesterday 28/06/2021:

There are still a few weeks until Q2 earnings season, but early indications point to mainly positive news when events kick off properly in July. In this week’s Key Beliefs, we also discuss the ‘meme’ stock phenomenon and whether the 1960s pose a historical parallel for inflation today.

We’re in the middle of pre-announcement season for corporate results. While this is always very anecdotal in nature, company comments have so far had a generally positive tone and, perhaps even more tellingly, there has been an absence of any high-profile negative pre-announcements. Results from early reporters, companies with different quarter ends, have had a similar positive tone.

Another positive indicator is that earnings revision ratios have stayed at exceptionally high levels. There are always fewer forecast changes by analysts in between earnings seasons, but from the data that have come in, there have been far more upward than downward revisions. In May and the first few weeks of June, more than three quarters of revisions in the US were to the upside, a figure only matched in the immediate aftermath of recessions and after the corporate tax cut at the end of 2017.

All of this bodes well for the upcoming earnings season and adds confidence to the view that we’ll see another round of significant upgrades to analyst forecasts in the summer. And of course, significant analyst upgrades either put upward pressure on share prices or downward pressure on valuation multiples. We believe the truth will likely lie somewhere in between and continue the pattern of equities grinding higher at a slower pace than earnings estimates, which gradually deflates the high PE (price to earnings) ratios of the immediate recession aftermath.

Retail is here to stay

Retail investors and ‘meme’ stocks have been centre stage again in equity markets in recent weeks. Three things come to mind on the topic from a macro perspective.

First, the extreme moves continue to be limited to a handful of stocks. There are still no obvious signs of the volatility in affected stocks spilling over into the wider market. If you look closely enough, you can see the gyrations of Gamestop* and AMC* reflected in the relative intraday performance of US small cap indices like the Russell 2000. But the S&P 500 put together a long string of daily moves smaller than 1% in the last period of meme stock volatility.

Second, this most recent rally in retail favourites has been far weaker than what we saw in spring. This applies both to the magnitude of the outperformance of the stocks involved and to retail trading volumes. The share of TRF volumes (seen as a proxy for retail activity) of overall US volumes has stayed in the low-mid 40% range, which is far above pre-2020 levels, but a good bit below the nearly 50% mark regularly reached earlier this year. Overall, it’s still fair to say that the froth that was apparent in several retail-driven niches of the market in spring is much less of a concern today. Indeed, SPAC (‘special purpose acquisition company’) activity and prices have dropped a lot, as have prices in the digital asset sphere, like bitcoin.

Finally, if retail is a growing part of equity flows, then we are still in the early part of this story. The activity has so far been concentrated in Robinhood-type investors, who tend to be younger and less wealthy than the traditional retail investor base. US households own just under a third of US equities, but the top 10% of households own almost all of that, according to Goldman Sachs. Private client flow data from brokers show net purchases of equities this year, but their magnitude still pales into insignificance when compared with the previous decade’s net selling. So far, the increase in retail activity appears to have been driven by the smallest section of retail investors. The private client flow data suggest activity is spreading to traditional retail investors, but from today’s perspective we believe this theme remains much more of an upside than a downside risk.

Sounds of the ‘60s

In the mid-1960s, after years of subdued core inflation, there was a sudden increase which began a period of prices ratcheting higher. Unemployment fell through the first part of the decade, but as soon as it reached 4%, both wages and inflation moved up significantly. This suggested the economy was overheating and unemployment had probably breached the NAIRU a couple of years earlier. Indeed, it took a recession in 1970 to halt wage and price pressures temporarily, before the oil-shock induced big inflation of the 1970s.

The simultaneous increase in wages and inflation is a finding consistent with Ram’s econometric work, which shows that neither wages nor prices tend to lead one another; the wage and inflation process seems to happen simultaneously. So, if we wait for wages to move materially higher, we could be too late in spotting the inflation outbreak.

But there were some unique features of the ‘60s:

The Vietnam war played a crucial role. US Federal spending (entirely on defence) shot up by over 1% of GDP from mid-1965 to early 1967. The deployment of over 300,000 more troops served to tighten the domestic labour market further. This episode shows it is not a good idea to add stimulus to an economy already at full employment. The stimulus today has been in response to a large amount of slack, with unemployment still relatively high and participation low. We expect the current labour market demand and supply imbalances to be resolved later this year, but there are some risks if Congress passes a large deficit-funded infrastructure package

Unionisation exacerbated the wage-price spiral. The labour market appears much more flexible today, aided by an increasing number of ‘digital nomads’ or ‘work anywhere’ jobs

In the ‘60s, the Fed had far less sophisticated understanding of the role of inflation expectations (there was no TIPS market) and was less independent. We are confident that the central bank will take appropriate action, should the current wave of inflation not prove transitory

The increase in prices was broad-based. This is a clear difference from today, where the median CPI is still behaving well

In 1966, England last won a major football tournament (though I’m still convinced that the ball never crossed the line on England’s winning goal). This time round, however, we’ll need to wait a few more days to know whether it’s a unique feature of the 1960s or not…

Please continue to utilise these blogs and expert insights to keep your own holistic view of the market up to date.

Please see below article received from AJ Bell yesterday, which discusses the long-term picture after the latest US Federal Reserve meeting delivered a shock.

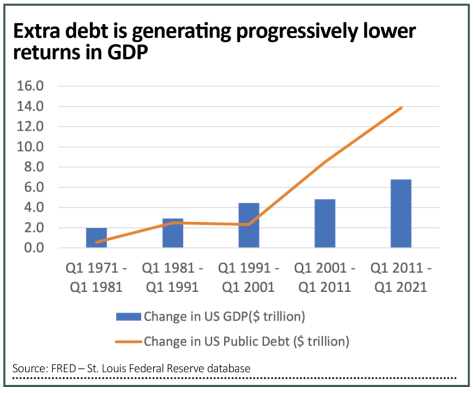

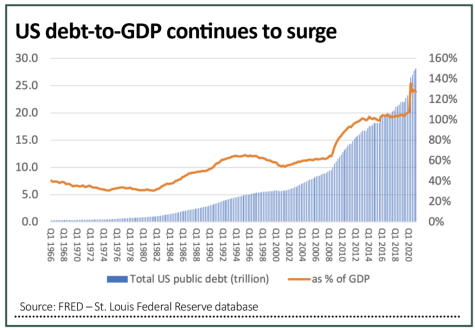

During the first 200 years of its existence, the US accumulated a cumulative federal debt of $1 trillion, the equivalent of 30% of its GDP (gross domestic product). In the last 40 years, that figure has surged to $28 trillion.

The good news is that the US economy has grown too, as annual GDP has advanced from around $3 trillion to $23 trillion. As a result, America’s national debt-to-GDP ratio has therefore grown from roughly 30% to 128% and that is bad news for two reasons.

First, it means that it is taking ever-increasing amounts of debt to generate an extra dollar of GDP.

Second, it leaves the US sitting well above the 80% to 90% debt-to-GDP ratio described by economists Kenneth Rogoff and Carmen Reinhart as a key tipping point, whereby economic growth would slow thanks to (unproductive) debt servicing costs – although that research, used by many governments as the basis for austere fiscal policies in the last decade, has since been widely challenged.

Whether you side with Reinhart and Rogoff or their detractors, the challenge that faces the US Federal Reserve is undeniable.

The US central bank needs to keep interest rates as low as it can to help the US government fund its interest payments even as it maintains welfare programmes, spends on defence, education and other vital needs, such as investment in public infrastructure.

That may leave the Fed having to raise interest rates to fend off inflation, maintain the value of the dollar relative to other currencies and maintain its credibility with financial markets and also holders of US treasuries, since they are effectively bankrolling America’s economy.

Investors now have to assess which way they think the Fed (and the White House) will go and to what degree the central bank’s ultimate policy path is priced into bonds, equities, commodities and currencies.

In the end, every option available to the chair Jay Powell and president Biden may help in some areas but do damage in others, as if to confirm the view of Stanford University professor Thomas Sowell that: ‘There are no solutions, only trade-offs.’

Multiple options

To make a reasoned decision here – and then draw up an appropriate asset allocation – investors will need to think like the Fed and its officials. History is very clear that there are only four ways out once a national debt reaches America’s current levels, relative to GDP:

Rapid economic growth. This is the best option, but it is not proving easy, if the period from 2009 and the end of the financial crisis is any guide. This underpins the push toward Modern Monetary Theory and the argument that governments should spend on productive assets and focus on the long-term payback rather than worry about near-term borrowing.

Default. This is not ideal, as serial offenders like Argentina will attest. It leaves you locked out of international debt markets and means you must pay higher coupons even if you can persuade someone to lend to you. It can also prompt capital flight, hitting both your currency and value of other assets and financial markets. The US will not countenance anything that jeopardises the dollar’s status as the world’s reserve currency (although most other developed countries face the same dilemmas and policy options).

Inflate. This is more like it and is exactly what the US and UK did when debt ballooned thanks to the Second World War. Rebuilding programmes and public spending fuelled growth, interest rates were kept below inflation and lenders were repaid in effectively devalued currency as a result. Yet again, though, this leaves the Fed with the dilemma of stoking some inflation but not too much that investors take fright and both financial markets and the wider economy are destabilised, as happened in the 1970s.

War. This is the option that no-one in their right minds would consider, even if the new Cold War between China and America feels like it is getting steelier by the month, even if president Biden is now in the White House rather than Donald Trump. Taiwan is still a potential flashpoint for ‘Hot War’, both territorially and technologically, thanks to Taipei’s predominance in the global silicon chip supply chain.

Path of least resistance

If growth is unlikely (or least relies on wanton government borrowing and overspending) then inflation still appears the likeliest outcome, but the Fed will not want to tighten policy too far, too fast. Just look at how financial markets are welcoming talk of two Fed rate hikes to the far-from-challenging level of 0.75% by the end of 2023. Equity and commodity price wobbled and volatility indices such as VIX moved higher.

Yet the US 10-year treasury yield fell, the last thing you would expect if inflation is coming, especially when yields are already miles below the current rate of increases in the cost of living.

These trends may not be as mutually exclusive as investors might think. The Fed is still running QE (quantitative easing) flat out to massage yields lower. There is more uncertainty now over its policy direction than there has been for some time. Investors seek havens, like bonds, at times of concern.

Perhaps the bond and stock markets are getting ready for the return of volatility and bumpier times ahead. But then the chances of the Fed raising rates or hauling in QE may recede further, as the end of the debt-fuelled bull market and economic upturn would surely be seen as deflationary and any policy response would have inflation as its ultimate goal.

We will continue to publish relevant content, market updates and news as we optimistically push towards the end of lockdown restrictions in the UK.

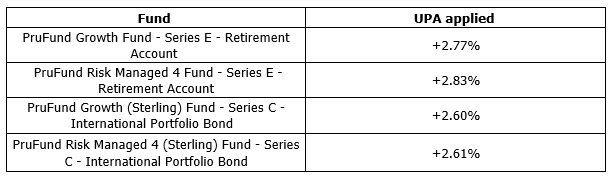

I’ve just cut and pasted this content from an email received this afternoon (25/06/2021) from Prudential about upwards Unit Price Adjustments: PruFund Series E and Series C funds UPA announcement

At this month’s review, we’ve announced upward Unit Price Adjustments (UPAs) to the Series E (Retirement Account) and Series C (International Portfolio Bond) PruFund range of funds.

On the monthly PruFund Investment Date, a UPA is applied if the unsmoothed price is:

4%, or more, higher than the smoothed price, for our PruFund Cautious, PruFund Risk Managed 1 or PruFund Risk Managed 2 funds, or

5%, or more, higher than the smoothed price for our PruFund Growth, PruFund Risk Managed 3, PruFund Risk Managed 4 or PruFund Risk Managed 5 funds.

Growth rates aren’t guaranteed. The value of an investment can go down as well as up. Your client may get back less than they have paid in.

This is good news from Prudential as markets and economies recover. It’s still pretty volatile with both headwinds and tailwinds for investments.

Your best option is to remain fully invested and focus on your long-term goals.

Please see below an article published yesterday (24/06/2021) by A.J. Bell, which outlines factors that need to be considered when thinking about using Property as a vehicle for retirement:

Please continue to check our Blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.

Please see article below from Invesco received yesterday afternoon – 23/06/2021

Is the best yet to come for US Stocks?

In the first year of this new market cycle, stocks enjoyed strong returns alongside expanding price-to-earnings (P/E) multiples and deteriorating business fundamentals. Naturally, investors wondered how stocks could do so well when earnings were so bad?

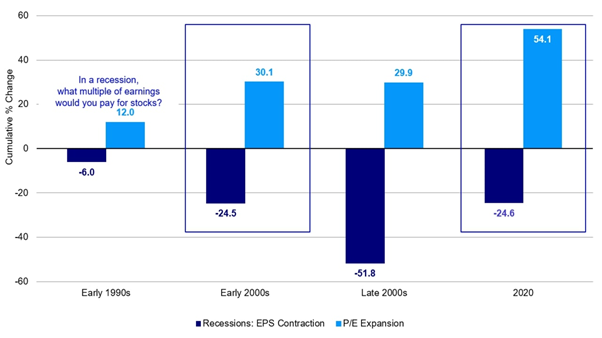

However, the combination of expanding P/E ratios and contracting earnings is far from unusual. Like clockwork, corporate profits fell and multiples rose during each of the last four recessions, including this one (Figure 1).

Figure 1. Like clockwork, earnings fell and multiples rose during each of the last 3 recessions, and this one was no exception

Sources: Bloomberg L.P., Standard & Poor’s, Invesco, March 31, 2021. Notes: Operating EPS = Income from products (goods and services), excluding corporate (M&A, financing, layoffs) and unusual items. EPS = Earnings per share. P/E = Price-to-earnings ratio or multiple of EPS. Economic recessions are defined by the National Bureau of Economic Research (NBER). An investment cannot be made in an index. Past performance does not guarantee future results.

Why? One explanation is it’s a denominator effect. When earnings (E) decrease, they cause the P/E ratio to increase. Another explanation is that stocks, which are leading indicators of business activity, anticipate corporate profits by three to six months. Near major lows in the business cycle, stock prices (P) tend to look across the valley to better times ahead, as they’ve done over the past year.

Aren’t stocks overvalued?

In the second year of this new market cycle, investors are now concerned about lofty stock market valuations with seemingly little room for further gains.

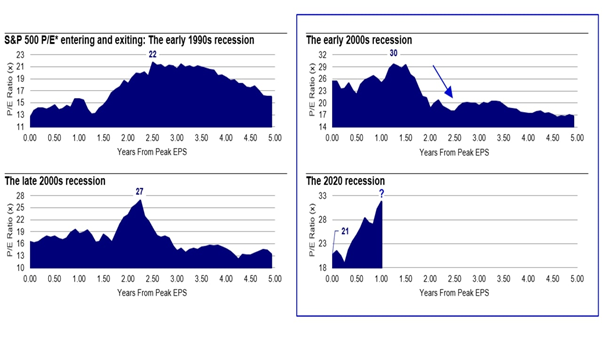

Nonetheless, history informs us that stocks grew into their multiples after every recession since the early 1990s. In each case, it was just a matter of how soon that process began. In the early 2000s, P/Es peaked a little more than a year after earnings peaked.

Currently, we think the stock market is nearing the end of its transition from peak earnings to peak multiples (Figure 2).

Figure 2. Stocks may be on the verge of growing into their multiple, which they did after each recession since the early 1990s

Sources: Bloomberg L.P., Standard & Poor’s, Invesco, 03/31/21. Notes: *Trailing 12-month operating. An investment cannot be made in an index. Past performance does not guarantee future results.

What’s better for stocks? Multiple expansion or earnings growth?

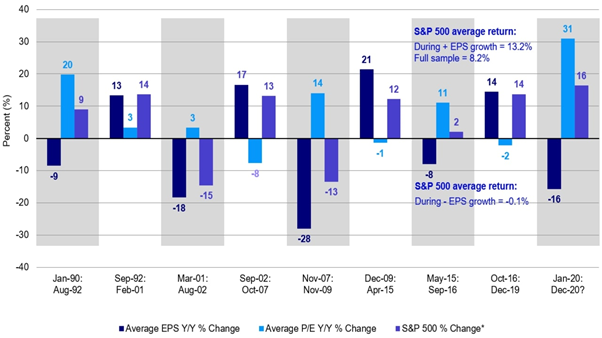

More importantly, my research shows that stocks produced consistent double-digit returns during periods of positive earnings growth over the past 31 years, regardless of what multiples did.

While the stock market did very well last year, the combination of rising P/Es and falling profits hasn’t always been good for stocks. Since 1990, negative earnings growth and expanding multiples actually produced below-average (i.e., flat) stock market returns.

True, multiple expansion helped generate positive single-digit returns in the early 1990s and 2015-2016. But that wasn’t the case in the early or late 2000s, when returns were deeply negative (Figure 3).

Figure 3. Multiple expansion helps, but stocks did best during periods of positive earnings growth, regardless of what multiples did

Sources: Bloomberg L.P., Standard & Poor’s, Invesco, 03/31/21. Notes: *S&P 500 % change = Compound annual growth rate (CAGR). An investment cannot be made in an index. Past performance does not guarantee future results.

After a year of deteriorating business fundamentals, what’s the outlook for earnings?

The good news is that unsmoothed earnings growth is already showing nascent signs of bottoming, much like it did in the relatively short and shallow economic recession of 2001. At first blush, terrorism and pandemics have little in common. Another look reveals that both the 2001 and 2020 economies were struck by endogenous shocks, leading to fear and shutdowns, which gave way to rapid recoveries in confidence, mobility and business conditions. Looking ahead, my framework of leading indicators signals that a V-shaped recovery in earnings growth greater than 20% may be imminent!

As Frank Sinatra once sang, “Out of the tree of life I just picked me a plum. You came along and everything’s startin’ to hum. Still, it’s a real good bet, the best is yet to come.”

Please continue to check back for our regular blog posts and updates.

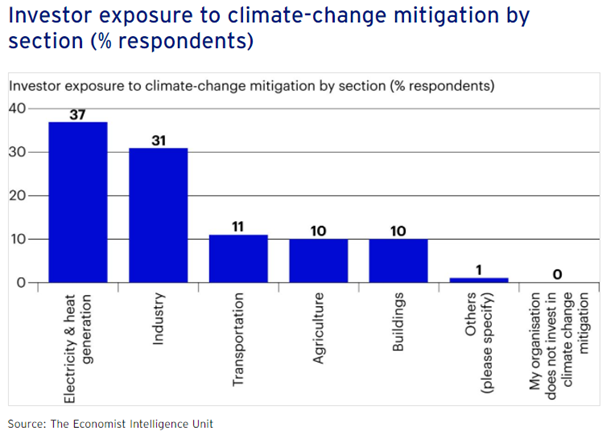

Investors are focusing too much on certain sustainability areas, without paying attention to the broader – or even counterproductive – effects. Invesco partnered with The Economist to explore the topic in more depth in their ‘The art of the possible’ series.

Sustainability is the new investment ‘must-have’. It’s estimated that about 20% of investments are badged environmental, social and governance (ESG) of one form or another, and that proportion grows continually. That’s a lot of money: about $20trn and counting.

This has generated a ‘green rush’—what’s now the largest trend in investment. But it isn’t a silver bullet to make money and do good. Although the positive aspects are very real, there are also challenges: how the benefits and costs of such investments are apportioned—indeed, even down to how they are calculated.

There is, for instance, a persistent disparity between where environmental investments are going—largely towards established technologies such as wind and solar—and integral parts of the sustainability puzzle that remain underinvested. A recent survey of large investors globally conducted by The Economist Intelligence Unit found that electricity and heat generation, followed by industry-related investments, represent the lion’s share of sustainable investments. Jason Tu, cofounder and CEO of ESG analytics company MioTech, is seeing a lot of investor interest in “energy generation, transmission or storage, or usage such as electric vehicles”. He also cites farming technology as a particularly hot topic among investors.

Conversely, buildings, transport and agriculture, despite being major sources of greenhouse gases (GHG), have relatively low uptake.

How useful is ESG?

“The starting point for ESG is flawed,” argues Aswath Damodaran, professor of finance at New York University’s Stern School of Business. “We’re trying to substitute company behaviour for laws we should be passing as a society.”

However, others object that pushing this back onto society or the individual is a distraction from the role large corporations play—and sometimes an intentional distraction at that.

“Professor Damodaran is quite wrong to think that anyone in ESG actually thinks voluntary action is a good substitute for good laws,” says Mark Campanale, founder and executive chairman of the Carbon Tracker Initiative. “Quite the opposite. What ESG does however recognise is that the law is a minimum and we should all aspire to higher standards. When governments abrogate their responsibilities—for example by allowing themselves to be lobbied by powerful business interests to block certain standards—then shareholders can step in and take action.” He points to the recent removal of senior executives at Rio Tinto over the mining violation of indigenous Australians’ historical sites as a good example of this.

Technology is playing an increasing role in exposing these sorts of abuses. Mr Tu cites the use of satellite imagery “to see whether there’s any decrease in greeneries at the plantation, or any kind of signs of pollutants around a 30 km radius of a factory”.

This helps investors ensure that their sustainable projects are actually doing good—and choosing projects where they care about their success is exactly how Professor Damodaran suggests approaching green investing. “My advice to investors is pick your dimension of goodness,” he says. “Each of us has something we think is most critical to us, and invest based on that dimension, which means ESG scores are completely useless.”

How well does a company perform on gender diversity, water usage, emissions and so on? Distilling all these factors and more to one ESG number is obviously problematic. Some investors want as low fossil fuel exposure as possible—while others will intentionally be targeting more carbon-intensive companies—to finance a transition from the brown to green economy. ESG scores cannot resolve this; it’s only the starting point.

Mr Campanale takes a different approach: “ESG scoring is neither an investment thesis nor a strategy. What’s more compelling is to find areas that can demonstrate a valuable impact on society, for example investing in the clean energy revolution, or medical technologies. ESG-led investment research strategies that allow you to invest in a spread of high social impact enterprises is really at the heart of responsible finance.”

Pedal to the metal

Such strategies can’t be summed up in one number. A single ESG score—one number encompassing diverse factors—arguably doesn’t tell you much. A fund or stock can have a high ESG score by being in an industry with a low carbon footprint, such as finance, for example, or simply by reporting on lots of metrics that ESG ratings agencies score on. Some large oil companies, for example, score well on transparency, compensating low E with high G.

A positive impact in one area, earning a good ESG score, can also have a negative impact in other areas, which may not be highlighted by some ESG metrics, and so asset owners may be unaware of important consequences of some of their investments. One example of this is the knock-on effect of low-carbon technologies on metal extraction. These technologies use much larger amounts of metal than fossil fuel-based systems, creating an exponentially rising demand. An electric car typically contains 80 kg of copper, four times as much as a petrol-fuelled one. Both wind and solar power plants contain more copper than their fossil fuel equivalents: a typical solar plant contains about 5 kg of copper per kilowatt versus 2 kg per kilowatt for a coal-fired power station, points out economist Frances Coppola.

“It’s surface level ESG, because you think about carbon footprint, you think people who produce gas cars create this huge carbon footprint,” says Professor Damodaran. “If you create electric cars, you’re good. But electric cars create their own costs. And if you start digging into those costs, the question you have to ask is, are we really trading one devil for another?”

Given the reliance of the green energy transition on poorly regulated mining in these regions, does this not risk minimising the S in ESG? And is this not creating wilful blind spots to other forms of environmental degradation? It leads to the accusation, expressed pointedly by charity War on Want, that this green rush threatens a “new form of green colonialism that will continue to sacrifice the people of the global south to maintain our broken economic model”.

That the developed world has used the available resources, then pulled up the ladder to the global south, is echoed by Invesco’s The 21st Century Portfolio report, authored by Paul Jackson, which notes “the developed world has got rich by using up the CO2-absorbing capacity of the atmosphere, leaving little room for the rest of the world to develop”.

For Professor Damodaran, addressing the issue cannot rest at the door of the corporation: “Much of the ESG literature starts with an almost perfunctory dismissal of [founder of monetarism] Milton Friedman’s thesis that companies should focus on delivering profits and value to their shareholders, rather than play the role of social policymakers,” he says.

This article highlights one of our key points about ESG which we have repeatedly stated over the past year throughout our ESG related content, that ESG is a journey.

It isn’t a ‘one size fits all solution’, its about aspiring to do better.

As the ESG trend continues to grow, fund managers and investors alike, are learning more and more every day. Companies are having to adapt to the increasing ESG standards that are set.

Whilst a company may only score well on one aspect of ESG, it may be lacking in others, however over the next few years, ESG isn’t going away so it’s important to remember that every company will have a starting point and should continue on their journeys to improve in all aspects. If they don’t, they will be held accountable by their clients and fall behind the rest who will be actively trying to improve their ESG ratings.

Keep checking back for our usual market updates, insights and ESG related content.

Please see below an article published by Invesco within the last week covering an interesting topic for us all.

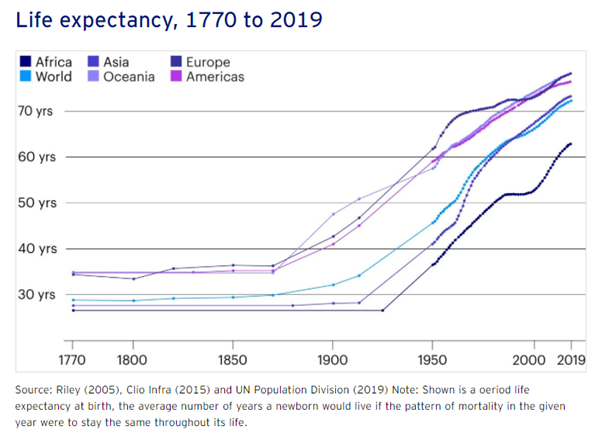

As you can see from the above article, longevity is increasing. This increase in longevity, places additional importance on ensuring you draw a sustainable level of income from your assets in retirement to target maintaining a standard of living that you are accustomed to.

Current industry research suggests that drawing between 2% and 4% per annum of the value of the total invested assets as an appropriate withdrawal rate which should help investors sustain the value of their assets over the long-term.

Global events, such as Covid-19 which had a big impact on markets when it was announced, could accelerate depletion of assets. Receiving ongoing advice in retirement can help mitigate some of the risks and help you protect and sustain your assets.

Please continue to check our Blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.

Please see article below from Invesco received late on Friday afternoon – 18/06/2021

Don’t fear the singularity

Technology is moving up the skill curve. As AI becomes more ‘I’, how far can it go? Invesco partnered with The Economist to explore the topic in more depth in their ‘The art of the possible’ series.

You can look at the revolution in artificial intelligence (AI) in two ways—as two alternate universes, almost. One, where machines support and enhance the human. Star Trek, if you will. The other, where access to technology has created an impassable divide between the haves and have-nots, more like the dystopian film Elysium.

Technology is certainly taking us closer to an automated future, whatever that may be. AI may have started by replacing low-skilled call centre jobs with rather clunky bots, but things are becoming more sophisticated.

Take the field of medicine, for example. To qualify as a diagnostician takes people years of training, and is often an arduous, time-consuming process. What’s more, in many areas, demand for this expertise outstrips supply, putting the healthcare system under strain. But where diagnostic information can be digitised, machines can step in to take the load. “AI is being used to help solve complex societal challenges, such as climate change, healthcare and food poverty,” says Robert Troy, Ireland’s minister for trade promotion, digital and company regulation. The advantage of an algorithm is that it can draw conclusions from the data in a fraction of a second. And, unlike a flesh-and-blood expert, machine-learning expertise can be reproduced potentially infinitely.

Mr Troy is optimistic about the wider ability of AI to transform society. “Globally, it is estimated that the application of AI could double economic growth by 2035,” he says. One study estimates that AI could contribute up to $15.7trn globally in 2030, more than the current output of China and India combined.1

Kevin Roose, author of Futureproof: 9 Rules for Humans in the Age of Automation, highlights the ways that AI is shaping work, such as “labour displacement that we traditionally think of when we think about automation”, although he says this is happening in a broader swath of industries than it traditionally has, through to white-collar workplaces. What’s less recognised is the supplanting of management functions: “There’s now a whole industry of worker surveillance and performance tracking software, and in some cases automatically making decisions about hiring and firing.” Overall, this could lead to the replacement of 47% of current job functions by 2034.2

Data curators

Where does this leave work, as we traditionally conceive it? Two centuries ago, England’s Luddites destroyed the emergent machinery of the first industrial revolution, as a way of combating what they saw as the replacement of manual jobs. Are human workers becoming a thing of the past?

Not really, says Mr Troy, as “much of the disruption caused by AI will result in changes to job roles, tasks and distribution”. Your doctor, for instance, won’t necessarily be replaced by a robot. “AI-based systems will augment physicians and are unlikely to replace the traditional physician–patient relationship,” according to one recent study published in PeerJ.

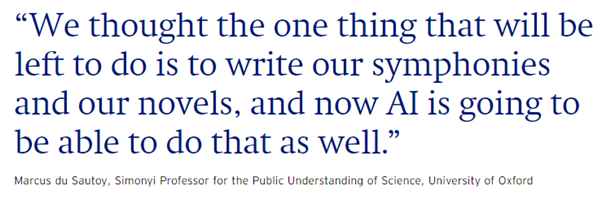

Marcus du Sautoy, Oxford Simonyi Professor for the Public Understanding of Science, agrees with Mr Troy: “We are going to see AI encroach on an increasing number of white-collar jobs, but as with all these revolutions, new jobs appear.”

The abilities of machines can enhance what it means to be human, not constrain it. Professor du Sautoy gives the example of the data curator, calling it “almost a new type of artist”. “Algorithms learn from data,” he says. “You give it data, it will go in one direction, you give it different data, it goes in another.” The still central role of human agency is to understand that process, and how to manipulate it to make it do what you want it to do—something that is a new and very human skill set. So, although AI can mimic artistic styles, from poetry to painting, it functions mostly in an assistant role, rather than replacing the human genius in the loop. The ghost in the machine has yet to become the machine.

Says Professor du Sautoy: “We thought the one thing that will be left to do is to write our symphonies and our novels, and now AI is going to be able to do that as well.” He sees a positive aspect to this, as the imperative to be creative can be terrifying. It’s a high entry level to taking that leap into writing or painting. “There’s something quite exciting about the power of these tools to democratise something that before was quite an elitist activity,” he adds. AI banishes the terror of the blank page. It’s an interesting idea.

Towards a two-tier economy?

Mr Roose predicts the rise of a two-tier economy: the machine economy and the human economy. The products of the former will become very cheap. “AI will enable the people who run those companies to strip out all the inefficiency and waste,” he says.

Conversely, the human economy will consist of people who are not so much making things and providing services as they are creating feelings and experiences, examples being healthcare workers, teachers and artists. And why stop there? Even people you wouldn’t think of as being irreplaceable, such as bartenders, baristas and flight attendants, fit the bill because they’re about making people feel comfortable. It’s the human touch that is so important.

Mr Roose reckons that this will increasingly see hyper-scale tech companies create higher-touch versions of their services: for example, a luxury version of Netflix, where film curators pick out movies for you. “There will be layers within these companies where users pay for human interaction on top of the base layer,” says Mr Roose. He predicts a new generation of companies that scale human connection without dehumanising it.

Does this mean that the tech leviathans will dominate everything? Professor du Sautoy doesn’t think so—but he does believe changes need to be made to ensure an open field. “You don’t need huge companies to analyse this data,” he says. “It’s about having clever algorithms to search data allowing smaller players to come into the field.”

However, he cautions, “If you don’t have access to data, you’re completely stuffed, frankly.” There are already examples of this in open source data—for instance, open banking regulation, which compels large banks to share their customer financial information. This has enabled disruptors in fintech, such as UK challenger banks Starling and Monzo, each now valued at more than £1bn, to enter the playing field.

There are, of course, strong vested interests with this. But that’s also true of ‘traditional’ financial services, and yet the field was still opened. Could the same be done with AI?

Please continue to check back for our regular blog posts and updates.

Please see below a comprehensive and insightful investment article received from JP Morgan, which provides educated predictions for the second half of the year and considers what might lie in store for global economies.

THEME 1 – INFLATION SIMMERING BUT NOT YET BOILING OVER

Developed economies are expected to continue their strong post-lockdown bounceback in the second half of the year. Vaccine rollout is well advanced in the US and UK, and continental Europe is quickly catching up. Despite recent spending, we estimate that households still have considerable excess savings as we head into the second half of the year, amounting to about 12% of GDP in the US, 7% in the eurozone and 10% in the UK.

Not all sectors of the economy are returning to normality: travel restrictions are likely to remain in place until governments are more confident that vaccination levels can cope with new strains of the virus. However, consumers are spending where they can and tourism’s loss appears to be home renovation and construction’s gain. Housing markets are booming in much of the developed world.

For now, it is rising consumer prices, rather than house prices, that central banks are monitoring. After over a year of pandemic-related disruptions, supply is struggling to keep pace with surging demand. Alongside soaring global commodity prices, input costs are on the up, with many companies passing cost increases on to end consumers. US CPI inflation is likely to remain above 3% into next year, and eurozone and UK inflation also looks set to rise in the coming months (see On the Minds of Investors: Monetary and fiscal coordination and the inflation risks).

Central banks believe these inflationary pressures will prove transitory. Whether this turns out to be the case depends in large part on the behaviour of labour markets. If workers are able to bargain for higher pay, inflationary pressures will become more entrenched.

Unfortunately, labour markets are as hard to predict as goods markets at this point. For example, in the UK, the unemployment rate has risen to 4.7%, but is well below the 8.5% peak it reached following the Global Financial Crisis. But 8% of the workforce are still on furlough, making it hard to gauge the true degree of labour market slack. In the US, the unemployment rate did rise sharply and, at 5.8%, still sits 2.3 percentage points above the pre-pandemic low. And yet firms are saying they are having more difficulty recruiting than at any point on record.

Inflation is likely to create market jitters in the second half of the year, but ultimately we believe it will take a lot to shift the central banks away from their current preference for tightening too late, rather than too early. Talk of tapering by the Federal Reserve (Fed) will no doubt become louder over the summer, but our base case sees a reduction in asset purchases beginning only at the start of 2022, with rate hikes not until at least the following year. In the eurozone, large asset purchases are set to continue for a long time in the context of still subdued inflationary pressures, even if we see some shuffling of purchases among the European Central Bank’s (ECB’s) various purchase programmes. Recent commentary from the Bank of England (BoE) suggests that policymakers may be open to tightening policy a little more quickly in the UK, but it should still be a debate for next year rather than this.

This new, more patient reaction function from the central banks is not without risks. A willingness to let the economy run hot sets up a strong near-term rebound. Yet, once the time for rate hikes arrives, we see a risk that central banks (especially the Fed) will have to tighten policy more quickly than the market currently expects.

Supportive policy from developed world central banks will help emerging economies catch up. While some economies, such as China, came through the pandemic relatively quickly, others are still struggling to contain the virus. However, we expect the vaccine delay in key parts of the emerging world to be a matter of quarters rather than years and believe economic activity should prove relatively resilient given the strength of global goods demand and commodity prices.

Overall, we think the outlook for near-term global growth remains strong. As the bounce from pent-up consumer spending fades, we expect government and business spending to pick up the baton. Focused on ‘building back better,’ governments are lining up multi-year infrastructure projects. This marks a stark contrast to the last cycle, in which government austerity proved a consistent drag on activity and inflation.

It is also remarkable to see how quickly investment is bouncing back, again in stark contrast to the last cycle. Indeed, if inflation is the greatest downside risk for investors to monitor, investment spending is the key upside risk, since it could potentially herald the start of a new era for productivity growth and help alleviate inflationary pressures.

Overall, the macro backdrop for the second half of the year remains strong. Growth in the developed world may slow by year end, but is likely to remain above trend, broadening out to investment spending and becoming more evenly distributed across geographies. Inflation concerns are likely to linger, but ultimately we think it will take a lot of bad news for central banks to meaningfully alter their current plans for a glacial removal of stimulus. While this approach may create further risks down the road, economic activity and corporate earnings look well supported for now.

THEME 2 – STICK WITH ROTATION INTO VALUE

The key question for equity investors is how moderately higher inflation and bond yields will affect corporate profits and valuations. Given significant pent-up consumer savings and elevated capex intentions, sales growth will likely be strong. When sales are strong, profits tend to rise, even if input costs are rising.

Higher bond yields could raise borrowing costs but this can also be offset by higher sales, while higher wages tend to boost sales as well as costs. Meanwhile, any additional taxes that hit the corporate sector are likely to be at least partially offset by the demand boost from additional government spending.

So, against the current economic backdrop, it seems unlikely that rising costs will fully offset the anticipated benefit from strong sales growth. Higher inflation is therefore likely to coincide with higher profits, as is normally the case.

The bigger concern for investors is whether higher bond yields will hurt equity valuations, since it raises the discount rate on companies’ future earnings. However if bond yields are rising because growth expectations are rising, then valuations don’t have to decline. Indeed, it is common for valuations to rise (and fall) at the same time as bond yields. Even if rising bond yields do lead to lower valuations, then as long as profits rise by more than valuations decline, stocks can still rise. Our base case is that rising corporate profits, driven by strong demand, will offset any decline in valuations for most stocks.

Growth versus value is another key debate as we head towards 2022. So far in 2021, last year’s losers have outperformed last year’s winners, with value stocks significantly outperforming growth stocks. Despite this, growth stocks still trade on high valuations compared with history and relative to value stocks.

Given that we believe 12-month forward earnings expectations are likely to keep rising for most stocks, the biggest risk to our continued optimism on equities is that valuations on the more expensive growth stocks decline by enough to offset the earnings upside.

However, our base case is that any further compression in the valuations of growth stocks will just limit the extent of their upside, rather than fully offset the expected increase in earnings. While we do not expect further price/earnings (P/E) expansion on value stocks, valuation compression seems less likely than for growth stocks, given much lower starting valuations.

For example, consensus expects 12-month forward earnings on the Russell 1000 growth index to be 19% higher by the end of next year, compared with 17% higher for the Russell 1000 value. Both indices should therefore rise, but even a modest decline in growth stock valuations relative to value stocks could lead growth stocks to underperform.

At the very least, it is worth being aware that a large part of the reason for the outperformance of growth stocks since 2009 has been the substantial increase in their valuations. A repeat of that tailwind seems unlikely from this starting point, and it is possible that it could now become a headwind, if valuations on growth stocks continue to decline. Value stocks, by contrast, are unlikely to see P/E compression, given valuations remain relatively modest.

It is also worth noting that financials are by far the largest part of value indices globally. Over the last decade, their relative performance has been highly correlated with 10-year bond yields. We therefore expect financials – and hence probably broader value indices – to outperform, if we’re right that bond yields will rise further from here.

Overall, we believe equities will move higher but at a slower pace, and with the potential for the usual bumps in the road. We also have a moderate preference for value over growth stocks, based on relative valuations and our view that bond yields will continue to rise.

At the index level, this means the US could underperform other regions, because of its large weighting to more expensive growth stocks. US value stocks could continue to perform well though, while more value-oriented markets such as Europe and the UK could outperform. For investors keen to avoid putting all their eggs in the value basket, we believe emerging markets offer long-term growth opportunities at a more reasonable price than some other markets.

THEME 3 – RETAIN FOCUS ON ASIA’S DECADE

Asian equities began 2021 with a lot of promise. Favourable longterm trends in demographics and technology, in combination with better containment of the pandemic, provided a strong tailwind for the region (see On the Minds of Investors: Asia’s decade: Getting ahead of the growth opportunity).

Since February, it seems that the tide has turned. Absolute performance stalled, while US and European equities stormed ahead. While part of the story relates to better developed market prospects following President Biden’s massive fiscal stimulus, the relatively poor performance of China since February has been a significant source of the underperformance of Asian equities.

This may seem surprising given that China’s economic outlook for the year appears compelling. Due to its early success in containing the pandemic, China looks on track to achieve more than 8% GDP growth in 2021.

However, three near-term challenges have investors concerned. First, Beijing has begun tightening policy after an expansion during the crisis amounting to growth in credit stock of over 30% of GDP. Second, a number of new announcements about tech regulation have generated worries about Beijing’s reform agenda. And third, in Asia the vaccination programme has been slower than those of many developed economies leading to lingering virus concerns.

We are not overly worried that these headwinds will provide a lasting drag on either economic or market performance. Any tightening of credit will be gradual and measured. Consumer inflation is currently contained, giving China’s central bank little reason to raise policy rates in the coming months. Therefore, current policy measures should be understood as normalising and not as outright tightening.

While not overly worried about tightening, neither do we believe China’s reform efforts should deter international investors. Faced with monopoly concerns, worries about financial stability and changing public sentiment, regulators are taking a more hawkish approach towards leading tech and financial companies. Recent high-profile fines for companies breaking competition laws, as well as the closing of regulatory loopholes, may signal the end of the highly supportive environment that these firms have enjoyed in recent history.

Given the weight these firms have in both Chinese and broader Asian indices, their underperformance has had a significant impact on overall returns. While the market leaders might be constrained by potential new rules in the short term, we believe their long-term growth outlook remains compelling, and valuations are now more attractive.

And on vaccinations, China is now making significant headway in catching up on vaccinating its population (EXHIBIT 7). In India, meanwhile, only 19% of the population are over the age of 50, so while the current outbreak is taking a heavy toll, it shouldn’t be too long before the most vulnerable have been vaccinated. In some smaller Asian countries, the slower pace of vaccine rollout may lead to ongoing problems with local outbreaks, delaying a full economic recovery this year.

In summary, while we acknowledge that President Biden’s stimulus has provided a near-term turbo boost to the US economy, we do not think developed market outperformance will last over the medium term. US and European policymakers will soon face the very same tough questions as their Chinese counterparts today – when and how to normalise the enormous amount of stimulus. So in 2022 and the following years, dynamics are likely to change as the distortions in corporate earnings caused by the pandemic and the policy responses recede. In this environment of more moderate growth, structural themes such as rising household incomes and technology adoption in Asia should gain importance relative to the cyclical stories that dominate today’s market performance. Since we are already in the middle of the year, it will be just a matter of time before investors shift their focus to the earnings outlook for next year, which should be beneficial for Chinese as well as broad Asian equities.

In the second half of the year, the outlook for Chinese local bond markets continues to be compelling. Moderate consumer inflation, solid corporate earnings and a low probability of rate hikes are supportive for the asset class. However, after the 10% appreciation of the renminbi in the past 12 months, we think that investors should expect a reduced tailwind from currency effects.

THEME 4 – CONSIDER PORTFOLIO IMPLICATIONS OF COP26

In early November, major nations will reconvene to discuss global plans to tackle climate change. COP26 (the 26th UN Climate Change Conference of Parties) will see leaders revisit the commitments that were made under the Paris Agreement in 2015, assess the progress to date and set a roadmap for the future. The legally-binding commitment made in 2015 was to limit global warming to well below two degrees Celsius, compared to pre-industrial levels, by the end of the century.

What is different about this annual meeting is that the US is back at the table, providing renewed momentum. Top of the agenda will be to compare national greenhouse gas emissions outcomes to those planned, and assess whether they are sufficient to achieve global climate objectives.

The conclusion is likely to be that greater efforts are required – though many governments have already accelerated their plans. The EU plans to reduce its emissions by 55% by 2030, while achieving net zero emissions by 2050 has recently become the new benchmark. In 2020, the UK and France were the first major economies to write their net zero emissions targets into law, and many other countries, including the US, are now following their example. China has given itself an additional decade with net zero emissions targeted for 2060.

The realignment of the US with global climate initiatives is a gamechanger. Having organised a global climate summit on Earth Day and supported a G7 announcement to end fossil fuel subsidies by 2025, the US will probably support a new Grand Climate Accord during COP26.

With the major economies already aligning behind the goal, reaching net zero emissions may well become the new official global target. This will require dramatic changes to the global economy, and we expect a wave of new policy and major investments in green infrastructure to be announced at COP26. However, to reach net zero emissions, policymakers will also need to increase private sector incentives to reduce carbon emissions, so carbon pricing initiatives such as emissions trading schemes (ETS), and carbon taxes are also likely to be key topics of conversation at COP26 (see On the Minds of Investors: The implications of carbon pricing initiatives for investors).

However, such discussions could lead to trade tensions as countries try to lay blame – and the need to change – at others’ doors. By country, China is the biggest emitter of greenhouse gases (EXHIBIT 8). But looking at the data by capita suggests the US has the most work to do. Others will argue the most appropriate comparison takes into account stages of economic development or reliance on manufacturing for GDP. This may hinder the group’s ability to agree on a common solution.

Obstacles to progress may prove particularly frustrating for Europe, which is far more advanced in this area, and keen to ensure that its own high regulatory standards are matched elsewhere, so that measures such as higher carbon prices in the EU don’t damage the profitability or competitiveness of the region’s companies (EXHIBIT 9). If the EU, China and the US cannot agree on a path towards a common carbon price, the EU may need to find a short-term solution to ensure that its climate efforts do not disadvantage European businesses.

One solution that appears to be growing in appeal in Europe is a carbon border adjustment mechanism (CBAM). This import tariff would be designed to ensure that the environmental footprint of a product was priced the same whether it was manufactured locally or imported.

Investors should be aware of how announcements at and after COP26 might influence their portfolios. Some companies will benefit from new green infrastructure investments, or from being relatively well prepared for the transition compared with their peers. Others may lose out – particularly firms that will face higher costs due to higher carbon prices, and especially if they are unable to pass these costs on in higher prices.

THEME 5 – SEEK PROTECTION FROM CHOPPY WATERS

As economies continue to open up, we are expecting a strong rebound in growth, with potentially sticky inflation. When central banks take their foot off the pedal and begin to apply the brakes, bond market returns suffer. The first quarter, which saw a loss of over 4% for US Treasuries – their largest quarterly drawdown since 1980 – is a case in point. With this backdrop, clients are wondering what role bonds should play in a balanced portfolio in the coming years (see On the Minds of Investors: Why and how to re-think the 60:40 portfolio).

There is no doubt that the return outlook for fixed income is challenging. In the past, the coupons that bonds paid at least cushioned the blow of rising rates. For example, during the Fed’s last hiking cycle (December 2015-December 2018), the price of US Treasuries fell by around 2% but the coupon paid over the period more than made up for that loss, such that total returns were still positive at around 4% over that period. Over the same period, global investment grade government bonds managed to return roughly 12%. Today, with starting yields and spreads so low, there is very little income to cushion against rising rates (EXHIBIT 10).

It might be tempting then to exclude bonds from portfolios altogether. However, that would lead to much higher portfolio volatility and little protection against unforeseen downside risks. For example, should the virus mutate to the extent that vaccines are no longer effective, government bonds would likely be one of the few assets generating positive returns.

In our view, investors should consider fixed income strategies that have the ability to invest globally in search of greater income protection, and which can move flexibly in the event of changing economic winds.

One global solution that, in our view, looks particularly attractive today is Chinese government bonds, which currently yield over 3% and benefit from a strong credit rating. A relatively low average duration also makes them less vulnerable to rising yields. Chinese bonds have proved to have a low correlation to both global bond and equity markets, making the market a good source of portfolio diversification (EXHIBIT 11). The Chinese onshore fixed income market is the second largest after the US Treasury market, but its representation in global benchmarks is still small. As its weighting grows, investors should benefit from the rising demand.

Beyond fixed income, investors can look to other alternatives for diversification. Macro strategies can adjust their correlation to equities and other asset classes and move dynamically according to changing market conditions. In periods of uncertainty – in which investors need portfolio protection – macro funds have historically outperformed equities (EXHIBIT 12).

The real market jitters would occur if a disorderly rise in inflation were to be realised. We view this as a tail risk, but given it would be unlikely to be good for either stocks or bonds, it’s one we should not be complacent about. Real estate and core infrastructure have low correlations to equity markets but their income streams are often tied to inflation, so can serve as a good inflation hedge. Of course, there are no free lunches, and such assets usually come with liquidity constraints, but those who can invest for the longer term may benefit from the inflation protection they can provide.

THEME 6 – CENTRAL PROJECTIONS AND RISKS FOR THE NEXT 6–12 MONTHS

Our core scenario is a continued recovery that broadens out and becomes more synchronised. Inflation worries provide some bumps, but monetary policy normalisation is slow. However, we remain in an unusual environment, and it’s as important as ever to keep an eye on the risks to our central view. On the positive side, inflation concerns could recede more quickly than we think as supply bottlenecks unstick, allowing central banks to remain accommodative for even longer. On the negative side, if those supply bottlenecks become more entrenched and vaccine progress falters, we could find ourselves dealing with stagflation.

Please check in again with us soon for further market updates and relevant content.