Please see below this week’s Markets in a Minute update from Brewin Dolphin – received late yesterday afternoon – 13/04/2021

Equities hit new highs on hopes of sustained economic recovery

Numerous share markets hit all-time highs last week, with the S&P500 bursting further past the 4,000 mark, finishing the week comfortably in record territory at 4,129. European markets also performed strongly, as investors bet on continental economies reopening later this year despite problems with the vaccination programme. The European Stoxx600 hit a record high of 437.23 on Friday.

In the UK, confidence in the continued easing of restrictions helped the FTSE100 rally by more than 2.6%, to levels not seen since before the pandemic. Meanwhile, the more domestically focused FTSE250 surged through its previous record of 22,000.

The tech-heavy Nasdaq also recouped some of its recent losses last week, rising more than 3%, helped by a pause in rebounding bond yields. Asia was more subdued, however. Chinese policymakers are reportedly considering tightening monetary and fiscal policy to prevent the economy overheating and inflation rising too high, leading to a pullback in share prices.

Last week’s market performance*

- FTSE 100: +2.64%

- Dow Jones +1.95%

- S&P 500: +2.70%

- Nasdaq: +3.11%

- Dax: +0.84%

- Hang Seng: -0.82%

- Shanghai Composite: -0.45%

- Nikkei: +1.29%

*Data from close of business on Thursday 1st April to close of business Friday 9th April.

Shares start week on cautious note

Markets edged back from their record highs on Monday, as investors digested last week’s surge in equity markets, and looked ahead to key US inflation data out later today. It is the start of first-quarter earnings season in the US this week.

In the UK, the FTSE100 closed down 0.39% at 6,889, despite the feelgood factor accompanying the reopening of non-essential shops and pubs.

In the US, the Dow fell 0.16% at 33,745.40, while the S&P500 fell slightly, losing 0.02% to close at 4,127.99 and snapping a three-week winning run in the process. The Nasdaq fell by 0.36%. In Europe, the Stoxx600 index dropped by 0.25%, although markets in France and Germany edged up.

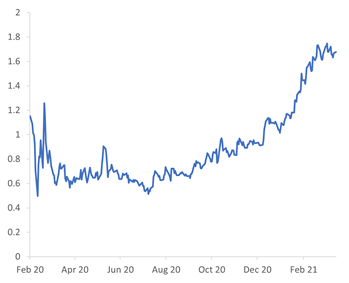

Bond yields take a breather

The yield on 10yr US treasuries started the year below 1%, but surged in the first quarter to hit 1.67%. Rising treasury yields are usually a sign of increasing investor confidence since yields move inversely to bond prices. When investors sell bonds and invest more of their portfolios in risk assets such as equities, yields rise.

However, there can come a point at which higher yields can tempt investors back into bonds to enjoy a risk-free return on their money, or to search for sectors with more upside potential, especially if yields rise too fast.

Hence, we have seen a large-scale rotation out of growth stocks and into more value-orientated, cyclical sectors during the first quarter, as evidenced by the recent correction in big tech in the US.

The pause in rising yields last week was a key factor in the strong performance in share markets over the past few days, particularly on the Nasdaq.

While yields will likely continue to rise, with 10yr treasury yields expected to hit 2% by the end of 2021, the increase is expected to be more gradual, which equity markets should find easier to digest.

US 10yr Treasury yield

Source: Refinitiv Datastream

Global growth set for record year

The International Monetary Fund (IMF) said last week that it expects the global economy to grow by 6% this year, up from the 5.5% it forecast in January.

If true it will be the fastest expansion on records going back to 1980, despite large parts of the world still being mired in the pandemic.

Also supporting the bullish outlook are the trillions in excess savings waiting to be spent around the world, an improving employment picture in the US, and the Federal Reserve’s insistence that it will not be rushed into raising rates until there is solid evidence of a sustained recovery. Minutes from the last Federal Reserve meeting suggest that there is no intention to raise interest rates until at least 2024, and even then would require firm evidence of a sustained economic recovery and inflation at or above its 2% target.

All this should support further growth in equities as long as we don’t get a nasty overshoot in inflation, and bond yields remain relatively stable.

UK economic recovery appears on track

Last week we saw a slew of positive economic data that suggests the UK economy is enjoying a healthy rebound. The ISM/Markit Purchasing Managers’ Index for the key UK services sector, which accounts for around 80% of GDP, showed business levels improving for the first time since last October, with 56.3% of respondents reporting higher business volumes in March than in February. The UK construction industry is also recovering strongly, with the construction activity index hitting a reading of 61.7, its highest level in seven years.

Another quick update from Brewin Dolphin, these updates are a good way of keeping up to speed with developments in the markets.

Please continue to check back for our latest blog posts and market updates.

Charlotte Ennis

14/04/2021