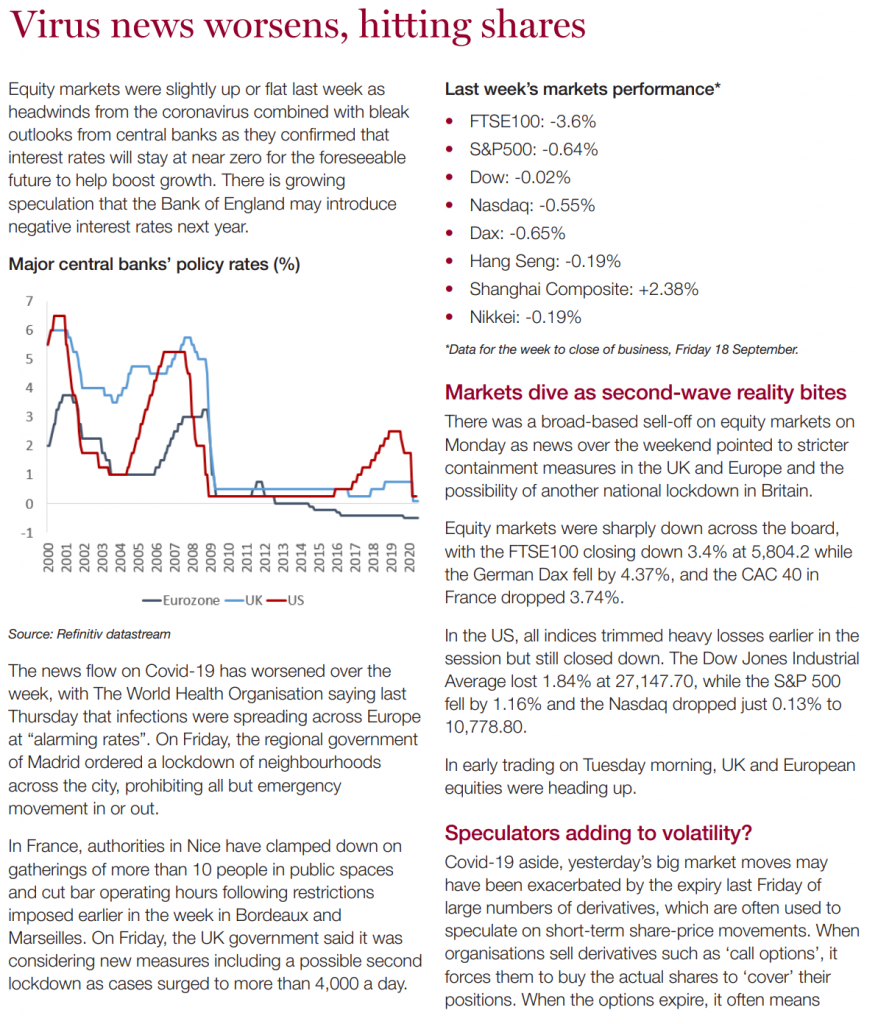

Please see below the latest market insight from Karen Ward at JP Morgan, with particular reference to the ongoing complexities of Brexit.

An American colleague joined me on a call recently and was perplexed by the fact that I was talking about Brexit. “Isn’t Brexit done?”, he asked me. Alas, no. While the UK did officially leave the EU on 31 January, for the economy nothing actually changed since the UK entered into an 11-month period of transition. During this period, the UK and EU were supposed to agree on a future trade arrangement to commence on 1 January 2021. The clock is well and truly ticking.

Negotiations are proceeding slowly and significant differences still remain. At the root of the problem is the same issue that has plagued the discussion for the last four years. The UK wants to regain control – to become fully sovereign – setting its own rules and regulations overseen by British courts. However, the EU is not willing to grant significant access to the single market without guarantees that standards will not be undercut to gain competitive advantage.

So what happens next? Either the next six months will see a breakthrough and a free trade agreement (FTA) will be established or the UK will leave and trade on World Trade Organisation (WTO) terms.

Trading on WTO terms has been used synonymously with ‘hard Brexit’. What exactly does that mean? The short answer is potential tariffs, more customs paperwork for businesses that trade with the EU and potentially the need for the UK to be removed from EU supply chains if regulatory conformity cannot be guaranteed. It is these nontariff barriers that we would expect to have the most economic impact. There could also be significant ramifications for financial firms since the UK would lose its passporting rights – its ability to serve EU clients from the UK. Advocates for a hard Brexit argue that a clean break would allow the UK more flexibility in negotiating future trade deals with other trading partners, although any benefit from these agreements would still only be seen once these trade deals had been implemented, which is often a lengthy process.

What will happen and what will be the implications for markets? In our view, the announcement of a comprehensive FTA might see sterling rise to 1.45 against the US dollar. By contrast, in a no-trade deal scenario we see sterling closer to 1.10 against the dollar. Much weaker sterling would partially help the UK to cope with new trade frictions.

Our central expectation is that despite ongoing near-term sabre-rattling, by year end pragmatism will prevail and a relatively narrow trade deal will be agreed. When ‘Brexit’ was added to the English dictionary, the word ‘fudgery’ should also have been included.

We expect a significant amount of ‘fudgery’ in order to get a partial trade agreement done. This may, in fact, involve highlevel agreements that disguise what is essentially a transition to iron out the finer details. Such a narrow trade deal will likely still be disruptive to economic activity in the EU and the UK over the long term. But we expect various arrangements to ease the near-term burden of the change for both sides. We expect that both sides will want to minimise the day 1 disruptions given the extent to which both economies are still struggling to overcome the Covid-19 recession. Therefore, changes may well be phased in over time, spreading the economic cost over a number of quarters if not years. The UK could thus claim the sovereignty to set their own rules and standards without initially making substantial disruptive changes.

While this outcome is our central expectation, there are significant risks around it that investors should be mindful of. Sterling may be particularly volatile and, with almost 80% of revenues coming from abroad for the FTSE 100, this will also have implications for the stock market, since higher sterling could put downward pressure on earnings and vice versa should sterling fall, all other things being equal. However, we caution against relying too heavily on the FTSE rallying in the event of a hard Brexit as a disorderly Brexit would be likely to impact both UK and EU activity negatively, depressing some of the overseas earnings that matter to UK companies.

We will continue to provide the most up to date information on the markets and economy. Please check in with us again soon.

Stay safe.

Chloe

24/09/2020

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}