Please see below the latest market update article from Brewin Dolphin – received 04/08/2020.

Brewin Dolphin – Markets in a Minute – Equity markets mixed, gold and silver continue to rise

Global share markets were mixed last week, with China outperforming the rest of the world as its economic recovery continues. US indices were flat or marginally up thanks to some extraordinary results from the US tech giants, but equities in the UK and Europe have fallen on poor economic data, rising coronavirus cases and a “wall of worry” about the economic outlook later this year.

Bond yields broadly fell again with yields on US Treasuries hitting record lows, while gold and silver prices rose as investors looked for safe havens. Meanwhile, the US dollar suffered its worst month in 10 years against a basket of currencies.

A positive start to the week…

Markets started the new week with a rebound. Equities in the UK, Europe, US and Asia all pushed higher on Monday, as surveys of manufacturing businesses in the US, UK and Europe suggested that factory activity was increasing. The FTSE100 saw the largest daily increase, jumping by 2.3% on Monday, pushing back up through the 6,000 level to 6,032.85.

Virus developments

New cases appear to be slowing in the US, suggesting the pausing of re-openings and the mandated use of masks in many states may be working. It also saw a reduction in hospitalisations, and the fatality rate is now around 1.5% compared to 7% in April. This is probably because more young people are getting the virus while older people are taking more care to protect themselves, while treatments are also improving. All this helps reduce the chance of another national lockdown.

Unfortunately, after a period of falling cases, Europe is now seeing infection rates rise again, driven heavily, but not exclusively, by Spain (about 50%).

Japan has also seen a big rise and even China has seen a pick-up in new cases, albeit from a very low base. It demonstrates just how hard the virus is to completely suppress, but China is an example of how an economy can recover while managing localised outbreaks.

The news of two revolutionary new coronavirus testing kits that give results in 90 minutes will no doubt be a great help in containment efforts. Previous tests took two days.

What’s eating the dollar?

Even after falling so far last month, we suspect the trend remains weaker for the dollar. Despite the recent reduction in coronavirus cases it still seems as if Europe will do a better job of containment than the US, with governments generally prepared to impose local lockdown measures before things get out of hand.

Both regions have produced stimulus packages that are supporting growth, primarily consumption at the moment, which you might expect to be positive for the dollar. But it comes at the cost of an increased budget deficit (where government spending exceeds its revenues), and this will likely result in an increased current account deficit (where the value of its imports exceed the value of its exports). Both of these can weigh on the dollar.

Time is tight for US stimulus deal

The extra $600-a-week in unemployment payments announced as part of the original stimulus package in March, came to an end last week. Politicians are still deadlocked in negotiations about the details of a new stimulus bill, with Republicans wanting to cut the payments to $200 a week and Democrats wanting to keep payments unchanged.

All this while the employment crisis burns (as evidenced by another week of higher jobless claims). Even given the tight timeframe, with the Senate due to go into summer recess on 7 August, we still think a deal will be passed, even if it means having to push back the summer break. The alternative would be delaying until September which is an outcome that both parties would be keen to avoid.

Corporate news

Earnings season in the US has been producing the right kind of headlines. Around halfway through and nearly 85% of companies have beaten EPS estimates, ahead of the more usual 80%. Exactly two thirds of companies have reported better-than-expected sales levels. That is an improvement on most other years, when an average of 50% of firms exceeded sales expectations.

Last week saw updates from some of the big tech names. After announcing stellar results as beneficiaries of the new work and play at home environment, the combined market value of Facebook, Amazon, Apple and Google soared by $230bn in after-hours trading on Thursday, taking their total value to more than £5trn for the first time and lifting the S&P500 into positive territory for the week.

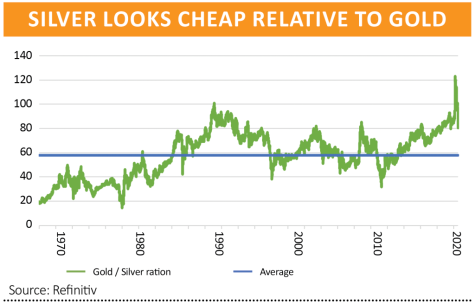

All that glitters…

The best play on a weaker dollar has been precious metals, and while the focus has centred on the gold price hitting record highs, silver has actually been the better performer of late, rising nearly 25% in July alone. We still think there is more upside because silver’s rebound has not yet fully reversed the historic divergence in the ratio between the price of the two metals, plus silver has additional demand for industrial uses.

Another good overview of the markets from Brewin Dolphin. Although markets started with a rebound this week, we are still experiencing high levels of volatility.

Please continue to check back for our latest blog posts and updates.

Charlotte Ennis

05/08/2020