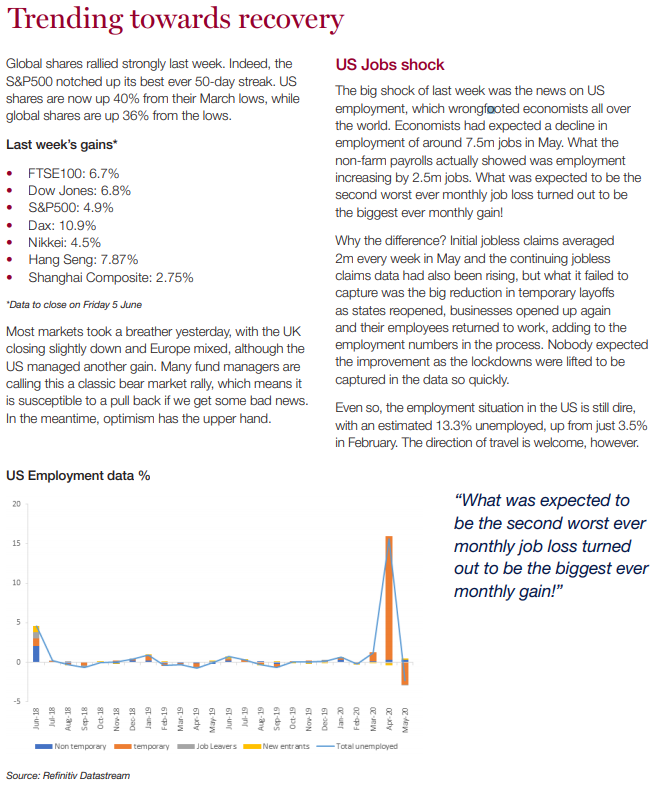

Please see the below article posted by AJ Bell on 11/06/2020.

What the pandemic meant for moving house and what could be in store

The coronavirus crisis has had an unprecedented impact on the UK property market, as viewings and sales ground to a halt and the market stalled during lockdown.

Activity is now starting to resume, but at a slow pace and with a number of big changes that househunters and sellers will have to adapt to. So what does that means if you’re trying to buy a property or sell your pad?

What Happened During Lockdown?

The property market effectively stopped during lockdown. No-one was allowed to carry out viewings of properties as it would have breached lockdown rules. Some estate agents came up with video tours of houses, but who was likely to make the biggest purchase of their life just based on a video?

What’s more, removal companies were not meant to operate, so actually moving house was tricky – although there were some exceptions if you were moving into an empty property.

What’s more, during this time mortgage companies started pulling their products. It meant that only those who had the highest loan-to-value, so the largest deposits, were able to get new mortgages.

Mortgage companies said they were overwhelmed with work and facing staff shortages so needed to reduce new customer numbers, meaning they restricted their new loans to just the highest-quality ones – so those people borrowing relatively less compared to the value of the property.

What About Now?

Viewings can happen in properties now, so long as they stick to strict guidance. Estate agents are advised to offer virtual viewings as a first step, which is either a video tour where the estate agent is live in the house, or a pre-recorded video of a walk-through of the property.

The Government advises that in-person viewings should only be carried out by buyers who are already strongly considering putting an offer in.

In-person viewings will have to follow social distancing guidelines and it’s advised that the homeowners leave the property while the viewing happens. Afterwards the house should be cleaned.

Two big changes are that open houses aren’t allowed and estate agents are not allowed to drive potential buyers to viewings – which could present some problems if you’re searching outside your home area and don’t have your own transport.

If you were ready to move before the crisis struck you can now also move, as removal companies have resumed their work. The advice is to do as much of the packing yourself as possible, and when moving day arrives make sure the movers can wash their hands and open internal doors for them so they don’t have to.

If anyone in the household has coronavirus symptoms or is self-isolating then the move should be delayed.

The mortgage market has also improved, with providers offering more products now. This means if you have a smaller deposit you’ll likely have more options now than you would have done a month or so ago.

What About House Prices?

You’d need a crystal ball to be able to tell what’s going to happen to house prices. The Government has an official measure of house prices, which tracks the direction their moving in.

However, it has suspended the measure as it says there isn’t enough reliable data to generate the figures – this is because so few house moves happened in March and April and the market hasn’t fully resumed yet, so the data would be based on a small sample size.

Nationwide, which has data of its customers (so only includes mortgaged purchases and no cash-buyers), says house prices fell 1.7% in May when compared to April – representing the largest fall in its data in 11 years. However, the sample size of this is likely to be even smaller than usual, so it’s difficult to know if it’s a reliable measure.

Stamp Duty Refund Deadline Extended

People who have paid higher stamp duty after buying a new property before selling their existing one will now have longer to sell their original home in order to claim a stamp duty refund.

Homeowners who buy their next property before offloading their current home pay additional stamp duty, as though they are buying a second property.

This means they’ll pay a three percentage point surcharge on the purchase, which can easily run into the tens of thousands of pounds. Ordinarily if they sell their original property within three years they can reclaim the additional stamp duty from HMRC.

However, the Government has now extended this three-year period if your home sale has been affected by the Covid-19 crisis.

It means anyone who bought their home from 1 January 2017 onwards will have longer than three years to sell it and get the refund, assuming they can prove the coronavirus crisis was the reason for the delay in the sale. Find out more information here.

The logic behind house prices falls is that fewer people might move as their income is more precarious and fears about the wider economy mean people are less likely to pay top whack for a property.

In contrast, the property search portal RightMove (RMV) said it had its busiest ever day towards the end of May, with 6m visits to the site – up 18% on the same time the previous year. The site also said there was an increase in calls and emails to estate agents – showing that at least some of the demand isn’t just bored people on lockdown browsing property listings.

There’s some expectation that with people having spent more time in their homes they’ve realised they need to upsize or get a bigger garden, for example, or they want to live in a new area. There may also be some pent-up demand from the market having halted for seven weeks in lockdown.

The Pandemic ground the housing market to an unprecedented halt causing issues for the industry and people looking to buy or sell their property! As the article explains, activity is starting to resume now, albeit socially distant activity.

If you are looking to move, make sure you keep up to date with developments in the housing market and continue to follow government guidelines.

Andrew Lloyd

12/06/2020