Please see below article received from AJ Bell yesterday afternoon, which provides useful tips on how to avoid scams and illegitimate investments. As scammers become increasingly more cunning and commonplace, this article is certainly a must-read.

Financial scams are depressingly common and often target people’s hard-earned pensions. This has particularly been the case since 2015, when government reforms gave savers total freedom and choice over what they do with their retirement pot from age 55.

Official estimates from the Pension Scams Industry Group suggest £10 billion has been stolen from pensions in the past six years.

Scam activity has increased during the coronavirus pandemic, with fraudsters aiming to take advantage of increased vulnerability among UK savers.

And while efforts are being made by the authorities to protect people from financial crime – including banning pensions cold-calling and giving providers more power to reject suspicious transfers – the onus remains on individual investors to protect themselves.

Here are five things you can do:

Be suspicious of unsolicited calls, texts or emails about your pension: Scams often start with a call, text or email out of the blue offering ‘help with’ or perhaps a ‘review of’ your pension arrangements. To be safe, if someone you don’t know contacts you about your pension – or indeed your finances in general – do not engage with them. If you believe someone is trying to scam you, report them to Action Fraud to help protect other investors.

Be extremely wary of anyone promising large, guaranteed returns: Another tell-tale sign of a scam is the promise of huge, guaranteed investment returns, often over relatively short spaces of time. These investment ‘offers’ take many weird and wonderful forms, while the rise in popularity of cryptocurrencies has also been an obvious target for financial fraudsters.

Only deal with regulated companies and individuals: At the heart of scams are often unregulated ‘introducers’ peddling unregulated investments. While there is nothing wrong with investing in unregulated assets, where fraud occurs these often turn out be vastly overhyped or entirely fictitious. Even where an unregulated investment is real, if you suffer losses through misselling you will not qualify for FSCS protection worth up to £85,000.

Do your due diligence: Scammers’ tactics have become more sophisticated in recent years, with ‘clone’ scams – where fraudsters impersonate a real firm to con you out of your cash – increasingly common. You can cross-check the phone number or email address provided by someone who contacts you with the FCA register to make sure they are who they say they are.

Don’t be rushed and if in doubt, speak to a regulated financial adviser: High-pressure sales tactics – such as telling someone they need to invest by a set deadline – are a classic scam tactic and should immediately set off alarm bells. Do not under any circumstances be rushed into a decision you aren’t completely happy with. If you want help with your options or are unsure what to do, consider speaking to a regulated financial adviser or visit Government-backed retirement guidance service www.pensionwise.gov.uk.

We will continue to publish articles that are relevant and useful to our clients. Please check in with us again soon.

Please see below an article from Invesco which was published on Tuesday and received yesterday afternoon:

Please continue to check our Blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.

Please see below for Brewin Dolphin’s latest markets in a minute article, received by us yesterday evening 27/04/2021:

Most major stock markets declined last week on fears that rising Covid-19 infections could hinder economic recovery.

With Europe firmly in the grip of the so-called ‘third wave’, the pan-European STOXX 600 ended the week down 0.8%, while Germany’s Dax fell 1.2% and France’s CAC 40 declined 0.5%. The UK’s FTSE 100 slid 1.2%, with positive economic data failing to lift investors’ spirits.

Rising infections also weighed on Japan’s Nikkei, which dropped 2.2% after the country reported nationwide daily infections of more than 5,000 for the first time in three months. This led to another state of emergency being declared in several prefectures.

US stock markets posted small declines last week after President Joe Biden announced proposals to nearly double taxes on capital gains for those earning more than $1m a year. In contrast, Chinese stock markets posted solid gains following strong inflows from Hong Kong via the Stock Connect trading programme.

Last week’s markets performance*

FTSE 100: -1.2%

S&P 500: -0.1%

Dow: -0.5%

Nasdaq: -0.3%

Dax: -1.2%

Hang Seng: +0.4%

Shanghai Composite: +1.4%

Nikkei: -2.2%

* Data from close on Friday 16 April to close of business on Friday 23 April.

European stocks gain on travel plans

UK and European stocks rose on Monday after European Commission president Ursula von der Leyen told the New York Times that inoculated Americans will be able to visit the EU in the summer. The STOXX 600 added 0.3% and the FTSE rose 0.4%, with shares in easyJet, Ryanair and TUI all posting strong gains.

In the US, the Dow slipped 0.2% whereas the S&P 500 and the Nasdaq rose 0.2% and 0.9%, respectively. Tesla started a busy week of corporate earnings statements, reporting a 74% surge in quarterly revenues. Apple, Microsoft, Amazon, Alphabet, Boeing and Ford are all due to release first quarter results this week.

HSBC and BP were in focus at the start of trading on Tuesday, with the former posting a 79% rise in first quarter pre-tax profit, and the latter receiving an earnings bump from higher oil prices and a surge in revenue from natural gas trading. The FTSE 100 opened flat ahead of the US Federal Reserve’s two-day policy meeting.

UK economy shows signs of rebound

Last week saw the release of several pieces of economic data that suggest the UK economy is starting to rebound from the Covid-19 crisis. Friday’s IHS Markit/CIPS flash composite PMI showed a strong revival in private sector output following the downturn seen at the start of 2021. The index rose to 60.0 in April from 56.4 in March – the strongest overall rise in private sector output since November 2013.

For the first time since the pandemic began, service activity growth outperformed manufacturing production growth. The service sub-index rose from 56.3 to 60.1, marking the fastest pace of expansion for more than sixand-a-half years. The manufacturing sub-index increased from 58.9 to 60.7, the highest since July 1994.

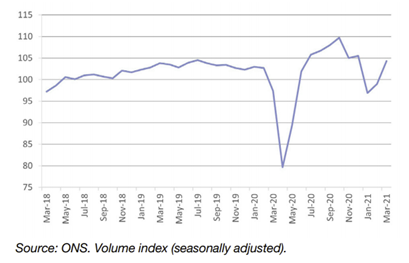

Separate data from the Office for National Statistics (ONS) showed UK retail sales volumes continued to recover in March, increasing by 5.4% from the previous month. This reflected the easing of Covid-19 restrictions on consumer spending. Sales were 1.6% higher than in February 2020 – the month before the pandemic struck.

UK retail sales surge 5.4% in March

Non-food stores provided the largest positive contribution to the monthly growth, with increases of 17.5% and 13.4% in clothing stores and other non-food stores, respectively. Fuel retailers reported monthly growth of 11.1%.

However, the ONS said retail sales for the quarter were subdued overall. In the three months to March, sales fell by 5.8% when compared with the previous three months because of tighter lockdown restrictions.

US economy moving to post-pandemic state

Last week’s flurry of US corporate earnings reports suggest the economy is starting to transition to life after the pandemic. Most notably, Netflix announced it had added just under four million subscribers in the first quarter – missing its forecast of six million. The company said it expected one million paid net additions for the second quarter – versus ten million in the second quarter of 2020, when it benefitted from a surge in demand at the beginning of the crisis.

Elsewhere, figures showed US weekly jobless claims fell to their lowest level since the onset of the pandemic, declining by 39,000 to 547,000 in the week ending 17 April. This was far better than the 617,000 figure. forecast by analysts.

US existing home sales declined by 3.7% between February and March to a seven-month low, largely because of the acute shortage of houses on the market. Compared with a year ago, when home sales first started to fall when the pandemic hit, sales were 12.3% higher. Limited supply and strong demand pushed the median existing home sales price by a record-breaking annual pace of 17.2% to an historic high of $329,100, the National Association of Realtors said.

Eurozone manufacturing enjoys record boom

Over in the eurozone, business activity in April experienced its fastest rate of increase since July 2020, thanks to record expansion in manufacturing output and a return to growth in the service sector. The composite PMI rose from 53.2 in March to 53.7 in April, according to IHS Markit’s preliminary ‘flash’ reading, which is based on around 85% of final responses to the survey.

Manufacturing output grew for a tenth straight month, expanding at a rate unsurpassed in more than two decades of survey history. The service sector continued to lag because of Covid-19 restrictions in many member states, but still reported the first expansion of activity since August 2020, rising from 49.6 in March to 50.3 in April.

Please continue to utilise these blogs and expert insights to keep your own holistic view of the market up to date.

Please see the below article from JP Morgan received yesterday, 26/04/2021:

The concept of sustainability is rapidly rising up the agenda within the fashion industry. Yet while consumers are increasingly interested in sustainable fashion, they are not willing to pay a premium for it. Still, sustainability can be a competitive advantage. We have seen companies delivering a sustainable message, but identifying the true leaders from the potential greenwashing takes research.

Consumers care about sustainabilty, but not at any price

As the global population grows, the negative environmental impacts of our demand for fashion are becoming more apparent. The industry is responsible for 10% of global carbon emissions and 20% of global wastewater, as well as producing significant amounts of waste. The equivalent of one garbage truck of textiles is dumped in landfill or burned every second.

75% of consumers view sustainability as ‘extremely’ or ‘very important’ in their fashion purchasing decision. And over 50% of consumers would switch for a brand that acts in a more environmentally and socially friendly way. But in practice, are consumers really willing to pay? Not yet, it seems. Only 7% of consumers say sustainability is the most important factor in their decision making.

Exhibit 1: Consumers care about sustainabilty, but not at any price – most important factors in decision making

Consumers continue to rate ‘high quality’ and ‘good value for money’ as the most important factors in their decisions. This is backed up by our engagements with fashion companies, who claim that consumers are not willing to pay a premium for sustainability, although at the same price point they would choose the more sustainable offering.

To us, this signals that consumers have a preference for sustainability and it can be a competitive advantage for retailers. But companies need to see it as a way to maintain or grow their market share rather than a way to increase prices. Sustainable leaders should be investing in innovation and scale for sustainable solutions to bring prices down and maintain their brand position.

Case study 1

Re:NewCell: Driving down costs for sustainability in fashion

Re:NewCell is a Swedish company driving down the costs of sustainable materials through innovation. The company has developed and patented Circulose, a high quality material made from recycled clothes. We expect Circulose – which has already been adopted by the likes of H&M and Levi’s – to see increasing uptake within the fashion industry, helping to lower the cost of sustainable materials and improve the industry’s environmental footprint.

Case study 2

Adidas: Leading the charge on sustainability

Adidas, the well-known sportswear brand, is at the forefront of sustainability within the fashion industry. The company particularly stands out on circularity, which is embedded in its strategic priorities: by 2024, Adidas has committed to replace virgin polyester with recycled polyester. The company already partners with the environmental organisation Parley for the Oceans to use recycled polyester made out of plastic collected from the coastline. All of Adidas’s cotton is sustainably sourced via the Better Cotton Initiative, earning Adidas the top spot in a 2020 independent ranking on sustainable cotton sourcing. Adidas has committed to reducing greenhouse emissions across its entire value chain by 30% between 2017 and 2030, and then achieving climate neutrality by 2050. As a further validation of Adidas’s sustainability efforts, these goals were submitted for external verification by the Science Based Target initiative in February 2020.

Sources: Adidas and the Sustainable Cotton Ranking 2020 (77 companies).

The companies above are shown for illustrative purposes only. Their inclusion should not be interpreted as a recommendation to buy or sell.

Distinguishing the real from the fake

The fashion industry is highly fragmented, and sustainability standards are still in their infancy. More and more companies are reporting on both their environmental and social impacts. But with different companies focusing on different disclosures, metrics and measurement methodologies, how can we identify the best? For us, fundamental research and company engagement are key, allowing us to assess whether fashion brands are paying lip service to sustainability or whether they are truly committed to it.

What do we look for in a sustainable fashion leader?

Has the company signed up to measurable targets to reduce its negative environmental footprint?

Is the company abiding by external certifications to demonstrate the sustainability of its products?

Is the company accurately measuring and reporting its entire carbon footprint?

The last of these requires particular research focus as only about 5% of a fashion retailer’s carbon footprint comes directly from its own operations (scope 1 emissions) or indirectly from generating the energy used by the company (scope 2). The vast majority of carbon emissions occur in the company’s value chain (scope 3). This includes production, processing and transportation of fibres and fabrics, transportation of the end product to its final destination, and emissions related to use, care and disposal. Unsurprisingly, this complexity means that emissions are currently underreported, with many companies only reporting on transportation of the end product. Fundamental research is therefore key to understand the supply chain picture and determine what companies are really doing to reduce their total emissions.

Conclusion

While price sensitivity remains key for consumers in the fashion industry, evidence points to sustainability becoming more important in purchasing decisions and ultimately to long-term brand value. This implies a material opportunity for sustainable leaders to stand out while unsustainable fashion brands lose out. Yet the potential for greenwashing is rife in the industry, making it difficult to distinguish between leaders and laggards in the transition to sustainable fashion. Company research and engagement is key.

Our Comments

This is another example of sustainability and ESG themes filtering down to everyday life.

The fashion industry, particularly the problematic ‘fast fashion’ companies seem to hit the headlines on a regular basis for all sorts of issues, from waste to poor working conditions so the sustainability of the fashion industry is starting to be questioned more often.

With fund managers now also becoming increasingly more concerned with ESG and sustainability issues, the fashion industry will have to also adapt to these changes in the way consumers and investors are thinking and what it is they are looking for when investing or purchasing their products.

Shopping for items such as clothes became pretty much an online only occurrence for a large proportion of the past 13 months, I have myself noticed that sustainability is being used a selling point, whether it be statements on the companies website or even noted in the products description. Some companies plant a tree for every item of clothing purchased.

As this article highlights, a lot of people would consider switching to more environmentally and socially friendly brands, but they may not be willing to pay an extra premium for it. Personally, I don’t think it will be long until paying extra won’t be an issue, as the world changes and now has ESG principles under a microscope, these companies will have to adapt to remain competitive in the marketplace.

From a personal experience perspective, I recently purchased an item of clothing having no idea it was part of a ‘sustainable’ line until I was checking the label for the washing instructions only to find out that the item was made out of 100% recycled plastic bottles and textile waste that had been processed and melted down into new fibres in an effort to save water, energy and reduce greenhouses gases.

The item was no more expensive than a ‘non sustainable’ item and the quality was probably better than products that use ‘virgin’ or non-recycled materials.

As consumers, if you don’t have to compromise on cost or quality, then why wouldn’t you choose more sustainable options?

Please see below article received from AJ Bell yesterday morning, which provides analysis of the current market landscape and discusses potential investment opportunities.

As regular readers will know, one of this column’s favourite market sayings comes from fund management legend Sir John Templeton, who once asserted that: ‘Bull markets are founded on pessimism, grow on scepticism, mature on optimism and die on euphoria.’

Applying this test can potentially help investors spot where value and future upside opportunities can be found. It can also help avoid areas which are so popular they could be overvalued and capable of doing damage to portfolios.

It is hard to avoid investments everyone is talking about with great excitement and resist ‘fear of missing out’. Yet history suggests looking at assets, stocks or funds no one is interested in is the best way to make premium long-term returns.

The last 12 months are a fine example of how some careful, but not wilful, contrarian research could have yielded rich rewards. As the pandemic began to make its presence felt, share prices plunged, oil collapsed into negative territory and government bonds’ haven status meant their prices rose and yields fell. Cryptocurrencies were tossed aside amid the general panic, too.

Yet wind on a year, and equities have beaten bonds hands down, with commodities not far behind. Technology is no longer the leading equity sector and defensive areas such as healthcare are relatively out of favour. Commodities (with the notable exception of precious metals) are doing well and cryptocurrencies are going bananas, as evidenced by the flotation of America’s leading crypto exchange just last week, namely Coinbase.

Studious analysis of these trends may therefore help investors to spot value and dodge the traps that the coming 12 months and beyond may offer.

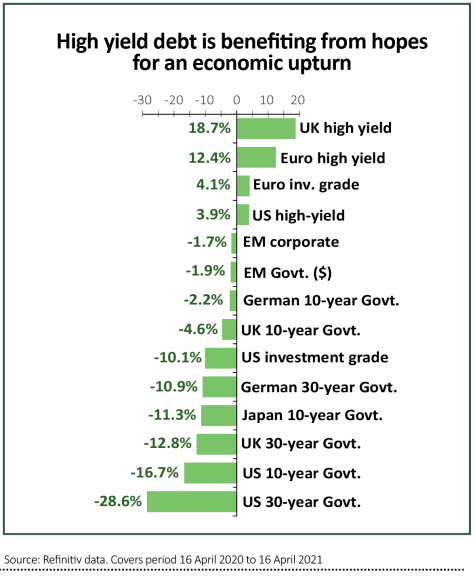

UP, UP AND AWAY

Incredible as this would have seemed a year ago, ‘risk’ assets are showing the best total returns in sterling-denominated terms over the 12 months, as equities and commodities easily outpace bonds. Within fixed income, the riskiest option – high-yield corporate paper – continues to lead government and investment-grade corporate debt.

Within equities, Asia and Japan are doing best, perhaps owing to the relatively limited impact of Covid-19 upon their populations’ health and their economy.

Emerging markets overall are coming in from the cold (in another win for contrarians), and America’s dominance of the geographic performance tables is waning a little, too.

By equity sector, it felt like technology was the only game in town a year ago, with defensive areas like healthcare also proving popular. Yet cyclical, turnaround sectors now lead the way, with defensives and income-generating bond proxies lagging badly.

All of this fits the prevailing narrative that the combination of vaccination programmes, government fiscal stimulus and ultra-loose monetary policy from central banks will see the economy through the pandemic and provide a firm base for a robust economic recovery.

So too do the losses on long-duration government bonds and the outperformance of high yield debt. The latter tends to correlate more closely to equities than it does fixed income. A strong economic recovery would help to bring financially stretched firms back from the brink and leave them better placed to meet their obligations.

NEXT STEPS

Analysis of those performance statistics means this column currently sees the major asset classes like this as we head into summer 2021, using Sir John Templeton’s four phases as a framework.

Euphoria – and optimism – are a lot easier to find than they were a year ago. This is not to say that markets are primed for a collapse, but it may not take much to shake them up a bit as a result.

Scepticism pervades fixed income and government debt, so anyone who fears disinflation or deflation more than inflation could take this as a cue to top up allocations.

Conversely, anyone who sees the world returning to normal pretty quickly could seek out value on commercial property stocks or funds, especially those with exposure to office space, while those portfolio builders who are wary of a market wobble – and suspect that central banks will respond with every greater monetary largesse – may note with interest the underperformance of gold and miners of precious metals.

Please check in with us again soon for further updates and news.

Diversification and capital appreciation are two major goals for many crypto investors.

Reward potential is tempered by volatility

Bitcoin has had a meteoric rise, but when prices fall, they have tended to fall hard.

A cautious approach may be warranted

For those who want to invest, I would urge them to consider classic investment tenets such as diversification and regular rebalancing.

It’s about that time again — time to write another blog about cryptocurrencies. Not surprisingly, I received a deluge of client questions on cryptos last week given the Coinbase IPO and the record highs bitcoin reached earlier in the week (followed by the steep pullback in prices over the weekend).

Of course, the most common question I get is, “Should my portfolio have an allocation to bitcoin?” This is not dissimilar to the questions I got back in late 2017 when bitcoin was on a tear and there was a lot of media coverage of it. However, what’s different this time is that not only retail investors are asking me these questions but so are institutional investors.

The critical question about cryptos

When considering the inclusion of any asset class in one’s portfolio, we must ask the simple question: What will this asset bring to the portfolio? For an alternative asset class — investments beyond traditional stocks and bonds — usually the primary goal is diversification.

Historically, bitcoin has had a low correlation with traditional asset classes such as the S&P 500 Index. For example, from Jan. 1, 2011, through March 31, 2021, the correlation between bitcoin and the S&P 500 was 0.15. However, as bitcoin has become increasingly popular, that correlation has increased, hitting a much higher 0.66 for the period of Jan. 1, 2020, through March 31, 2021. This suggests that bitcoin may no longer offer as much in the way of diversification benefits as it previously did. However, that does not mean that other cryptocurrencies will not offer diversification benefits.

Of course, capital appreciation potential can be an important goal as well, and bitcoin has had a meteoric rise from just $314.50 on Jan. 2, 2015, to a new high of more than $64,000 early last week. And bitcoin could potentially move far higher if more retail and institutional investors choose to include it in their portfolios. However, it has also experienced extreme volatility and major drawdowns, as evidenced by the significant drop it experienced last week — after hitting that all-time high, it quickly fell to less than $54,000.

Potential investors need to recognize this risk/reward profile. Since 2011, bitcoin has spent 93.6% of days trading beneath its highs. This compares favorably to gold, which over the same time period spent 98.4% of days trading beneath its highs, and compares unfavourably to the S&P 500 Index, which spent 86.6% of days trading beneath its highs. But importantly, on days when bitcoin was beneath its highs, it was trading on average 53.5% below its highs. By contrast, when gold was trading beneath its highs, it traded on average 25.6% below its highs, and for the S&P 500, that number was 3.8%. In other words, when bitcoin prices fall, they tend to fall hard. Other cryptocurrencies have also had strong price appreciation — and have been similarly volatile with substantial drawdowns. In other words, cryptocurrencies have historically offered significant reward and significant risk.

Other reasons for wanting to own alternative asset classes may include the ability to hedge inflation and the ability to hedge geopolitical risk. For example, some investors add gold to their portfolios in an attempt to hedge inflation, even though historically gold has only sometimes been an effective hedge against inflation. Because cryptocurrencies are relatively new, there is no long track record we can examine to determine whether any have historically offered these properties. It will remain to be seen if cryptocurrencies can provide hedges for such risks.

Four additional crypto considerations

Just a few other considerations investors should be aware of:

Regulation. First of all, there is the potential for regulation of cryptocurrencies. Now that is not necessarily a bad thing. For example, regulation could increase confidence in investing in cryptocurrencies. However, it could also mean additional costs, which could depress the prices of cryptocurrencies. Moreover, extreme regulation could result in the shuttering of local crypto exchanges and a ban on the use of cryptocurrencies.

The environment. Bitcoin is not the most environmentally friendly investment. Bitcoin averages around seven transactions per second, and each one requires a substantial amount of electricity: 951 KWh per transaction.3 I could envision some institutional investors coming under pressure from groups demanding divestment of environmentally unfriendly investments such as bitcoin. The good news is that other major cryptocurrencies use far less electricity.

Competition. Other than being the first successful cryptocurrency and a pioneering invention coinciding with the birth of blockchain, there is not much that makes bitcoin special. Other cryptocurrencies share some similarities with bitcoin, and it may very well be possible that as bitcoin approaches its terminal supply amount, another cryptocurrency that is more technologically advanced and efficient takes its place. This perspective complicates the exercise of asserting a long-term value to bitcoin.

Liquidity. Investors can be overwhelmed by the number of cryptocurrencies out there — it can be difficult choosing which ones to invest in. I suggest focusing on the largest cryptocurrencies given they are the most liquid: in addition to bitcoin, that includes ethereum, ripple, litecoin and perhaps a few others. However, investors should research the different attributes of each of these cryptocurrencies.

So, should bitcoin be in a portfolio?

And so for every client who asks me whether they should add bitcoin to their portfolio, I respond “it depends.” It depends on risk tolerance, investment goals and other factors. For those who believe cryptocurrencies are suitable for investment, I would urge them to consider a small allocation and to perhaps diversify among a number of major cryptocurrencies, since each has different characteristics. And I would favor diversification with other alternative asset classes such as gold and real estate. Regular rebalancing may also help investors to methodically take profits on upward price movements, and to take advantage of price swings lower, and active management should help as various cryptocurrencies rise and fall in investor popularity.

Cryptocurrencies seem to always be in the headlines, whether it’s Bitcoin’s meteoric rise or its rapid falls.

This article from Invesco is more about using Bitcoin as a diversifier than a direct investment and its important to note that Bitcoin and other cryptocurrencies are still more of a gamble than an investment.

Please see below ‘Markets in a Minute’ article received from Brewin Dolphin yesterday evening. The commentary provides an update on market performance as it reacts to current global news events.

Most major stock markets rose last week as the start of the US earnings season helped to offset concerns about a resurgence in Covid-19 infections.

The pan-European STOXX 600 added 1.2%, marking its seventh consecutive week of gains. Germany’s Dax rose 1.5%, despite chancellor Angela Merkel warning that the country was firmly in the grip of the third wave of the pandemic. The FTSE 100 advanced 1.5% after official data revealed the UK economy grew by 0.4% in February following a 2.2% contraction in January.

In the US, the S&P 500 gained 1.4% with healthcare and mining stocks performing particularly strongly. The release of earning results from several banking giants also helped to boost investor sentiment. The Dow added 1.2% and the Nasdaq gained 1.1%.

Over in Asia, the Nikkei ended the week down 0.3% amid a spike in coronavirus infections in Tokyo and Osaka. China’s Shanghai Composite fell 0.7% whereas Hong Kong’s Hang Seng managed a 0.9% gain.

Last week’s market performance*

FTSE 100: +1.50%

S&P 500: +1.37%

Dow: +1.18%

Nasdaq: +1.09%

Dax: +1.48%

Hang Seng: +0.94%

Shanghai Composite: -0.70%

Nikkei: -0.28%

*Data from close on Friday 9 April to close of business on Friday 16 April.

Dull start to the week as investors take profits

US stocks pulled back from record highs on Monday as investors took profits ahead of the peak of the earnings season. The S&P 500, the Dow and the Nasdaq closed down 0.5%, 0.4% and 0.9%, respectively. Nearly half of S&P 500 companies are set to release their first quarter results over the next two weeks, including the majority of the FAANGs.

European stocks also retreated slightly from record highs, following the weaker open in the US and rallying currencies. The FTSE 100 dipped 0.3% yet managed to stay above the 7,000 mark after figures from Rightmove revealed UK house prices rose by 2.1% in April to a record high of £327,797. This marked the second time in only five years that prices have increased by more than two percentage points in a month.

The FTSE 100 was down 0.4% to 6,972 in early trading on Tuesday following mixed employment data from the Office for National Statistics. The unemployment rate fell slightly from 5.0% in January to 4.9% in February, but 56,000 workers were cut from company payrolls in March – the first monthly drop since November.

UK economy expands in February

Last week saw the release of encouraging economic data in the UK. Official figures showed the economy grew by 0.4% in February as companies prepared for the easing of coronavirus restrictions. Growth was helped by the first rise in factory output since November, and a pickup in sales among wholesalers and retailers.

The data also suggested that trade between Britain and the EU partially recovered in February. Goods exports to the EU fell by 12.5% year-on-year in February, versus a 41.4% year-on-year decline in January. Imports declined 11.5% year-on-year in February, compared with a 19.2% drop the month before.

Despite this, UK GDP remained 7.8% below its level in February 2020, shortly before the pandemic struck. It was also 3.1% lower than its level in October, just before further lockdown restrictions hit the services sector.

Non-essential shops and outdoor hospitality venues reopened on 12 April, and it is hoped most restrictions will be lifted before the end of June.

US consumer spending rebounds

Over in the US, figures showed retail sales grew by an eye-catching 9.8% in March, far higher than the 5.8% monthly increase that analysts were anticipating. This followed the continued reopening of restaurants and retail, and a recovery from the severe weather-induced 2.7% contraction in February.

Meanwhile, weekly jobless claims plunged to their lowest level since the pandemic began, and a key gauge of factory activity in the mid-Atlantic region hit its highest level in nearly five decades.

US inflation data revealed headline consumer prices rose by 0.6% in March from the previous month and by 2.6% compared with the same period a year ago. The year-on-year gain was the highest since August 2018. Gasoline prices were the biggest contributor to the monthly increase, surging by 9.1%.

China sees record growth

China’s economy achieved year-on-year growth of 18.3% in the first quarter of 2021 – the biggest jump since the country started keeping quarterly records in 1992. Industrial production rose 14.1% year-on-year, while retail sales surged by 34.2%.

However, the headline growth figure was skewed by the huge economic contraction witnessed in the first quarter of 2020, when China imposed a nationwide lockdown at the peak of the Covid-19 outbreak. On a quarterly basis, China’s GDP grew by a far smaller 0.6% – well below expectations and slower than the revised 3.2% expansion recorded the previous quarter.

We will continue to publish further analysis and input as the UK enjoys an easing of lockdown restrictions. Please check in again with us soon.

Please see article below from Legal & General’s Asset Allocation team received yesterday afternoon – 19/04/2021

Our Asset Allocation team’s key beliefs

Questions of geography

We will address just two topics this week. First, looking at the global numbers, the pandemic is once again intensifying with cases and deaths sadly reaccelerating. But have markets become immune to bad news on the virus? Second, bond yields fell last week despite inflation and growth both surprising on the upside. We think a small island chain in the Caribbean holds a clue to the newfound resilience of the Treasury market.

Is the COVID-19 threat receding? It depends where you live

Looking at recent economic data, it is easy to conclude that the COVID-19 crisis is fast receding in the rear-view mirror. Last week, we learned that China’s GDP grew by 18% year-on-year in the first quarter and that US retail sales jumped by an extraordinary 28% year-on-year in March. Such annual comparisons are flattered by the base effects from the collapse in activity this time last year, but the sense of economic renaissance is palpable.

In the OECD, vaccination programmes have started to bear fruit. Even the EU, which has been infuriatingly slow to roll out its vaccine programme, is now getting its act together and vaccinating at roughly at the pace of the US in mid-February. The EU is on track to hit its target to inoculate 70% of the adult population by September. The main change is in Germany, where the country’s 35,000 GP practices are now permitted to administer shots, rather than just 430 centralised vaccination hubs. A little decentralisation goes a long way.

At the global level, however, there is sadly little sign of the pandemic slowing down. The virus is still raging in emerging markets, with Brazil and India suffering from their darkest days since the crisis began. Headlines of 150 million cases worldwide are likely only a few weeks away.

Does this matter for global markets? At the aggregate level, we think the answer is no. We’ve stuck to a positive medium-term outlook on equities despite these virus dynamics. It’s always important to remember that markets are a discounting mechanism. Notwithstanding the staggering death toll from COVID-19 (nearly three million and counting), investors are collectively capable of looking through today’s ongoing pandemic to the prospect of normalisation tomorrow.

Caribbean clue to the CPI conundrum

On top of the strong growth numbers mentioned above, US inflation rose by more than economists’ consensus expectations in March. Core CPI rose by 0.34% month-on-month (versus the expected +0.2%) and 1.65% year-on-year (versus the expected +1.5%). Several of the beaten-up components climbed slightly on the month, but still remain depressed with scope to rise significantly over the next few months as the economy opens.

In the coming months, we expect core inflation (on both CPI and PCE) to peak around 2.5% year-on-year. There are strong base effects which we believe make a rise above 2% inevitable. In addition, there are reopening effects with some prices normalising and supply-chain disruptions boosting components such as used-car prices. Finally, demand-pull inflation from stimulus spending could add to upward inflation pressure. It is plausible that core inflation could even reach 3%.

Despite that upside news, and the prospect for stronger inflation ahead, Treasury yields have fallen over the course of the past couple of weeks. One explanation comes from Treasury International Capital System data released last week, which revealed that investors domiciled in the Cayman Islands have made net sales of $400 billion of US Treasuries in the 12 months through to February. Not bad for a small island chain with a population of 70,000!

What’s going on here, and why is it relevant? It is estimated that over 80% of the world’s hedge funds are registered in the Cayman Islands and the size of the net sale suggests that a sizeable short base has built up in what is euphemistically referred to as the “fast-money community”.

The message on positioning from these data are matched by a similar story from the options market and surveys of investor sentiment. Having worried about COVID-19 for 12 months, institutional fund managers now say they worry most about inflation and a bond-market tantrum.

Yet in the words of General George S. Patton, “If everyone is thinking alike, then somebody isn’t thinking.” Consensus bets can sometimes pay off, but they are vulnerable to small changes in sentiment having an outsized impact. The size of the short base is now such that the reflationary narrative needs to be constantly buttressed by new information to keep yields moving up.

The bar for taking short duration positions just got that little bit higher.

Please continue to check back for our latest blog posts and market updates.

Please see below an article published by Money Marketing today, which was written by Rachel Vahey, a Senior Technical Consultant from AJ Bell. This article highlights some of the key considerations of the proposed changes to the Normal Minimum Pension Age moving from age 55 to age 57:

I think the above article helps highlight some of the key factors that will need to be factored in when considering possible pension consolidation exercises or general pension switches. It could be that to switch your pension to a new provider in the future could mean you losing a minimum pension age of 55 under the existing contract and instead not being able to access your pension benefits until age 57.

There are a few questions clients will have to consider with their I.F.A., which are:

When do I realistically anticipate drawing pension benefits?

How do I want to draw benefits from my pension? and

Does this change (in minimum pension age) really impact on my plans?.

The reality is that you need a lot of capital to retire early and for the majority of people it’s not an option.

Another key issue that needs to be considered is that some old-style legacy pensions cannot facilitate Flexible Access to pension funds and instead force you to either purchase an Annuity or encash the pension.

All of the above really need to be weighed up very carefully before making any decision and taking financial advice will help you consider your own situation.

It remains to be seen how the government will implement the proposed changes and what the potential fallout could be, but we will keep you fully updated with any changes that are announced.

Please continue to check our Blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.

Please see article below from Quilter Investors received yesterday afternoon – 15/04/2021

The need to diversify

Quilter Investors chief investment officer, Bambos Hambi, explains why private investors need to diversify across different asset classes and different geographies.

Over the last 30 years or more, while the ‘average’ retail investor (if there is such a thing) has undoubtedly become more investment savvy, investment markets and the fund strategies that draw upon them have taken a quantum leap in both size and sophistication. Consequently, the chasm between the two has probably never been greater.

Even today, too few private investors really understand the need to diversify their savings across different asset classes and geographies and how this impacts the risks to which their financial futures are subject.

Given the constant media barrage, it’s hardly surprising that investor ‘champions’ such as the ‘FAANG’ stocks – namely Facebook, Apple, Amazon, Netflix and Google (Alphabet) – arise. A previous investor acronym that once attracted similar attention is the ‘BRICS’, which stood for Brazil, Russia, India, China and South Africa.

While both helped attract huge levels of new investment, anyone who plumped solely for these investment areas will have experienced a bumpy ride. By contrast, the essence of diversifying across a range of different risk categories is that it smooths the investment journey, enabling us to make more reliable plans for our financial futures.

Spinning the wheel

Many people still think of diversification in terms of eggs and baskets, but it’s a flawed analogy. In reality, the risk of concentrating your savings into a few leading tech stocks, or a group of ‘hot’ emerging markets, is much more akin to walking into a casino, putting your ‘egg’ on one number and spinning the roulette wheel.

A better analogy is to think of diversification in terms of cooking. Imagine an array of different pots bubbling away. While each one will come to the boil at different points, delivering the desired outcome, each could also boil over, or just go cold, if left unattended.

This is where a multi-asset portfolio manager comes into play. It’s their job to stir each ‘pot’ and see that it receives the right amount of heat, at the right time, to achieve the desired end result.

Over the last 30 years or more, investment markets and fund strategies have taken a quantum leap in both size and sophistication.

Active not reactive

Having a fully resourced portfolio manager at the helm is important because, as the table (see the pdf at the bottom of this page) shows, different asset classes and regions respond to economic events in different ways. Accounting for this requires constant monitoring, analysis and position refinements at the portfolio level.

Take UK property as an example. In terms of investment returns for the 11 asset classes listed in the table, UK property had yo-yoed from last place in 2016, to first place in 2018 and back to last again by 2019.

Meanwhile, UK equities, which have never placed higher than fifth in the last 10 calendar years, proved to be the worst performing asset class of 2020, thanks to the onset of the pandemic and the last thrashes of the Brexit farrago.

By contrast, the pandemic, and the speed with which China was able to deal with its fallout, helped to propel Chinese equities into first place in 2020. They were also the best performing asset class in 2017 (but the worst in 2018).

Creating solutions

Thanks to our scale and reach as an investment business, we begin with a universe of many thousands of different strategies and fund structures and whittle it down to find the ‘best of breed’ in each space.

This means our portfolio managers and investment teams spend the majority of their time researching, analysing and modelling to find those managers who can demonstrate the most consistent returns for the level of risk with which we’ve entrusted them.

As dedicated portfolio managers, we have two key advantages over investors who decide to manage their own investments. The first is the time, expertise and expense required to actively monitor global markets, to decide which asset classes are best suited to the conditions and to identify those managers that consistently do the best job in each asset class.

The other great advantage we have is access. Unlike private investors, we have access to a huge swathe of investment managers and strategies from around the world covering every major equity and bond market. Often we invite proven managers to create dedicated funds (called mandates) that are run especially for us.

We also have access to a whole universe of fund strategies that either aren’t available to UK investors, are too sophisticated for private investors or which require minimum levels of investment that put them far beyond the reach of ordinary investors. This is especially so in the case of so-called ‘alternative investments’.

Alternative thinking…

The term ‘alternative investments’ covers an enormous global investment industry that’s all but closed to private investors. Alternative investment funds cover the widest range of asset classes from commodities like gold and oil to other ‘real assets’ such as commercial property, infrastructure and renewable energy.

They also include hedge funds that invest in all manner of asset classes but which, thanks to the complex derivative strategies they employ, can pursue all manner of different instruments. Many of these focus on generating returns that have a low ‘correlation’ to those of equity or bond markets, others focus on delivering consistent ‘absolute returns’ whatever the investment environment.

Having access to such diversity allows us to reduce the correlation of our holdings both with one another and with major global equity and bond markets. This means that if, say, a global pandemic broke out and sent equity markets into steep decline, as was the case in 2020, other holdings, not correlated to equity markets, could take up the strain.

Unlike private investors, we have access to a huge swathe of investment managers and strategies from around the world covering every major equity and bond market.

Diverse times

Recent months have provided ample illustration of the need to properly diversify portfolios.

The unprecedented events of 2020 ended with one of the greatest relief rallies on record, thanks to news of three viable coronavirus vaccines. Within this, ‘value stocks’ that had been in the shadow of ‘growth stocks’ for almost a decade began to outperform as investors rotated into those areas previously left behind (see the inset box).

Only weeks later, the headlines were dominated by news of rocketing government bond yields and major losses for bond investors as markets began to price-in ‘reflation’ – the period of rising prices and growth that tends to follow a period of ‘deflation’ (falling prices and growth), like the one caused by lockdown.

On the whole, reflation is a welcome sign for long-term investors like us, as it shows that an economic recovery is well underway and that improving economic growth lies ahead. However, bond markets naturally recoil at the prospect of the higher inflation and interest rates that might accompany it.

Not only did lower-risk bond investors feel this in the pocket, but investors at the other end of the risk spectrum, namely, higherrisk ‘growth investors’ in equities, also suffered. The so-called FAANGs and other leading tech companies were among the early casualties.

This is because growth stocks tend to struggle with the risk of higher interest rates and inflation; as a high level of their predicted profits lies in the future, the prospect of higher interest rates reduces their value today.

While all this was going on, smaller companies began to outperform as they tend to enjoy reflation.

These issues (and too many more to mention) have already exposed investors with too little diversification to significant volatility and potential losses so far in 2021. .

This underlines the ‘smoothing’ benefits of a well-diversified, global portfolio. When changes in the economic cycle or the broader tapestry of society take hold, the diversified investor doesn’t need to ‘run out’ and find a solution because it’s already simmering away somewhere in their portfolio.

Understanding ‘value’ and ‘growth’

In general terms, ‘value’ investment approaches target those companies regarded as looking cheap relative to the value of their assets (also known as their ‘intrinsic’ or ‘book’ value). Value stocks tend to be well-established businesses, which often offer high levels of dividend.

Good examples of value stocks include banks, oil and mining, utility and industrial companies although any company whose valuation is below the market average is technically regarded as a ‘value stock’.

Meanwhile, ‘growth investing’ is more focused on capital growth than on collecting dividends. Growth stocks tend to be younger or smaller companies whose earnings are expected to increase faster than those of other companies in their industry sector or the broader market.

They tend to pay limited dividends as they are busy reinvesting their profits in growing their businesses.

Growth stocks are most commonly found in the technology sector with companies like the ‘FAANGs’ the most prominent example of recent years.

Other ‘cyclical’ areas (meaning companies most impacted by the economic cycle) such as consumer goods, leisure and travel or the automobile sector often contain ‘growth’ stocks. The same is true of areas like biotech.

Ultimately, any company with a disruptive business model, ground breaking new technology or an irresistible new line of consumer goods can find itself classified as a ‘growth’ stock if its earnings growth starts to outpace the broader market.

As companies mature and become more established in their industry niche, they naturally evolve from being growth companies into being value companies. That is, until they bring something new to the market, at which point the cycle can begin all over again.

Interesting input from the CIO at Quilters. A lot of this is what we discuss daily with our clients. We need diversification by assets, geography, and styles. Good strong ‘Active’ and ‘Tactical’ fund management helps too, particularly in volatile markets.

As IFAs we use a wide range of investment options for our clients to meet their objectives and risk profiles. We have a myriad of choice.

Please continue to check back for our latest blog posts and market updates.