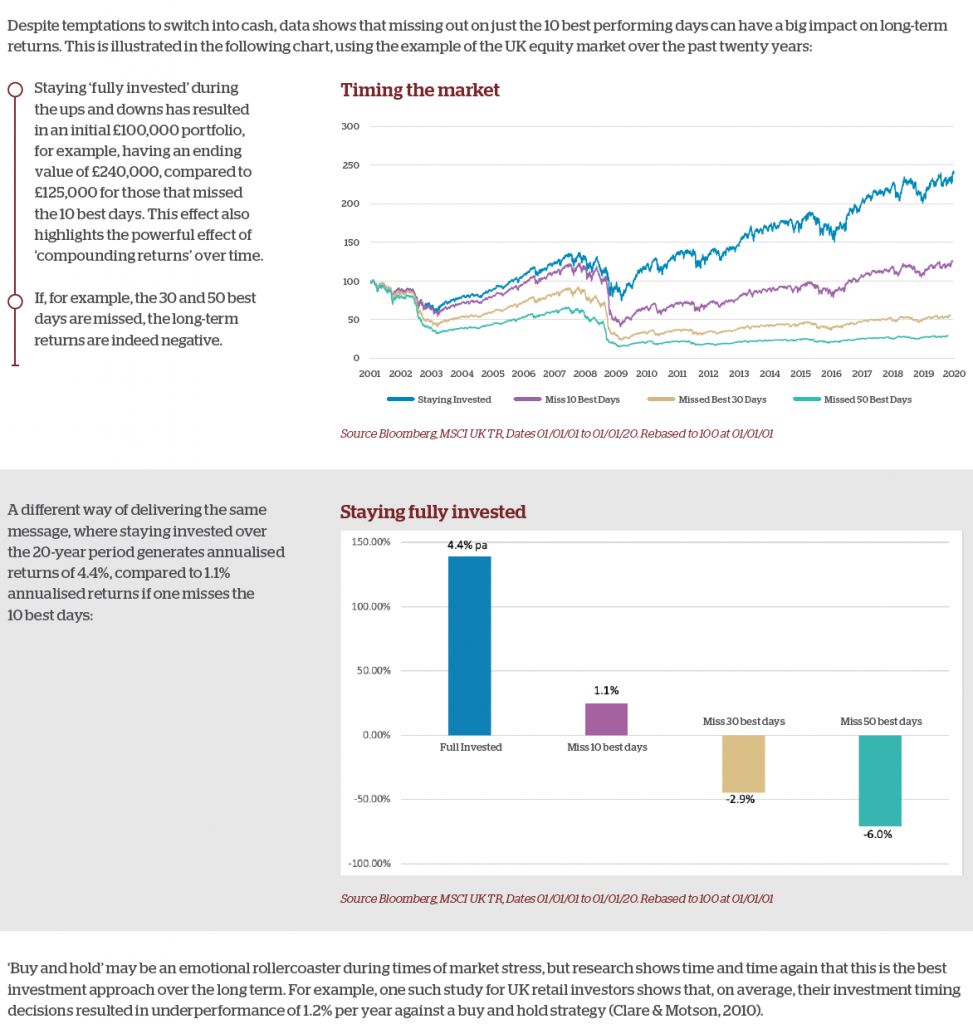

Received by email today 11/05/2020 concerning potential investor concerns. SEI explore what markets suggest the potential recovery paths could be.

The Shape of the Recovery: V, W or L? Looking Beyond the Letters

- It’s challenging to make accurate economic calls under normal circumstances

- Add in the uncertainty around oil prices, interest rates and epidemiological models and there’s a serious lack of clarity about the future

- While we believe that another significant pullback is likely, we also believe that long-term investors will be rewarded for their patience

Major economic setbacks can trigger a complex reordering of entire industries. Our current predicament has gone even further, forcing society to function under challenging conditions with consequences for every corner of the economy.

It’s challenging to make accurate economic calls even under more normal circumstances. Add in the direct and knock-on impacts of lockdowns, the range of potential paths that the COVID-19 outbreak could take, and the countless combinations of business and policy responses under each of these scenarios, and it is truly anyone’s guess what the future holds.

Why, then, do we try to distil these setbacks into simple shapes? Because humans—and financial markets— don’t like uncertainty. Despite that, guessing whether a recession and the ensuing recovery will look like a U, V or W provides minimal benefit to long-term investors. Focusing on the underlying fundamentals and economics, we believe, is more useful for framing investment decisions.

Searching for Clues

What do markets themselves suggest about the road ahead? A glance at the path of oil prices over the last few months certainly doesn’t project confidence for a strong rebound. The West Texas Intermediate oil price turned negative—a first—as its May 2020 contract neared expiration, and the June contract slid to between $10 and $20 per barrel at the end of April.

Low (and negative) prices imply that storage capacity has gotten full as demand plummeted during lockdown. The U.S. Energy Information Administration’s (EIA) April 2020 Short-Term Energy Outlook estimated “that the 2020 build could add 1.6 billion barrels to global inventories, which would fill them at or near their estimated full storage capacity levels.”

The EIA doesn’t see demand begin to cut into inventories until fourth-quarter 2020, and that assumes global consumption returns close to its long-term level starting in the third quarter (see Exhibit 1).

Interest rates also reflect considerable economic uncertainty. After falling sharply in late February and early March, long-term U.S. Treasury rates bounced into the second half of March. They have inched lower again in recent weeks. Long-term rates generally decline as economic conditions soften, so a flattening yield curve— anchored near zero on the short end—suggests there’s still great uncertainty about the economic road ahead.

Contagion Contingencies

Projections for the spread and fallout from COVID-19 have been subject to revision in recent weeks. First, they declined as the public adhered to social distancing and lockdown measures at a greater-than-expected rate. Then, as epidemiological models moved through their peaks and the narrative rolled on to the timing of reopening society, policies were forced to follow— loosening restrictions and pushing projections back upward.

Exhibit 1: World Liquid Fuels Production and Consumption Balance (millions of barrels per day)

The fluidity of COVID-19 forecasts is compounded by their wide potential ranges of outcomes. It’s completely in keeping with honest statistical modelling to offer a base case along with low and high projections, but such a wide range limits their utility for health-system planning purposes, let alone forecasts about the economy and financial markets.

SEI’s View

We spent much of February, March and April preaching patience and moderation in the face of steep selloffs and historic volatility. We contended that the decline was too fast and that it would likely be followed by a substantial rebound.

We think moderation is warranted again, albeit in the other direction. The rebound (notably driven by the same mega-cap technology firms that led the bull market) could eventually yield to another pullback, especially given the widespread uncertainty and shortage of concrete positive developments.

We expect the re-opening of the global economy to proceed cautiously and unevenly within and across countries. Many major developed-market countries still need to establish enhanced testing to track and isolate the outbreak before returning to broader re-opening. It will take time before this accrues to a meaningful increase in economic activity.

Many emerging markets are still seeing increased infection rates, so we’re far from a return to normal conditions. Moreover, there’s a possibility we may return to lockdown later this year if COVID-19 cases appear set to spike again.

Our investment managers are thinking in terms of years, rather than months, before the corporate earnings environment recovers from below-trend economic activity to more normal conditions. We believe there will be plenty of opportunities for skilled managers to capitalise on and that investors will be rewarded for their patience and moderation through shorter-term advances and declines.

As you can see SEI have a different view to some of their peers, with a slightly more negative (realistic?) view.

Since 1968, SEI has been a leader in the investment services industry, recognized for its history of innovation. Today, they serve about 11,300 clients, including banks, trust institutions, wealth management organizations, independent investment advisors, retirement plan sponsors, corporations, not-for-profit organizations, investment managers, hedge fund managers, and high-net-worth families. SEI manages or administers $920 billion in hedge, private equity, mutual fund and pooled or separately managed assets, including $283 billion in assets under management and $632 billion in client assets under administration.

Paul Green

11/05/2020