Please see the below article from Invesco received this morning:

Key takeaways

- In our analysis, Invesco experts offer key insights into the changing risks facing markets and offer their views on what this means for fixed income and equities.

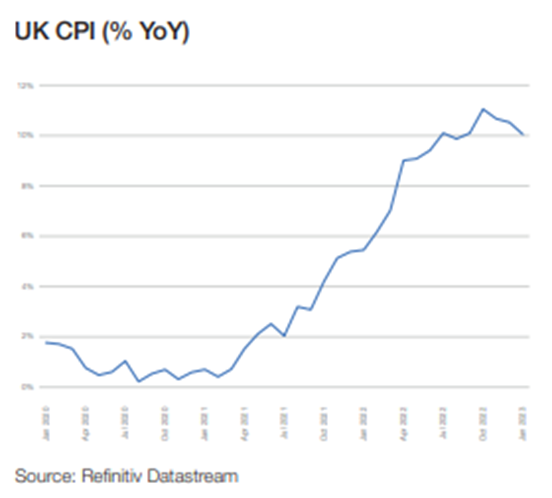

- The outbreak of conflict on 24 February 2022 exacerbated inflationary pressures. And in hindsight it seems clear that central banks reacted too slowly.

- Geopolitical and energy risks, though still present, have receded. The focus has largely shifted to monetary policy and whether central banks can curb inflation and avoid recession.

On the first anniversary of Russia’s invasion of Ukraine, the outlook for the global economy is much changed. Geopolitical and energy risks, though still present, have receded. The focus has largely shifted to monetary policy and whether central banks can curb inflation and avoid recession.

So, Russia’s belligerence is just one facet of a complex macroeconomic environment. After years of persistently low inflation, the post-Covid economic restart in late 2021 unleashed inflationary forces across the world as pent-up consumer demand was released despite snarled supply chains. The outbreak of conflict on 24 February 2022 exacerbated inflationary pressures. And in hindsight it seems clear that central banks reacted too slowly. In Europe, meanwhile, the war has had an outsized impact, especially on its energy security.

Amid this backdrop, Invesco experts offer insights into the arc of economic, geopolitical and policy changes since the war started. They also offer their views on key asset classes and environmental, social and governance (ESG) considerations.

Flexible thinking in the fixed income space

The period following the invasion was the worst ever for global credit, which lost 18% from January to October, surpassing even the drawdowns of 2008.

“In truth, the conflict was more of an aggravating factor to the monetary tightening by central banks which had started in Q4 2021,” said Co-Head of Global Investment Grade Credit Lyndon Man.

“Nevertheless, we did see European assets impacted more acutely given the physical proximity and the tighter squeeze on energy supplies.”

Man expects the US Federal Reserve’s rate hikes to “top out” this year, notwithstanding some recent hawkish comments.

“The European Central Bank is playing catchup and European spreads remain wider3 vs. US; Asia also looks attractive having underperformed last year. Though we had a strong rally in January, yields are still at highs not seen since 2009, while flows and corporate fundamentals remain broadly supportive,” he said.

European equities: Renewables in focus

Fears that Europe could face widespread energy shortages were commonplace at the outbreak of the war. But a relatively warm winter helped countries navigate the crisis despite higher energy prices.

“After the initial shock sell-off when Russia invaded Ukraine and subsequent short-term market recovery, energy security and inflation have become the dominant themes driving the European market,” said European Equities Fund Manager James Rutland.

“Energy costs have already fallen substantially, with economists revising up their negative economic forecasts accordingly. With inflation starting to fall from high levels, we could see the headwind from falling real wage growth turn into a tailwind and therefore a rather better outlook for the consumer alongside the broader economic environment,” he said.

ESG and policy: The energy transition

The EU agreed to phase out the bloc’s dependency on Russian fossil fuel imports in March last year. It banned almost 90% of all Russian oil imports by the end of 2022 (with a temporary exception for crude oil delivered by pipeline). In December, it followed up with the introduction of a temporary emergency energy price cap to protect its citizens from excessively high gas prices.

“While much of the response this past year has been dealing with the immediate priority of keeping the lights on by finding alternative sources of gas and oil, political focus is starting to shift towards more structural reforms. These include the structure of the European electricity market and measures to further support renewable energy,” said Invesco’s EU Government Relations and Public Policy team.

The energy trilemma – energy security, affordability, and sustainability – points to renewables in the medium to long term as a resolution to some key underlying pain points around regional energy supply and fossil fuel-led inflation, according to Sudip Hazra, Head of ESG Research.

“Calls for the oil and gas sector, which has the expertise and cash flow to increase investments into the energy transition via diversification into renewables, look set to continue,” he said.

Please continue to check our Blog content for advice, planning issues and the latest investment, markets and economic updates from leading investment houses.

Andrew Lloyd DipPFS

03/03/2023