Please see below for the latest market update from Invesco this morning:

The main focus of the week was the Jackson Hole Symposium and comments from Fed Chairman Jerome Powell on the way forward for US monetary policy (see chart of week). A “dovish”, risk asset supportive Fed remains the order of the day. Andrew Bailey, the governor of the Bank of England, also spoke at the Symposium, where he emphasised that the BoE had plenty firepower left to fight off recessions and stimulate growth. The other “highlight” of the week was the unexpected resignation of the long-standing Japanese Prime Minister, Abe, which potentially brings some shortterm uncertainty to Japanese politics, although the key reforms of the Abenomics-era are likely to be sustained by whoever emerges as his successor.

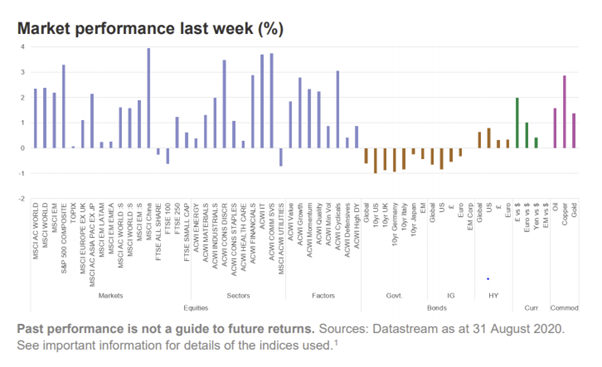

Global equities had a strong week, edging higher last week, with the MSCI ACWI hitting an all-time high on Friday. Gains were again led by the US, where the NASDAQ is now up over 30% YTD. EM also had a good week. Strength in IT-related stocks boosted Growth ahead of Value, despite strength in Financials, as bond yields moved higher. UK equities underperformed, down slightly on the week, with a stronger £ weighing on the foreign earnings-heavy FTSE 100.

Fixed income markets had a tougher week. Rising yields hurt government bond markets, which in turn negatively impacted the closely correlated IG market. Both were down slightly on the week. HY, however, managed a small gain, with global spreads and yields hitting post-crisis lows.

The dovish Fed pushed the US$ back close to its post-crisis lows, with gains strongest in £ and the Euro, with the former now having regained all its previous YTD losses and the latter at its highest since 2018. A weaker US$ provided a boost to commodities, with oil, copper and gold all making modest gains.

- One of the highlights of last week was the speech by the Federal Reserve Chairman, Jerome Powell, at Jackson Hole, which he used to officially announce historic changes to the Fed’s approach to setting monetary policy. A shift in policy that had been widely expected given the policy framework review that Powell had initiated nearly two years ago.

- The chart shows the 3-year monthly moving average of PCE headline inflation over the past two decades and the Fed’s target rate of 2%. It clearly shows that there has been a persistent shortfall of inflation relative to the 2% objective over the past decade. In light of this, the FOMC now “seeks to achieve inflation that averages 2% over time”. Powell emphasized that the new inflation strategy is “flexible”, with the Committee aiming to achieve this objective “over time” without defining a specific lookback period or horizon over which to achieve the average. Although the Fed has been deliberately vague as to the extent of overshoot that will be tolerated, the upshot is that the Fed is now aiming for above-target inflation.

- At the same time with the 50-year low in unemployment (3.5% in late 2019/early 2020) failing to push inflation higher, the Fed will also now focus on “shortfalls” rather than “deviations” in employment from its maximum level, and won’t raise interest rates in response to labour market strength in the absence of clear signs that inflation is actually rising.

- What does this mean for monetary policy? It effectively gives the Fed more leeway to run looser for longer policy. This means that the Fed Funds Rate is unlikely to be going up anytime soon. Goldman Sachs believe that it won’t be until 2025 that tightening starts. And with average inflation likely to weaken before it strengthens, there is an expectation that this will potentially open the door for further unconventional policy measures at the FOMC’s September meeting (16th).

- And the implication for financial assets? The higher inflation outlook on its own should benefit real assets (equities, gold and other commodities) over nominal fixed income (government and corporate bonds), although easier monetary policy for longer should also underpin bonds. Finally, a more “dovish” Fed will likely put some downward pressure on the US$.

Key economic data in the week ahead:

- A pick-up in news flow from the previous week.

- A lot of survey data will be published. Final PMI readings for August for major economies (US, Japan, EZ and UK) will come out on Tuesday (Manufacturing) and Thursday (Services and Composite). These are expected to confirm the results from the Flash surveys a couple of weeks earlier, with the highest readings in the UK and the US, while the EZ and Japan were the laggards, with the latter still below the 50 level.

- In the US, alongside the PMIs there are also the closely followed ISM Manufacturing (Tuesday) and Services (Thursday) surveys for August. The former is expected to see a marginally more positive reading of 54.5, but the latter is forecast to decline to a still robust 57.4. The first Friday of the month brings US Non-Farm Payrolls expected at 1.5m, slightly lower from the 1.7m in July. US unemployment is expected to show a reduction to 9.8% from 10.2% in July. The Underemployment rate, however, is forecast at 16.5% – slightly lower than last month’s 18% and perhaps a truer reflection of the current state of the US labour market. Ahead of this data, US Initial Jobless Claims on Thursday is expected to show an improvement to 950k last week from 1,006k the previous week.

- In the UK, July’s money and credit figures are published on Tuesday and are expected to show further signs that business and household borrowing rates are moving back towards normal. Mortgage Approvals, for example, are expected to rise to 55k from 40k, but that is still well below the 60-70k range seen prior to the crisis. Likewise, Consumer Credit growth is expected to be in positive territory for the first time since April (£0.8bn). Nationwide’s House Price Index comes out on Thursday, with August expected to see a 0.5%mom increase, which would make it 2%yoy. Pent-up demand and the Stamp Duty holiday are clearly helping here.

- Preliminary CPI for August in the EZ is released on Tuesday and expected to continue to show inflation at very weak levels, flat mom compared to July’s level of -0.4%mom. This would leave headline inflation at a mere 0.2%yoy and Core at 0.9%. Retail Sales for July are published on Thursday and, while remaining positive (1.4%mom), are expected to be somewhat weaker than in June (5.7%mom).

- In Japan the Jobless Rate for July on Tuesday is expected to increase to 3.0% from 2.8%, so somewhat above the lows of 2.2% seen in late 2019. The closely followed Jobs-toApplicants Ratio is expected to decline further and at 1.08x would be the weakest since early 2014.

- In China, business surveys dominate the week with both the Caixin and Official PMIs being released. Little change is expected in both sets of readings, with all remaining above the 50 level and Services continuing to be stronger than Manufacturing.

- Australia rarely gets a mention here, but on Wednesday Q2 GDP is published, which will confirm that the economy has slipped into its first recession for a remarkable 29 years.

Invesco are market leading investment managers and so their views and insight can be valuable in providing a well informed and holistic view of the markets.

Updates like these are useful tools in keeping your views of the markets widespread and up to date.

Stay safe and well.

Kind Regards

Paul Green

01/09/2020