Please see below an article published late yesterday by A.J. Bell, which looks back on the initial outlook for 2020, in contrast to what was experienced and what we might see in 2021:

Please continue to check our Blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.

Please see below an article recently published by Jason Pidcock, who is Head of Strategy on Asian Income at Jupiter, which outlines his thoughts on potential investment opportunities in a post-Covid world:

Please continue to check our Blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.

Please see below update received from Brooks Macdonald this afternoon, which comments on the markets’ reaction to political developments in the US as well as ongoing Brexit negotiations in the UK.

What has happened

After starting somewhat moodily, markets gradually recovered ultimately ending in positive territory with the US close. Whilst US Fiscal Stimulus pre-Christmas is still up for debate, constructive comments from the Republican Senate leadership helped support risk appetite.

US Stimulus

Senate Majority Leader McConnell urged both sides to set aside their top priority demands which had generated sticking points earlier in the year. Both parties are acknowledging that this is stage one of the negotiations with another package inevitable when the new administration enters the White House. It’s within that context that the narrative has shifted to ‘pass those things that we can agree on’ in the words of Mnuchin. Treasury Secretary Mnuchin presented a $918bn bill to House Speaker Pelosi so there is a suggestion that we are getting closer to a headline figure on the package. Below the surface there are quite a few differences however, including unemployment insurance where the bipartisan bill backed by Pelosi allocates $180bn with Mnuchin’s White House bill containing just $40bn. Markets have taken the language of compromise, backed by actions, positively however and this has been enough to shrug off the European risk with Brexit.

Brexit

The contentious provisions in the Internal Market Bill were withdrawn by the UK Government yesterday after an agreement in principle was reached around the Northern Ireland arrangements. This draft agreement is yet to be published but these talks, led on the UK side by Michael Gove, have been running in tandem to the main trade talks. This has removed a key point of contention between the EU and UK with the former suggesting that the provisions meant the UK could not be trusted. This improved backdrop is the context for UK PM Johnson to meet EC President von der Leyen over dinner tonight to discuss the Brexit impasse.

What does Brooks Macdonald think

Both sides have played down the odds of a deal and have sounded cautious without entirely snuffing out hope. Is this theatrics or managing expectations ahead of a dinner that shows ‘both sides tried’ – who knows. That said, yesterday was a positive day for Brexit developments as the dropping of the Internal Market Bill provisions (and promise not to include similar measures in the Taxation Bill) does suggest a continued softening of the UK’s position ahead of the crunch dinner tonight.

We will continue to monitor the markets’ performance as we edge closer to the end of the Brexit transition period on the 31st December. Please therefore, check in again with us soon.

Please see below for the latest key beliefs article from Legal and General’s Asset Allocation team, received by us late afternoon 07/12/2020:

Festive spirits

Markets don’t seem to be taking a holiday break yet. Last week, equities rose, the US dollar weakened, and rates and inflation climbed higher. It doesn’t look like we will be able to relax any time soon, either; the coming weeks could see the start of vaccine distributions, the Trump administration transferring power, the conclusion of Brexit’s game of ‘deal or no deal’, and potentially a fiscal deal in the US.

As with all Key Beliefs emails, this email represents solely the investment views of LGIM’s Asset Allocation team.

Could the last bull please switch off the lights?

Recent news on COVID-19 vaccines has generally been positive, but the immediate economic outlook remains challenging. Europe is already in a renewed contraction, following a significant increase in restrictions to get the virus under control. US economic data have held up well so far because restrictions had been relatively limited, but stricter measures are starting to be deployed amid a surge in cases.

Then there are the fading hopes for fiscal stimulus. US households are beginning to run out of savings from the income transfers received during the spring lockdown, while more unemployment benefits are set to expire at the end of this month. There are signs Congress is beginning to recognise this danger, and Friday’s weaker payrolls report was a clear warning as talks have resumed on passing some targeted measures in the $500-900 billion range. It is not clear a compromise can be reached in time for Christmas; failure to achieve one risks an outright contraction in activity over the festive period and a negative GDP print for the first quarter.

Does it matter? The outlook for 2021 is bullish and markets might be able to look through any weakness as temporary. The main headwind for markets at the moment is the very broad positive sentiment. Next year’s consensus outlooks are bullish and our sentiment indicators are exuberant. What could possibly go wrong?

We remain cautiously bullish for the medium term but tactically neutral. We will not chase the rally at this point, preferring to take our risk in relative-value trades.

Every hero needs a crisis

Central banks had no choice in either 2008 or March this year. The world needed to be saved from a financial meltdown and so they flushed liquidity into the world.

However, today’s monetary policy can contribute to tomorrow’s meltdown. Keeping interest rates low to provide a safety net for markets can induce corporations and households to take on more debt and more risk. This dynamic has also tended to stoke inequality, as asset prices have been boosted even though unemployment has spiked. Managed stability creates instability.

Global leverage has increased significantly this year, undoing much if not all of the deleveraging of recent years. In a normal world, increased leverage is often resolved by a credit crisis, massive defaults, forced liquidations, or massive inflation. But apparently this isn’t a normal world.

Most of the increase in debt during the pandemic has been in the public sector, and a large part of this has been absorbed by central banks via quantitative easing. This debt sits with central banks and is perpetually rolled over, effectively debt monetisation. Central banks could commit to never selling it or just write it off, which would improve debt-to-GDP ratios. Cancelling public debt like this is prohibited in some countries, due to the moral hazard it could create for politicians. For others, the only constraint is ultimately inflation.

But ballooning debt is also a symptom of other problems like weak productivity and inequality (encompassing poor health, low wage growth, and poor education). This could result in further political tensions and anti-globalisation, similar to the experience of the 1930s.

Given the current economic output gaps, we don’t see runaway inflation as a likely scenario but our head of economics does expect mildly higher inflation in the years to come. This would change if we saw continued broad global fiscal support financed by central banks.

Do you feel lucky?

Bitcoin reached a new all-time high last week. The crypto-currency has mostly seemed a private-investor phenomenon, but we have seen increased interest from institutions. There are many things for them to like: past returns have been stellar (an annualised return above 100% over the past five years); it has offered some diversifying properties with only a slight positive correlation with risk; and, contrary to many currencies, it has the attraction of limited supply at a time when central banks are printing money.

However, there are also plenty of downsides. Bitcoins have no intrinsic value (at least tulip bulbs could yield a beautiful flower); they are not widely recognised or regulated; it takes the energy of a medium-sized nation to mine a bitcoin so it isn’t very environmentally friendly; and it is very expensive and slow to use in day-to-day transactions.

The first is perhaps the most existential risk: at some point bitcoins could become worthless if a more popular or efficient alternative is found. Central banks could well develop their own crypto-currencies, especially if bitcoins and others become too big and interfere with efficient monetary policy.

It could easily be years before the next bitcoin selloff but we know how this story is likely to end. At the peak of the 17th century tulip trade in Amsterdam, those paying fortunes for a single bulb were surely speculators who understood that tulip prices had no link to bulbs’ intrinsic value and just hoped to sell them to someone else at an even higher price. Many were successful in the year before the crash in 1637; their quick gains were what drew in others and excited pundits. Does that sound familiar?

These articles provide concise well-informed views that cover the whole of the market and are useful to maintain your up to date view of the markets globally.

Please keep reading our blogs regularly to give yourself a holistic and up to date view of the markets.

Please see the below look back at 2020 from Jupiter Asset Management’s Chief Investment Officer:

Jupiter’s Chief Investment Officer reflects on the longer-term implications of a year most unlike any other.

In a year overwhelmingly dominated by the pandemic, it could be tempting to dwell on the challenges that have been presented to businesses and to global society.

Long before any of us had heard – let alone uttered – the words “COVID-19,” there was a trend towards more flexible working in many sectors of the economy, including in asset management. Some in our industry were embracing growing requests for more flexible working arrangements, while others may have viewed them with a certain degree of scepticism, pondering whether fund management was the kind of industry that could accommodate such arrangements at scale.

As much of the world went into lockdown, personal opinions on the merits and disadvantages of remote working became largely irrelevant; a significant policy decision that would, historically, have been the preserve of individual businesses was essentially taken for them.

Simultaneously, the important question as to whether a firm like ours could operate effectively with virtually all employees working remotely for a prolonged and potentially open-ended period was answered; we could, and we did. Indeed, a recent conversation with our head of dealing, Jason McAleer indicated that our industry as a whole has not only coped with the challenges presented, but has seen no perceptible increase in operational errors or issues.

In my view, the changes we have seen have the potential to make asset management a fundamentally more inclusive industry. Put simply, it now feels reasonable to hope that many of those who – for oft-cited reasons, including perceptions of long hours, punishing travel schedules and reconciling the demands of a challenging career with family life – might never have considered a career in fund management, will feel newly emboldened to take a closer look.

If, like me, you believe that more diverse investment teams are better performing ones, then this can only be a welcome development from the perspective of our clients.

Inclusivity leads to diversity

The pandemic and associated changes to working patterns and practices have also reminded us of the value of the office environment, as evidenced by numerous requests from colleagues for permission – which was generally denied, in line with the official guidance at the time – to continue to work from the office as the second UK-wide lockdown came into force.

This all begs a question: how quickly will the potential benefits of changes to working patterns in our sector filter through into the reality of the make-up of our workforce? Naturally, in a profession like fund management, hiring cycles are relatively lengthy. For this, there can be no apologies; the business of taking fiduciary responsibility of other people’s money is a serious one, and it is right that those charged with this duty should first have to prove their aptitude.

Of course, recruitment decisions are largely devolved to hiring managers; while this makes it difficult to “force” change in hiring practices from above, as CIO I am committed to continuing to challenge ourselves.

Changing behaviours: impact on markets and innovation

For a business like Jupiter, one of the more testing trends to emerge over the last year has been a tangible increase in direct participation in financial markets by retail investors. The exact cause of this change in behaviour is difficult to pinpoint, but we can reasonably speculate that it may have much to do with a combination of increased market volatility creating perceptions of attractive entry points, and the simple reality of the increase in available time many people have found in lockdown.

Whatever the cause, there is no doubt that such a sharp increase in activity in stock markets among individual retail investors has had an impact not only on stock prices, but also on liquidity and on sources of liquidity.

For asset managers, this potentially disruptive trend should act as something of a wake-up call; as retail investors in growing numbers show signs of exploring different ways to put their money to work, we must remain relevant, and continue to demonstrate that our products offer value.

As a firm, we place great emphasis on the importance of fostering innovation. A particularly exciting development for us in this regard was the formalisation earlier in the year of our strategic partnership with US-based NZS Capital, LLC (“NZS”), a highly innovative investment boutique which itself focuses on identifying disruptive businesses with the potential to generate favourable outcomes simultaneously for investors, customers, employees, society, and the global environment.

2020: when ESG became truly “mainstream”

Our partnership with NZS also serves as a timely reminder of our commitment to innovation and leadership in the field of ESG investing, a topic that has enjoyed a meteoric rise in prominence over the course of the last year. Indeed, I would be unsurprised if, in the future, social anthropologists looked back on 2020 as the year ESG investing became truly “mainstream.” This is an overwhelmingly positive development, and one to be embraced.

From a fund management perspective, I believe that ESG in the years ahead will be a refinement, evolution and re-categorisation of many of the assessments managers already make when looking at an investment case. How is a company run? Do its activities and/or products cause detriment to the environment? Are its employees mistreated or endangered? Does it mistreat its customers in a way that is detrimental to them and unlikely to build long-term loyalty? Has it taken on excessive leverage in pursuit of short-term shareholder returns that might undermine its longer-term viability? For us, these are not new questions, but they are being asked of us by a broader range of clients and other stakeholders, and with a frequency and determination not before seen.

Such focus on these issues is having a marked effect on markets, and on the way in which capital is being allocated to investment managers. This, in turn is undeniably changing and disrupting perceptions of the characteristics of a business most prized by investors.

The “what” and the “how” of asset management

I believe that the single most important thing we can do as a business is to generate strong and sustainable investment returns for our clients. As the end of every year approaches, we take the time to reflect on our performance; for a year that is likely to stand out in the collective memory for many of the “wrong” reasons, in this particular regard, 2020 has been a year much like any other.

The change, challenges and uncertainties we have all faced notwithstanding, it is pleasing to see that many of our strategies have performed very well throughout this period. Meanwhile, the new colleagues who joined Jupiter through our acquisition of Merian Global Investors have already made a significant contribution to Jupiter, bringing fresh energy, ideas, and perspectives to our debates.

But investment and performance are not the only things about which we hear from clients, who increasingly want to know how a firm like Jupiter manages its money managers. This is perhaps the most important part of the role of the CIO office, and it has been a privilege to speak with so many clients over the course of the year about how we seek to hold our fund managers to account. Put another way, it might be said that in 2020, what we seek to do (generate strong, sustainable investment performance), and how we go about it have become first among equals in the pecking order of clients’ priorities.

In truth, nobody knows how 2021 will play out. With the promise that vaccine programmes may be imminently deployed, a final end to the next chapter of Britain’s exit from the EU in sight, and a the potential for a more stable geopolitical scenario, it is tempting to look forward to the coming year with a great sense of optimism. At the same time, none of us must be under any illusion over the scale of the challenges facing the global economy as the world emerges from the pandemic. Whatever happens, our focus in the CIO office will be on seeking to ensure we deliver the best performance we can, in the most sustainable way we can; it is this pursuit, I believe, that gives us our real licence to operate.

As the end of every year approaches, reflections on the year we are about to leave behind tend to come naturally to everyone.

Look backs at the financial world and investment markets pour out from fund managers followed by outlooks, predictions, and goals for the year ahead.

2020 was a year that nobody could have predicted, and a year I’m sure nobody will look back fondly on.

One of the (positive) key points that can be taken away from this year (as demonstrated in the article above) is something we have been talking about for a while now, ESG is now mainstream.

It’s real, it’s important and it’s here to stay.

From firms and fund managers beginning their ESG journey, to the ones talking about how they already factor in a strong ESG process within their operations.

Whatever our industry takes away from this year, one thing is for sure, ESG is now firmly on everyone’s radar.

Please see below this week’s Monday Market Update from Blackfinch Investments – received today 07/12/2020.

Blackfinch Group – Monday Market Update

Issue 20 | 7th December, 2020

UK COMMENTARY

• The COVID-19 vaccine developed by Pfizer in conjunction with BioNTech was granted authorisation for use in the UK by regulators, with the first doses expected to be rolled out imminently • The FTSE 100 hit its highest level since March thanks to a solid performance in pharma, mining and energy stocks • House purchase mortgage approvals increased to 97,532 in October, from 92,091 in September, beating the forecast of 84,000, helped by the stamp duty holiday which has turbocharged the housing market • Nationwide house price index rose 0.9% in November from October. The year-on-year increased quickened to 6.5% from October’s 5.8%. • The UK was lifted out of ‘lockdown 2.0’ leading to many UK department stores experiencing a mini boom as shoppers rushed back through their doors. Meanwhile Arcadia group fell into administration, putting 13,000 jobs at risk. • Tesco surprised markets by deciding not to accept its £585m of business rates relief from the government. Many of its peers followed suit providing a c.£2bn saving to the public purse. • The manufacturing Purchasing Managers’ Index (PMI) rose to a 35-month high of 55.6 in November (revised up from the ‘flash’ reading of 55.2), up from 53.7 in October. PMI has now signalled expansion (i.e. above the 50.0 level) for six successive months. • PMI appears to have been boosted by the stockpiling of critical inputs and increased demand from the EU ahead of the UK-EU transition arrangement deadline on 31st December • Private new car registrations in November were 32.2% lower than in November 2019 caused by the second lockdown. They were up 0.6% year-on-year in October.

US COMMENTARY

• Both the Dow and S&P posted their best November returns since 1928 as hopes around vaccines and a stimulus package assisted sentiment • US jobless claims fell from 787,000 to 712,000 undershooting the 775,000 consensus estimate. Continuing claims also fell to 5.52m from 6.09m, lower than forecasts of 5.8m. However, 245,000 jobs were added in November compared 638,000 on the previous month and it was the fifth month in a row employment has fallen in the US. • This mixed jobs report added weight to the argument that further financial assistance and stimulus is needed to help the US economy • A bipartisan $900 billion relief package bill has been put forward but is it unlikely to get much support as too many discrepancies exist • Moderna has applied to the US Food and Drug Administration for emergency use authorisation for its COVID-19 vaccine

ASIA / AUSTRALIA COMMENTARY

• China’s Caixin manufacturing purchasing managers’ index (PMI) jumped to 54.9 in November, from 53.6 in October; the consensus forecast was for a reading of 53.5 • Australia’s economy expanded 3.3% quarter-on-quarter in September after a 7% quarter-on-quarter contraction in the June quarter

GLOBAL COMMENTARY

• The Organisation for Economic Cooperation and Development (OECD) now predicts that global Gross Domestic Product (GDP) will contract by 4.2% this year, which is an improvement on the previous forecast of -4.5%. At the same time, it lowered its 2021 forecast to 4.2% from 5%. • OPEC+ ministers agreed to withdraw previous output cuts by no more than 500,000 barrels a day each month, starting in January, with production hikes subject to review each month helping to push up oil prices

COVID-19 COMMENTARY

• In the UK, cases and hospitalisations continue to fall, with some of the hardest-hit parts of the country reporting a halving in new cases since the second national lockdown began on November 5th • The US reported 100,000 COVID-19 hospitalisations for the first time

Please continue to check back for our latest blog posts and updates.

Please see below an article received from Invesco this morning providing their latest market update:

As you can see from the above, many sectors had a positive week last week in terms of investment returns. The main losers appeared to be Government Bonds and some Investment Grade Bonds. Thursday could be a day to watch, with the U.S. Jobless report, the ECB meeting and UK economic activity indicators are all released.

We will continue to provide details on any announcements made on a deal or no deal scenario and what impact this could have on markets and investments.

It is important to remember, whatever happens, it is important to remain invested and focus on your long-term objectives.

Please continue to check our Blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.

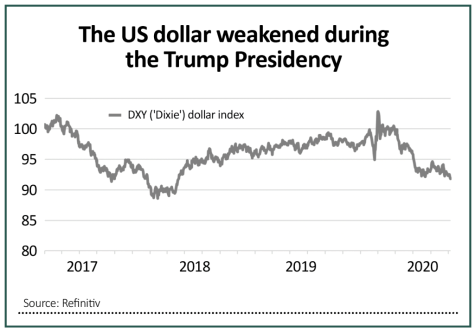

Please see below AJ Bell article received yesterday morning which provides a market commentary relating to the dollar’s 9% fall since Donald Trump’s inauguration on the 20th January 2017.

It wasn’t always easy to understand what US president Donald Trump wanted, but at least he was consistent about the dollar. He spent much of his four-year tenure in the White House complaining about how the greenback was too high and ultimately he got his way, even if he may have finally come around to the view in 2020 that a rising currency was a back-handed compliment from markets about the relative strength of the US economy.

The dollar has fallen 9% since his inauguration on 20 January 2017, using the trade-weighted basket of currencies that makes up the DXY (or ‘Dixie’) index as a guide, and now trades at a two-and-a-half-year low.

A loss of value in the globe’s reserve currency, and a major haven asset, has potential implications for a range of markets, and not just foreign exchange.

Gloomy greenback

There are multiple possible reasons for the buck’s case of the blues. First, the president regularly railed against the US Federal Reserve’s monetary policy, arguing that chair Jay Powell and the Federal Open Markets Committee were running it too tight.

Whether they listened to the president, heeded stress in the financial markets in autumn 2019 or took other data on board, Powell and colleagues had begun to push through interest rate cuts even before the global pandemic pulled the rug from under the US economy in 2020.

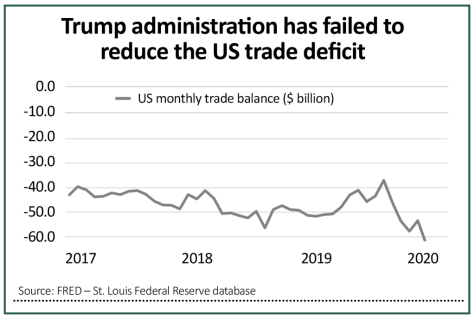

Second, the president’s trade war with China unsettled markets and seemed to bring no great economic benefit. The US trade deficit has surged back toward its all-time high, with the result that dollars are flowing out of America to pay for the overseas-produced goods that consumers are sucking into the country.

In some ways this can be seen as a good sign. In 1960, economist Robert Triffin argued that America would always have to run a trade deficit, and hand out more than dollars than it received, to ensure the world had enough of the reserve currency to go around.

The alternative would be a painful liquidity squeeze on the globe’s economy and financial markets alike as dollars flooded home.

Third, the markets’ latest round of optimism that the pandemic may soon be over and a global economic recovery underway, following the vaccine announcements from Pfizer-BioNTech, Moderna, and AstraZeneca and the University of Oxford, means that perceived havens such as the dollar are less in demand.

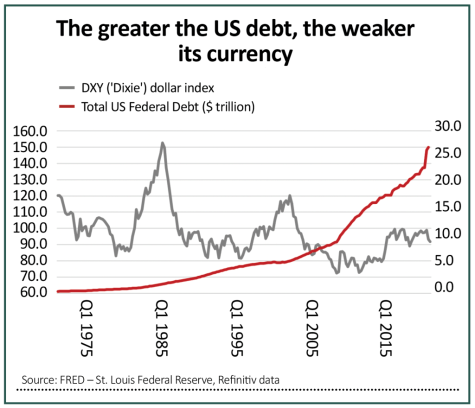

Finally, and perhaps most fundamentally, Trump oversaw a huge increase in the Federal deficit. When he took office America’s national debt was $18.9 trillion. It began to surge even before the pandemic and has soared in its wake to $27 trillion. Although Republicans and Democrats have failed to agree upon another round fiscal stimulus, the debate centres on the degree of further borrowing, not whether there should be further debt creation or not.

This argument is not unique to America – something which may be sparing the dollar a few more blushes – but it will surely continue a trend of ever-higher government debt ceilings.

That dates to the early 1970s, when Richard Nixon took America off the gold standard so he could pay for welfare programmes and the Vietnam War, but the trend is clearly accelerating.

Remember that Moody’s downgrade of America’s credit rating, and summer of turmoil in financial markets, came after 2013’s debt ceiling suspension, when the limit was $16.7 trillion. It had taken America 237 years to get there but Uncle Sam has taken just seven years to overspend by a further $9.3 trillion.

Road to ruin

Anyone who takes the view that American debt is not a sustainable path will be wary of the dollar.

Anyone who feels that Covid-19 can be contained, and the world builds a reliable recovery, will also fight shy of the buck. Triffin’s theories imply that a weak dollar is the natural result of a strong US economy and robust global trade flows – both of which would logically benefit emerging markets and commodities, asset classes that traditionally do well when the dollar is weak.

The dollar is likely to hang tough for a while yet, not least as suitable candidates to replace it as the world’s reserve currency are in short supply.

China’s renminbi is not fully convertible, a return to gold will impose disciplines which no politician or central banker will accept (or can afford) and cryptocurrencies do not have universal acceptance.

But any attempt to reset currencies and debts could yet be spearheaded by central bank-backed digital currencies, a trend which must be closely watched.

We will keep an eye out for updates on the value of currency as the new President-elect, Joe Biden, takes office in January 2021. Please check in again with us soon.

Investment Management House Janus Henderson recently published some thought pieces on ESG and Socially Responsible Investing. Please see the key takeaways from these pieces below:

Sustainable equities: the future is green and digital

The pandemic has accelerated investment into digitalisation, which we consider to be a key enabler of sustainability.

We expect support for sustainable development to gain momentum as countries embrace the need to be low carbon and as Joe Biden takes his seat in the White House.

Investment into electric vehicles is expected to surge in 2021 as innovators ‘race’ to the top.

Sustainable design in consumer products

The apparel sector is well known for its detrimental effects on the environment. However, as consumers become more aware of their own environmental footprints, there has been a surge in demand for sustainable goods.

A circular economy is based on the principles of designing out waste and pollution, keeping products and materials in use, and regenerating natural systems.

Companies including Nike, Adidas and DS Smith have incorporated a circular approach to the design and production of their goods, creating durable and long-lasting products with a reduced environmental footprint.

Investing in Diversity: analysing the investment risks and opportunities

Companies are increasingly being held accountable by consumers who reward brands aligned with their values.

For many global businesses, matters of diversity and inclusion go beyond the workplace, and efforts are made to address discrimination in the countries in which they operate.

Investors should be wary of companies that fail to futureproof themselves in terms of diversity. Socially conscious brands that make inclusivity a central part of their business strategy and brand ethos are more likely to succeed.

What gets measured, gets improved. Investors should focus on company disclosure, diversity-related targets, and meaningful initiatives in place. A list of suggested investor questions can be found at the end of this paper.

Janus Henderson are ahead of the game with ESG policies and started factoring this in back in 1991 shortly following the 1987 United Nations Report, ‘Our Common Future’ which I mentioned recently in an ESG blog. Their philosophy is below;

‘We believe there is a strong link between sustainable development, innovation and long term compounding growth.

Our investment framework seeks to invest in companies that have a positive impact on the environment and society, while at the same time helping us stay on the right side of disruption.

We believe this approach will provide clients with a persistent return source, deliver future compound growth and help mitigate downside risk.’

As I wrote about in our blog, as a firm we undertake regular due diligence with regards to the investments we recommend to our clients. This an ongoing process and we are constantly monitoring the market, and this year ESG has become a key factor in what we look for in the due diligence process.

Of course, many businesses may have a broad and generic ESG statement, but having a strong and well defined ESG process embedded into a businesses culture and investment process is definitely one of our key determining factors in the companies we choose to recommend.

We start off with an investment houses ESG statement, but then we dig deeper, to make sure these investments do exactly what they say they do, in terms of ESG, then factor this into the rest of our research i.e. investment returns, track records, cost etc.

It’s good to see so many investment houses now openly talking about and promoting ESG and demonstrating their views and philosophies.

Now could be a great time to invest whilst asset prices are still generally low, all whilst taking a responsible approach to investing!

As always, keep checking back for a variety of blog content from a wide range of investment houses, fund managers and our own original pieces.

Please see the below 2021 Outlook from Legal & General:

Foreword: A fresh start

Despite the ongoing challenges, we see next year as a time for healing – for the economy, environment and society.

After contending with the terrible human and economic toll of a pandemic, as well as market volatility reminiscent of the financial crisis, investors could well be forgiven for wondering anxiously: what could 2021 possibly have in store for us?

We cannot, of course, predict the outcome of risk events already on the horizon, let alone identify any black swans fluttering menacingly. But based on our research and the available information, we can sketch out the contours of next year’s macro and market landscape. Pleasingly, we believe it is one in which investors can thrive, albeit with the right approach.

In this outlook, we offer views from across LGIM that inform this optimism, grounded in our assessment that even though the world economy’s immediate prospects may have darkened, 2021 could still be a strong year for growth. Other key points include:

• The bull case for equities at this point in the cycle

• How a Biden administration could create ripples in the bond market

• The role of cashflow-driven investing in tackling market gyrations

• Why 2021 could be a pivotal year for battery technology and renewable power

• How China’s financial sector is opening up potential opportunities for investors

As we noted in our autumn update, COVID-19 has accelerated a number of long-term investment themes that were previously underway. The global energy transition is an obvious example, as the shock of coronavirus has focused attention on the looming threat of climate change just as it has shaken up carbonintensive industries.

At the same time, environmental regulations are likely to tighten under the incoming US administration, whose climate policies will have a worldwide impact. The changing of the guard in Washington, meanwhile, brings us to another long-term trend: populism.

While Donald Trump lost the 2020 US election, the result was not a repudiation of everything he stood for. We will need to continue monitoring the way our politics have changed forever as a result of the forces that propelled the outgoing president, and other populists around the world, to power and sustained them in office.

It’s also clear that many Americans continue to view China unfavourably, despite the election result, with the uneasy relationship between the world’s two largest economies likely to be a key driver of geopolitics for the foreseeable future.

In Europe, even though a UK-EU trade deal now looks probable, much else remains to be decided after the Brexit transition period ends. Expect the UK’s long divorce from the bloc never to stray too far from the headlines, or the radar of investors, next year.

And while we look forward to a post-pandemic world, we are still living with coronavirus and the dramatic steps taken to contain it. As such, expect further debates over fresh monetary and fiscal stimulus to be a prominent feature of the coming months – even as we contemplate the ultimate cost of such measures.

Despite these challenges, we see next year as a time for healing – for the economy, environment and society – in which we can play an important role on our clients’ behalf, by seeking to create a better future through responsible investing.

Sonja Laud

Chief Investment Officer

Economics: Unlocking growth

The immediate economic outlook may have darkened, but there are reasons to believe 2021 could be a strong year for global growth.

The primary downside risk we saw for the economy – further waves of COVID-19 leading to renewed lockdowns – has sadly materialised across many parts of the northern hemisphere. While we don’t expect the impact on the economy to be as severe as it was during the spring, the measures taken by European governments during the autumn and winter are likely to lead to another significant fall in output following the strong summer rebound.

The US has been slower to respond and, as pressures build on hospitals, the approach taken to tackle the virus across different states is likely to toughen.

The US probably has sufficient momentum into November to avoid an outright contraction in the fourth quarter, but the holiday season will now be far from normal.

After rapid progress to reduce unemployment, the improvement in the labour market could stall or even reverse heading into 2021. The US election outcome, discussed by Jason on page 8, has reduced the chance of a radical shift to sustained fiscal expansion, but we still expect some additional support to emerge in the coming months in response to the deteriorating virus news.

Vaccine change

Offsetting the gloom are several positive developments. First, China has largely eradicated the virus and so has a much greater chance of successfully deploying track, trace and testing programmes to prevent future outbreaks. Second, we have seen how quickly activity can recover once restrictions are eased. But most crucially, progress on developing safe and effective vaccines has continued, bringing forward a potential return to normality – or something approaching that condition – by one or two quarters.

We still await more comprehensive data, and there will be logistical and public-relations battles ahead before the world can reach herd immunity – or at least reduce the threat of the virus – to allow most people to resume normal activity.

Yet although the precise timeline remains uncertain, we expect more widespread distribution of vaccines to begin in the spring. As restrictions ease from the winter and confidence builds that the end is in sight, activity could rebound strongly through the course of 2021.

Aiding the recovery will be exceptionally loose monetary policy as central banks focus on preventing inflation from dipping further below target. There is also an understanding from fiscal authorities that next year is not the time to address the large budget deficits caused by the response to the pandemic.

Bringing all this together, our central view expects global GDP to finish 2021 around 3% below its pre-virus trend, but there remains huge uncertainty around this outcome, with risks skewed to the downside should a vaccine be delayed.

Beyond this horizon, there is a concern the pandemic is causing lasting economic damage through capital stock obsolescence and belief scarring, which leads to increased saving and caution around future investment. However, it is also possible to see the potential for creative destruction and increased dynamism, accelerating change and boosting productivity.

Tim Drayson Head of Economics

Asset allocation: The year of hope

We believe the economic outlook is positive for equities, but investors will probably need to think carefully about their allocations to fixed income.

My takeaway from Tim’s economic outlook is that 2021 will be the year of hope. The fundamental backdrop he describes should boost equity markets in particular as investors start to see a potential end to the economic and social hardship of the past year.

But this isn’t just about optimism. We are only early in the economic cycle, with a meaningful output gap that can still be closed, while recession risk is low and there are limited inflationary pressures. Risk-adjusted equity returns from this point in the cycle have historically been strong.

Valuations are not a troubling headwind either. Equities may look expensive in absolute terms, but on a relative basis the equity risk premium – the equity earnings yield minus bond yields – remains attractive, in our view.

All things considered, our base case would therefore be that equities are among the best-performing asset class in 2021; we would not be surprised to see double-digit returns.

One point to note is that we are obviously not alone in this view. Sentiment has turned bullish for the first time since the pandemic, and at some point in 2021 it is very likely that markets will price in too much optimism. For now, though, we think this is too early to be a dominant factor.

We continue to believe in our ‘lower for longer’ theme in fixed income, seeing limited upside potential for bond yields from their current levels. We expect inflation dynamics will become more important than growth dynamics in determining bond yields once we get past the recession phase. That has been true for the past four cycles, but should be even more important now that the Federal Reserve (Fed) has indicated it will not react pre-emptively.

That should mean positive news on the vaccine rollout is unlikely to be enough to put sustained upward pressure on bond yields. We will also need evidence that inflation is moving sustainably above 2%, which is very unlikely to happen in 2021 with unemployment still extremely high.

On the corporate side, investment-grade credit is in our view less attractive than other risky assets like equities, given the compression in spreads seen since March. Today’s tight spreads are partly a reflection of subdued corporate bond defaults thanks to fiscal support, cheap financing and the prospect of a vaccine in 2021.

Returns from credit do not typically accrue evenly; instead, and perhaps understandably, they tend to be higher when starting spreads are wider. That suggests to us there is potential value in having space in portfolios to add significantly to credit in extreme selloffs. Admittedly, that comes at a cost – namely the returns given up by patiently waiting for a better entry point – but we believe it’s the right framework for thinking dynamically about credit for the medium term.

A low yield environment provides challenges for investors both from a return and a risk mitigation perspective. Though there is no single panacea, one of the measures we believe investors can take is to look at smaller, non-traditional fixed income markets to find better risk-off hedges. Smaller rates markets with higher yields that could still fall become more interesting and important, for example. At the time of writing in mid- November, these include South Korea 10-year bonds yielding over 1.5% and Australian 30-year yields over 1.8%.

Emiel van den Heiligenberg Head of Asset Allocation

US politics and policy: Biden, bonds and the limits of presidential power

Despite its limited room for manoeuvre, we expect the Biden administration to make some ripples in the fixed income market.

Somewhat lost in all of the noise surrounding the 2020 presidential election is the fact that control of the Senate remains undecided: in order to reclaim the upper chamber of Congress, the Democrats need to win both Georgia seats in a runoff election on 5 January.

Betting markets imply about a 30% chance of this happening, as at the time of writing. Yet even if the Democrats do succeed in Georgia, it would be difficult to characterise this victory as looking anything like the ‘Blue Wave’ outcome expected before the November election.

Democrats look to have lost about 10 seats in the House of Representatives, which means Speaker Nancy Pelosi will operate with the slimmest margin in that body for 20 years. A 50-50 split in the Senate could be even more difficult to navigate, particularly as Senator Joe Manchin (D-WV) has expressed opposition to ending the filibuster – a tool to delay legislation and appointees. As such, President-elect Joe Biden’s agenda will likely need to be scaled back significantly.

That said, the last two years of the current administration have demonstrated the power of executive orders to circumvent Congress. A newly elected President Biden will probably use the same tools to tackle immigration, trade, energy and housing policy.

And yet there are likely to be legal setbacks along the way, much as President Trump encountered. Consider energy: while rejoining the Paris Climate Accord should be relatively straightforward, the President-elect’s plans for a green energy policy could hit considerable resistance in courts, where the previous administration was able to appoint more conservative judges.

Biden’s signature agenda items – taxes, healthcare and infrastructure – will face even longer odds. Without being able to circumvent the Senate filibuster, it will be nearly impossible to reverse the Trump tax cuts. As a result, corporate and personal tax rates will stay at current levels at least until 2022, which will in turn lower the likelihood of an expansive infrastructure deal.

Lower for even longer

Meanwhile, it is quite likely that components of the Affordable Care Act (ACA) will be found unconstitutional by the Supreme Court and require legislative fixes. Rather than expanding the ACA as he would like, the new president may find himself fighting to preserve the existing platform.

For bond markets, the failure of the Blue Wave to materialise decreases the likelihood of an imminent shift away from the theme of lower for longer, as less expansive fiscal policy implies there will be less upward pressure on interest rates.

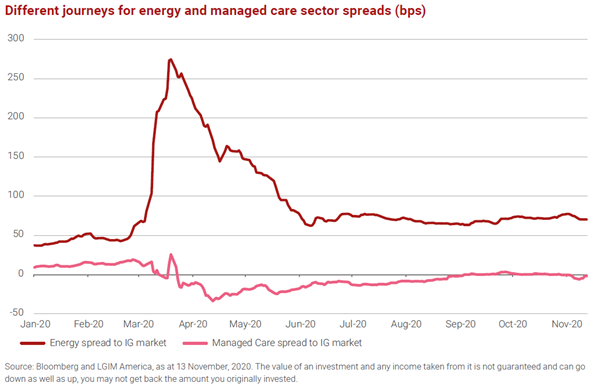

There are equally important implications at the sector level for corporate credit. While US energy companies will remain in focus as investors increasingly consider ESG themes, the pressure on the industry is likely to be less acute with the control of government more divided.

The risks around a wholesale change to the healthcare reimbursement ecosystem seem to have waned, meanwhile, but the managed care and pharmaceutical sectors could yet face headwinds even if they are less severe than previously anticipated.

In short, we believe 2021 is shaping up to be a year of opportunities for fixed income investors, where the policy backdrop will probably remain supportive and the Biden administration will make some ripples in the market – despite the President-elect’s limited room for manoeuvre.

Jason Shoup Head of Global Credit Strategy, LGIMA Fixed Income

Energy: Batteries charge up the renewable agenda

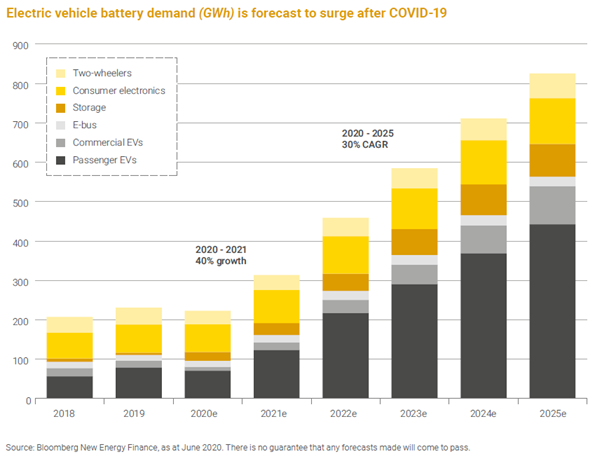

We believe battery technology is the key to unlocking the potential of renewable power, and 2021 could be a pivotal year for this market.

220 years have passed since Alessandro Volta paired copper and zinc discs separated by a layer of cardboard and salted water. Now, thanks to some recent breakthroughs, the battery technology market is again in an early growth phase, ready to power the next technological revolution in 2021 and beyond.

Of course, battery technology has not been static through those two centuries, as is evident from how electronic devices have become ever smaller and able to go for longer without charging.

But two events late in 2020 really electrified the industry: Tesla’s admission to the S&P 500, and the UK’s plan to ban the sale of new cars fuelled solely by petrol or diesel from 2030.

Epitomised by the rise of Tesla, a company that we believe should be recognised as much for its battery innovation as its car design, these welcome steps illustrate how investors can focus on batteries principally as an element of the electric-vehicle revolution.

That market, however, is only part of the role batteries will play in helping the world move to a less carbon-intensive economy. We believe they will also be vital in harnessing the potential of renewable energy.

Charging at windmills

Fossil fuels have accounted for most of the world’s mix of power generation since the 1970s, but according to BloombergNEF, renewables are now poised to take the lead. Wind and solar technologies alone are expected to provide 48% of all our electricity by 2050.

This progress is both exciting and essential, but the utility of clean energy will be limited without better and more extensive battery storage. Improved energy storage can help overcome the short-term intermittency – due to daylight hours or fluctuating weather – of renewable sources. Without an upgraded storage infrastructure, much of the electricity that could potentially be generated by renewables will be lost, and coal and gas-fired power stations will remain necessary to cover supply shortfalls.

Electric vehicle battery demand (GWh) is forecast to surge after COVID-19 Encouragingly, 2021 should be a marquee year for storage capacity. The world’s largest new battery installation was completed near San Diego in August, and we expect that record to be broken again next year. For example, the new San Diego plant has a capacity of 250 megawatts (each megawatt can serve an estimated 750 homes). Another new project just south of San Francisco will provide 400 megawatts of storage when completed in 2021.

Maintaining this trajectory of progress, underpinned by the advances made in battery technology, will be critical in achieving the energy transition necessary to avert the climate emergency.

Aanand Venkatramanan Head of ETF Investment Strategies

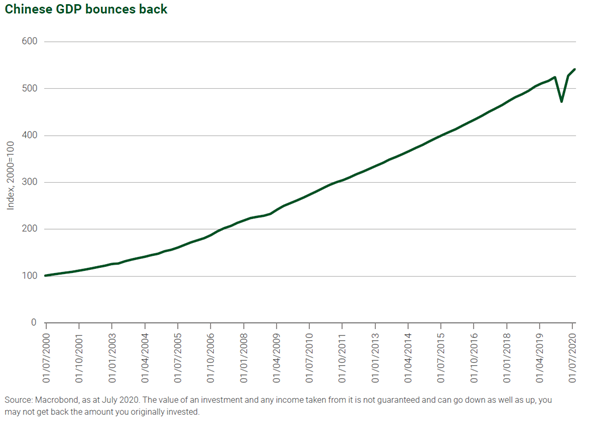

Letter from Hong Kong: Meanwhile, in China…

China’s financial sector is clearly growing more dynamic, opening up significant opportunities for international investors, in our view.

While global investors have understandably focused on the US election, virus waves and a potential vaccine, seismic events have also been occurring in the world’s second largest economy with similarly significant implications.

First, it’s easy to underplay just how successful the country has been at controlling the virus and returning to pre-pandemic economic output. The benefits of an efficient track-and-trace system are obvious. And by getting back on its feet quickly, China has avoided much of the sustained unemployment and defaults that will scar Western economies for years to come.

The cost is government control of private data. But for now, economic practicalities dominate such concerns and, in our view, China is well placed to be a relative winner from this crisis.

The technology sector has been another pandemic winner, but the second key event in China has been the regulatory focus on its domestic players. Clearly, the country has some extremely successful technology companies, with Alibaba recently announcing that Singles Day sales totalled 498.2 billion yuan, an increase of 26% versus last year.

But Alibaba’s founder Jack Ma publicly criticised Chinese regulators for holding back technological innovation, with an investigation and suspension of Ant Group’s impending IPO quickly following, ultimately causing the roughly $35 billion capital raise to be postponed. This doesn’t look like an isolated incident, with China announcing a set of draft rules against the broader monopolistic behaviour of its technology sector. A motivation for such intervention is to protect consumers and nip fintech systemic risks in the bud.

Constrained expansion

Does this spell the end for the Chinese technology boom? Certainly not if you believe the latest plenum of China’s Communist Party, which declared that self-reliance in science and technology is a strategic pillar of national development.

Perhaps the unconstrained expansion is over. But even constrained growth is attractive in a country expanding much faster than Western economies, so many investors could see recent market volatility as potentially an opportunity to add exposure.

The final key event is actually more of an ongoing trend, arguably even more important than the first two. This is the opening up of domestic Chinese financial markets; the internationalisation of the renminbi; and the introduction of risk into previously ‘bullet-proof’ investments, such as dominant property developers and bonds issued by state-controlled entities.

The direction is clearly towards a more dynamic financial sector, with significant opportunities for international investors. Here, the result of the US election will be influential, as the new administration will have to decide how much to push against China’s globalisation and how much to embrace it.

Once a COVID-19 vaccine has been successfully deployed, perhaps we can also remember 2020 for this hugely important development, which will be the topic of future Letters from Hong Kong.

Ben Bennett Head of Investment Strategy and Research

Please continue to check our Blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.

The 2021 forecasts are all starting to be released now – expect more to follow.

This year has been an interesting year (to say the least), now we just have to hold onto our seats and see what next year will bring!