Please see below that latest articles published by Jupiter Asset Managers yesterday (15/07/2020):

UK recovery pushed further out as GDP growth disappoints

Philosophically, Dan Nickols, Head of Strategy, UK Small & Mid Cap and his team are investors who are happy to range across the Value/Growth spectrum depending on where they can find the most appealing opportunities at a given point in time. In the UK small and mid-cap universe, as elsewhere, Growth has trumped Value for a number of years. The most expensive quintile in the universe trades on about 39x forward P/E, but if you remove the outliers from either end and compared the 30th percentile against the 70th percentile in terms of valuations, the gap there is widening too. This is the most polarised market from a valuation perspective that Dan can remember over his c.20-year career.

It is easy to rationalise why the market is behaving this way, said Dan, with so much uncertainty due to Covid-19 as well as the ongoing geopolitical issues at present. In that environment, with interest rates even lower for even longer, it is understandable that so many investors favour the relative ‘certainty’ of earnings provided by the growth dynamic notwithstanding elevated valuations. UK GDP growth in May was only 1.8% compared to the consensus expectation of 5%, meaning that the recovery feels like it is getting pushed further out. Nevertheless, looking forward it feels to Dan like the cheaper, more economically sensitive parts of the market, have more to gain from economic normalisation – providing, crucially, that one can find stocks that are not structurally challenged.

Everyone is in a holding pattern, for now, said Dan, while we wait to see what path the virus will take over the coming months and into next year. Have governments and central banks done enough to put economies into cold storage so they can be thawed out and resume growth, or will there be widespread balance sheet disruption that will take longer from which to recover? Only time will tell, but some visibility around these issues is what the cheaper parts of the market need to outperform, in Dan’s view. In the meantime, Dan and his team continue to prefer structural growth stocks, but are very conscious to have complementary exposure to well-run, conservatively-financed cyclical stocks that they believe can re-rate when conditions to normalise.

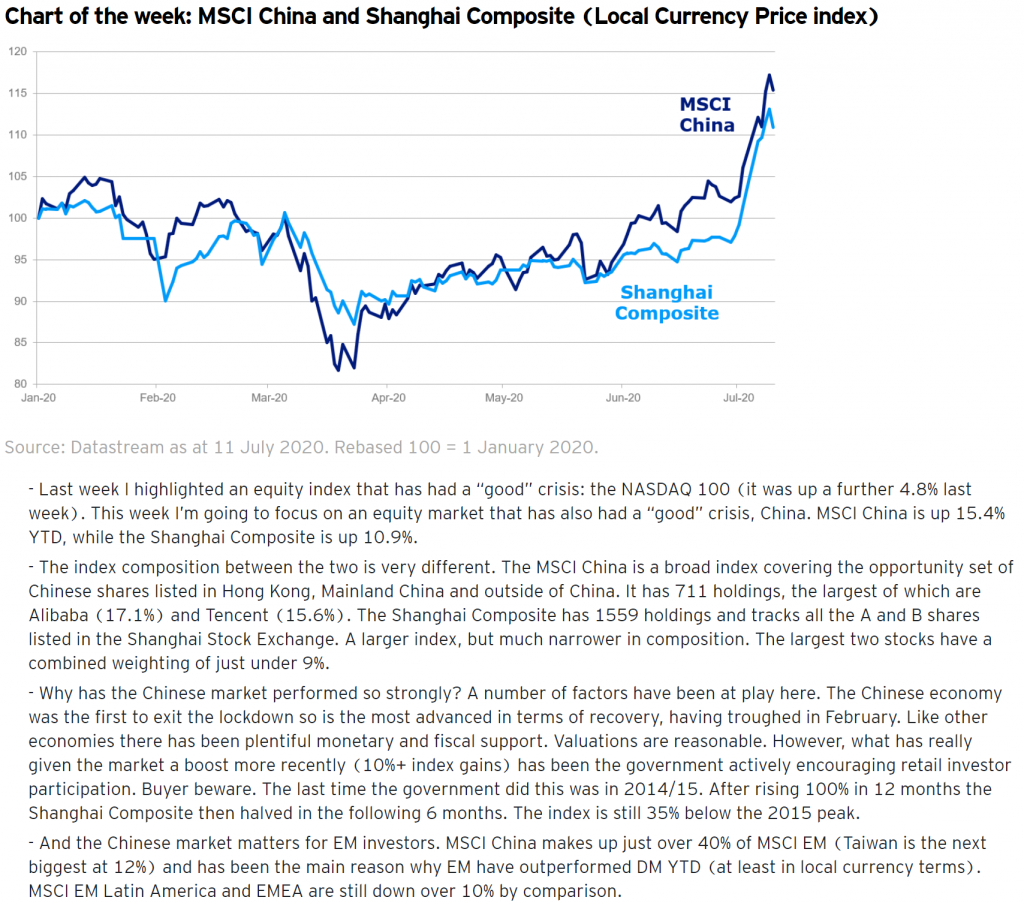

Is China’s domestic market overheating?

The biggest standout in a sea of red for global equity indices this year is the NASDAQ, which is up about 16%. However, there has, said Ross Teverson, Head of Strategy, Emerging Market, been a similar move in the CSI 300 Index, which consists of the 300 largest domestic A-share companies listed in Shanghai and Shenzhen. Meanwhile, other major emerging markets like Russia, Brazil, India and Mexico are down anywhere from 13% to 34%.

If you look within China, that gain in the CSI 300 Index looks modest to compared to what some other indices have done, for example China’s own equivalent to the NASDAQ is up c.55% YTD. Helping to fuel this rally has been a growing number of retail margin accounts in China.

There are signs, therefore, that the domestic Chinese market is starting to get quite heated. Valuations of Chinese companies with dual listing in Hong Kong began this year on a premium for their domestic listing, and that premium is now even wider.

What has driven this investor optimism? It is certainly true that China has coped relatively well with Covid-19, and there is also a strong narrative about the Chinese government’s support for home grown technology. Ross stressed that we should remember, however, that the Chinese economy has by no means escaped damage from Covid-19. A recent survey found 18% of respondents said their income had fallen by more than 50% during the pandemic, with another 15% saying their income had fallen 25%-50%. As in the West, the full impact of this economic stall has yet to be fully felt.

Ross’s own preference has been to gain exposure to China through Chinese businesses listed in the US, Hong Kong or Taiwan, as often he finds it possible to buy better business on lower valuations that way. Given the strong bull run in China’s domestic market, that clearly has not been the right positioning recently, and Ross won’t try to predict the timing of a correction, but Ross continues to believe that asset price discipline is vital.

What does a 5G world look like?

We don’t yet know exactly what the 5G technological revolution will look like, but it will certainly change how we interact with the world, said Stuart Cox, Fund Manager, Global.

With so many people now working from home, it’s easy to see why very efficient, high performing phones would be in high demand. Theoretically, 5G is dramatically faster than current 4G technology. Initially, coverage may be patchy, of course, until the infrastructure is fully rolled out, but the long-term potential of 5G phones is clear, says Stuart.

With such fast speeds, 5G handsets could render WiFi routers from broadband providers obsolete. We don’t yet know what ‘killer apps’ would replace it – the equivalent to Office 365 kickstarting the cloud revolution – but it’s very likely that 5G phones will become the medium through which we interact with a future 5G world, whether that’s smart cities, autonomous driving, industrial applications, or home offices. It’s a huge opportunity, says Stuart, and one that could unlock a lot of future growth that some of the world’s largest tech companies in particular are well placed to capitalise upon.

Please continue to check our Blog content for the latest investment, markets and economic updates from leading investment houses.

Please keep safe and healthy.

Carl Mitchell – Dip PFS

IFA and Paraplanner

16/07/2020