Please see below for the latest Blackfinch Group Monday Market Update:

UK COMMENTARY

House prices rose 1.6% in August from July’s level according to the Halifax House Price Index. The annual increase in house price accelerated to 5.2% from July’s 3.8%, hitting its highest level since 2016.

Reports suggest that the UK is willing to walk away from Brexit negotiations in mid-October if a free trade agreement hasn’t been agreed upon.

A week of Brexit talks conclude with the EU telling Britain that it should urgently scrap a plan to break the divorce treaty, but Boris Johnson’s government have refused and continued with a draft law that could collapse four years of negotiations.

A rise in the number of COVID-19 cases in the UK brings fears of a second wave, forcing the government to reimpose some restrictions over social distancing. Daily cases have risen to close to 3,000, from c.1,000 at the end of August.

The British Retail Consortium’s figures report that year-on-year growth in retail sales rose 3.9% in August, but city centre shops continue to struggle.

UK gross domestic product (GDP) rose for the third month in a row in July, up 6.6%, although this is still 11.8% below January’s level.

A report from the National Institute of Economic and Social Research forecasts that the UK economy will emerge from recession at the end of the third quarter.

US COMMENTARY

Comments from Donald Trump that he may seek to ‘decouple the US economy from China’ suggest that the trade war between the two nations is far from over.

The US revokes visas for over 1,000 Chinese students on grounds of ‘national security’.

Initial jobless claims for the week are an exact repeat of the previous week’s number of 884,000. Continuing jobless claims rose to 13.39mln, above analyst expectations of 12.92mln.

Once again mutual agreement between the Democrats and the Republicans fails to be reached over details of a further COVID-19 support package.

US inflation rises by 0.4% in August, higher than forecast, but below the 0.6% rise seen in July.

EUROPE COMMENTARY

Insee, the national statistics institute of France, forecasts that the economy will contract by 9% this year, down from earlier predictions of an 11% drop.

EBC President Christine Lagarde announces that monetary policy remains unchanged, but that the bank has to carefully monitor the ‘negative pressure on prices’ that the Euro is exerting.

ASIA COMMENTARY

Revised GDP figures for Japan show that the economy shrunk by 28.1% in the second quarter of the year, worse than preliminary estimates released in mid-August.

China reports its largest jump in exports in 18 months, rising 9.5% in August compared to a year prior.

COVID-19 COMMENTARY

AstraZeneca confirmed that it had halted work on its COVID-19 vaccine, currently in development with Oxford University, after a ‘serious event’ during the trial process, reported to be a member of the clinical trial falling ill. However, trials officially restarted over the weekend.

These articles provide concise well-informed views that cover the whole of the market and are useful to maintain your up to date view of the markets globally.

Please keep reading our blogs regularly to give yourself a holistic and up to date view of the markets.

Please see below for the latest Markets in a Minute update from Brewin Dolphin, received late yesterday 02/09/2020:

Global share markets mostly rose over the past week, driven by growing signs of an economic recovery, positive news on coronavirus developments, and the US Federal Reserve’s shift on inflation targeting (see below).

Sentiment in the US was so bullish that the S&P500 set fresh record highs every day last week, helped by a cooling of the US/China tensions. The UK, however, was a notable underperformer, with the FTSE100 weighed by a stronger pound. This reduces the value of multi-national companies’ dollar-based earnings.

A mixed start to the week

The UK markets, along with many in Europe, were closed on Monday, although in the US it was business as usual and shares fell slightly.

On Tuesday, however, US shares rebounded, with the Dowgaining 0.76% and the S&P500 rising by 0.75%, while the Nasdaq continued its extraordinary rally, rising by 1.4% to 11,939.67.

In the UK it was a different story, as the continuing strength of the pound and Brexit uncertainties saw the FTSE100 fall by 1.7% to 5,862.05, its worst level in three months.

In early trading on Wednesday, UK shares were heading up, as Nationwide reported house prices had had risen to an all-time high of £224,123 in August, as activity rebounded after the lockdown was eased.

Market performance*

FTSE100: -3%

S&P500: +2.4%

Dow: +1.4%

Nasdaq: +4%

Dax: -0.6%

Hang Seng: -1.2%

Shanghai Composite: +1%

Nikkei: -0.7%

*Data for the week to close of business, Tuesday 1 September.

Coronavirus news

New global coronavirus cases have been trending sideways for a month now. Infections in emerging economies may be slowing especially in Brazil, South Africa (which has gone from 13,000 new cases a day down to around 2,000), Pakistan, Mexico and Saudi Arabia. In addition, new cases are falling in developed countries, led by the US which has seen a sharp decline, and also Japan, both of which are helping to offset some worrying rising trends in Europe.

Encouragingly, the death rate in this second spike of cases in developed countries is far lower than the highs of April, even though the number of new cases being detected is well above the April highs. This is likely to be because there is more testing of younger people and therefore more cases detected among younger, more resilient populations. This is helping to avoid a return to a generalised lockdown and helping keep confidence up.

UK piles on the debt

Although the UK has only just entered a recession, recent data has started to illustrate the true extent of the damage so far suffered during the coronavirus pandemic. The Office for National Statistics has revealed that, following the sheer cost of its Covid-19 response, UK government debt has risen above the £2trn mark for the first time.

According to the data, spending on measures (such as the widely used furlough scheme) meant total UK government debt was £227.6bn higher in July 2020 than it was a year before. At the same time, tax revenue has been hit hard by the fact many businesses and people are earning and spending less. Combined with greater government borrowing, this is the first time UK government debt has been above 100% of gross domestic product (GDP) since the 1960s.

Jackson Hole Symposium

In his speech to the annual gathering of central bankers and policymakers in Jackson Hole, Wyoming, US Fed Chair Jerome Powell confirmed it is moving to a system of inflation “average targeting”.

This is important because it means that it will allow inflation to run above 2% to make up for a previous undershoot. The Personal Consumption Expenditure (PCE) price index is the Fed’s preferred inflation index for the 2% target, and in the chart below you can see it has been running below 2% for a sustained period of time for the past decade.

According to the St Louis Fed, even if you allow for 2.5% PCE inflation, which is an overshoot of inflation of 0.5%, it will take until 2032 to make up for the inflation undershot over the past decade. So, the implication is that the Fed wants to let the economy to run “a little hotter”, with faster-rising prices, without the need to raise interest rates or tighten monetary policy when inflation is above 2%. It also likely means that US interest rates will stay at, or near, 0% for a long time, which should be a positive for investment assets. Indeed, many think that the US will need to return to near-full employment and inflation of at least 2% before the Fed will consider raising rates again. We expect further guidance on this at the next Fed meeting later this month.

US/China tensions cool

Powell’s speech came in a week of broadly positive economic news for the US. At the beginning of the week, both the US and China affirmed their willingness to negotiate and declared they were ready to progress with trade talks. With tensions between the two nations a recurring source of stress for investors, this update was welcomed by markets.

US economic data

US Durable goods orders in July were up 11.2% vs expectations of 4.8%, helped mostly by new orders for vehicles and parts (+21.9%), electrical equipment and electronic products. Durable goods orders are a proxy for business investment demand and it has now risen for a third consecutive month – a sign things are really normalising.

US housing data, which is vital in supporting economic growth, has been really encouraging. July new home sales came in significantly above expectations at $900k versus the estimated $790k, surging to the highest level since the 2009 financial crisis. Existing home sales increased by a record 24.7% in July to an annual rate of $5.86m, the highest level since December 2006. The median house price rose to 8.5% on an annualised basis, the highest since April 2015. Pending home sales also rose 5.9% in July compared to June, after a huge 16.6% increase in June over May.

Australia enters recession

Having avoided a recession even during the financial crisis of 2008/09 (thanks to huge demand from China for its iron ore and other commodities), the world’s longest economic expansion has finally ended. After almost 30 years of uninterrupted growth, Australia’s economy contracted by 7% in the June quarter, following a 0.3% contraction in the first three months of the year.

Brewin Dolphin are market leading fund managers, and so receiving their regular insight in this efficient manner is a quick but well-informed way to update your consensus view of the global markets.

Please keep using these blogs to regularly update your knowledge of current market affairs from around the world.

Please see below for Brewin Dolphin’s latest Markets in a Minute article received yesterday 18/08/2020:

Global equity markets pushed higher for most of last week on positive economic data, before an ugly session on Friday erased most of the gains. Markets dropped in the UK and Europe as France was added to the quarantine list, which hit travel stocks hard. Prior to that, the Nasdaq hit a new record high, as did the gold price, while the S&P500 briefly surpassed the record high it set back in February before closing slightly lower.

Last week’s markets performance*

• FTSE100: +0.95%

• S&P500: +0.64%

• Dow: +1.8%

• Nasdaq: +0.07%

• Dax: +1.8%

• Hang Seng: +3.84%

• Shanghai Composite: +0.2%

• Nikkei: +4.3% *

Data for the week to close of business on 14 August 2020

Mixed start to week on US/China tensions and virus concerns

Markets were mixed yesterday after digesting news that the US and China cancelled their weekend talks to assess how Phase 1 of the trade deal was progressing. It was blamed on “scheduling conflicts” but given the recent escalation in tensions, including banning WeChat and Huawei, perhaps a postponement is no bad thing. London equities rose, with the FTSE100 up by 0.6%. In the US they were mixed – the Dow closed down 0.3% at 27,844.91, while the S&P500 rose 0.27% to 3,381.99. The Nasdaq closed 1% higher at 11,129.73. Europe was also mixed, with the pan-European Eurostoxx up by 0.3%, alongside gains in Germany and France, but equities in Italy and Spain lost ground.

There are concerns that economies are reaching their maximum capacity for growth without further easing of restrictions, which could increase the chances of a second wave of coronavirus infections. However, surging cases in some European countries are leading to more containment measures, not less.

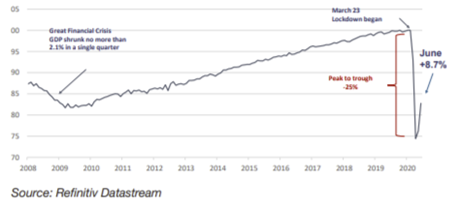

Level of UK GDP (February 2020=100)

UK recession

The standout headline last week was the UK’s record decline into recession in the second quarter. The -20.4% quarterly fall in GDP does look ugly. It is the largest quarterly decline on record, and it was the biggest quarterly fall amongst major economies. As a services-sector driven economy, the UK has been hit harder than other countries – there was a -23.1% drop in consumer spending, while business investment fell by -31.4% in the second quarter.

More encouragingly, GDP rose by 8.7% month-onmonth in June after 2.4% rise in May thanks to the easing in lockdown restrictions and there is good reason to think this will continue in the short term. For instance, wholesale and retail output rose by +27.0% in June compared with May. And with the reopening of pubs and restaurants in July and the “eat out to help out” scheme in August, we believe the unprecedented fall in GDP in quarter two will be followed by a recordbreaking double-digit growth in quarter three.

In addition, more current high-frequency data such as restaurant bookings, retail footfall and travel show normalisation in activity. However, the risk is that unemployment rises sharply once the furlough scheme ends in October. The ONS said last week that 730,000 fewer people were employed in July compared to March, based on data from HMRC, but with an estimated 5 million people still on furlough.

If such headwinds emerge later in the year, we think the Bank of England will expand its asset purchase program and further stimulus maybe announced by the Chancellor.

Japan follows UK into recession

Japan announced on Monday that its economy had contracted by 7.8% in the second quarter, which is less severe than the slowdowns in the UK, US and much of Europe. This is most likely because it had a less stringent lockdown. Still, the annualised rate of contraction of 27.8% for the three months to June is worse than Japan’s decline at the height of the financial crisis.

US retail sales and inflation

US retail sales rose 1.2% in July compared to June, below expectations for a 1.9% increase. While the sharper than expected slowdown was a disappointment, the good news is that US nominal retail sales have already surpassed their pre-Covid level, so a flattening off is to be expected. Also, there is uncertainty surrounding the unemployment benefits which account for a large part of the income for millions of unemployed Americans, and there is little sign of progress between Republicans and Democrats at the moment. This will be weighing on consumer confidence.

Meanwhile, the US consumer price index jumped 0.6% in July compared to June, which is the biggest monthly increase since June 2009 (vs +0.3% expected), while the core annualised rate rose to 1.6%. These numbers are clearly still very benign compared to the Fed’s inflation target of 2%, but the risk is that inflation could be a problem further down the road.

Chinese data hints at slowing recovery

Overall the China July activity data continued to show improvement but at a slower pace, not surprising given the lingering Covid threat. The talking point was the disappointment in retail sales given China is increasingly a consumption-based economy, retail sales were still down -1.1% on an annualised basis, perhaps due to a spike in cases and people being cautious about going out. However, the Chinese savings rate is over 40%, so consumers would appear to have plenty of spending power for when confidence returns.

We can use these blogs to keep an up to date consensus view of the global markets. Recent recession news may have come as a shock to many, but the background to situations like these can be more easily understood by reading widely on investment issues.