Please see below an article received from Brewin Dolphin yesterday (09/03/2021), which details their views on markets:

As you can see from the above, markets remain positive, although some are seeing corrections. The fiscal stimulus from governments around the world should help economies recover.

Please continue to check our Blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.

Please see below market analysis received from Brooks Macdonald yesterday evening. The article comments on how the continuous rise in yields is affecting market volatility and refers to political developments during Biden’s first 100 days in Office.

The US Federal Reserve (Fed) enters its communication blackout period at a crucial time for sentiment

European and US equities had a pretty subdued Friday until after the European close, when US equities picked up to close higher for the day and the week. Market expectations are now for the first Fed rate hike to occur in early 2023 and with the Fed now absent due to the communications blackout, further assumptions could be baked in given the policy void1.

Rises in yields continue to drive market volatility

US 10-year yields are now over 1% higher than their lows last August2. This is a testament to the dramatic moves seen over the last few months. Of course, for context, a circa 1.6% yield is still on a par with the lowest rates seen in 20193, so perhaps it’s remarkable that rate expectations had stayed so low in Q4 2020 when more economic optimism was being priced in. In Q2 and Q3 last year, the equity market was drawing its optimism from the low rate environment and the relative support this gave to high growth equities. Since November 2020, and the first vaccine efficacy trials, we have seen a boost to economic expectations which brought cyclical equities into vogue and has catalysed this reappraisal of bond yields. The big question in markets is whether the Fed are comfortable with this rapid rise, albeit only to 2019 lows, and to find that out we need to wait another week.

The Senate passes President Biden’s $1.9 trillion US fiscal stimulus package

The Senate passed President Biden’s $1.9 trillion package on Saturday meaning it will now move to the House for a final vote before going to the White House for Biden’s signature. The economic growth expectations that have been revised up since November 2020 take account of both the expected post-COVID-19 recovery but also the size of US stimulus. With the package’s total size having survived Congress intact, despite some concessions to moderate Democrats, we are likely to see a supercharged period of economic growth and short-term inflation.

With the Democrats only able to use the budget reconciliation process for a fiscal stimulus package once in 2021, the instinct was always to ‘go big’. Market concerns that the support would be too large and therefore inflationary has been one of several factors being priced into equity and bond markets this year. With the package likely to enter law early this week, and the Fed blackout period ongoing, rising inflation expectations could be a major driver of volatility this week.

Please check in again with us soon for more news updates and interesting analysis.

Please see below for Blackfinch Asset Management’s latest Monthly Market Moves article, received by us yesterday 08/03/2021:

Market Performance

1st- 28th February 2021 (in GBP Total Return)

FTSE 100

+ 0.65%

S&P 500 (USA)

– 1.21%

FTSE Europe (Ex UK)

– 0.94%

TOPIX (Japan)

– 1.87%

MSCI Emerging Markets

– 3.82%

Market Overview – February 2021

February was a tale of two halves for global bond and equity markets. What started out as a relatively positive month quickly reversed into a period of turbulent trading. Almost exactly one year to the day since the initial pandemic sell-off, inflation concerns caused bond yields to rise, causing a negative impact on equity markets, particularly those tilted towards growth stocks.

Inflation Fears Shake Markets

It has long been assumed that the economic recovery from the pandemic would cause some inflationary pressures. However, the fear that central banks, particularly in the US, may withdraw their substantial monetary policy support gripped investor attention.

President Biden’s $1.9trn stimulus package, which includes issuing further cheques to large swathes of the US population, moved closer to being agreed. This added further fuel to the inflation flames, evidenced already by the $600 cheques issued in January causing retail sales to come in way ahead of market expectations.

US Federal Reserve Chairman, Jerome Powell, did his best to reassure investors that the central bank will not consider raising interest rates, but his assurances did little to calm their nerves.

These fears caused the value of the US Dollar to appreciate. This in turn negatively impacts Emerging Markets, where countries hold significant portions of their debt in Dollars and therefore servicing this debt becomes more expensive.

Is the End in Sight for Lockdown?

More than 20 million people in the UK, almost one-third of the population, have received their first COVID-19 vaccine injection, with nearly 800,000 having received both doses.

Prime Minister Boris Johnson set out his ‘roadmap’ for an end to lockdown measures in England, starting with children returning to school on 8th March. While proposed dates are in place for a complete easing of lockdown, the public, and investors, should not get complacent given the prevailing uncertainty in the interim.

UK Gross Domestic Product came in ahead of expectations in December, reiterating the ongoing economic recovery.

Despite this, the UK economy contracted by a record 9.9% in 2020 but has so far managed to avoid a double-dip recession.

Little Change in Central Bank Policy

The Bank of England (BoE) left interest rates unchanged at 0.1% and kept its bond-buying programme at £895bn.

The BoE also commented on the possibility of negative interest rates, stating that most banks would need six-months to prepare for such a move. While this could be seen as foreshadowing a potential move towards negative rates in the future, it at least gives institutions some comfort that any move would not be in the near term.

The European Central Bank made no change to its monetary policy, keeping interest rates on hold as well as maintaining the €1.8trn Pandemic Emergency Purchase Programme (PEPP), confirming it will run until at least March 2022.

Chairman Jerome Powell announced that the US Federal Reserve will need to remain accommodative for “some time” yet. While its programme of substantial monthly government bond purchases looks likely to continue, Powell noted this could be eased once inflation and employment targets are reached

Summary

With markets having a difficult month, it is important to recognise just how far they have come in the last 12 months. As we pass the one-year anniversary since developed equity markets started to decline, as the potential impact of the pandemic became a reality, we must keep in mind that markets have rallied strongly since their trough in mid-March 2020. Therefore, periods of profit-taking are to be expected, particularly in those areas that have rallied the strongest.

While an end to lockdown measures feels within touching distance for some countries, including the UK, the emergence of new variants of COVID-19 remains a concern. As such, we need to temper any excitement of a ‘return to normal life’, as there is still a long way to go. Even so, right now in the UK the signs are promising that we may have our freedoms returned to us come the summer.

Please continue to utilise these blogs and expert insights to keep your own holistic view of the market up to date.

Please see the below article from JP Morgan received this morning:

‘Emerging markets pose particular ESG challenges. But factoring ESG considerations into decision making can benefit performance, and demand for more sustainable investments is helping to drive change.’ – Tilmann Galler

In our 2021 Investment Outlook, we outlined that one of the key imperatives for investors in 2021 was to understand how the global policy and regulatory initiatives behind environmental, social and governance (ESG) factors are likely to increasingly affect the macro landscape and financial sustainability of companies.

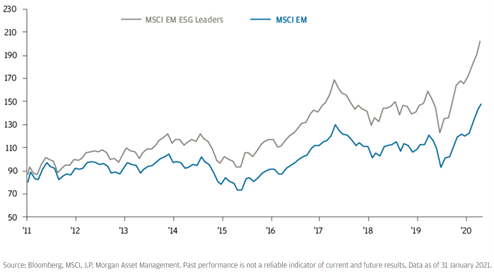

In this context, should investors shy away from investing in emerging markets given lower standards? In this piece we consider the diverse array of ESG challenges that exist in emerging markets and argue that selecting companies that are rising to the challenges and navigating a changing ESG landscape can lead to significant return opportunities, as we have already seen in recent years (Exhibit 1).

Exhibit 1: ESG leaders outperformed in emerging markets

Index level in USD, rebased to 100 at December 2010

Environment (E):

Preserving the environment and fighting climate change are becoming increasingly pressing global policy priorities. With President Biden now in the White House, the Paris Climate Agreement has been invigorated, and the discussion is likely to intensify ahead of the important regroup at the COP26 meeting in November.

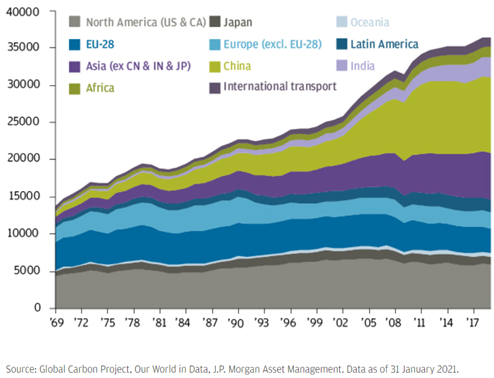

Reducing carbon emissions and aiming for carbon neutrality have been identified as important milestones. Fifty years ago, today’s developed countries contributed two thirds of global carbon emissions and emerging markets only one third. Today, total CO2 emissions have tripled, but the ratio has reversed and emerging markets contribute almost 70% (Exhibit 2).

Exhibit 2: Emerging markets are the biggest contributor to CO2 emissions

Annual total CO2 emissions by region from fossil fuels and cement production only; million tonnes

Europe and the US have committed to achieving carbon neutrality by 2050, while China has given itself an additional 10 years. Reaching these goals will require a significant alteration to the business fundamentals of corporations in carbon- intensive sectors such as energy, materials and utilities, but also for fossil fuel-dependent economies such as Russia, Saudi Arabia and South Africa. Business and economic models that fail to adjust will likely face increasing sanctions from investors and climate-committed governments.

A prominent example is the carbon border adjustment mechanism, which is currently being discussed in Europe and the US with the aim of avoiding regulatory arbitrage.

The adjustment would take into account the carbon intensity of goods sold. Countries that did not set a sufficient carbon price would be perceived to be gaining a competitive advantage and so would face tariffs at the border. But implementation is complex. Any carbon border adjustment has to be embedded into existing obligations under the World Trade Organisation and should also relate to local emissions trading schemes. There is also a risk that such a mechanism could fuel further trade conflicts and in the end evolve as a new frontier in the US-China trade war.

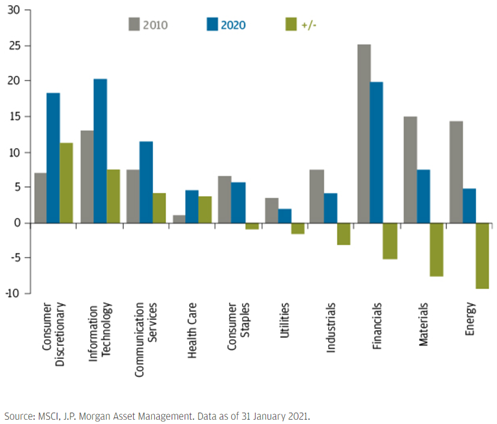

As emerging economies mature and services become a larger part of their economies, their CO2 footprints will naturally improve. We have already seen a significant decline in the market cap weighting of carbon intensive sectors in the MSCI Emerging Markets Index (Exhibit 3). Nevertheless, challenges remain, particularly in manufacturing, food processing standards, and water and waste management. Governments may be resistant to change if it is perceived to be an impediment to GDP and income growth. But emerging market companies that are part of an international supply chain will have to improve their standards, because large multinational companies are beginning to optimise their value chains for ESG criteria. Failing to adapt will be a significant disadvantage in the global competitive landscape. We therefore expect that transition will, in many cases, be faster on a corporate level than in government policy.

Exhibit 3: MSCI Emerging markets sector weights

Social (S):

Human rights, labour and health conditions, and diversity are social criteria on which businesses operating in emerging markets are facing increased scrutiny. Growing awareness from consumers and investors worldwide is putting governments and corporates under pressure to improve – with social media bringing increased visibility of the issues. The Foxconn labour abuse controversy is a good example. Reports of poor working conditions in the company’s Chinese factories, where it manufactures products for Apple, created a very negative global feedback loop. Companies exploiting employees and the communities they operate in are risking significant reputational damage on a global basis.

Governance (G):

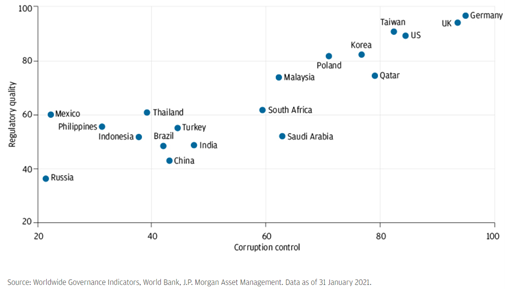

While environmental and social factors are gaining prominence, governance issues such as regulation, corruption, transparency and share-/bondholder rights have long been important considerations for investors in emerging markets. World Bank Indicators provide a useful top-level indication of the countries that require particular investor vigilance and those that already have higher standards in place (Exhibit 4). However, it’s important to keep in mind that these indicators provide just a snapshot of the current status and that the dynamics in corruption and regulation are quite different across the regions. In the past 10 years, Asian countries, on average, have showed significantly more improvement than Latin American, where the situation has deteriorated. Even if countries are engaging in more sustainable policy and introducing stewardship codes, like Korea,Taiwan, and Brazil in 2016, results can differ widely. The investment world will watch China’s next five-year plan closely to see whether financial sector reform and stricter environmental regulation will also improve government stewardship.

Exhibit 4: Corruption control and regulatory quality per country

Percentile rank indicates the country’s rank among all countries covered by the aggregate indicator, with 0 corresponding to lowest rank, and 100 to highest rank.

A key issue in emerging markets on a corporate level is ownership. The free float of the MSCI Emerging Markets is only 50%, compared to nearly 90% for developed markets. Investing in emerging markets generally means that you are in a minority position, because the entity is controlled by either the state, individuals or families. The risk for investors is that the company management is not only pursuing economic goals. Close relationships to government officials are also detrimental to efforts to fight anticompetitive practices, corruption and bribery and protect shareholder rights. Engagement is crucial to get a clearer picture of the management’s commitment to improving governance. Compared with developed markets, the power to induce change through voting in shareholders’ meetings is more limited.

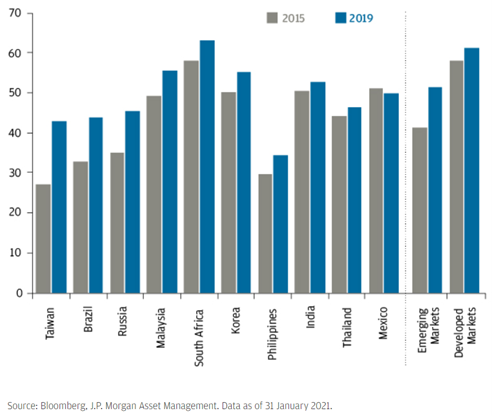

However, policymakers in emerging markets are reacting to the increased demands for better governance. For instance, the introduction of corporate governance codes in Taiwan (2010), Brazil (2016), and Russia (2014) improved the representation of independent directors on boards. In emerging markets overall, such representation has increased by 10 percentage points to 51% in the past four years. Governance standards in South Africa are already close to those in developed markets.

Exhibit 5: Governance is improving in emerging markets

Average % of independent directors in selected emerging markets

Conclusion

Emerging markets and ESG represent the place where two investment mega-trends come together. The dynamic growth of emerging markets will lead to a significantly higher representation in portfolios in the next 10 years. At the same time, due to investor preferences and developed world capital regulation, we are seeing a growing preference for investments that meet ESG criteria.

Emerging markets are not homogenous on a country nor a corporate level. But growth and sustainability can be reconciled through careful company research and engagement. Companies that are the beneficiaries of fast growth in their local markets, but which at the same time demonstrate an awareness and desire to meet global ESG standards, have sustainable business models. Indeed, ESG characteristics often serves as a proxy for quality, since companies that screen well are often managed with a long-term view, with higher levels of broad R&D and innovation.

In summary, we do not see that investing in emerging markets sits in opposition to the world’s broader ESG ambitions – the opposite might be the case. By demanding higher ESG standards, investors are helping to accelerate the pace of change. The scope for improvement in sustainable outcomes is significant and the consideration of ESG factors in this asset class provides ample return opportunities for long-term investors.

Please continue to check back for more ESG related insights along with our usual market updates and commentary.

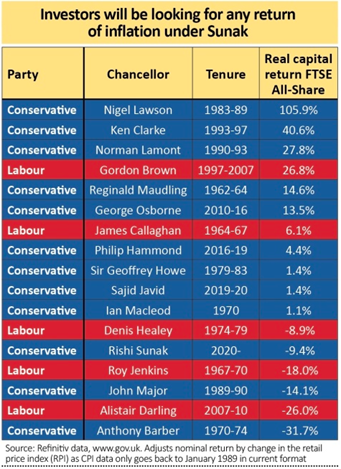

Please see the below article received by AJ Bell late last night:

On average a Tory occupant of Number 11 has been better for ‘real returns’.

The Conservative Party’s Benjamin Disraeli, twice prime minister and thrice chancellor of the exchequer, once said of his bitterest political rival, who held each post on four occasions: ‘Well, if Mr Gladstone fell into the Thames that would be a misfortune; and if anybody pulled him out, that would be a calamity.’

The Tories’ latest Chancellor, Rishi Sunak, will be hoping for a warmer welcome for Wednesday’s Budget (3 March) and he is likely to measure success in terms of jobs, economic growth and ultimately opinion polls and votes.

Investors will be looking to their portfolios to gauge the effect of his policies and history suggests that the UK stock market has, for whatever reason, done better on average under Conservative chancellors than Labour ones, at least once inflation is taken into account.

Party On

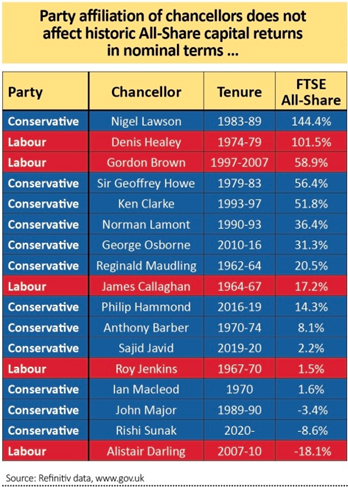

Since the inception of the FTSE All-Share index in 1962, the UK has had 17 chancellors, 12 of whom have been Conservative and five Labour.

At first glance, there is nothing in it between the two parties. Under Conservative chancellors, the FTSE All-Share has chalked up a total capital gain of 355%, in nominal terms.

That equates to an average advance per chancellor of 32.1% (including Macleod’s brief term with that of his successor, Anthony Barber), while under Labour the benchmark has risen by 161% for an average gain of 32.2%.

Across 34 years of Tory chancellorships that is a compound annual growth rate (CAGR) of 4.5% against 4.1% under 24 years of Labour in 11 Downing Street and two of the top-five best spells under a single chancellor actually come under Labour, again in nominal terms.

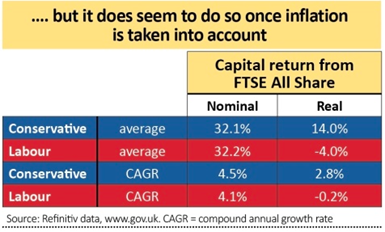

However, the picture changes profoundly when inflation is taken into account and capital returns from the FTSE All-Share are assessed in real (post-inflation) terms rather than nominal ones.

Here, Conservative chancellors come out well on top, as the withering effect of inflation upon investors’ returns from the stock market under Labour’s Healey chancellorship of the mid-to-late 1970s comes into play.

It must be noted that inflation also chewed up the nominal gains made by the FTSE All-Share under the Tory chancellors Sir Geoffrey Howe (1979-83) and Tony Barber (1970-74).

Beware A Return to Barber

As financial markets today ponder whether inflation is about to make a return, and the yield on the benchmark UK ten-year bond, or gilt, rises as prices fall, a repeat of the ‘Barber Boom’ is something that Sunak will be determined to avoid, even if he will be looking to support and boost growth as best he can, as the economic fall-out that followed was very painful for the UK and so painful that the Tories fell from office after a pair of general elections in 1974.

Not all of the inflation that tore through the British economy could be laid at the door of Barber’s policies, as the 1973 oil price shock had a huge amount to do with it, and this highlights the importance of factors which are beyond the control of any chancellor, no matter how diligent or skilled.

Alastair Darling could hardly have expected to inherit the 2007/8 financial crisis which prompted a deep recession and a wicked bear stock market. Norman Lamont inherited British membership of the Exchange Rate Mechanism, fought to defend the pound and a policy in which he did not believe and oversaw a devaluation of sterling which actually helped the FTSE All-Share to rally.

Sunak has had to contend with Covid-19 and the worst recession for three centuries, so perhaps he has been given the worst hand of all.

Even so, investors, looking at the world through the narrow perspective of their portfolios, will be wanting Sunak to think back to Barber. Inflation mangled portfolio returns for much of the 1970s and all the way through to the Thatcher-Howe prime Minister-chancellor team of 1979-83. Bizarre as it may sound, markets may therefore want to see a little inflation – and growth – but not too much, especially as any sustained surge in prices could force bond yields higher and even oblige the Bank of England to act and raise interest rates.

Markets came close to falling out of bed last week, as they pondered such a prospect, so as ever Sunak has a difficult balancing act going forward, as he juggles growth, jobs, the deficit and inflation, as well as votes.

Please continue to check back for more of our regular blog content.

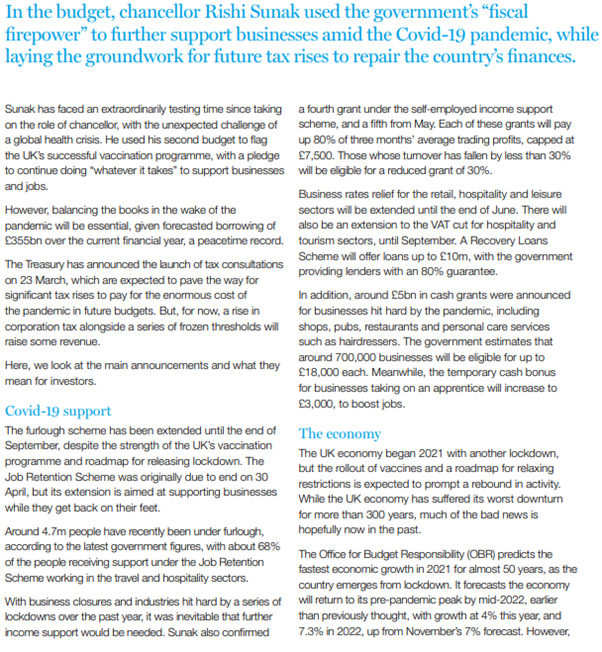

Please see below article received from Jupiter yesterday evening, which analyses whether the measures announced by Rishi Sunak in Budget 2021 will sustain the UK’s economic and financial market recovery in the years ahead.

In every downturn, the UK Government’s finances turn down sharply. Tax receipts fall as job losses, bankruptcies and subdued spending impact the three big sources of revenue for the Treasury – income tax, National Insurance and VAT. But Government spending must rise to cushion the impact of a recession, through unemployment benefits and welfare payments.

There is always a moment at the depths of a downturn when the Government’s budget deficit looks awful and the prospect of a return to more balanced books nigh impossible.

Clearly this pandemic has a rather different dynamic, as the Government measures to support the economy from complete collapse during extended lockdowns, has pushed their spending to levels unprecedented outside wartime. Roughly 75% of the increase in the budget deficit has arisen due to these support measures – about £200bn. Today’s extension of such support until September will only increase the scale of this spending, all funded through borrowing.

Whilst tax receipts have fallen during the pandemic, they have done so only modestly – testimony to the success of the support in limiting the rise in unemployment and bankruptcies thus far. Tax receipts as a percentage of GDP have remained roughly in line with their long run average of 37% of GDP.

Government spending, by contrast, has risen from its more usual level of 40% of GDP to 55% and rising. Hence the Chancellor’s desire to ‘level with the British people’ on the unsustainability of current levels of borrowing and spending by Government and the need to rebuild public finances in the future.

The risk of raising taxes too soon into the post-pandemic recovery is that it saps the strength of the recovery. I believe there is bound to be a surge in consumer spending as individuals and families enjoy their freedom from lockdown to shop, eat out and holiday. But it won’t be until well into 2022 before we know the full scale of the likely bankruptcies to come, the peak levels unemployment will reach – today’s more upbeat forecast notwithstanding – nor the longer-term psychological impact on consumers of the pandemic on spending and saving habits.

Crucially, though, the Chancellor needs to remember the lesson of all his predecessors in the depths of a recession. The cyclicality of Government finances means that as the economy recovers, automatically Government spending will fall and tax receipts will rise. The end to Government support measures and a resumption of consumer spending will boost VAT receipts just as the support cheques cease to be written; in this regard, I believe the transition measures announced today are to be welcomed.

Clearly though, one of the most significant of today’s announcements is the planned increase in Corporation Tax as of April 2023 from the current 19% to 25%. While this does indeed give businesses clarity, it is nevertheless a substantial increase, which will in time impact on companies’ ability to return profits to shareholders, and at variance with widely held expectations that such hikes would begin sooner and would be more gradual in their introduction.

Investors will be considering the impact of this pending rise and will be asking themselves to what extent it can be offset by the generous-sounding 130% “super deduction” on business investment. While this is, in my view, an innovative and progressive policy, taken together with the upcoming rise in Corporation Tax, it is likely to mean that the economic growth benefits resulting from the policy will be somewhat front loaded.

Meanwhile, the decision to maintain income tax, National Insurance and VAT at their current levels should provide some support consumer confidence and household budgets as the country emerges from the pandemic. Nevertheless, the Chancellor’s explicit announcements of upcoming fiscal drag – the result of not adjusting taxation thresholds to take account of future inflation – reflects the reality of the situation of the post-pandemic economy. Although this is undoubtedly a progressive policy, put simply, the higher inflation rises, the more the Treasury is likely to benefit. Over time, should we enter a more inflationary environment, in public finance terms this may well turn out to have been a prudent decision, given the impact of rising inflation on the cost of servicing our national debt.

Turning to the UK equity market, it was no surprise to see rising share prices among those businesses that should be beneficiaries of further support to the domestic economy, such as banks and leisure stocks, alongside housebuilders. The latter may well benefit from the extension of the stamp duty holiday and mortgage guarantee programme, as well as a more benign backdrop through the extension of Government support through the summer’s transition from lockdown and re-opening to the end of measures such as the furlough scheme.

Looking to the longer term, to my mind, the truly prudent but wise Chancellor will not risk the upturn by setting out a plan for increased taxation in the years ahead, but keep his powder dry to see just how radically Treasury finances improve over the coming year, without any action on his part whatsoever. While today’s Budget announcements appear well placed to support the transition to life after the pandemic over the next couple of years, it remains to be seen whether the “front-loading” of business incentives to spend now but be taxed later leads to a slowdown in growth thereafter which might not have been necessary.

We will continue to publish relevant content and news as the vaccine roll-out in the UK continues to expand and the light at the end of the tunnel brightens. Please therefore, check in again with us soon.

Please see below an article from Brewin Dolphin received late yesterday evening, which details their overview on the Chancellor, Rishi Sunak’s budget, which was unveiled in Parliament yesterday:

As you can see from the above, the Chancellor has announced significant measures to help businesses get back on their feet and innovate and help the economy recover. It looks like businesses will bare the initial brunt of raising additional revenue for the Treasury and the freeze of the allowances and thresholds until 2026 after April’s increases will also generate some additional revenue.

Tax consultations are commencing shortly – we await the outcome of these.

Please continue to check our Blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.

HM Treasury and HMRC quietly launched additional proposals on 11/02/2021 with the potential to have a much greater effect on retirement planning over the coming years.

The proposals

The main proposal is this: anyone who was a member of a registered pension scheme on 11 February 2021 (the date of the consultation) and had a right to take pension benefits before age 57 on that date, would keep that right as a protected pension age. That protected pension age (which in most cases would be 55) would be scheme specific and work similarly to existing protected pension ages. This would mean:

Anyone joining a new pension scheme from 12 February 2021 onwards would have an NMPA of 57 from 2028 for that scheme, although they may have other pensions that they could still access before age 57.

From 12 February 2021, anyone who transfers to a new scheme would lose the right to take benefits from that pension before age 57 (assuming the original scheme offered that right), unless they completed a block transfer.

One key difference highlighted between the rules for existing protected pension ages and these proposals, is that clients would not need to crystallise all the benefits within a scheme on the same date in order to keep their protected pension age.

Next steps

The timing of proposals like these is always difficult. The consultation doesn’t close until 22 April, and we don’t expect to see draft legislation from the Treasury until the summer. However, if the proposals do go ahead as they stand, transfers that take place from today could affect when clients are able to take benefits. While many people may not expect to retire at 55 or 56 (and until yesterday might have assumed it simply wouldn’t be an option), it still adds an additional consideration into people’s pension planning.

It’s still early days, and I’m sure you’ll see more about the industry’s thoughts about the proposals over the coming weeks. What seemed like a very straight forward upcoming pension change has suddenly become something to keep a keen eye on.

Our Comment

We need to see what the outcome is in the summer, but this is one to watch for those who are considering retiring early at age 55 or if you thought you might access your pension benefits, typically tax free cash, early at age 55 from 2028.

In real terms this will only be a few people, most in the UK haven’t got the pension assets they need for early retirement and shouldn’t access their pension funds too early either.

However, if you are one of the few that may have a plan to retire early or access your pension benefits early, at age 55, from 2028 you now need to be careful about any pension switching or consolidation. Let’s see what we get at the end of the consultation, hopefully draft legislation in the summer. Watch this space.

Steve Speed

03/03/2021

Technical content cut and pasted from Curtis Banks Technical Update.

Please see below the latest ‘Markets in a Minute’ article from Brewin Dolphin received late yesterday afternoon – 02/03/2021

Equities slide as rise in bond yields sparks tech sell-off

Global equities fell sharply last week after a steep rise in long-term government bond yields led to the worst technology sell-off in four months.

In the US, the S&P 500 recorded its biggest weekly drop in a month, falling 2.5%. The Nasdaq Composite suffered its worst decline since October, down 4.9%, as investors continued to rotate out of highly valued growth stocks into value and cyclical stocks. A rise in oil prices saw energy shares outperform, whereas consumer discretionary stocks were weak.

Stock markets in Europe also fell, with the pan-European STOXX 600 ending the week down 2.4%. The FTSE 100 dropped 2.1% as the pound rose to its highest level in almost three years, fuelled by the rapid roll out of the Covid-19 vaccine and hopes of economic recovery.

The global sell-off fed through to Asia, where the Nikkei fell 3.5% and the Shanghai Composite tumbled 5%. China’s large-cap CSI 200 recorded its worst weekly performance since October 2018, falling 7.7% as profit-taking hit companies in sectors such as semiconductors and electric vehicles.

*Data from close on Friday 19 February to close of business on Friday 26 February.

Budget leaks boost FTSE 100

The FTSE 100 rebounded on Monday, gaining 1.6% following a series of leaks about Wednesday’s budget. Housebuilders rallied on news that the government will launch a mortgage guarantee scheme to help buyers, with small deposits, onto the property ladder.

In the US, the S&P 500 gained 2.4% in its best session since June 2020. The Nasdaq surged 3% after vaccine optimism boosted risk assets and Treasury yields retreated. The Bank of England echoed sentiments from the Federal Reserve about accommodative monetary policy.

The rebound began to falter on Tuesday, with the Hang Seng and CSI 300 both declining by around 1% overnight. A top Chinese banking regulator said he was ‘very worried’ about bubbles in overseas financial markets and in China’s property sector. The FTSE 100 opened flat, with energy and mining stocks among the worst performers amid fears of slowing demand for commodities in China. Taylor Wimpey was the biggest gainer, adding 3.4% after it revealed the 2021 selling season had started positively.

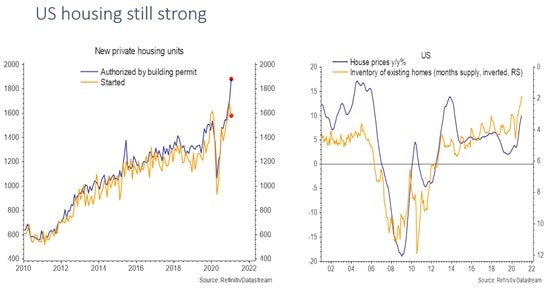

Economic data stronger than anticipated

The yield on the ten-year US Treasury note increased to its highest level in over a year last week, as stronger-than-expected economic data fuelled fears about rising inflation. In the US, data revealed continued robustness in the housing market, with building permits hitting a new high and house prices continuing to surge.

Sales on new single-family homes increased by 4.3% in January to a seasonally adjusted annual rate of 923,000 units. Sales were helped by historically low mortgage rates and a shortage of previously owned houses on the market. The median new house price rose by 5.3% from a year earlier to $346,400.

The housing data added to solid PMIs published the week before, which showed a 1.3% increase in the prices that businesses receive for their goods and services – the biggest gain since the index was launched in 2009. Weekly jobless claims also hit their lowest level in three months at 730,000, while personal incomes increased by 10.1% in January following payments from the coronavirus relief package.

On Wednesday, Fed chair Jerome Powell sought to allay investors’ fears that stronger economic growth will result in monetary stimulus being removed sooner than expected. Powell said inflation remains soft and confirmed the Fed’s dovish stance. Stocks briefly recovered on Wednesday, but began their descent again the following day, suggesting Powell’s comments have done little to quell investors’ concerns.

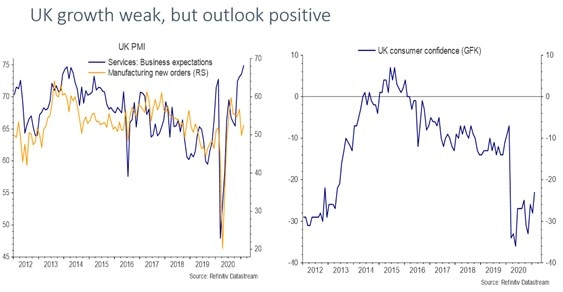

UK consumer confidence creeps higher

There is also optimism in some of the UK’s economic data. Manufacturing new orders remain in expansion territory, and the expectations component of the services PMI hit the highest level in over a decade. UK consumer confidence is also starting to creep higher.

Lockdown restrictions will start to ease in England from 8 March, with nearly all sections of the economy due to be reopened in late May. In Wednesday’s budget, Rishi Sunak is expected to announce that the furlough scheme will be extended until at least May. Around 20 million people in the UK have now received their first dose of the vaccine.

The vaccine rollout continues to lag in Europe, with just 6.4% of the European Union’s population receiving a jab. Despite this, the eurozone Economic Sentiment Indicator increased to 93.4 in February from 91.5 the month before – the highest level since March 2020. Fourth-quarter German GDP data was revised to a growth rate of 0.3% from an initial estimate of 0.1%, following strong exports and construction activity.

Over in Japan, the Reuters monthly Tankan Index, which tracks the Bank of Japan’s quarterly Tankan survey, recorded a positive reading among manufacturers for the first time since 2019, thanks to improving demand from overseas. Japan is also seeing a decline in the Covid-19 infection rate, which will see the state of emergency status being lifted for six prefectures a week earlier than planned.

Weekly updates like these from Brewin Dolphin help us keep up to date with what is happening within the markets. This week’s ‘Markets in a Minute’ article focuses on exploring some of the reasons behind the tech sell-off.

Please continue to check back for our regular blog posts and updates

M&G plc (M&G) is today joining the Powering Past Coal Alliance (PPCA) and announcing it wants to end investment in thermal coal by 2030 for developed countries and 2040 for emerging markets.

M&G’s coal phase out plan is a key step towards achieving its goal of net zero carbon emissions across its investment portfolios by 2050 at the latest, and helping to restrict global warming to 1.5 degrees in line with the Paris Agreement on climate change.

As stewards of long term capital, actively managing the savings of millions of people around the world, M&G will use its influence to accelerate the transition to a greener, cleaner economy with ambitious plans to cease all investment in new coal mines and coal-fired plants and to exclude public companies which cannot commit to a complete phase out of coal by 2030 in developed countries and 2040 in emerging markets.

As an asset owner, M&G will be implementing this approach to coal-related investments across its own internal portfolios over the coming year. As an asset manager, M&G will be working with clients to align existing mandates and funds to this position.

At the same time, through its growing range of sustainable investment funds, M&G is giving institutional clients and individual customers the opportunity to invest in technologies, infrastructure and services which offer financial returns as well as making a positive difference to the environment.

Speaking at PPCA’s Global Summit today, M&G plc Chief Executive, John Foley, said: “An accelerated phase-out of coal is essential if we want to limit global warming and ensure a sustainable future for our planet. We are delighted to join the PPCA and fully support its work to encourage businesses, governments and other organisations to commit to a transition away from coal in the run up to COP26 later this year.”

Welcoming M&G’s commitment to the PPCA, Nigel Topping, COP 26 High Level Climate Champion, adds: “Phasing out thermal coal is a critical early step on the race to net zero. PPCA is a key part of the COP 26 Energy Transition Campaign, and it is fantastic to see M&G making this commitment in response to attending the PPCA ministerial round table co-hosted by the UK and Canada.”

As our clients will know, Prudential’s PruFund range of funds are managed by M&G’s multi asset team, Treasury & Investment Office (T&IO) – one of the largest and most well resourced in the UK.

This is great news, and another step along the ESG road for M&G.

M&G plc aim to be carbon net zero as a corporate entity by 2030. Further, they aim to achieve 40% female and 20% ethnicity representation in their leadership by 2025.

Prudential Assurance Company aims to achieve net zero carbon emissions across AUMA (assets under management and administration) by 2050, of which the PruFund range is a material part, in line with the Net Zero Asset Owners Alliance.

The scale of PruFund allows the management team to use segregated mandates to apply a variety of implementation techniques for their ESG views, up to and including, exclusion of certain stocks or sectors from portfolios.

Currently their policy excludes investment in certain controversial weapons companies, namely cluster munitions and anti-personnel mines.

M&G look to the asset managers they select to engage with companies as active owners that help foster a more sustainable economy, participate in voting on key issues such as Climate Change and ensure that ESG is integrated into their investment processes. The majority of PruFund assets are managed by M&G, whose Responsible Investment team provide issuer and sector specific ESG risk and opportunity analysis and education on sustainability themes to portfolio managers and analysts.

Investments have recently been made with the PruFund range by purchasing a solar power plant in the Nevada desert.

Keep checking back for more ESG related content along with our usual market updates and outlooks from a variety of fund managers.