Please see below an article published by J.P. Morgan last week on 03/08/2020 and received today, providing their summary of markets throughout July 2020:

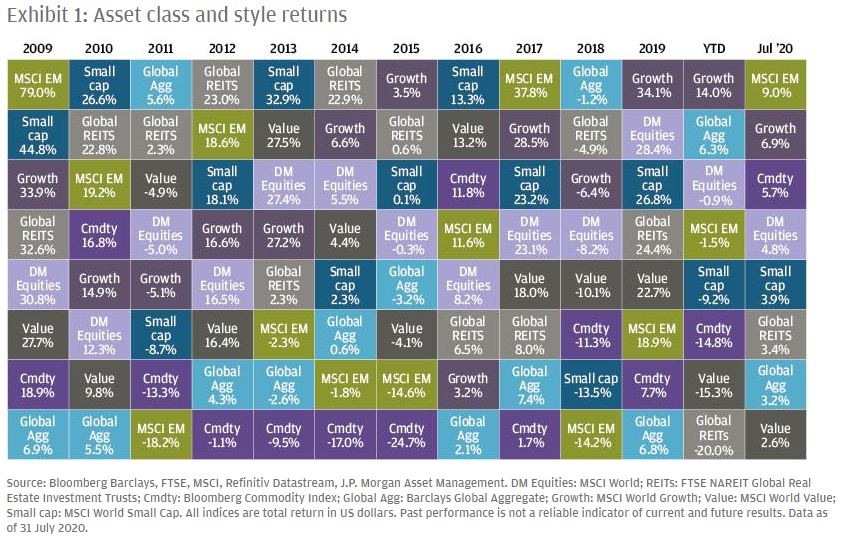

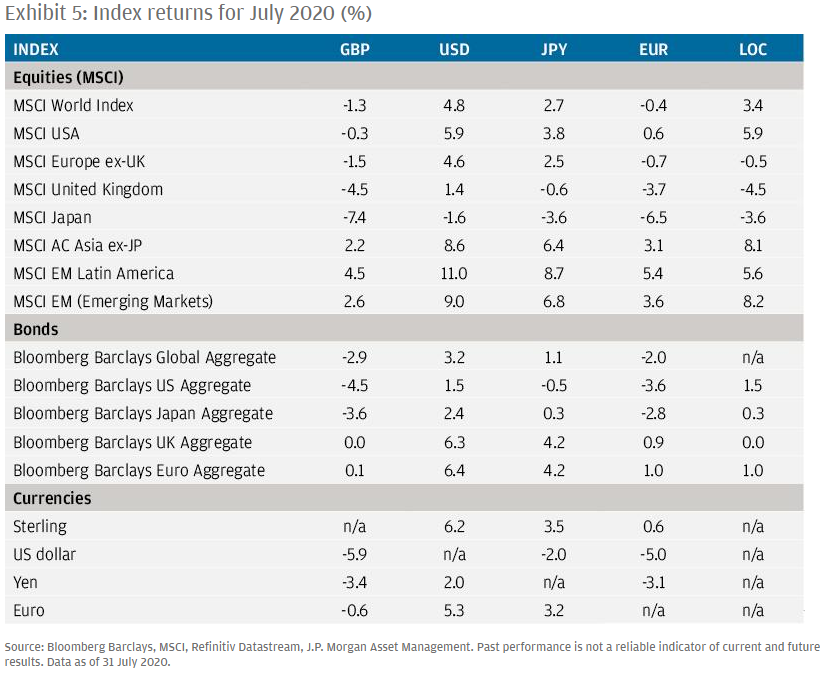

July provided further evidence that economic activity has improved since lockdowns were lifted, but high-frequency data pointed to a pause in the recovery, particularly in the US. The pace of increase in new infections also rose in most regions from the start of July, but appeared to slow towards the end of the month in the US, while rising, from much lower levels, in Europe and Japan. Hopes for a vaccine were boosted by positive early-stage trial results. Over the month, the MSCI Emerging Markets equity index rose by 9.0% and MSCI Developed Markets by 4.8%. Credit also rallied, while government bonds held on to their gains for the year and gold rose by 11%.

Major central banks took something of a back seat over the past month, having already flooded the market with liquidity and taken rates close to their lower bounds. However, governments have been under pressure to provide further fiscal support. Congress debated the extent to which unemployment benefits should be extended and whether further stimulus cheques should be provided, with a deal proving difficult to get over the line.

US

Daily new infections in the US began to rise again from mid-June, and that trend continued throughout most of July. The initial Covid-19 outbreak was mostly centred in the northeastern states, but throughout June and July infections began to rise rapidly across the rest of the country. As a result, many states have now begun to partly reverse or pause their reopening plans. The World Health Organisation recommends that the percentage of tests that are positive should remain below 5% for 14 days before starting to reopen an economy. Currently, the majority of US states are seeing positive tests in excess of this recommendation. Despite a higher number of daily new infections, the number of new daily deaths as a result of Covid is lower now than at the prior peak. This could be due to improved treatment and more social distancing among older age groups. However, hospitalisations have risen and will need to be monitored to assess whether new infections will lead to rising pressure on health systems and potential further business shutdowns in the worst-affected states.

US GDP for the second quarter fell by an annualised rate of 32.9% compared with the previous quarter. While this confirms the largest decline in GDP since the Second World War, investors have been more focused on the recovery in some of the economic data since April. US retail sales have rebounded by 27% since their low in April and are just 1% below their peak in January of this year. Not all the data is picking up at such a rate though. The high-frequency mobility data has begun to slow as the spread of the virus has increased. Small business revenue has partly recovered, but still remains around 20% below pre-Covid levels. The labour market recovery is also showing some signs of stalling. Initial jobless claims remain high and are no longer falling; meanwhile, the employment component of the July manufacturing purchasing managers’ index (PMI) remains below 50. July’s consumer confidence reading also fell.

Consumer incomes have so far been protected by support measures from the US government, which provided USD 1,200 stimulus cheques as well as a USD 600-per-week boost to unemployment benefits. Congress is negotiating another stimulus bill, which could see a second round of stimulus cheques as well as some extension to unemployment benefits, though probably at a less generous level than before.

We are in the midst of the US second-quarter earnings season, with expectations of roughly a 45% year-on-year decline. So far, with over 55% of companies having reported, earnings have come in a little stronger than expected. The S&P 500 rallied 5.6% over the month.

Europe

Europe looked to have managed the virus better than many other regions in the second quarter, though there are some concerns about rising cases more recently. Activity has been rising across the region, particularly in Germany, given new infections had remained low for some time. However, a recent outbreak in Spain, coming just before the peak of the summer tourist season, has cast some doubt over the potential for a swift economic recovery. The risk of an increase in Covid cases as economies reopen is leading to a potentially more stop-start and geographically differentiated recovery, though an effective vaccine would clearly be a strong catalyst for a more sustained economic rebound.

Second-quarter GDP fell by 12.1% compared with the previous quarter – the largest quarterly decline in the eurozone’s history. European consumer confidence also stalled after healthy gains in previous months, but the composite PMI improved significantly, to 54.8 versus April’s reading of just 13.6.

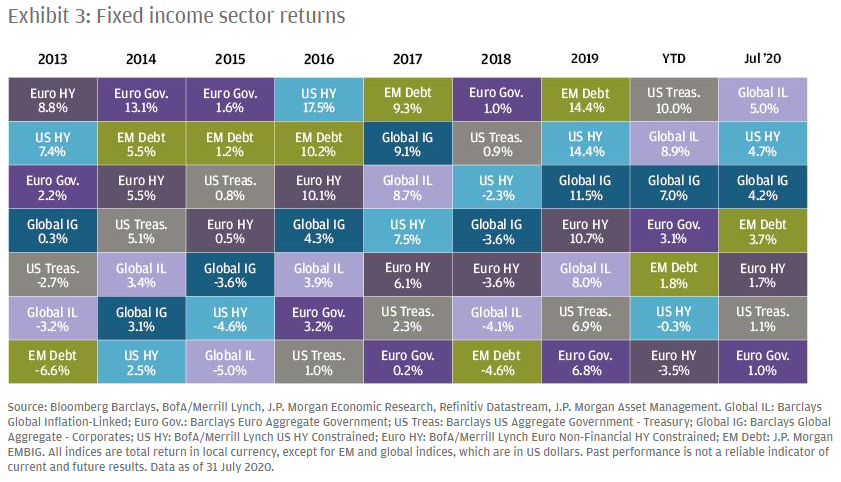

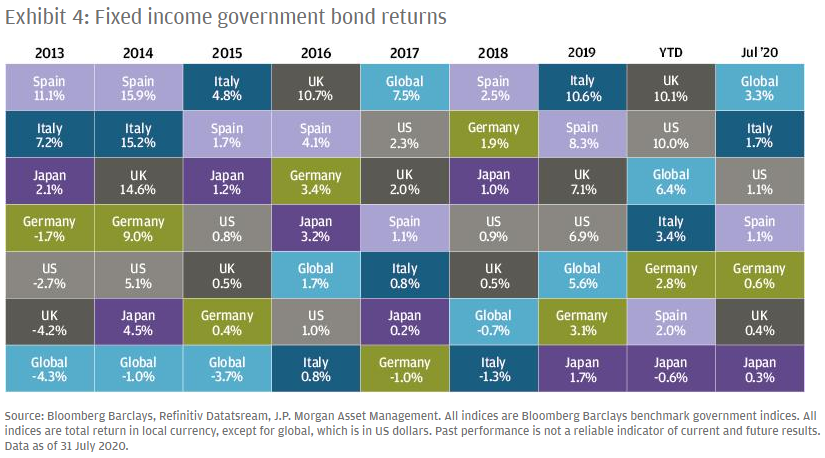

The European Union (EU) agreed a EUR 750 billion recovery fund in response to Covid-19. Importantly, the recovery fund will be backed by common bond issuance by the European Commission. This is a significant step toward potential fiscal integration across the EU and has increased appetite for European assets. Italian and Spanish bonds returned over 1%.

UK

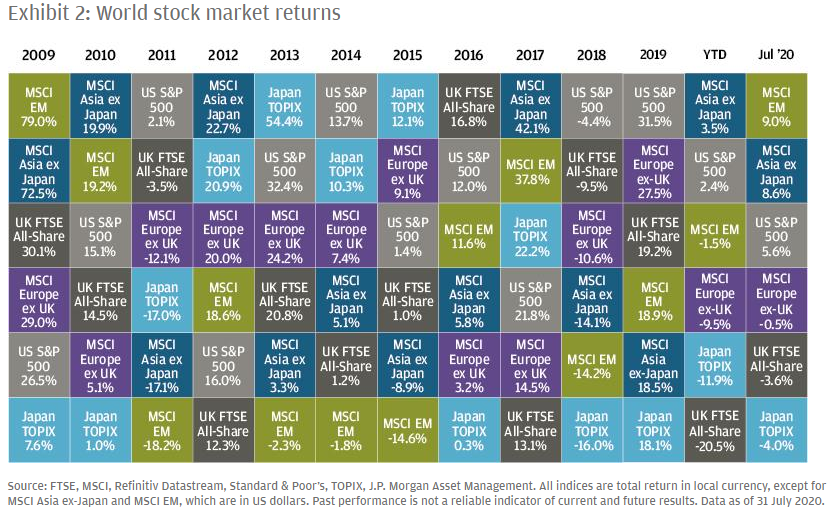

Daily new cases of Covid-19 in the UK had been falling, but again concerns around a small increase in cases have surfaced at the same time as the government has lifted activity restrictions. A summer economic plan put forward by the Chancellor aims to introduce measures to get the economy back on its feet by reducing stamp duty, cutting VAT for the food and hospitality sectors and offering companies GBP 1000 for each furloughed staff member that they retain until the end of January. At the same time as giving with one hand, the Chancellor plans to take with the other as he rolls back the furlough scheme, which had helped protect the jobs of millions of UK workers. Some of those jobs could now be at risk if activity doesn’t recover before the scheme is wound down. UK assets have been somewhat out of favour compared with other regions over the past month. The FTSE All-Share fell by 3.6% in July.

Emerging markets and Asia

The increase in new cases in Brazil and India continued throughout July. Recent outbreaks in Hong Kong have also seen the reintroduction of restrictions, which will limit the number of people in group gatherings to just two, while mask-wearing is mandatory.

In China, GDP for the second quarter grew by 3.2% year on year. Travel app data shows that mobility in China and South Korea has recovered well without a significant rise in cases. Both countries appear to show, at least so far, that a recovery is possible without a vaccine if the virus can be brought under control with other measures. Chinese equities were up 8.7% over the month.

Conclusion

The policy response to Covid-19 from central banks and governments has been swift and sizeable and helped lift markets, as policymakers have aimed to build a bridge to the other side of the virus. However, a full economic recovery can only take place if rising activity doesn’t also lead to rising infections. Governments should therefore continue supporting consumer incomes and businesses until a vaccine is available or until the virus is brought under control by other means. The extent to which they do so will be key to the outlook from here. It appears progress is being made towards a potential vaccine, but it is too early to sound the all clear just yet. Given the high uncertainty around the outlook for the virus and a vaccine we continue to favour an up-in-quality approach across both stocks and bonds, along with a focus on valuations relative to fundamentals. Alternatives such as macro strategies may help diversify portfolios given the reduced diversification that government bonds are likely to provide at current yields. With the uncertain outlook so dictated by the virus, but also given the potential for a vaccine, we continue to believe it makes sense to aim for balanced and well-diversified portfolios.

Please continue to check our Blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.

Please keep safe and healthy.

Carl Mitchell – Dip PFS

IFA and Paraplanner

10/08/2020