Please see below for one of AJ Bell Youinvest’s latest Investment Insight articles, received by us yesterday 21/03/2021:

New consumer research* by Opinium for AJ Bell shows Cash ISA savers are holding high levels of cash, and aren’t switching accounts looking for better rates, partly because they think they’re getting more interest than they probably are.

We know that since the start of the pandemic, many savers have been all cashed up with nowhere to go. But our research shows that cash hoarding isn’t just a recent phenomenon, it’s been happening for some time, and reflects a natural aversion to taking risk with money that has been hard-earned.

It’s definitely prudent to build up a cash buffer to deal with any unexpected costs, particularly in uncertain times. But Cash ISA savers may well be doing themselves a disservice by holding too much money in cash, opening themselves up to inflation risk, and missing out on the potentially higher returns available from investments. As stock market investors need to avoid irrational exuberance, so cash savers should be wary of excessive prudence.

Over the last ten years, the average Cash ISA has turned £10,000 into £9,770 after factoring in inflation, while in contrast, an investment in the global stock market has turned £10,000 into £20,760 in real terms.** Looking at returns from 1899, Barclays found that over ten years, UK equities have beaten cash 91% of the time. Given that today cash interest rates are at record lows, it would have to be an extremely anomalous decade for the next ten years to buck that trend.

Cash ISA savers aren’t shopping around for the best rate a great deal either. Much of their apathy can be attributed to ultra-low interest rates, but part of it may simply be that they haven’t checked the rate they’re getting. Our survey found that on average Cash ISA holders hadn’t reviewed their rate for two and a half years, over which time the average Cash ISA interest rate has more than halved, from 0.9% to 0.4%.

Not all rates move in step though, and individual savers can suffer as a result of their provider slashing rates more aggressively than the rest of the market, hence why it continues to make sense to shop around. For instance, last November, savers in NS&I’s Direct ISA saw their interest rate cut from 0.9% to 0.1%, while the best rates on the market are around 0.5%.

Even the top rates on offer aren’t exactly going to set pulses racing, but switching can mean hundreds of pounds extra for those with large amounts held in Cash ISAs. At the very least Cash ISA savers should find out what rate they’re getting right now, to make an informed decision on whether it’s worth moving on.

All cashed up and nowhere to go

Our survey shows Cash ISA savers reported holding on average £27,727 in their accounts. That’s enough to pay for 11 months of household expenses, which come in at £2,538 on average according to the ONS.*** When you consider that many households will contain two Cash ISA holders, and may also own other cash products like savings accounts and Premium Bonds, that suggests that savers have enough built up to deal with any emergency spending, and then some. On top of that, 6 out of 10 (59%) or respondents said they intended to add more to their Cash ISA in this tax year or next, no doubt in part thanks to the pandemic savings turbo-charging cash balances, as spending options have dried up.

While this is encouraging from the point of view of short term financial security, it does mean savers are sitting on cash for the long run, missing out on potential returns from other assets, and seeing the buying power of their cash eroded by inflation. Clearly there is a balance to be struck here between having a robust safety net, and seeking higher returns by investing in the stock market, which can lead to a loss of capital in the short term. Typically, savers should seek to have 3 to 6 months of expenses in cash to deal with any emergencies, beyond that they should seek to tilt the balance between security and return more towards the latter.

Three to six months of expenses equates to £7,613 to £15,226 for the average household, which may well have two Cash ISA savers in it. This broadly ties in with the view expressed by the FCA in December, that those with more than £10,000 held solely in cash were missing out on the historically higher returns from investing their money, and opening themselves up to inflation risk.****

There are some reasons why you might want to hold more than six months of expenses in an ISA, namely if you are saving for a specific goal, for instance a house deposit. This probably explains a surprising kink in the data, which shows that younger savers actually have more held in Cash ISAs than older generations.

Broadly speaking, if you think you may need access to your money within five years, then cash might be the best option. If you’re putting money away for five to ten years, then you should start to think about putting at least some of it in the stock market. If you’re putting cash away for more than ten years, then an approach that invests more heavily in the stock market is likely to yield significantly better results.

Cash ISA inertia

Cash ISA savers aren’t paying a great deal of attention to the rate they’re getting, and who can blame them, seeing as picking cash products right now is about selecting the least worst option. Our survey found that on average Cash ISA holders hadn’t reviewed their rate for two and a half years, over which time the average Cash ISA interest rate has more than halved, from 0.9% to 0.4%, according to Bank of England data. Worryingly, almost a quarter of Cash ISA savers (23%) said they hadn’t reviewed their cash ISA rate for 5 years or more. This goes some way to explaining why 25% of Cash ISA savers reported getting over 1% interest, which looks unrealistically high in today’s market.

Despite holding a Cash ISA for an average of 8.5 years, 45% of Cash ISA savers said they have never switched provider. Half of these savers said it was because rates were so low, it didn’t seem worth it. That’s perfectly understandable, though for those with large sums in Cash ISAs offering poor rates, the difference can still be significant.

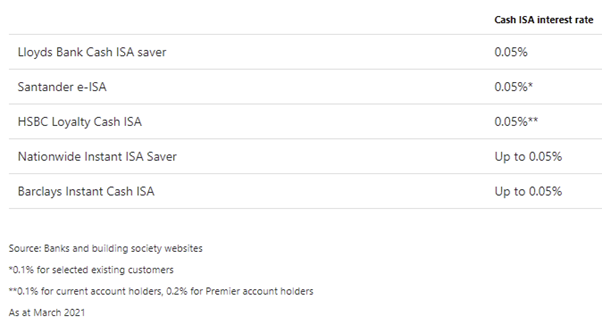

20% of Cash ISA savers said they held £50,000 or more in their Cash ISA. If they were picking up a high street rate of 0.1% (see table below) on £50,000, simply by moving to an account providing the average rate of 0.4% they could make an extra £150 a year. Not a king’s ransom, but worth having in your pocket rather than the bank’s. Particularly when you consider that at a rate of 0.1%, the total interest you are receiving is £50, and by moving to an account paying 0.4%, you would be quadrupling that amount to £200.

Selected high street instant access Cash ISA rates

Switching to a Stocks & Shares ISA

Half of Cash ISA savers surveyed (51%) said they had considered switching to a Stocks & Shares ISA. It used to be the case that you couldn’t cross the streams, but since 2014 you have been allowed transfer money from a Stocks and Shares ISA to a Cash ISA, and vice versa.

Doing so may be worthwhile if you feel you’ve got too much sitting in cash, earning next to nothing, and you’re willing to keep your money invested for the long term. You must be willing to tolerate falls in the value of your capital however, but the reward should be higher returns in the long run.

It’s important to always maintain a cash buffer for emergencies, three to six months of expenditure is the rough rule of thumb, but beyond this, you can start to think about investing in the market. Instead of transferring you might consider funnelling some of your new savings into a Stocks and Shares ISA, thereby gradually reducing your reliance on cash. Investing in the stock market bit by bit also helps to take the edge off the inevitable bumps in the road.

Please continue to utilise these blogs and expert insights to keep your own holistic view of the market up to date and for advice and planning tips.

Keep safe and well.

Paul Green DipFA

22/03/2021