Please see the below article from JP Morgan received this morning:

The election of Joe Biden has fueled expectations of an increase in global momentum on tackling climate change. Climate action was one of Biden’s key campaign promises and, according to exit polls, the main reason that 74% of his voters voted for him. Having control of the Senate gives the Democrats more scope to deploy their (climate) programme, but they will still need to compromise given that they fall well short of the 60 seats required to easily pass major legislation. Business groups will also be active in lobbying Congress to oppose the pieces of legislation they find the least acceptable.

Biden’s climate proposals

In his Plan for a Clean Energy Revolution and Environmental Justice, President Biden set out his central ambitions on climate, including:

- “Rally the rest of the world to meet the threat of climate change”: The president has stated that rejoining the Paris Climate Agreement will be a day one priority. He also wants to fully integrate climate change into US foreign and trade policies in order to get every major country to further ramp up their domestic climate targets. From a global climate policy perspective, greater US support could be a game changer, as the US is the second-largest CO2 emitter in the world and the carbon intensity of its economy is three times higher than the global average. Quite how the president intends to work with the international community should become clearer following COP 26, the United Nations Climate Conference due to take place in Glasgow in November. At that point, we could see a new Grand Climate Accord. One possibility investors should look out for is that Biden makes climate policy central to ongoing trade tensions with China.

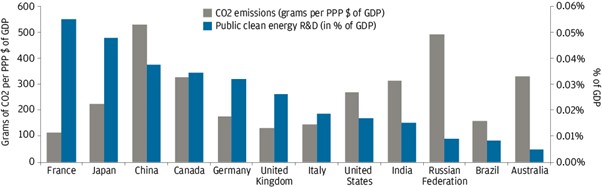

- “Ensure the US achieves a 100% clean energy economy and reaches net-zero emissions no later than 2050”: Biden’s pledge to achieve net-zero emissions by 2050 has already been made by more than 110 countries, accounting for more than 50% of global GDP and carbon dioxide emissions. To achieve the net-zero goal and ensure that the US becomes a 100% clean energy economy, Biden plans, among other policy measures, massive public investments (USD 400 billion) in energy- and climate-related research and development (R&D), an area where the US is lagging compared to Europe and China (see Exhibit 1).

- “Build a stronger, more resilient nation”: In addition to supporting R&D, Biden has promised significant investments in low-carbon infrastructure, committing to “a federal investment of USD 1.7 trillion over the next ten years, leveraging additional private sector and state and local investments to total to more than USD5 trillion”. This is probably the aspect of Biden’s climate plan that has generated the most enthusiasm in the US as there is a bipartisan consensus about the need to invest in infrastructure. The American Association of Civil Engineers estimates that to close its investment gap, the US “must increase investment from all levels of government and the private sector from 2.5% to 3.5% of US GDP by 2025”. Infrastructure spending will be part of a broader agenda of easy fiscal policy to promote the post-Covid 19 recovery.

As well as these key climate commitments, other parts of Biden’s programme could further support the sustainability agenda. For example, changes to the Employment Retirement Income Security Act could redirect pension capital flows to encourage private capital to be part of the climate solution.

Exhibit 1: Government investment in greening the economy and level of CO2 emissions

Source: IEA, OECD, World Bank, Mission Innovation, J.P. Morgan Asset Management. R&D budgets for Brazil, Russia, India and China are estimates. Note: R&D numbers from public sector data and may not reflect private sector or joint venture research initiatives. Data as of 2019 or latest available.

Implications of climate policy initiatives for the (global) economy

The economic impact of the transition to a low carbon economy generally depends on whether it is “sticks-based”, with private businesses bearing the bulk of the cost of the transition, or “carrots-based”, with governments supporting the transition through subsidies and other forms of fiscal stimulus.

The carrots-based approach, on which Biden focused in his campaign, is of course the most popular in the current economic environment as it could support the recovery while also addressing the longer-term threat of climate change. Even though he inherits the highest debt/GDP ratio since the second world war, Biden aims to maximise the fiscal impulse of his policies by leveraging public-private partnerships. Similar approaches, such as the European Fund for Strategic Investments, launched in 2015, have delivered strong results in terms of economic growth and energy transition while also generating opportunities for private investors.

However, to be most effective from a climate perspective, this approach should be combined with a sticks-based approach. The most common such approach is the implementation of a carbon tax, or more generally of a carbon price that can be set either through taxes or preferably through Emissions Trading Schemes (ETSs) to incentivise carbon producers to reduce their carbon intensity.

Although Biden has refrained from formally mentioning carbon pricing in his programme, his Treasury Secretary, Janet Yellen, has made clear in the past that she sees carbon pricing as a key element of any climate policy package. Yellen has also advocated so-called “carbon border tax adjustments”, which would ensure that ambitious carbon pricing does not undermine a level playing field globally. As already discussed, this may contribute to ongoing trade tensions with China.

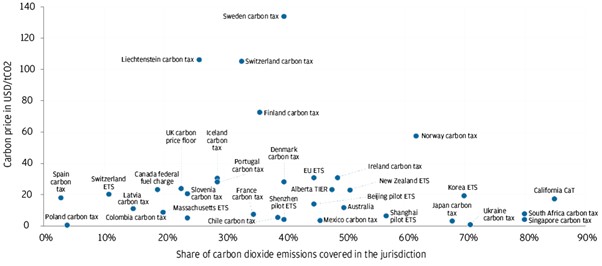

Conviction in the need for border tax adjustments is shared by many countries that have already launched their ETSs, but so far emissions coverage and price levels remain heterogeneous, and too low to reach our climate goals (Exhibit 2). The US could be tempted to leverage its experience with state-level ETSs, such as those in California and Massachusetts, to support the creation of a global level playing field for carbon prices.

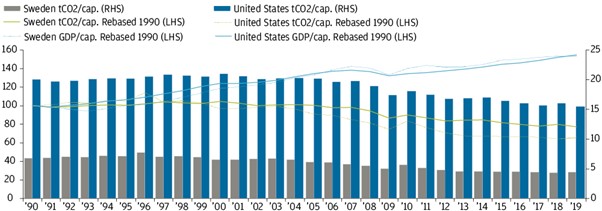

Contrary to the general belief, moving towards a fairer carbon price globally should not necessarily be negative for the global economy. The example of Sweden is striking in this respect. Although Sweden introduced the world’s highest carbon tax (Exhibit 2) in 1991 and joined the EU ETS in 2005, its GDP per capita grew by 53.5% between 1990 and 2019, or slightly less than the 54.6% posted by the US. In the meantime, Sweden’s carbon intensity has dropped from 6.8 tonnes of CO2 per capita (tCO2/cap) in 1990 to 4.45, a third of US carbon intensity (Exhibit 3).

Exhibit 2: Carbon pricing initiatives around the world

Carbon prices in USD (as of 1 November 2020) and % share of carbon dioxide emissions covered in the jurisdiction.

Source: World Bank Carbon Pricing Dashboard, National Bank of Belgium, J.P. Morgan Asset Management. Data as of 20 January 2021.

Exhibit 3: Economic and carbon performances of Sweden compared to the US, 1990-2019

Economic and carbon performances of Sweden compared to the USA 1990-2019

Source: National Bank of Belgium, Refinitiv Datastream, Emission Database for Global Atmospheric Research, Crippa, M., Guizzardi, D., Muntean, M., Schaaf, E., Solazzo, E., Monforti- Ferrario, F., Olivier, J.G.J., Vignati, E., Fossil CO2 emissions of all world countries – 2020 Report, EUR 30358 EN, Publications Office of the European Union, Luxembourg, 2020, ISBN 978-92-76-21515-8, doi:10.2760/143674, JRC121460. , J.P. Morgan Asset Management. GDP per capita based on purchasing power parity (PPP), 2011 international dollars. Data as of 20 January 2021.

Investment implications

Biden’s climate policy is likely to be part of a package of broader fiscal measures to support growth and speed up the energy transition of the country. It should also generate opportunities for investors in asset classes including real assets and global renewables, all of which have rallied over the last couple of weeks.

Internationally, the US is likely to re-embrace a more multilateral approach, after rejoining the Paris Climate agreement and committing to net zero carbon emissions by 2050. While US support for global carbon pricing initiatives remains uncertain, Biden’s administration may support carbon border tax adjustments, which could lead to a level playing field globally for carbon prices.

This is not necessarily negative from an economic perspective, as shown by the Swedish example, but carbon policy will need to be monitored by investors as carbon intensity is going to be an important non-financial parameter of economic and corporate performance.

Its good to see President Biden’s positive impact already showing through, from re-joining the Paris Climate Agreement to his recent repeal of Trump’s former transgender military ban. These are all elements which come under the heading of ESG.

Along with his more pro-active efforts to tackle the coronavirus, hopefully these positive moves will all help the markets move in the right direction.

Please keep checking back for more ESG related content along with a range of investment and market updates.

Andrew Lloyd

25/01/2021