Please see below an article from Invesco which was received late Friday (22/10) afternoon and covers their views on inflation in the US:

As you can see from the above, inflation remains a hot topic. Although market consensus states that inflation is transitory, Invesco’s view is that this ‘transitory inflation’ could last for up to 3 years or more. This is something we will continue to keep an eye on and also see how this translates to UK inflationary pressures. Many of the supply chain issues are global.

Please continue to check our Blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.

Please see below for Brooks MacDonald’s Daily Investment Bulletin, received by us late yesterday 21/10/2021:

What has happened

US and European equities continued their recent run of positive days with a small gain in the US leaving the index only a fraction away from its all-time high set in September. US earnings were, again, the driver of this upswing with around two-thirds of companies reporting yesterday beating expectations.

COVID-19

With the recent pickup in cases, headlines filtered through yesterday from across the globe. In Russia, President Putin has mandated a ‘non-working’ firebreak between the 31st October and 7th November whilst the Czech Republic has mandated the wearing of masks in indoor spaces. In New York City, municipal workers will need to show proof of vaccination to continue in their roles with the option of showing a negative test no longer available. Global governments appear to be taking one of two paths as cases increase in the northern hemisphere, either enacting restrictions now or doubling down on their vaccination/booster strategy. In the UK, weekly average cases have now risen to 45k per day with the Health Secretary yesterday urging citizens to register for vaccinations and for booster jabs ahead of the winter period.

Inflationary pressures

Whilst equities recorded another strong day yesterday, sovereign bonds remained under siege due to inflationary concerns. Oil prices hit another high for the year after reports from the US EIA pointed to falling inventories of both crude oil and gasoline. US 10 year inflation breakevens are now sitting at 2.6%, their highest level since 2012. Fed Speakers have been keen to push back against market expectations for interest rates, which are now running far ahead of the latest Fed dot plot from September. Fed Governor Quarles said yesterday that whilst he sees ‘significant upside risks’ to inflation, that his base case sees US inflation heading towards 2% next year. Quarles also addressed the elephant in the central bank room, saying that a demand/supply imbalance is not best addressed by curtailing demand via tighter monetary policy, describing such an approach as ‘premature’.

What does Brooks Macdonald think The market has fully priced in one rate hike in the US in 2022 with a second hike three-quarters priced in. The first step on the Fed’s monetary normalisation process will be the tapering of pandemic quantitative easing programmes so this will buy some time for the Fed to settle on the exact timing and pace of rate hikers, in the interim the Fed wants to avoid the market pricing in too rapid a tightening.

Please continue to utilise these blogs and expert insights to keep your own holistic view of the market up to date.

Please see below Brewin Dolphin’s latest market summary, which was received late yesterday (20/10/2021) afternoon:

Global equities rose last week on the back of better-than[1]expected US retail sales and encouraging employment figures.

The S&P 500 and the Dow gained 1.8% and 1.6%, respectively, following a 0.7% jump in US retail sales in September and a decline in weekly jobless claims.

In Europe, the STOXX 600 surged 2.7% amid an encouraging start to the US earnings season. The FTSE 100 added 2.0% with airlines among the strongest performers after the US announced it would ease travel restrictions from 8 November.

Japan’s Nikkei 225 clawed back losses from the previous week to finish up 3.6%, as investors took comfort from new prime minister Fumio Kishida’s comments that he would not increase capital gains tax for the time being.

Last week’s market performance*

• FTSE 100: +1.95%

• S&P 500: +1.82%

• Dow: +1.58%

• Nasdaq: +2.18%

• Dax: +2.51%

• Hang Seng: +1.99%

• Shanghai Composite: -0.55%

• Nikkei: +3.64%

* Data from close on Friday 8 October to close of business on Friday 15 October.

Wall Street mixed as China GDP disappoints

Wall Street stocks gave a mixed performance on Monday (18 October) following disappointing gross domestic product (GDP) figures from China. The Dow slipped 0.1% whereas the S&P 500 and the Nasdaq gained 0.3% and 0.8%, respectively, as bond yields rose and data showed China GDP grew by 4.9% in the third quarter from a year ago, below the 5.3% growth expected by economists.

The sombre mood continued in London, where the FTSE 100 fell 0.4%. Figures from Rightmove showed average UK house prices jumped by 1.8% in October from the previous month – the biggest rise at this time of the year since 2015. On an annual basis, the average asking price is up 6.5% to £344,445. Meanwhile, the two-year gilt yield soared to its highest level since May 2019 – a sign that traders expect UK interest rates to rise soon.

The FTSE 100 was flat at the start of trading on Tuesday as investors awaited more earnings reports from the US.

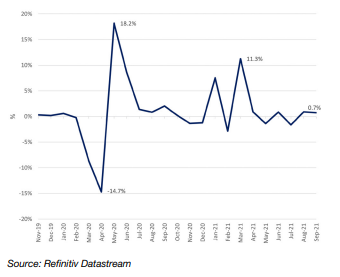

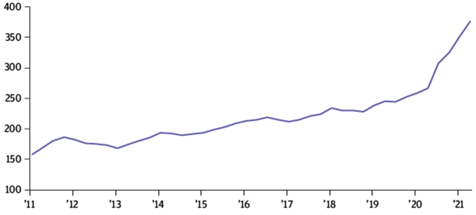

US retail sales surge as prices rise

Figures released by the Census Bureau last week showed US retail sales jumped by 0.7% in September, far better than the 0.2% decline expected by economists. Compared with a year ago, sales were up by 13.9%.

US retail sales – MoM change

The increase came as the government ended the enhanced benefits it had been providing during the pandemic. It was thought this would depress sales, but instead spending accelerated as workers and students returned to offices and schools.

Much of the increase was driven by higher prices, as US retail sales figures are calculated according to receipts as opposed to volume. Indeed, separate data showed inflation, as measured by the consumer price index (CPI), rose by 5.4% in September from a year ago, slightly higher than the 5.3% increase expected by analysts. On a monthly basis, prices increased by 0.4%, following a 0.3% rise in August. Core CPI, which excludes food and energy, rose by 4.0% from a year ago – well above the Federal Reserve’s 2.0% target.

Meanwhile, the University of Michigan’s consumer sentiment index slipped in early October to 71.4 from a final reading of 72.8 in September, suggesting consumers remain anxious despite spending more.

UK GDP rises by 0.4%

Here in the UK, figures showed GDP grew by 0.4% in August from the previous month, as the hospitality industry benefitted from the first full month of coronavirus restrictions being lifted in England. Accommodation and food service activities were the main contributor to growth in the services sector, rising by 10.3%. This was followed by arts, entertainment and recreation, up 8.5%. Despite the increase, the Office for National Statistics (ONS) said GDP remains 0.8% below its pre-pandemic level, while consumer-facing services are 4.7% below their pre-pandemic level.

Investors were also cheered by data that showed UK employers added 207,000 staff to their payrolls last month, shortly before the end of the furlough scheme. This meant the number of payrolled employees surged to 29.2 million – the highest level since records began in 2001. However, the unemployment rate for June to August was an estimated 4.5%, higher than the 4.0% rate seen before the pandemic.

Germany’s GDP forecast slashed

Over in Europe, Germany’s GDP forecast for 2021 was slashed last week by a group of economic research institutes. The group’s biannual report said the German economy would grow by 2.4% this year, down from its previous forecast of 3.7% growth. The researchers said the reduction was driven by the ongoing impact of Covid-19 on the service sector, and continuing supply chain issues. GDP is expected to grow by 4.8% in 2022, assuming the pandemic and supply chain disruptions are resolved.

Supply chain issues are affecting the eurozone more broadly, with industrial production falling in August by 1.6% from the previous month. Eurostat said one of the steepest declines was in Germany, where output dropped by 4.1%

Please continue to check our Blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.

Please see below article received from Brooks Macdonald yesterday afternoon, which provides a succinct update on current market behaviour.

Global equities fell in September as inflationary pressures remained elevated and on further signs of a global economic slowdown. Continued anxiety about a possible bond default by Chinese property group China Evergrande also rattled markets. Major central banks, particularly the US Federal Reserve (Fed), drew closer to the point of tightening monetary policy. The news boosted the US dollar while yields on government bonds generally rose. Supply disruptions and drops in US crude stocks helped oil prices hit the highest levels in almost three years.

UK stocks declined as increasing energy costs, supply chain issues, (which led to motor fuel shortages) and worries about an economic slowdown dampened sentiment. Increasing pricing pressures – the annual inflation rate leapt to 3.2% in August from 2.0% in July – added further gloom. The Bank of England signalled that it could bring forward its plans to increase interest rates as it raised its inflation target. The UK’s second-quarter GDP growth was revised up to 5.5% from 4.8% previously, although the economy expanded by just 0.1% month on month in July.

US equities dropped on concerns about a weakening economy and moves by Democrats to raise corporate taxes. Inflation remained relatively high – consumer prices rose by 5.3% year on year in August, down slightly from 5.4% in July – further dampening the mood. The Fed turned more hawkish, with Chairman Jerome Powell hinting that the process of winding back the central bank’s asset purchases, known as ‘tapering’, could begin as early as November.

European markets were lower as worries about the economic recovery, the debt problems at Evergrande and high inflation unsettled investors. The European Central Bank said it would slow bond buying under its pandemic emergency purchasing programme over the rest of 2021. It insisted the move did not amount to tapering as it warned that the economic recovery remained nascent. The eurozone’s GDP growth over the second quarter was revised up to 2.2% from 2.0% previously.

Japanese stocks strengthened as the resignation of Prime Minister Yoshihide Suga sparked hopes that his successor would implement new fiscal stimulus measures. Former foreign minister Fumio Kishida was, by month end, expected to become the country’s new leader after winning a Liberal Democratic Party leadership contest. The continued roll-out of COVID-19 vaccinations, after a slow start compared with other developed countries, further boosted the market. Japan’s second-quarter GDP growth was revised up to 1.9%, on annualised basis, from 1.3% previously6.

Asia-Pacific equities (excluding Japan) weakened on concerns about a global economic slowdown. In China, worries about a weakening economy and Evergrande’s debt problems and power shortages (which shut a number of factories) dragged down stocks. The prospect of a slowdown in China also hurt Taiwan’s market. South Korean stocks declined as technology companies faced the threat of tightening regulations, sparking a sell-off in the economically important sector. Rises in COVID-19 infections hurt investor confidence in Australia and Singapore.

Emerging markets were down, overall, as the strengthening US dollar weighed on sentiment. India’s market remained strong, however, as the continued roll-out of COVID-19 vaccinations underpinned confidence in the economy’s recovery. Increased buying by foreign equity investors added further support. Brazilian shares fell sharply as disaffection over the leadership of President Jair Bolsonaro – and his defiance in the face of a number of scandals – increased political tensions. Russia’s market made gains as it benefitted from increases in energy commodity prices, while Turkish stocks slumped as the central bank surprised investors with an interest rate cut, despite concerns about soaring inflation. South African equities came under pressure from the stronger US dollar.

Yields on core government bond markets generally increased. The yield on US benchmark 10-year Treasuries rose (prices fell, reflecting their inverse relationship) as the Fed moved closer to tightening monetary policy, sparking a sell-off towards month end. The yields on UK 10-year gilts and German 10-year bunds also gained, although the latter remained in negative territory. In the corporate debt market, US investment-grade and high-yield spreads tightened.

We will continue to publish relevant content as we approach Halloween and edge nearer to the festive season.

Please see the below article received by Legal & General late yesterday afternoon:

Quid Game

The Bank of England has signalled it’s getting ready to move, although battle lines were drawn last week as Silvana Tenreyro and Catherine Mann, both members of the MPC, voiced opinions against a rate hike. Nonetheless, there is an overall hawkish tone coming from Threadneedle Street. That has clearly been reflected in rates, with gilt yields moving higher even more aggressively than their international counterparts – both at the short end and further out.

The same cannot be said for the pound. Although interest-rate differentials are low today, such changes in expectations usually drive some currency movement, too. But the energy crisis, rising inflation and a lower growth outlook have kept sterling at bay; across the pond, rising yields and a risk-off environment have helped the US dollar dominate virtually all other currencies. The enthusiasm for dollars is also reflected in various measures of investor sentiment and positioning.

With supportive valuations, we think the combination of market dynamics and valuation warrants a trade, so we are moving to a more preferential view on the pound against the dollar. To diversify the idiosyncratic risks from picking one currency, we also have positive views on the Australian dollar and euro against the US dollar. Even though the fundamentals for each currency look a little different, they share the common factor of light positioning versus the greenback.

The Fed’s Gambit

Last week’s US CPI print of 0.2% confirms our view that we’re reaching the middle-game for the current inflationary spike. With the initial spike from the reopening of the economy potentially winding down, the Federal Reserve (Fed) is much more focused on the breadth of the current shock. In that regard, the 0.5% jump in median CPI is concerning. Some broader measures are already elevated and, if the others follow suit, that could bring forward Fed action. Our economists and the markets expect the first rate hike in late 2022, though there’s a strong consensus that the risks are skewed heavily towards an earlier lift-off, rather than a delay.

The Fed is gambling that labour market participation will pick up, providing a release valve for wage pressure and limiting the risk that consumers’ rising inflation expectations lead to higher pay and ultimately into an ugly endgame where rate hikes are needed to stop price rises from spiralling out of control. The growing risk is that there has been a negative structural shock to labour supply through a combination of retirements and people re-evaluating their work/life balance. With unemployment down to 4.8%, despite disappointing payroll data, we would need to see a rapid return of workers to alleviate this concern.

Considering the above, we are moving back to a negative view on US rates after a few weeks on the sidelines. A challenge to this position is that investor sentiment indicators point to a widespread consensus short view on rates, though not an extreme one.

As regular readers know, we don’t like to join the herd too often. We lean against another widely held position by taking a short US inflation view against the market’s overall long predisposition; if necessary, then we’d expect the Fed to act, reducing the risk of a prolonged spike in inflation pricing 5-10 years in the future. Higher today, lower tomorrow.

Peso Blinders

There are several currencies known as the peso in the Americas, and we are revisiting our stance on Chile’s versus its Colombian counterpart. We are bullish on the Chilean peso and, where possible in portfolios, short the Colombian peso.

The recent performance of the Chilean peso has been poor, but with reason in our view; the Chilean economy is overheating. Loose fiscal and monetary policy has caused the current account to deteriorate, inflation to rise, and the peso to underperform. Chile’s recent central-bank action to hike the policy rate by 1.25% is an important signal that it is keen not to see further currency weakness. Politics in Chile is messy, but it’s the same in Colombia and the whole continent has been leaning left in recent years.

Finally, while not a driver of the trade, Chile is massive exporter of copper, which could see a tailwind in case the metal’s price rises on the back of the global decarbonisation drive.

Combining these factors gives us confidence to take a position. The Chilean peso adds risk to our portfolios but, combined with a trade against Colombia, we believe it becomes more of a diversifier.

Please continue to check back for a range of blog content from us and from some of the world’s leading fund management houses.

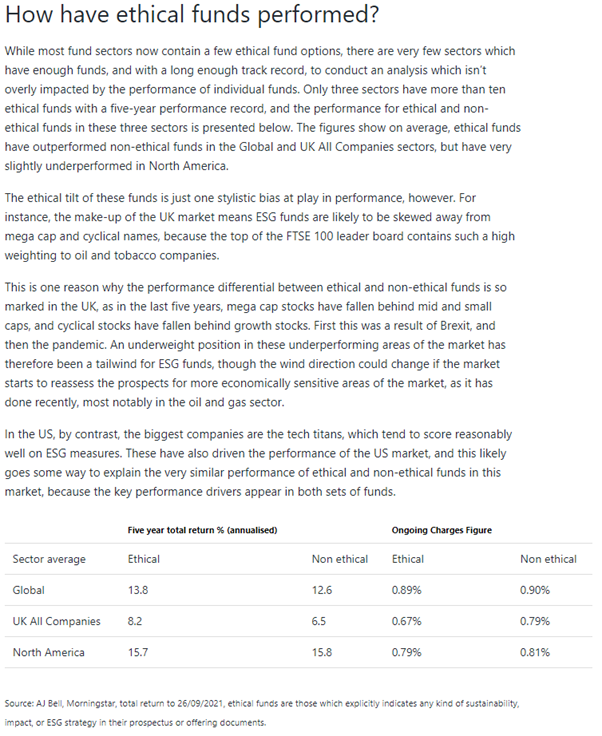

Please see below an article from A.J. Bell which was received yesterday (17/10) and covers their views on Environmental, Social and (Corporate) Governance investing:

As you can see from the above article, ESG investing is certainly becoming more mainstream, and this theme ties into what we are seeing and hearing from other fund management companies too.

One question I am most typically asked by my clients when we discuss ESG investing is, ‘Will I have to compromise on investment returns to be an ethical investor?’ and I believe the above article demonstrates that this is not the case.

It has been suggested that in the future, ESG investing may actually become the default investment offering with investors specifically having to ‘opt out’ of this type of investment strategy.

ESG investing is certainly an area to keep an eye on in the future. We believe it is a great option.

Please continue to check our Blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.

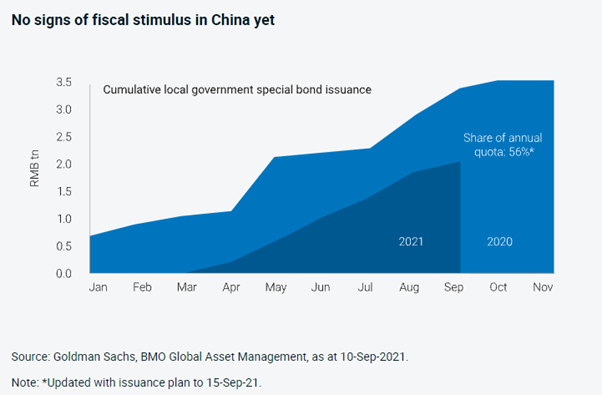

Please see article below from BMO Global Asset Management – received yesterday 14/10/2021

Steven Bell monthly update – Investing in the time of COVID

Despite the success of vaccines, the virus may put pressure on hospitals in the northern hemisphere as winter sets in; these are headwinds for equities and we could see a 5-10% correction before year end.

The global economic recovery has run into a string of supply shortages, from natural gas to key workers to silicon chips. Inflation has risen. Central banks still maintain that it is temporary, but the pressures are such that the Bank of England and US Federal Reserve may have to raise rates earlier than the market had expected. Despite the success of vaccines, the virus may put pressure on hospitals in the northern hemisphere as winter sets in; these are headwinds for equities, and we could see a 5-10% correction before year end. But the longer-term outlook for risk assets is positive with a notable capex boom likely to boost productivity and corporate earnings.

• Vaccination rates are higher in Europe but the indoor season is approaching for northern countries too, so expect another wave of hospitalisations. • The UK is enjoying an improvement in new cases, new hospital admissions haven’t risen as fast as expected recently, especially in England. But there are still far more people in hospital with Covid in the UK on a per capita basis than most European countries. Double the number in France and five times those in Italy, Germany and the Netherlands. • Covid precautions have reduced the number of available beds in the UK by 6,000, and we started off with fewer beds per capita than most other developed market countries. The crisis here is far from over. • The crisis at Evergrande is a symptom of a wider structural change. China is weaning itself off a credit-fuelled construction boom with Beijing preferring ‘quality’ over ‘quantity’ in terms of economic growth. • An energy crisis is leading to shutdowns in key sectors; the economy is slowing. • A policy response is coming but it has been delayed by inflation concerns and the desire to avoid further fuelling excessive credit growth.

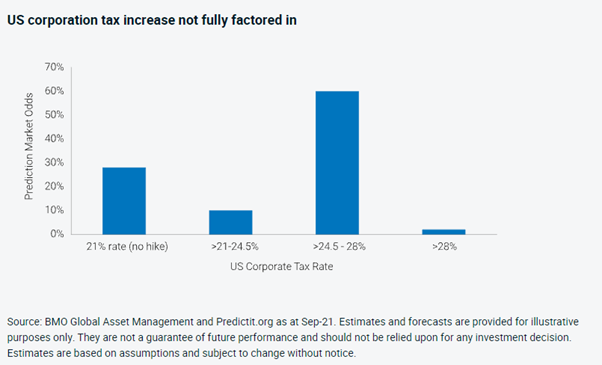

• Used car and car rental prices have started to ease in the US, signalling that some bottleneck price pressures are beginning to ease. • Having increased over the past 12 months, US inflation expectations have now stabilised at around 2%. • But signs of a pick-up in wages suggest that either profit margins are squeezed or that inflation could stay high for longer. • Although analysts forecasts for Q3 US company earnings look too low, they also haven’t fully factored in the impending corporation tax increase, and earlier-than expected rate hikes due to rising wages will squeeze profit margins. We could see a 5-10% correction in markets before year end. • Equity markets have stumbled recently as developed market central banks have suggested that official interest rates could be headed higher sooner than markets expect. • However, a boom in capex orders in the US and elsewhere is a major positive for the longer term, boosting productivity and corporate earnings.

Please continue to check back for our latest blog posts and updates. Charlotte Clarke 15/10/2021

Please see below Daily Investment Bulletin received from Brooks Macdonald yesterday, which provides a pertinent update on the markets, with reference to supply shortages and transitory inflation.

What has happened

US and European equity indices recorded small losses as investors looked ahead to today’s US CPI release and the start of the US earnings season. There was plenty of movement within government bond yields with the US 10-year Treasury yield now off its recent highs, trading at 1.58% ahead of the key inflation data point today.

Fedspeak and inflation

Vice Chair Clarida will shortly end his term at the Federal Reserve but yesterday signalled that the time was approaching for a tapering announcement. Clarida followed the transitory inflation narrative but recognised market concerns that inflation risks are now poised to the upside rather than the downside. Atlanta Fed President Bostic, who is known to harbour more hawkish views, said that price pressures were spreading amongst the CPI basket and that they looked more entrenched than previously believed. Today’s CPI figures are the last inflation release before the Federal Reserve considers monetary policy in their November meeting. Market expectations are for Core CPI to hold steady at 4% year on year and for CPI to also mirror the last release at 5.3%. It will take some months for the recent run up in energy, used cars and commodity prices to come into the data which may mean a downside miss on these numbers is shrugged off by a more hawkish market.

Apple and Semiconductors

One of the highest profile shortages during the pandemic has been semi-conductors and yesterday Bloomberg reported that Apple was struggling to acquire sufficient chips to meet its iPhone production targets. There was hope in recent months that more supply would come online to meet the surge in demand however this is yet to filter through to production creating fears that the problems will continue well into 2022. A lack of availability of chips has also catalysed another leg higher in used car prices over the last month and looks set to continue to cloud the inflation picture for Q4.

What does Brooks Macdonald think

The chip shortage is reducing the supply capacity of most technology hardware suppliers and auto manufacturers. The shortage risks reducing economic output as well as creating inflation which will place further pressure on central banks to raise rates ahead of the risk of stickier inflation.

Please check in with us again soon for more relevant content and news.

Please find below, an update received from Brewin Dolphin yesterday, on how the increase in prices for wholesale gas have impacted stock markets.

Most major stock markets ended last week in the green after a volatile few days that saw wholesale gas prices hit record highs.

The S&P 500 gained 0.8% as the rise in UK and European gas prices boosted energy stocks. The Dow ended the week up 1.2%, with stocks rallying on Thursday amid reports that the Senate had passed a bill to raise the debt ceiling and enable the government to keep paying its bills through early December.

The pan-European STOXX 600 and the UK’s FTSE 100 both added 1.0% as fears about the impact of rising energy prices eased throughout the week.

In contrast, Japan’s Nikkei 225 slumped 2.5% on concerns that new prime minister Fumio Kishida would increase capital gains tax in an attempt to rectify wealth disparities.

Last week’s market performance*

• FTSE 100: +0.97%

• S&P 500: +0.79%

• Dow: +1.22%

• Nasdaq: +0.09%

• Dax: +0.33%

• Hang Seng1 : +1.07%

• Shanghai Composite2 : +0.67%

• Nikkei: -2.51%

* Data from close on Friday 1 October to close of business on Friday 8 October.

Closed Friday 1 October.

Closed Friday 1 October to Thursday 7 October.

Wall Street slips on inflation concerns

US indices fell on Monday (11 October) as fears about inflation and supply chain constraints continued to weigh on investor sentiment. The S&P 500, Dow and Nasdaq all lost 0.7% as the surge in oil prices fuelled concerns about tighter monetary policy. In contrast, the FTSE 100 gained 0.7%, boosted by strong performance in its large mining sector.

UK and European indices started Tuesday in the red, with the FTSE 100 and the STOXX 600 down 0.8% as investors mulled the latest UK jobs data. Figures from the Office for National Statistics showed that while unemployment fell to 4.5% in the three months to August, vacancies rose to a record high of 1.2 million, indicating that companies are struggling to fill jobs.

Investors are looking ahead to this week’s US inflation and retail sales figures, and for any signs of ‘stagflation’ – a period of high inflation and unemployment coupled with slow economic growth.

Wholesale gas prices soar

UK wholesale gas prices hit a new all-time high on Wednesday, surging by nearly 40% in just 24 hours. High global demand and reduced supply has seen prices soar this year, resulting in several UK energy firms collapsing. Prices subsequently fell back after Russia’s president Vladimir Putin said the country would help to ease the crisis by boosting supplies to Europe.

UK gas prices Markets

There are concerns higher prices will lead to unaffordable bills for some businesses, especially those requiring heat as part of their production processes. This could result in lower production, factory closures and unemployment. Businesses could also pass on higher energy bills to consumers, thereby squeezing household finances.

Europe has also seen rising gas prices, but European Central Bank president Christine Lagarde said last week that policymakers should not ‘overreact’ to rising energy prices or supply shortages because ‘our monetary policy cannot directly affect those phenomena’. Minutes of the ECB’s September meeting, reported by the Financial Times, showed some policymakers were concerned about ‘upside risks’ to inflation and had called for a bigger cut in asset prices than was ultimately decided. Policymakers said inflation could exceed the ECB forecasts ‘if a different path materialised for oil prices’ and if supply chain issues lasted longer than expected.

US payrolls miss expectations

Last week also saw the release of the closely watched US nonfarm payrolls report, which showed payrolls rose by 194,000 in September – well below the Dow Jones estimate of 500,000. This followed an upwardly revised gain of 366,000 in August, according to the Labor Department.

Several newspapers are speculating about whether the jobs report could encourage the Federal Reserve to start tapering its support for the economy. The Fed previously said it would continue its current asset purchasing programme until there was substantial further progress on two goals: inflation averaging around 2% and maximum employment.

Although the headline payrolls figure missed expectations, other aspects of the jobs report were more positive. For example, whereas the number of Americans on government payroll fell by 123,000, there was a 317,000 increase among those on private payrolls, suggesting hiring strength in the private sector. Meanwhile, the unemployment rate fell to 4.8%, the lowest since February 2020 and better than the expected 5.1%.

New Japanese PM takes office

Over in Asia, Fumio Kishida, who won the leadership race for Japan’s ruling Liberal Democrat Party, was confirmed as the country’s new prime minister. This was thought to be one of the reasons behind last week’s slump in Japanese stocks, with investors rattled by suggestions that Kishida might push for an increase in capital gains tax. On Sunday, however, Kishida announced that he had no such plans for the time being, and that he would pursue other steps to rectify wealth disparities first. To view the latest Markets in a Minute video click here

Please continue to check our Blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.

Please see the below article from JP Morgan received yesterday morning:

Environmental, social and governance (ESG) factors have all grown in importance for investors in recent years. But the S in ESG – the social factor – has, until recently, often played second fiddle to environmental considerations.

This neglect is understandable, because what makes up the social factor – how well companies treat their employees, suppliers and customers – is harder to measure than performance on the environment or in governance. Nonetheless, failing to pay heed to the social factor is a mistake because there appears to be some correlation between social performance and share price performance.

The benefits of happy employees

One way to measure this correlation is by looking at Glassdoor, the website where employees anonymously rate employers. Over the past 10 years, the share prices of companies ranked in the top fifth in Glassdoor ratings have outperformed companies ranked in the bottom fifth by over 6%. Glassdoor provides useful quantitative and qualitative evidence, so it can help open the door to engagement with management on social issues. We used Glassdoor, for example, to start a conversation with a management team about issues employees were raising on the platform. This prompted a productive discussion with senior executives about what they thought they could do to address these issues.

Exhibit 1: Glassdoor versus returns

This glassdoor model is a proprietary neural network, which was trained to forecast future financial performance from content in Glassdoor reviews. The model was trained in an expanding window manner, using 5 million reviews from more than 5,000 unique publicly-traded companies, covering the time period from 2008 to present. For more information please refer to footnote.

Another example of how employee satisfaction can contribute to a better company is Rentokil Initial, a British pest-control and hygiene company. The company has a strong culture of listening to employees; this has likely contributed to its high employee retention rate of 85%. Importantly, customer retention is equally high at 86%, supporting the idea that happier employees produce more satisfied customers because the workers tend do their jobs better.

The value of customer service

Treating customers well is another social factor that can also have an impact on company performance, as evidenced by the recent issue of travel refunds thrown up by the pandemic. Customers who booked directly with a hotel or airline found it easier to secure a refund than if they had booked through a third party. We believe that this may translate into an increase in direct bookings, which allows us to try to capture and quantify the differences in customer service by feeding these expected new booking trends into our earnings growth estimates.

Diversity in focus

Treating employees and customers well is one way companies are taking the social factor more seriously. The corporate sector, as a whole, also seems to be paying more attention to social factors. For example, since early 2020 there has been a sharp rise in the number of management mentions of diversity and inclusion in the earnings calls of companies in the MSCI All Country World Index.

Exhibit 2: The importance of social issues in ESG investing

Corporate mentions of “diversity”/“inclusion” in earnings calls

Number of mentions for MSCI ACWI companies, four-quarter moving average

Studies have started to examine the impact diversity on corporate performance. A 2018 study by McKinsey found that companies in the top quartile for gender diversity on executive teams were 21% more likely to outperform on profitability and 27% more likely to have superior value creation, while companies in the top quartile for ethnic/cultural diversity on executive teams were 33% more likely to have industry-leading profitability.

Conclusion

We believe increased corporate focus on social factors will ultimately be good for productivity, economic growth and – in the long term – corporate profits and share prices. We see much for investors to celebrate in the future if the social factor is good for share prices.

Comment

Its an interesting area to improve businesses in the UK. For large corporates like Rentokil Initial, you can see how they can drive change through the business. Is this more challenging for smaller companies?

Keep checking back for our usual market updates, insights and ESG related content.