Please see below the latest ‘Markets in a Minute’ article from Brewin Dolphin received yesterday – 26/01/2021

US equities strengthen on stimulus plans

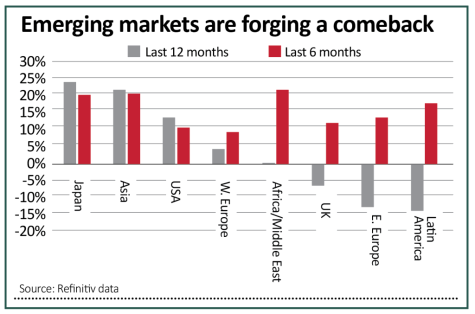

Global equities performed relatively strongly last week, as fresh hopes of US stimulus outweighed concerns about extended lockdowns in Europe.

The Nasdaq was the strongest performer among the main markets, rising by an impressive 4.19% thanks to a comeback from the FAANGs. The S&P 500 and the Dow also recorded gains, with investors celebrating Joe Biden’s inauguration and Janet Yellen’s call for Congress to ‘act big’ on stimulus measures.

Renewed coronavirus concerns weighed on the UK’s FTSE 100 as well as several European indices. Over in Asia, hopes of better relations between China and the US boosted the Shanghai Composite by 1.13%, while the Nikkei remained relatively flat.

Last week’s markets performance*

- FTSE100: -0.60%

- S&P500: +1.94%

- Dow: +0.59%

- Nasdaq: +4.19%

- Dax: +0.63%

- Hang Seng: +3.06%

- Shanghai Composite: +1.13%

- Nikkei: +0.39%

*Data from close on Friday 15 January to close of business on Friday 22 January.

Merck abandons vaccine

News that pharmaceutical giant Merck is abandoning its vaccine development efforts have dampened last week’s gains. The FTSE 100 slipped a further 0.8% yesterday amid fears that Merck’s decision could delay the global rebound from the pandemic. Airlines, who could face severe travel restrictions, struggled the most, with shares in International Consolidated Airlines 7.2% lower.

In the US, the S&P 500 and the Nasdaq briefly turned negative yesterday, but the Nasdaq ended up closing at a record high, gaining 0.69% ahead of quarterly results from Apple, Microsoft and Facebook this week. The Dow, in which Merck is a component, ended yesterday 0.12% lower.

US celebrates Biden and the FAANGs

Following his inauguration last Wednesday, Joe Biden wasted no time in unveiling details of how he intends to support the US through the pandemic. His proposed $1.9 trillion Covid-19 fiscal package includes another round of direct payments, an increase in the federal weekly unemployment insurance benefit and, somewhat controversially, a hike in the national minimum wage to $15 per hour.

Biden also repeated his goal of one million vaccinations a day for the first 100 days of his presidency, and reversed Trump’s decision to withdraw from the World Health Organization and Paris Agreement on climate change.

The fact that Biden’s inauguration took place without any significant violence helped to calm nerves, as did strong provisional services PMI and better-than-expected housing data.

Although Biden’s election has brought some comfort to investors, it is worth noting that his Cabinet appointments are less market-friendly than Trump’s were. His appointments for the head of the Securities and Exchange Commission, the Consumer Financial Protection Bureau and the Senate Banking Committee could result in tougher regulations for the financial sector.

Last week also saw the return of big mega-caps in the US, which helped to drive up the Nasdaq and S&P 500. Netflix, which reported robust earnings, gained 13.5%, while Apple, Google and Facebook all rose 9%. A strong start to the US reporting season added to investor optimism for the new president.

Lockdowns extended in Europe

Over in Europe, investor sentiment was more subdued as renewed coronavirus concerns took hold. Germany’s Xetra DAX Index edged up by 0.63%, whereas France’s CAC 40 and Italy’s FTSE MIB both declined by 0.93% and 1.31%, respectively. The UK’s FTSE 100 Index fell 0.60%.

There are growing concerns that social distancing restrictions in the UK could last until the middle of the year, after Boris Johnson announced it is ‘too early’ to say when the national lockdown will end. Germany extended its restrictions until 14 February, and The Netherlands introduced its first nationwide curfew since World War II.

Disappointing economic data did not help matters. A Purchasing Managers’ Index revealed business activity in the eurozone contracted at a faster rate in January, while the UK’s quarterly CBI business optimism index plunged from 0 to -22, largely driven by fears about the impact of Covid-19 on British businesses.

Q1 is shaping up to be a bad quarter for the UK economy

In contrast, gilt yields increased after Bank of England governor Andrew Bailey said he anticipated a pronounced economic recovery in the UK later in the year as vaccines are rolled out.

Japan trims GDP forecast

In Japan, the Nikkei rose 0.39% following the country’s first positive exports data since November 2018. The government also announced it has agreed to buy additional vaccines for 12 million people, meaning it will have enough to vaccinate more than half of the country’s population.

On the flipside, Japan’s monetary policy committee lowered its gross domestic product (GDP) growth forecast for the current fiscal year from -5.5% to -5.6%. Although it increased its growth target for 2021 from 3.6% to 3.9%, it warned that the outlook was highly uncertain.

In China, where stocks rallied following Biden’s election, forecasts revealed the economy grew by 2.3% in 2020 – a clear sign that, unlike much of the rest of the world, it has largely recovered from coronavirus lockdowns. Fourth quarter real GDP growth increased to 6.5%.

Markets show impressive resilience

Overall, global stock markets are showing remarkable resilience during the pandemic, underscoring the case for exposure to risk assets. Markets are on course for a third consecutive month of gains, and more stocks are hitting their 52-week highs.

Now, all eyes are on this week’s raft of US corporate earnings figures. Investors will be looking for insight into whether tech stocks can continue their strong growth trajectory over the coming year.

Please continue to check back for our regular blog posts and updates.

Charlotte Ennis

27/01/2021