Please see below Daily Investment Bulletin from Brooks Macdonald:

What has happened

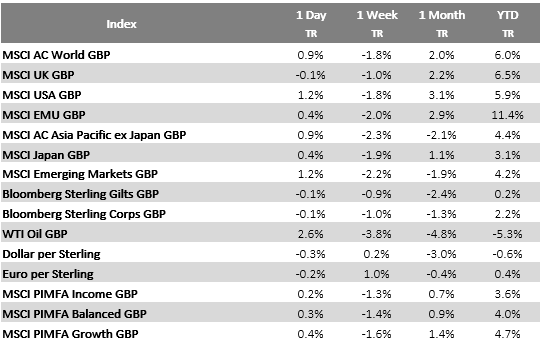

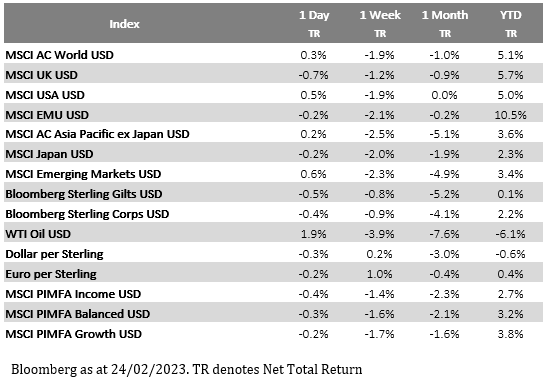

Equity markets saw huge intraday volatility yesterday as risk assets initially surged then retreated before staging an end-of-day rally. The afternoon sell-off was catalysed by further revisions to the US and European inflation prints whereas the final rally has been attributed to technical factors generating buying activity in the options market. While the focus was on the inflation data, Nvidia’s shares surged following their upside beat to revenue forecasts, this helped lift semiconductor shares more broadly.

Inflation data

The Euro Area core inflation print for January was revised upwards by 0.1% yesterday, bringing the year-on-year rate to 5.3%, the highest since the Euro was formed. This will increase the pressure on European bond markets while also giving additional justification to more hawkish members of the ECB to continue to tighten policy aggressively. The US also saw upward revisions to inflation with the PCE inflation measure rising by an annualised 3.7% in Q4 rather than the 3.2% previously. The core PCE number was also revised higher, from 3.9% to annualised 4.3%, showing that the inflationary slowdown in Q4 was less dramatic than markets had hoped.

Jobs data

The release of the weekly jobless claims provided more comfort to market with both the number of new unemployment claims for the week, and the ongoing number of claims, coming in lower than market expectations. Before anyone prematurely declares victory on the tightness of the labour market, the last 3-months of data have continued to show a tight labour market on many measures.

What does Brooks Macdonald think

While the market moves were dramatic yesterday the volume of market data and news was relatively light. One additional area of volatility was the UK gilt market with the Bank of England’s Mann saying that she believed ‘that more tightening is needed, and caution that a pivot is not imminent.’ One should note that Mann is known as one of the tougher hawks on the Monetary Policy Committee but these comments helped bond markets to almost fully price in a 25bp interest rate hike when the Bank of England next meets in March. This would bring the base rate up to 4.25%

Please continue to check our Blog content for advice, planning issues and the latest investments, markets and economic updates from leading investment houses.

Adam

24/02/2023