Please see below for the latest market update from AJ Bell:

The pound losing its recent strength and oil stocks responding to a higher commodity price could boost the index

Investors in UK stocks have been looking jealously (or frustratingly) at the performance of the US markets and wondering why the FTSE 100 has stubbornly refused to rebound as fast.

Year to date, the S&P 500 is up nearly 5% and the Nasdaq is up 25% whereas the FTSE 100 is down nearly 19%, all on a total return basis.

The answer is simple – the UK stock market is very under-represented by tech stocks which is the sector that has driven US markets this year.

The UK is also heavily weighted towards banks and energy stocks, two of the worst performing sectors in 2020.

The former has been depressed by a drop in interest rates, rising concerns over potential bad debts as consumers and companies struggle as a result of the pandemic, and the suspension of dividends.

The energy sector has been hit by a big decline in the oil price and a reduction in dividends making it less appealing to income investors.

Yet are we about to see a reversal of fortunes?

Recent strength in the pound versus the US dollar will have worked against the multitude of companies on the FTSE 100 which earn in the latter currency, but whose share price is quoted in the former. Those dollar earnings will be worth less when translated into sterling.

Approximately three quarters of the FTSE 100’s earnings come from outside the UK, so foreign exchange rates really matter to the performance of the index.

Bank of America this month turned bullish on UK equities, partly because it expects the pound to weaken again on the back of rising no-deal Brexit risks. If sterling weakens then dollar revenues, once converted back into sterling, are worth more.

The bank also believes the energy sector should catch up with recent strength in the oil price, thereby giving another support to the FTSE 100 with oil producers Royal Dutch Shell (RDSB) and BP (BP.) being major constituents of the index.

Such predictions would suggest investors are right to remain hopeful for better returns from the FTSE. However, performance is still dependent on economic activity picking up around the world and unfortunately there are some mixed signals.

Stock markets last week took a tumble after the US central bank expressed concern that the pandemic could greatly impact the US economy in the medium term.

The latest Eurozone PMIs disappointed while the US and China’s recent figures have been more upbeat. These are various indices which show confidence levels from purchasing managers and which are a good economic bellwether.

Against this backdrop, the latest Bank of America survey of fund managers shows that institutional investors remain bullish about markets despite a difficult backdrop.

It’s an ever-moving feast and investors would be best served by not fiddling with their portfolios in response to every bit of economic data that comes out. Stay diversified and accept that there may well be some parts of your portfolio lagging others – it’s just the nature of investing.

A brief but concise summary like this is an efficient way of keeping your views of the markets up to date.

If you read the previous blog you can see Jupiter’s Fund Manager, UK All Cap, James Bowmaker’s views on the FTSE too.

Please see below for this week’s market update received from Blackfinch Asset Management earlier today:

In the ever-changing world that we live in, we recognise the importance of regular and current communication. This weekly news update from our MPS Portfolio Managers provides you with a short summary of events around the world which we hope you will find useful.

Issue 5 | 24th August, 2020

UK COMMENTARY

The IHS Markit UK Household Finance Index fell to 40.8 in August from 41.5 in July.

UK retail sales increased by 3.6% in July and are now 3% above the pre-pandemic levels seen in February. Online sales numbers fell by 7.0%, but remain 50.4% higher than in February.

The IHS Markit Composite Purchasing Managers’ Index (PMI) for August rose to 60.3 from 57.0 in July, the fastest rate of business activity expansion since October 2013.

UK retail footfall showed a weekly increase of 0.8%, following a 3.8% increase the week before. Market research group Springboard suggest the slowdown in growth could be attributable to the hot weather.

Market research group Kantar released data showing that the grocery market grew by 14.4% in the 12 weeks to the 9th August, with households averaging 14 shopping trips per month.

Inflation, measured by the Consumer Price Index (CPI), rose unexpectedly to 1.1% in July, driven by an increase in culture and recreation costs, analysts had predicted a reading of 0.7%.

A Reuters survey of economists suggests that the UK economy will take at least two years to recover from the impact of COVID-19.

US COMMENTARY

US/China trade talks are cancelled, President Trump signs an executive order forcing TikTok developer ByteDance to sell off its US operations within 90 days and announces further tightening of restrictions on Huawei.

The S&P 500 reached record levels, stopping just short of closing above the 3,400 level.

Apple becomes the first company to reach a market capitalisation of US$2trn.

News on the next tranche of stimulus from the US government fails to materialise for another week.

Minutes from the Federal Reserve offer little encouragement, stating that the pandemic could have a ‘considerable’ impact on the US economic outlook for the medium term. The Federal Reserve also offer no further guidance on interest rates, reiterating that they will remain low for ‘a very long time’.

First-time unemployment claims rise by 135,000, counteracting the previous week’s fall.

ASIA COMMENTARY

The Chinese Central Bank added 700bn Yuan (c.£76bn) to their medium-term lending facility for commercial lenders in order to help liquidity, helping to boost sentiment.

Japanese Gross Domestic Product (GDP) shrinks at 7.8% on a seasonally-adjusted quarterly basis, the third consecutive quarter of negative growth.

These articles are useful for breaking down market input into sectors. This facilitates an all-round view of the markets from the experts in a quick and efficient format.

Please use these blogs to keep your own view of the markets up to date from a variety of different sources.

Please see below for Brewin Dolphin’s latest Markets in a Minute article received yesterday 18/08/2020:

Global equity markets pushed higher for most of last week on positive economic data, before an ugly session on Friday erased most of the gains. Markets dropped in the UK and Europe as France was added to the quarantine list, which hit travel stocks hard. Prior to that, the Nasdaq hit a new record high, as did the gold price, while the S&P500 briefly surpassed the record high it set back in February before closing slightly lower.

Last week’s markets performance*

• FTSE100: +0.95%

• S&P500: +0.64%

• Dow: +1.8%

• Nasdaq: +0.07%

• Dax: +1.8%

• Hang Seng: +3.84%

• Shanghai Composite: +0.2%

• Nikkei: +4.3% *

Data for the week to close of business on 14 August 2020

Mixed start to week on US/China tensions and virus concerns

Markets were mixed yesterday after digesting news that the US and China cancelled their weekend talks to assess how Phase 1 of the trade deal was progressing. It was blamed on “scheduling conflicts” but given the recent escalation in tensions, including banning WeChat and Huawei, perhaps a postponement is no bad thing. London equities rose, with the FTSE100 up by 0.6%. In the US they were mixed – the Dow closed down 0.3% at 27,844.91, while the S&P500 rose 0.27% to 3,381.99. The Nasdaq closed 1% higher at 11,129.73. Europe was also mixed, with the pan-European Eurostoxx up by 0.3%, alongside gains in Germany and France, but equities in Italy and Spain lost ground.

There are concerns that economies are reaching their maximum capacity for growth without further easing of restrictions, which could increase the chances of a second wave of coronavirus infections. However, surging cases in some European countries are leading to more containment measures, not less.

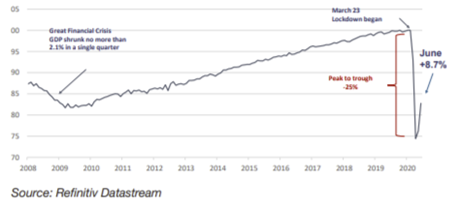

Level of UK GDP (February 2020=100)

UK recession

The standout headline last week was the UK’s record decline into recession in the second quarter. The -20.4% quarterly fall in GDP does look ugly. It is the largest quarterly decline on record, and it was the biggest quarterly fall amongst major economies. As a services-sector driven economy, the UK has been hit harder than other countries – there was a -23.1% drop in consumer spending, while business investment fell by -31.4% in the second quarter.

More encouragingly, GDP rose by 8.7% month-onmonth in June after 2.4% rise in May thanks to the easing in lockdown restrictions and there is good reason to think this will continue in the short term. For instance, wholesale and retail output rose by +27.0% in June compared with May. And with the reopening of pubs and restaurants in July and the “eat out to help out” scheme in August, we believe the unprecedented fall in GDP in quarter two will be followed by a recordbreaking double-digit growth in quarter three.

In addition, more current high-frequency data such as restaurant bookings, retail footfall and travel show normalisation in activity. However, the risk is that unemployment rises sharply once the furlough scheme ends in October. The ONS said last week that 730,000 fewer people were employed in July compared to March, based on data from HMRC, but with an estimated 5 million people still on furlough.

If such headwinds emerge later in the year, we think the Bank of England will expand its asset purchase program and further stimulus maybe announced by the Chancellor.

Japan follows UK into recession

Japan announced on Monday that its economy had contracted by 7.8% in the second quarter, which is less severe than the slowdowns in the UK, US and much of Europe. This is most likely because it had a less stringent lockdown. Still, the annualised rate of contraction of 27.8% for the three months to June is worse than Japan’s decline at the height of the financial crisis.

US retail sales and inflation

US retail sales rose 1.2% in July compared to June, below expectations for a 1.9% increase. While the sharper than expected slowdown was a disappointment, the good news is that US nominal retail sales have already surpassed their pre-Covid level, so a flattening off is to be expected. Also, there is uncertainty surrounding the unemployment benefits which account for a large part of the income for millions of unemployed Americans, and there is little sign of progress between Republicans and Democrats at the moment. This will be weighing on consumer confidence.

Meanwhile, the US consumer price index jumped 0.6% in July compared to June, which is the biggest monthly increase since June 2009 (vs +0.3% expected), while the core annualised rate rose to 1.6%. These numbers are clearly still very benign compared to the Fed’s inflation target of 2%, but the risk is that inflation could be a problem further down the road.

Chinese data hints at slowing recovery

Overall the China July activity data continued to show improvement but at a slower pace, not surprising given the lingering Covid threat. The talking point was the disappointment in retail sales given China is increasingly a consumption-based economy, retail sales were still down -1.1% on an annualised basis, perhaps due to a spike in cases and people being cautious about going out. However, the Chinese savings rate is over 40%, so consumers would appear to have plenty of spending power for when confidence returns.

We can use these blogs to keep an up to date consensus view of the global markets. Recent recession news may have come as a shock to many, but the background to situations like these can be more easily understood by reading widely on investment issues.

Please see below for the latest update from AJ Bell Regarding the housing market:

Both the property site and the wider space are likely to be tested in the autumn

Thursday 13 Aug 2020 Author: Tom Sieber

The resilience of the UK housing market has been one of the notable features as we moved out of lockdown and into the next phase of the pandemic.

This was reflected in recent first half results from property site Rightmove (RMV) which saw the company reveal that between the beginning of June and end of July demand for sales properties was 50% higher than the same period in 2019.

In lockdown there were predictions that estate agents would act on grumbles over Rightmove’s increasing level of fees and use a period when the market was effectively in hibernation to leave the platform.

However, membership numbers for agency branches and new home developments combined were down just 3.3% since the start of 2020 to 19,158.

It seems rather than driving agents away, a period of housing market volatility may have reinforced the network effect which has helped underpin the company’s impressive growth over the last decade or more.

Because the site has the most listings, it is therefore the one which prospective property buyers will go to when looking for their next home. This reinforces its position as a must-have product for estate agencies and gives it significant pricing power when it comes to securing subscriptions from agencies.

Agents are arguably more reliant than ever on Rightmove’s services and reach as they have to sell properties to stay afloat.

However, it will be interesting to see if this holds true if or when Rightmove looks to return to a pre-Covid pricing structure having offered discounts through the crisis.

Currently discounting has been extended until the end of September – although that month will see a reduction of just 40% compared with 75% when lockdown was at its height.

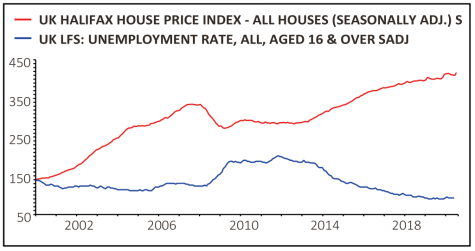

The foundations of the housing market may also come under pressure this autumn, assuming the furlough scheme comes to an end as planned in October.

This could lead to a material increase in levels of unemployment, which is likely to have a negative impact on demand for homes.

A look at house prices and unemployment over the last 20 years unsurprisingly indicates a significant negative correlation with house prices falling as unemployment rises and vice versa.

Please use these blogs to regularly update your view of the financial markets and remember to take a holistic view of your finances. Although liquid assets tend to take the headlines initially during market drops and grab the public’s attention, other assets, such as property, should not be left in the background of thought, as this article demonstrates.

Please see below for Invesco’s latest Investment Intelligence Update:

News flow last week, such as Non-Farm Payrolls and the ISM surveys in the US, was generally supportive of a positive tone in financial markets. “V” looks the shape of the recovery, for now at least. The virus news, however, remains mixed. New confirmed cases continue to roll over in the US, albeit still at elevated levels, while in Europe and DM Asia case growth remains relatively low, although it has risen in recent weeks. Case growth continues at elevated levels in Latin America. Central Bank dovishness remains very much the order of the day, with the Bank of England last week reiterating the uncertain outlook and the preparedness to do more if needed. Geo-political strains between the US and China refuse to go away, and in fact look as if they are escalating, while progress towards further US fiscal stimulus continues to frustrate.

Global equities hit their highest level since the bear market low during the week and are now back into positive territory for the year, now just 3% from their all-time high. Small caps and value/cyclical sectors led the way. In the UK further £ strength weighed on FTSE 100 relative performance, which dragged the All Share lower.

There was mixed performance in fixed income, with government bonds weaker at the margin, with the odd exception (Italy, EM). IG and HY continue to make progress. A new record low for yields for the former, while further declines in yields for the latter returned the asset class to positive territory for the year. Spreads for both still remain well above the lows seen earlier in the year.

The US$ halted its decline (see Chart of the week). Economic optimism helped boost economically sensitive commodity prices. China, the world’s biggest consumer of copper, saw record imports for the second straight month. Gold pushed to new highs as real yields declined to record lows and investor demand remained elevated.

Market performance last week (%)

Past performance is not a guide to future returns. Sources: Datastream as at 9 August 2020. See important information for details of the indices used.1

YTD market performance and YTD low (%)

Past performance is not a guide to future returns. Sources: Datastream as at 9 August 2020. See important information for details of the indices used.1

Chart of the week: US$ Index

Source: Datastream as at 8 August 2020.

One of the features of financial markets since the peak of the pandemic crisis dislocation in late March has been the weakness in the US$. In this chart we use the US$ Index (DXY) as a proxy for the currency’s performance (Fixed currency weights for DXY are Euro 57.6%, Yen 13.6%, £ 11.9%, Canadian $ 9.1%, Swedish Krona (SEK) 4.2% and Swiss Franc 3.6%).

At its YTD peak (late March) it had risen just under 7% on the back of its safe-haven, reserve currency characteristics and a shortage of US$ liquidity. Since then it has given up all those gains and more, declining 9.1% and now down just over 3% YTD. It is now at levels last seen in May 2018 and its 100-day decline has been the worst since November 2010. The major contributor to this weakness has been strength in the Euro (10.3%), given its high index weight, but other currencies have been stronger (SEK +18.7%, £ +11.1%). The Yen has been the weakest on a relative basis, but has still risen 4.6%.

Why has the US$ been so weak? A number of factors have contributed: the global rebound in growth has favoured more cyclical currencies, such as the Euro; an unwinding of safe-haven flows into the US$ on the back of this; real and nominal interest rate differentials between the US and another major markets have collapsed; aggressive Federal Reserve policy has alleviated US$ funding issues; fiscal and structural optimism in Europe on the back of agreement on the European Recovery Fund; the Federal Reserve and US government is happy to see a weaker currency; and finally, idiosyncratic US political and fiscal risk. All have weighed on a currency that on most measures was overvalued and where investor positioning was extended.

Can the US$ weaken further? Fundamentals are currently stacked up against the currency for now, but this is in the context where the DXY has moved from its most overbought level ever (relative to its 12m average) to its most oversold level since 1978. At the same time investor positioning (based on CFTC data) is now at a record short.

What does US$ weakness mean for financial markets? Historically it has benefitted global equites (and non-US stocks in particular), cyclical sectors, EM assets in general and commodity prices, such as Gold and Copper.

Key economic data in the week ahead:

A relatively quiet week ahead on the data front.

In the US there is July’s CPI reading on Wednesday. Headline inflation is expected to rise slightly to 0.7%yoy, off the pandemic lows, but still at the lowest level since 2015. Core inflation is expected to see a marginal decline to 1.1%yoy, its lowest level since 2011. The pandemic has been disinflationary. Initial jobless claims out on Thursday are forecast to show another 1.4m people receiving unemployment benefits, despite the better than expected Non-Farm Payroll data last Friday. Data on the strength of the US consumer is also out, with US retail sales for July published Friday and forecast to show a slowing recovery (1.9%mom vs 7.5%mom in June), while the preliminary reading of the University of Michigan Sentiment Index is expected to fall further and continue to hover around pandemic lows.

In the UK the most anticipated datapoint next week is the Q2 GDP release on Wednesday. If the forecasts of -20.5% prove right it would be the worst quarterly contraction of the UK economy on record. Broad-based weakness is expected, with the increase in government spending the only positive, depending on your point of view. Monthly GDP for June will also be released at the same time, which should show an underlying improving trend in the economy not seen in the quarterly numbers, with 8%mom forecast compared to May’s 1.8%mom. The latest UK unemployment report is published on Tuesday. The unemployment rate is expected to rise only slightly to 4.2% from 3.9% as the labour market continues to be underpinned by the government’s job retention scheme. The true health of the labour market will be seen away from the headline data in areas such as the number who are now economically inactive, hours worked and vacancy levels. These all point to higher levels of unemployment by year end, with the Bank of England’s Monetary Policy Report last week seeing it at 7.5%. Finally, there is July’s RICS house price data on Friday, which is expected to show a -5% drop in July, but up from -15% last month, highlighting the gradual improvement in the housing market in England and Wales.

China’s July data pipeline started last week and will continue throughout this week with figures on CPI (Monday) industrial production, fixed investment, retail sales, house price inflation and unemployment (all on Friday). Most indicators are forecast to post better readings than they did in June, suggesting that the third quarter is off to a relatively firm start.

Nothing of note during the week from either the EZ or Japan.

An insightful look into the markets by the experts at Invesco. These weekly updates are useful in terms of providing a regular overall view of the market.

Please use Invesco’s Investment Intelligence updates as well as our other blogs to refresh your view of current goings on in the global markets.

Please see below for the latest blog from UK Finance regarding scams:

UK Finance unveils ten Covid-19 and lockdown scams to be aware of

UK finance unveils ten Covid-19 and lockdown scams the public should be on high alert for and how to spot them

Criminals are preying on a worried public by tapping into their financial concerns due to coronavirus, asking for personal and financial information

New animation video from Take Five to Stop Fraud campaign warns people to remember criminals are sophisticated at impersonating other organisations

Using the coronavirus pandemic as an opportunity, fraudsters are using sophisticated methods to callously exploit people, with many concerned about their financial situation and the state of the economy. To coincide with the launch of its new animation urging people to follow the advice of the Take Five to Stop Fraud campaign, UK Finance today reveals ten Covid-19 and lockdown scams which criminals are using to target people to get them to part with their money.

Some scams manipulate innocent victims, urging people to invest and “take advantage of the financial downturn”. Others impersonate well-known subscription services to get people to part with their cash and personal information. Criminals are even posing as representatives from the NHS Test and Trace service in an effort to trick people into giving away their personal details.

To remind people that criminals are experts at impersonating trusted organisations, UK Finance has launched a new animation video urging people to follow the advice of the Take Five to Stop Fraud campaign. Consumers are reminded to always take a moment to stop and think before parting with their money or information in case it’s a scam.

The ten scams to be on the lookout for and how to spot them:

Covid-19 financial support scams

Criminals have sent fake government emails designed to look like they are from government departments offering grants of up to £7,500. The emails contain links which steal personal and financial information from victims

Fraudsters have also been sending scam emails which offer access to ‘Covid-19 relief funds’ encouraging victims to fill in a form with their personal information.

Criminals have been targeting people with official-looking emails offering a ‘council tax reduction’. These emails, which use government branding, contain links which lead to a fake government website which is used to access personal and financial information.

Fraudsters are also preying on benefit recipients, offering to help apply for Universal Credit, while taking some of the payment as an advance for their “services”.

Health scams

One of the most shocking scams that has appeared during the pandemic has involved using the NHSTest and Trace service. Criminals are preying on an anxious public by sending phishing emails and links claiming that the recipient has been in contact with someone diagnosed with Covid-19. These lead to fake websites that are used to steal personal and financial information or infect devices with malware.

Victims are also being targeted by fake adverts for Covid-related products such as hand sanitizer and face masks which do not exist.

Lockdown scams

Criminals are sending fake emails and texts claiming to be from TV Licensing, telling people they are eligible for six months of free TV license because of the coronavirus pandemic. Victims are told there has been a problem with their direct debit and are asked to click on a link that takes them to a fake website used to steal personal and financial information.

Amid a rise in the use of online TV subscription services during the lockdown, customers have been targeted by criminals sending convincing emails asking them to update their payment details by clicking on a link which is then used to steal credit card information.

Fraudsters are also exploiting those using online dating websites by creating fake profiles on social media sites used to manipulate victims into handing over their money. Often criminals will use the identities of real people to strike up relationships with their targets.

Criminals are using social media websites to advertise fake investment opportunities, encouraging victims to “take advantage of the financial downturn”. Bitcoin platforms are using emails and adverts on social media platforms to encourage unsuspecting victims to put money into fake investment companies using fake websites.

The banking and finance sector is working with the government and law enforcement to help identify scams and prevent people becoming victims of fraud. The industry is also encouraging everyone to remain vigilant and to follow the advice of the Take Five to Stop Fraud campaign, and to Stop, Challenge and Protect when they receive any messages out of the blue:

Stop: Taking a moment to stop and think before parting with your money or information could keep you safe.

Challenge: Could it be fake? It’s ok to reject, refuse or ignore any requests. Only criminals will try to rush or panic you.

Protect: Contact your bank immediately if you think you’ve fallen for a scam and report it to Action Fraud.

In order to spot a Covid-19 scam, people should be on high alert if:

The website address is inconsistent with that of the legitimate organisation

The phone call, text or emails asks for financial information such as PIN, passwords

You receive a call or email out of the blue with an urgent request for your personal or financial information, or to make an immediate payment

You’re offered a heavily discounted or considerably cheaper product compared to the original price

There are spelling and grammar mistakes, or inconsistencies in the story you’re given

Managing Director of Economic Crime at UK Finance, Katy Worobec, said:

“During this pandemic we have seen criminals using sophisticated methods to callously exploit people’s financial concerns, impersonating trusted organisations like the NHS or HMRC, to trick them into giving away their money or information.

“The banking and finance industry is tackling fraud on every front, investing millions in advance technology to protect customers and working closely with the government and law enforcement to stop the criminal gangs responsible and neutralise the threat.

“We would always urge people to follow the advice of the Take Five to Stop Fraud campaign to keep their money and personal information safe from fraudsters.”

As the world rapidly changes, we have criminals adapting just as quickly to pounce on vulnerable situations. We post blogs like this to keep you up to date and aware of the latest scams you should be aware of, some of which even surprised us with their inhumanity.

We are all in this together, the way to battle this new wave of crime is to be vigilant and don’t be afraid to question anything that doesn’t seem normal, even by the most minor detail. Please remember if you receive these communications:

If it seems to good to be true, it probably is

If you were not expecting it, treat it with suspicion

Do NOT give away any personal details if communications make you think either of the points above

Anyone can be vulnerable to these scams. These criminals are career experts in what they do and can catch anybody off guard with devastating consequences, do not be afraid or embarrassed to discuss these matters or ask for help/advice.

Please see below for Blackfinch Asset Management’s latest market commentary:

In the ever-changing world that we live in, we recognise the importance of regular and current communication. This weekly news update provides you with a short summary of events around the world which we hope you will find useful.

Issue 2 | 3rd August, 2020

UK COMMENTARY

Following the introduction of a two-week quarantine for travellers returning from Spain, Boris Johnson announces that further quarantines are being considered with Belgium, Luxembourg and Croatia the next likely candidates.

The UK finance ministry extends help to small businesses, announcing that Companies with fewer than 50 employees and a turnover of less than £9mln can now benefit from loans of up to £5mln under the Coronavirus Business Interruption Loan Scheme.

Data from Nationwide shows that house prices in the UK rose 1.7% in July.

Boris Johnson confirms that the UK needs to slow the reopening of the economy, delaying the reopening of some leisure businesses, as well as imposing restrictions in some areas of the country to counter a rise in infections.

US COMMENTARY

Florida and California continue to be the hubs for COVID-19 cases in the US, with both approaching 500,000 total cases, with only 5 countries globally having a higher case number.

Republicans and Democrats attempt to come to an agreement over a $1 trillion stimulus plan to help bolster the economy. A variety of steps are being proposed including $1,200 payments to most Americans and further funding for schools, businesses and increased testing.

The Federal Reserve leaves interest rates unchanged, as expected. A post-meeting statement confirms that “Following sharp declines, economic activity and employment have picked up somewhat in recent months but remain well below their levels at the beginning of the year.”

Data shows that the US economy contracted at its fastest pace ever in the second quarter of the year, falling 32.9%.

Donald Trump takes to Twitter to propose a delay to the November Presidential election, claiming that postal voting will make the election ‘inaccurate and fraudulent’.

EUROPE COMMENTARY

The European Central Bank (ECB) has told banks in the Eurozone to cancel dividends until 2021 and to exercise ‘extreme moderation’ with bonuses.

The German economy contracts by 10.1% in the second quarter of the year.

Data for the Eurozone as a whole shows economic contraction of 12.1% in the quarter.

COVID-19 COMMENTARY

Moderna Therapeutics began the final phase of clinical trials for its COVID-19 vaccine. The US trial, in collaboration with the National Institue of Alergy and Infectious Diseases is reported to involve up to 30,000 people.

The UK decides not to join an EU scheme to purchase COVID-19 vaccines, instead forming its own deals.

Following news that the UK had secured 90mln doses of the COVID-19 vaccine being developed by Pfizer and BioNTech, a deal worth £500mln was signed to purchase a further 60mln doses from Sanofi. In addition it is expected that Astrazeneca, in conjunction with the University of Oxford, may make 30mln doses available as early as September.

These articles are useful for breaking down market input into sectors. This facilitates an all-round view of the markets from the experts.

Please keep reading these blogs to keep your own view of the markets up to date.

Please see article below from Brewin Dolphin’s ‘Markets in a Minute’ update received 15/07/2020.

China shares rally as state media declares bull market

Global share markets were mixed over the past week, although China has been a standout performer after investors piled in, encouraged by a state-owned newspaper that effectively declared a “healthy” bull market was on the way in Chinese equities.

Investors took the message to heart, and Chinese shares surged by almost 6% at the start of last week on trade volumes roughly double the average.

In the UK, a rally late in the week lifted the FTSE100 comfortably above the 6,000 level but performance in most markets was fairly muted due to the ongoing downbeat news around the coronavirus, worries about tensions between the US and China, and uncertainty around stimulus packages.

Last week’s markets performance*

FTSE100: -1%

Dow Jones: 0.95%**

S&P500: 1.75%**

Dax: 0.84%

Nikkei: -0.07%

Hang Seng: 1.4%

Shanghai Composite: 7.3%

*Performance in the week to Friday 10 July **Performance from close of business on 2 July to Friday 10 July due to Independence Day holiday.

A mixed start to this week…

Share markets largely continued their bullish run on Monday, with the FTSE100 gaining 1.33% and European markets hitting their best levels in almost a month as reports suggested progress on two vaccine candidates in the US. China and other Asian markets continued their strong run.

However, the S&P500 and the Nasdaq in the US both closed down yesterday amid worries about the rolling back of reopening plans in some states due to rising coronavirus cases. That led to Asian markets falling sharply today.

Chinese policymakers have also become uneasy about the rapid rise in Chinese stocks, leading to two state-backed funds to begin offloading equities in a bid to cool the overheating market. The Chinese government has also sought to dissuade investors from accessing unauthorised sources of margin financing. The Shanghai Composite closed down by 0.8% today. In early trading in the UK and Europe, shares were heading down.

Stimulus cliff-edge in US, knife-edge summit in Europe

There can be no doubt that both the US and Europe need more stimulus to maintain their recovery, or at least prevent a sharp deterioration. In the US, a central plank of March’s $2trn stimulus package is being debated; the extra $600-a-week in unemployment benefits, which is paid on top of each state’s existing unemployment benefits, is due to end on July 31. This means a potential cliff-edge income drop for around 20m unemployed Americans that would cause average unemployment payments to fall by about 60%. Also, cash payments to households have already been received, and probably spent.

Fortunately, both the Democrats and Republicans want the extra stimulus to keep flowing, so it is more than likely we will see these benefits extended.

This coming Friday the EU will debate the €750bn coronavirus recovery package at a special summit, and it is far from certain the fund, dubbed Next Generation EU, will pass in its current size or format – the current proposal is that the fund is made up of grants and loans, and more fiscally conservative states, particularly the Netherlands, are objecting to the grants element and also, reportedly, the size of the package.

Virus news

While the headline figures from case growth around the world, and particularly the US, still make dire reading, a glimmer of hope can be seen in the decline in Swedish cases, although this could be for any number of reasons (less testing, some more lockdown measures). Crucially, however, there was an important suggestion that immunity may have spread more widely than believed, which has global implications.

Marcus Buggert of The Centre for Infectious Medicine at Karolinska Institutet, Sweden, said: “Our results indicate that roughly twice as many people have developed T-cell immunity compared with those who we can detect antibodies in.”

Apparently, this could mean herd immunity is achievable with far lower infection rates of, say, 20% rather than the 60% suggested more commonly.

Overall the trends in Covid cases may be improving but it is hard to say due to fluctuations in testing and the distortion of the Independence Day holiday in the US. Even outside Sweden, European cases seem to have been suppressed for now. The case growth rate in Brazil could be peaking but there is little sign of any improvement in Mexico, South Africa or India.

In Asia, after a week in which Tokyo recorded 100 new cases per day, they subsequently jumped more than 200 on Thursday. Hong Kong will close its schools early for the summer holidays after finding 34 new locally transmitted cases on Thursday.

On the vaccine front, research into T-cell immunity is now being incorporated into vaccine development, in addition to the focus on antibodies we have seen so far. If successful, this could significantly boost any vaccination’s efficacy and the duration of immunity, though it is still very early days.

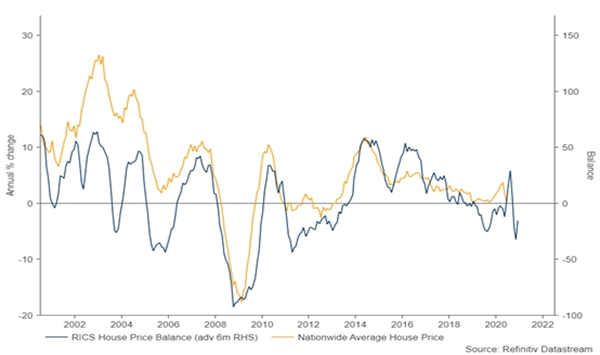

Summer statement boosts housing sector

In his summer statement last week, Chancellor Rishi Sunak refused to extend the government’s furlough scheme past October as widely expected, but he announced a stamp duty holiday until next March for properties worth up to £500,000. That boosted shares in housebuilders, and it may prompt an uptick in housing transactions. New buyer enquiries at estate agents were close to record levels in June, according to last week’s survey from the Royal Institution of Chartered Surveyors. Its survey, which questions surveyors around the country, suggested a slight recovery in prices and a big increase in properties being listed for sale. But looking ahead, views were a little more negative, implying price declines of 5% over the remainder of the year.

New buyer enquiries vs Nationwide average house price

RICS House price balance vs Nationwide average house price

Make the most of higher-rate tax relief in your pension while you can

Sunak hinted that efforts to address the dire situation that is the national finances will begin in November’s Budget. This may finally sound the death knell for one of the most attractive tax breaks in the UK, namely higher-rate tax relief on pension contributions.

It’s hard to see any more obvious revenue-raising step that would be so effective, and it has been speculated about for a decade. It would suggest anybody who hasn’t taken advantage of this year’s allowance should seriously consider doing so before the autumn.

One of the main focuses of this update are the views on potential monetary and fiscal policy actions from governments, particularly the UK, EU, China and US. It now seems that market analysts have turned their attention to how governments will act to deal with the financial consequences of this pandemic in the long term and how that will affect the markets as they begin to recover.

Hector Kilpatrick, Senior Investment Director and Head of Risk Managed Funds at Cornelian Asset Management, summarises the previous month and gives the Investment Outlook for July:

The MSCI UK All Cap NR index returned +9.4% during the three months to the end of June, whilst the MSCI World ex UK (£) NR index returned +20.4% in Sterling terms. Equity markets recovered a significant amount of the ground lost during the precipitous decline in asset prices observed during the first quarter of the year. The collapse was triggered by a sudden realisation that the economic impacts of the policies enacted to restrain the COVID-19 virus outbreak would result in a deep recession, the scale of which could challenge the debt-based capitalist economic system. However, policy makers were swift to announce enormous economic support packages, both fiscal and monetary. These, alongside the easing of lockdown restrictions in many jurisdictions and positive incremental news concerning the extraordinary effort being applied to develop possible vaccines, helped improve investor confidence during the period under review.

In Sterling terms, most major regional equity markets returned between +17% and +22%, the exceptions being the UK (see above) and Japanese markets (MSCI Japan NR (£) Index, +12.0%). The American equity market provided the strongest return (MSCI USA NR (£) Index, +22.0%), aided by the index’s significant exposure to technology and pharmaceutical stocks.

The UK equity market return was impacted by the index’s significant exposure to energy and financial stocks (which, in share price terms, have lagged the recovery seen in other sectors), the persistence of COVID-19 within the population and concerns regarding the outcome of Brexit negotiations.

“Gilts continued to perform well producing a positive return as investors anticipated further policy announcements which would support government bond prices.”

Despite the more positive investment environment, Gilts continued to perform well producing a positive return (iShares Core UK Gilts ETF, +2.4%) as investors anticipated further policy announcements which would support government bond prices. Investment grade debt rebounded strongly as credit spreads narrowed following the announcement that the Federal Reserve would support corporate debt markets (iShares Core £ Corporate Bond ETF, +9.6%). ‘Riskier’ high yield debt also produced a strong positive return but interestingly, given the seemingly more ‘risk on’ environment, marginally underperformed investment grade debt (iShares Global High Yield GBP Hedged ETF, +9.4%).

The Brent crude oil price ended the quarter at $41.2/barrel, an increase of 80.1% since the end of March. The hard stop to global economic activity has seen a collapse in demand for oil products, however production cuts and an incremental relaxation of economic lockdowns has helped the oil price recover somewhat.

In the three months to the end of June, the gold price rose 12.9% to $1781/oz. Sterling weakness versus the US Dollar boosted returns marginally such that the value of gold held by UK based investors rose by 13.5% (to £1,443/oz).

Investment Outlook

During the second quarter of the year asset prices rallied strongly following the sharp COVID-19 related declines witnessed during the first quarter. Policy makers have been impressively swift to announce innovative measures to support economies which have experienced a hard stop. Measures range from the fiscal (furlough schemes, top ups to unemployment benefits, emergency lending/grants to corporates, business rate reductions and the like) to the monetary (interest rate cuts, printing of money to finance the purchase of government debt and, to a lesser extent, corporate debt).

These measures (which have driven down the cost of government and corporate debt financing) allied with tangible successes in suppressing the spread of the virus in developed economies have, in aggregate, improved the confidence of company management teams concerning the outlook for economic growth. They have also galvanised investors’ risk-taking appetite and have led to a strong bounce in regional equity market indices. News concerning the unprecedented drive to find successful treatments and vaccines has also helped improve sentiment.

However, looking a little more deeply into the components of the market rally calls into question the improving confidence expressed by rising asset prices in general. Those companies most exposed to the economic cycle have lagged index returns appreciably. Some sectors (such as banks, energy and travel) remain close to their lows relative to index returns. The companies that have driven index levels higher include those which have seen a sharp acceleration in demand due to their web-based propositions and those which have little sensitivity to the economic cycle.

The question that needs to be answered therefore, is whether the sugar rush of extraordinary policy measures, both fiscal and monetary, will give way to a more sober assessment of the outlook for economies, and thereby profits. We believe this is likely, albeit with caveats.

“The real scale of ‘post COVID-19’ unemployment has yet to reveal itself.”

The first thing to note that the real scale of ‘post COVID-19’ unemployment has yet to reveal itself. With companies embracing higher debt levels to remain in business in the short term, the hangover could be material, particularly as the unfettered release from lockdown will only be assured after a successful vaccine is found and manufactured at scale. Unfortunately, it doesn’t appear that this condition will be satisfied in 2020. In a realistic best-case scenario, we may receive increasingly positive news concerning the development of a vaccine through the rest of the year, however populations will still have to suppress the spread of the infection until vaccines can be deployed in early 2021.

Barring the possibilities that the virus may lose some of its potency, or that specific populations are able to eliminate the virus completely from their midst, one has to assume that the rate of virus spread will correlate with the pace that economies open up (notwithstanding any seasonal effects). If correct, this means that the ‘V’ shaped recovery that is hoped for may well disappoint as rolling localised lockdowns are introduced which will ensure heightened public awareness of the need to continue to socially distance, etc. This may well sustain higher levels of unemployment, and therefore result in consumers hoarding cash after the first flush of spending driven by pent up demand.

“Companies are likely to continue to operate in an environment of reduced demand and increased costs for the rest of 2020.”

This means that companies are likely to continue to operate in an environment of reduced demand and increased costs for the rest of 2020. Given these dynamics we expect the rate of company bankruptcies to accelerate, which may undermine banks’ confidence to lend to corporates. The withdrawal of this financial lubricant from the engine of economic activity will further exacerbate the issues described.

It is also worth noting that over the past month or so the Federal Reserve has stopped the net printing of money and this slowdown in the rate of monetary stimulus could become a headwind to further asset price appreciation.

Nonetheless, central banks around the world have continued to demonstrate a desire to manipulate asset prices higher during times of economic crisis which reduces the perception of downside risk. This doctrine has not only resulted in all-time low interest rates, but also threatens the adoption more widely of negative interest rates. Given the enormous amount of cash currently sitting on the side-lines waiting to be deployed in this low (or no) interest rate environment, the pressure to put this money ‘to work’ is high and only small incrementally positive developments could be enough to see this happen. Therefore, given these factors, it is prudent not to be positioned too defensively.

The view from this update is that although signs of a recovery are apparent with market indices rising and lockdown gradually easing, this could be temporary relief before the real economic effects of the Coronavirus Pandemic begin to reveal themselves down the road.

The global coordinated policy response needs to be maintained and strengthened.

Please see below for Royal London’s latest market update received 29/06/2020. They provide an update on the impact of recent market events:

RLAM Economic Viewpoint

Survey data, high frequency data and now increasingly the hard data too, continue to show that developed economies are in the ‘recovery phase’ of this crisis. Albeit this is the somewhat mechanical bit as economies are allowed to open up and you get a bit of pent-up demand set loose as well. Some of the recent data points have shown much stronger than expected improvements. This, however, doesn’t tell us much about the next stage of the recovery that economists generally expect to be much slower. Social distancing, scarring (including permanent job losses, business closures and balance sheet damage) and residual fear of the virus (including as it relates to job security) will all influence the strength of that recovery and government policy still has a crucial role to play in all of them.

June business surveys improve substantially: Data in the past week or two has included several June business surveys and these have mostly seen solid improvements, with some notable upside surprises in European business surveys and US regional business surveys. However, the headline composite PMI business survey indicators for the US, eurozone, Japan and the UK remain below 50. Taken at face value, remaining below 50.0 would normally signal that these economies are still shrinking. However, mapping PMIs accurately to economic activity levels is somewhat hazardous after such a big shock to GDP (the survey asks whether things are better/worse, rather than by how much). Nevertheless, if you look at the commentary in the PMI surveys – social distancing has eased, helping many firms reopen and firms are more optimistic, but many companies also report weak demand as customers remain cautious. That is – so far – consistent with economies taking time (likely, several quarters) to get back to ‘normal’ levels of activity after a sharp initial recovery phase.

US data continue to suggest a strong start to the early stage recovery, but virus data more worrying: May retail sales, durable goods orders and some housing data have bounced significantly more than expected. However, US COVID-19 numbers have, in the meantime, become more worrying. The increase in virus cases in some states is likely to worry consumers, including the prospects of social distancing being reversed and the impact on job security. Meanwhile, Congress and the White House have still not agreed a package of economic support measures to replace those set to roll off this summer. US government policy interventions have so far done a good job in shielding household balance sheets (and therefore spending power) from the crisis. Reduced/disrupted fiscal support and the progression of the virus both have the potential to curb US recovery momentum.

Here in the UK, data also signal a solid start to the recovery phase but also a weak underlying labour market and an economy still in need of policy support: May retail sales were also an upside surprise, rising 12% in May. They are still 13.1% below February levels, but that’s a solid start to the recovery phase, especially since it was only mid-June that saw ‘non-essential’ retail stores reopen. Just as in the US, however, the UK’s early stage recovery has needed – and still needs – plenty of policy support. Government borrowing was also somewhat higher than expected in May and the levels of government debt as a percent of GDP, on the headline measure, moved above 100% for the first time since 1963. PAYE data meanwhile show the number of paid employees fell by 449K March to April. Early May estimates indicate another drop of 163K. Job vacancies in May fell to a record low. The furlough scheme is set to start unwinding from August, but this is a labour market that is far from out of the woods yet. That was recognised by the Bank of England who extended their asset purchase programme, though reduced the pace. They have become more concerned about long-term damage from the crisis. How the labour market evolves from here will be a key driver of their decisions going forward including, potentially, a decision around negative rates.

Market view from Piers Hillier, CIO, RLAM

The upwards trend in global equity markets was met with some resistance this week, resulting in sideways equity trading and moderate credit spread widening. Investors were perturbed by a sharp increase in Covid-19 cases in the US as the country reported a record number of new cases on Thursday. While the coronavirus appears to be under control in most developed countries at this stage, global new case numbers are at record highs; driven by the US, Brazil and India. In an effort to mitigate the damage of a second wave, US regulators gave in to a long-sought demand for a relaxation of the Volcker Rule as they allowed banks to invest in hedge funds and private equity funds.

Markets have also been rocked by increased global trading tensions. There have been signs of further difficulties in the trade negotiations between the US and China. Meanwhile the US threatened to impose tariffs on $3.1bn of European products, prompting an angry response from the European Commission.

On a more positive note, numerous key economic data releases have been far stronger than anticipated recently. There have been strong improvements in US and UK retail sales and in the European and US business surveys. While activity surveys are still consistent with contractions in many economies, possibly reflecting the elevated corporate debt and unemployment levels, they show that businesses are markedly more upbeat as they emerge from the worst of the lockdowns.

Reflecting a perception that the UK economy is somewhat stronger than expected, the Bank of England surprised investors at its latest meeting. While it announced an additional £100bn of bond buying, as had been expected, it slowed the pace of its purchases. The Bank said it would spend the £100bn by the end of the year, rather than by the end of August as the market had hoped. Of course, the very fact that spending was increased reveals the fragile state that the Bank considers the economy to be in, with serious concerns over the unemployment outlook.

The focus for many in the UK has been on further opening of businesses – both non-essential retail in mid June, and with the prospects of pubs, restaurants and others opening from early July. As investors we are pleased to see this – we are under no illusions that we as a society will return to prior habits in terms of spending; many of us will feel differently about being on a train, plane or in a restaurant for some time. And with other countries seeing flare-ups in the virus, it is clear that this road will have a number of bumps in it. However, it does appear that we are now through the first phase of this crisis, and returning to a more normal cycle of data and market reaction.

Royal London is the UK’s largest mutual life, pensions and investment company. This in-depth market outlook by a market leading financial services organisation adds valuable insight to our consensus view of the markets. It is evident that in recent times these views have been dominated by the Coronavirus Pandemic, but we have also now been offered insight into the socio-political tensions that have recently risen, particularly in the US, and how they in turn are effecting the economy. This is an example of how frequently reviewing these updates gives us a better view of the ‘bigger picture’.

The opinions of market leaders are key to keeping our understanding of the markets up to date. A wide variety of these views from different sources help us paint a more accurate picture on the events of the world and how they are influencing market behaviours.