Please see below article received from Invesco yesterday afternoon, which conveys a positive outlook for the global economy despite concerns over a ‘fourth wave’ in countries such as Brazil and India.

IMF upgraded its economic outlook

The International Monetary Fund (IMF) provided a press briefing last week, sharing recent alterations to its global economic outlook for this year. The IMF now expects the global economy to grow 6% in 2021 — the highest level of growth since 1980.1 This is an upward revision from its previous estimate in October of 5.5% growth in 2021 for the global economy.

This is a reflection of the optimism created by the discovery and rollout of effective vaccines as well as significant fiscal stimulus, which is already having a positive impact on some countries such as the United States. It dramatically revised its growth expectations for the US economy in 2021 from 5.1% to 6.4%.1 The IMF modestly upgraded its expectations for economic growth in China in 2021 from 8.1% to 8.4%.1 One key takeaway from the IMF’s press briefing is that the world is on divergent recovery paths. The US and China, the two largest economies in the world, are leading the recovery, but other countries are experiencing a far slower recovery and are not expected to reach pre-pandemic GDP levels until 2023.

Eurozone PMIs point to improvement

The final eurozone composite Purchasing Managers’ Index (PMI) reading for March was 52.5 versus 48.8 for February.2 More importantly was the final services PMI reading for March: 49.6 versus 45.7 in February.2 We saw significant improvement in a number of countries including Ireland, the UK, and Germany. And so while it’s no surprise to me that manufacturing continues to strengthen, led by manufacturing powerhouse Germany, it is surprising — and encouraging — to see the services sector improving in some countries despite rising COVID-19 infections and lockdowns.

Chris Williamson of IHS Markit explained what is happening in the euro area: “The survey therefore indicates that the economy has weathered recent lockdowns far better than many had expected, thanks to resurgent manufacturing growth and signs that social distancing and mobility restrictions are having far less of an impact on service sector businesses than seen this time last year. This resilience suggests not only that companies and their customers are looking ahead to better times, but have also increasingly adapted to life with the virus.”2

This is good news, given that the vaccine rollout in the eurozone has been disappointing. While I don’t expect a robust recovery until COVID-19 is well controlled, the PMI readings suggest the economy can still recover in an environment of slow vaccinations and higher stringency.

FOMC minutes represent a ‘have your cake and eat it too’ moment

The Federal Reserve upgraded its economic outlook — but that didn’t change its stance on accommodative monetary policy. The minutes from the March meeting of the Federal Open Market Committee (FOMC) were released last week, showing that its growth expectations for the US economy in 2021 were — similar to the IMF — upwardly revised to 6.5% from 4.2%, while unemployment expectations were revised down to 4.5% for 2021 from 5%.3 The Fed’s optimism was driven by the economic re-opening and increased fiscal stimulus. The Fed also upwardly revised its expectations for inflation, forecasting 2021 core personal consumption expenditures to increase by 2.2% — this is a substantial increase from its previous forecast of 1.8%.3

In my view, these minutes represent a “have your cake and eat it too” moment — a Fed that expects the economy to experience strong growth — but will not pre-emptively tighten as it has often done in the past. The Fed is expecting a brighter economic outlook, but wants to remain very accommodative. The minutes stated that it will be “some time before the conditions are met for scaling back the asset purchase program” — and the Fed still expects rates to remain zero through 2023.3 In these minutes, the Fed once again reiterated its plans to sit on its hands well beyond 2021, anticipating that the spike in inflation it expects this year will be transitory. Investors couldn’t ask for a nicer Fed.

We heard lots of ‘Fedspeak’

We didn’t just get the minutes from the March FOMC meeting last week. We also heard from various Fed officials. Here are the highlights:

- Last week Fed Chair Jay Powell suggested that COVID-19 infections are the biggest risk to the economy. He shared a cautionary message about the pandemic last week despite growing optimism about the economy: “Cases are moving back up here, so I would just urge that people do get vaccinated and continue socially distancing. We don’t want to get another outbreak; even if it might have less economic damage and kill fewer people, it’ll slow down the recovery.”4

- St. Louis Fed President James Bullard shared his view that the Fed should not even consider any changes to its monetary policy until we have certainty that the pandemic is over. In my view, this could further delay monetary policy normalization given that it could tether future Fed considerations to health-related accomplishments.

- Then, last night, Powell appeared on an American TV news show, “60 Minutes.” He reiterated that the principal risk to the economy is a resurgence of the pandemic. Powell stated that the US is “at an inflection point,” and he expects growth to be very strong in the back half of 2021. One important line from his interview, “The Fed will do everything we can to support the economy for as long as it takes to complete the recovery.”5

Signs of inflation in PPIs

The US Producer Price Index (PPI) rose substantially in March, exceeding expectations. However, markets barely flinched. And this rise in PPI is not specific to the US; China also experienced a big rise in producer prices. My view is that these data points are to be expected, a combination of base effects and short-term supply disruptions. However, that doesn’t mean we won’t want to follow future inflation data closely, including US Consumer Price Index this week.

Fears of a ‘fourth wave’ continue

The Fed’s concerns about COVID-19 are well-founded. COVID-19 cases are on the rise in a number of countries, most notably Brazil and India. Bruce Aylward, a World Health Organization official, described the situation in Brazil in stark terms, “What you are dealing with here is a raging inferno of an outbreak.”6 I believe concerns about infections, especially a rise in the spread of more contagious variants, will continue to be an intermittent cause of concern for markets.

So what happened in markets?

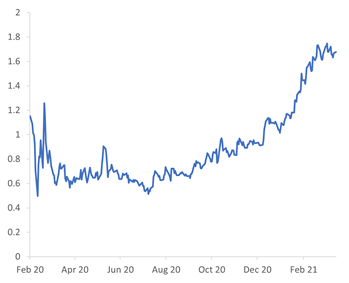

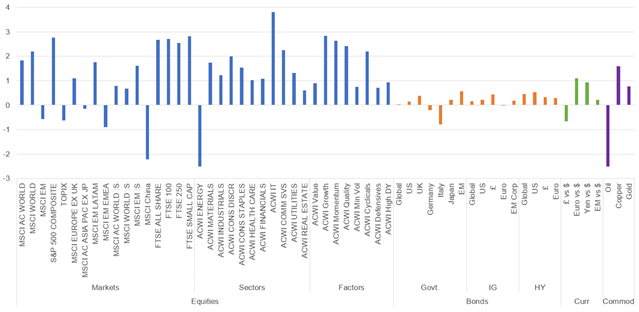

The big news is that the yield on the 10-year US Treasury backed down materially last week. This came as a surprise to many, given that the outlook for the economy continues to improve — as have expectations for inflation.

I think there are several possible reasons for this. First of all, it could be a reaction to rising COVID-19 infections in parts of the world, which could be causing investors to actually lower expectations for growth. Similarly, all this talk of rising taxes in the US could also be dampening expectations about a very strong economic recovery. Or perhaps investors are finally starting to believe the Fed when it says it will not be tightening any time soon.

Not surprisingly, because yields backed down, there was a rotation within stocks. Stocks in general made gains last week, but technology stocks and other more growth-oriented stocks — as well as larger-cap stocks — assumed positions of leadership. Going forward, I would expect a continuation of this trend: rotations in leadership tied to changes in the 10-year yield. But make no mistake — I am in the camp that expects yields to rise this year. Despite last week’s downward moves, I expect the yield on the 10-year US Treasury to reach 2% or higher this year.

Looking ahead

There is a lot to look forward to in the coming week, from US retail sales to UK gross domestic product (GDP) to the business outlook survey from the Bank of Canada. Here are a few items I am focused on:

- Eurozone retail sales. The services PMIs mentioned previously suggest that the pandemic and lockdowns don’t seem to be having as big an effect on the service sector of the economy. This data should help confirm that theory.

- Beige Book. The Fed’s “Beige Book” is chock full of anecdotal information from businesses in the different Fed districts across the country. It gives you a real sense of what they are experiencing — and thinking about.

- China GDP. China has clearly helped lead the economic recovery in the early innings. This will give us a sense of how strong that leadership has been in the last quarter, and what parts of the economy it has come from.

- Earnings season. Earnings season begins this week. Many companies abandoned guidance in the midst of the pandemic, but I am hopeful we will get more guidance this quarter. Any kind of outlook will be valuable.

- Global vaccination levels. As always, I remain most concerned about our ability to control the pandemic, and the speed with which we vaccinate populations plays a critical role. As Fed Chair Powell has made clear, he believes the pandemic is the greatest risk to the economy this year. When I went to receive my second COVID-19 vaccine yesterday, the physician’s assistant who inoculated me ominously warned me against laminating my vaccination card. She matter-of-factly explained, “You will be back periodically for boosters. This is not over.” That’s because variants are spreading, especially where COVID-19 hasn’t been controlled, and will likely make it quickly to other parts of the world. There is a funny expression in the US about the city perhaps best known for gambling and general fun that is arguably more decadent: “What happens in Vegas, stays in Vegas.” But there is no such thing when it comes to a pandemic. What happens in Sao Paolo (or New Delhi or Paris or Amsterdam or Los Angeles) doesn’t stay there. It can happen everywhere. So we need to care about vaccinations everywhere.

Please check in again with us soon for further market updates and news.

Stay safe.

Chloe

15/04/2021