Please see Active Minds article below from Jupiter Asset Management – received 06/08/2020

Summer warmth turns chilly for UK equities

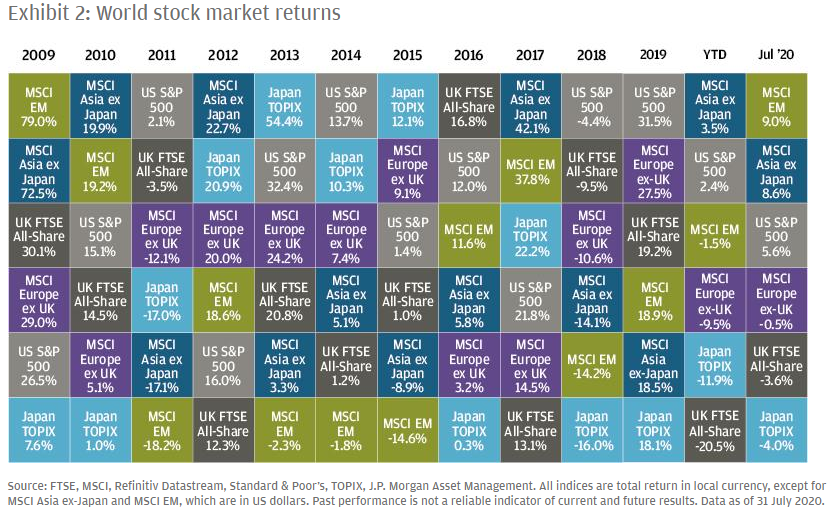

In contrast to the warm, sunny weather in the UK at the moment, the UK equity market feels quite chilly and unloved in a global context, said Dan Nickols, Head of Strategy, UK Small & Mid Cap. The S&P 500 Index in the US is now up year-to date, while FTSE All-Share Index is down over 20% and the Numis Smaller Companies Plus AIM ex Investment Companies Index of UK small and mid-caps is down almost 18%.1

The reason why the UK has been so weak compared to other markets is partly compositional, as it contains fewer technology names, more financials, and more discretionary consumer stocks. Dan believes there is another layer too: the ongoing Brexit drama means that, for overseas investors, the UK can simply be filed under ‘too difficult’ and ignored for now in favour of other equity markets.

With an eye on the future, Dan is looking at real-time data around things such as credit card transactions, which indicate there was a good recovery until the end of June that then showed signs of slowing in July. Dan also highlighted a risk off unemployment picking up in the coming months, as the furlough scheme tapers off into a weak economy, bringing the importance of judicious stock and sector selection into sharp relief.

All of the above creates a challenging environment for UK equity investors. Dan highlighted that, in the UK small and mid-cap world, leadership in the market from a style perspective is very stark, as value continues to struggle badly while momentum, growth and revision factors remain relatively strong. Dan and the team are trying to navigate this by being purposefully overweight structural growth names, while tempering that with some exposure to what they believe are well-managed, conservatively financed stocks that are more geared into economic growth – although they have pared these back over the last few weeks, while retaining exposure to the stocks in which the team have highest conviction.

Large-cap tech stocks drive emerging markets

Emerging markets had a pretty good July, with the MSCI Emerging Markets Index finishing the month up around 3% (in sterling terms), noted Colin Croft, Fund Manager, Emerging Markets. Year to date, the index is almost flat, which is quite remarkable given the state of the global economy, said Colin.2 However, gains have been concentrated in a fairly narrow set of large-cap tech stocks, which now represent significant weightings in the index. These stocks are up significantly year to date, almost entirely driven by re-ratings, rather than seeing much in the way of earnings upgrades.

It is impossible to predict what the trigger could be for a change in the relative rating of these kinds of stocks. However, Colin suspects that as soon as there’s some sort of light at the end of the tunnel in terms of the pandemic, investors will want to take profits in these kinds of ‘haven’ stocks that have become so expensive, and could instead choose to move into stocks with more leverage to the recovery. It’s likely to be a bumpy road to get there though – for example, sentiment for recovery-dependent sectors such as financials and travel has been badly affected by a pickup in cases in countries that were previously looking much more encouraging, such as Spain and Australia. Elsewhere, the outbreak in Latin America shows no signs of abating – instead, it is plateauing at high levels.

Fortunately, there are some structural themes playing out that are more or less independent of the pandemic, highlighted Colin. One of these is the likely positive impact of the 5G rollout; another is the gas pipe reform we’re seeing in China. The latter has been under discussion for years, but finally some progress was made over the past month or so. Pipelines there were owned by the big three majors, which were also producers; however, now China is injecting all the pipe assets into a national company, which will then allocate the capacity in a strategic manner. Colin noted that this is happening on terms that have been surprisingly favourable to investors: they’re being injected at 1.2x or 1.4x book value; they’re also getting 40% cash payments for it, not just shares; and there’s talk about paying special dividends too.

Tech in the time of coronavirus

The significant impact of technology across various sectors has been one key positive theme accelerated by the pandemic, says Makeem Asif, Fund Manager, Multi-Asset. Whether it is working from home, educating children online, retailers’ pivoting to online distribution or the need for more cybersecurity, the pandemic has led to a step change in the use of tech.

But, for Makeem and the global convertibles team, the biggest issue has been the valuation of some software companies where it is not unusual to see shares trade on 25x-40x revenues. In the semiconductor space, despite some initial supply chain disruptions, production in most factories in Asia is back on track. Earlier this week the semiconductor industry association published its monthly report which tracks sales and average selling prices of units. This highlighted how robust the semiconductor industry has been during the pandemic: in the twelve months to June, sales grew 7%, up from the 3% annual growth seen in May. The team expects chip sales to continue to rise driven by demand from data centres, autos, electric vehicles and other devices. In addition, says Makeem, such companies tend to have more reasonable valuations with good cashflow metrics.

In the fintech space, the hygiene requirements arising from the pandemic have acted as a catalyst to accelerate the uptake of digital payments with their clear advantage over cash. One of the dominant US card payment companies said it expected to reissue around 70% of its cards in the next 12-18 months. Although the switch to digital payments is not new, Makeem says there is still a significant amount of growth to come as some economies have been slow to adapt. Furthermore, there are still around 1.7 billion people worldwide who do not have a bank account.

1Source: FE, index returns in GBP to 31.07.2020

2Source: FE, index returns in GBP to 31.07.2020

Articles like this are useful for getting an insight to the market from market experts within their specified field.

The Coronavirus Pandemic has affected our lives in many different ways but as noted above a key positive theme has been the boost of the technology sector within the markets.

Please continue to check back for our latest blog posts and updates.

Charlotte Ennis

07/08/2020