Please see below for one of AJ Bell’s latest articles received by us yesterday 10/10/2021, looking at the importance of the US Dollar to Global Markets:

The International Monetary Fund’s quarterly Composition of Official Foreign Exchange Reserves report may not be everyone’s idea of bedtime reading but one trend immediately emerges from the latest data. The dollar is still – slowly – falling from favour as the globe’s reserve currency with non-US central banks.

As of June 2021, the dollar represented 59% of global exchange reserves, only a fraction above December’s 25-year low and way down from this century’s 73% peak, reached in 2001.

The creation of the euro may have something to do with this and the rise of the Chinese renminbi may be another, while the US may not have helped its cause with rampant deficit creation and money printing since 2009 (even if it is not on its own in either respect).

This has perhaps tempted some central banks to sell dollars in exchange for something else (gold or other currencies), because the greenback trades well below its early-century highs, as measured by the trade-weighted DXY index. The so-called ‘Dixie’ benchmark currently stands at 94 compare to its 2002 peak (for this century) of 120.2.

This may feed into the ‘demise of the dollar’ narrative that is popular with some economists and investors (even if that neglects the lack of credible alternatives, especially as the Chinese renminbi still represents just 2.6% of global foreign reserves). Yet for all of that, the DXY index trades at its highest mark for 2021 and all market participants, not just currency traders, will know that attention must be paid when the US currency starts to make a move, up or down.

Dollar dynamic

Two asset classes are particular sensitive to the dollar, at least if history is any guide.

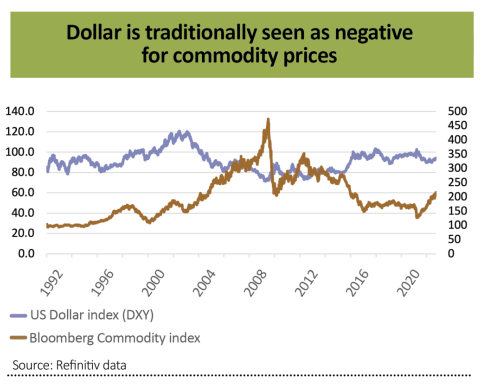

The first is commodities. All major raw materials, except cocoa (which is traded in sterling) are priced in dollars. If the US currency rises then that makes them more expensive to buy for those nations whose currency is not the dollar or is not pegged to it and that can dampen demand, or so the theory goes.

While the past is by no means a guarantee for the future, it can be argued that there is an inverse relationship between ‘Dixie’ and the Bloomberg Commodity Price index.

The second is emerging equity markets. They do not appear to welcome a strong dollar either, judging by the inverse relationship which seems to exist between the DXY and MSCI Emerging Markets benchmarks. Dollar strength at the very least coincided with major swoons in EM, or at least periods of marked underperformance relative to developed markets, during 1995-2000 and 2012-15. Retreats in the greenback, by contrast, appeared to give impetus to emerging equity arenas in 2003-07, 2009-12 and 2017-18.

This also makes sense, in that many emerging (and frontier) nations borrow in dollars and weakness in their currency relative to the American one makes it more expensive to pay the coupons and eventually repay the original loans.

Sovereign defaults are thankfully few and far between in 2021 – Suriname and Belize are the only ones that spring to mind – but a rising dollar could put more pressure on potential strugglers whose credit ratings continue to slip, notably Tunisia.

Bouncy buck

But before investors jump on the dollar bandwagon – and to conclusions – it must be worth asking why the US currency is back on a roll, and there are a couple of possibilities here.

The first is risk aversion. It may seem strange to say this as so many equity markets trade at or near all-time highs and so many sub-classes of the bond market offer record-low yields, but it may not be entirely a coincidence that the S&P 500 index has just served up its weakest month since the outbreak of the pandemic.

China’s regulatory crackdown, and signs of an accompanying economic slowdown, may be tempting some investors to seek out a haven asset and the dollar, as the globe’s reserve currency, still fits that bill.

The good news here is that the DXY index is nowhere its all-time high of 160 in the mid-1980s (a situation that was only resolved by 1985’s Plaza Accord, when the G5 unilaterally revalued the deutschmark, as they were then, against the US currency), let alone that 120 peak of 2002, but substantial further dollar gains could be a warning of a market dislocation of some kind.

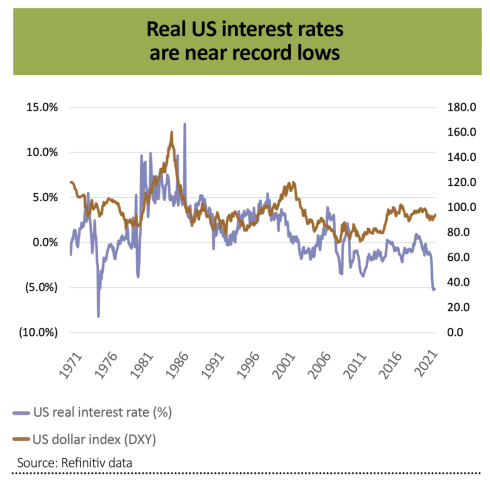

The second is US monetary policy. Whether you believe it or not, the US Federal Reserve is again discussing the prospect of tapering quantitative easing and raising interest rates in either 2022 or 2023.

Real US interest rates, adjusting for inflation, are as deeply in negative territory now as they have been for 50 years, thanks to record-low interest rates and a 5.2% inflation reading. History suggests a move upward, either due to lower inflation, higher borrowing costs or both, could boost the buck.

Yet the sensitivity of the emerging markets and commodity prices to sharp moves in the dollar suggests the Fed will have to move carefully, as the US central bank will not wish to cause – or be blamed – for the sort of upset which is now known as 2013’s taper tantrum. If monetary policy does become less loose, it seems sensible to expect higher volatility at the very least.

Please continue to utilise these blogs and expert insights to keep your own holistic view of the market up to date.

Please see below an article from A.J. Bell, which was received late yesterday (07/10/2021) afternoon which cover their thoughts on what effect rising bond yields will have on stocks:

As you can see from the above, rising interest rates aren’t necessarily a bad thing for cash assets and banks, although, this will lead to debt becoming more expensive. I believe that this will be something the UK Government will be reluctant to implement until absolutely necessary. Cheap debt is what has helped the Government support the country financially during the Covid pandemic.

Another thing to note is that if interest rates do increase, growth stocks could become less attractive as investors seek investments that have a higher equity risk ratio and may generate higher investment returns.

For the majority of our clients, the Fund Managers will switch between sectors on your behalf.

Please continue to check our Blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.

Please see investment bulletin below from Brooks Macdonald received yesterday – 06/10/2021

What has happened

Yesterday saw some stabilisation within equity markets however the start to the European trading session today has seen a good portion of the gains dissipate. Inflation remains the key topic and expectations increased again yesterday, catalysing weakness in bond markets.

Gas and Inflation

European natural gas futures surged by another 20% yesterday and have seen a more than six-fold increase since the start of 2021. The European natural gas market continues to have some of the most impressive price increases however US gas futures and oil also continued to rise as inflationary pressures continue in the commodity and energy space. All of this has translated into rising 10-year inflation expectations which are now just shy of 4% in the UK (using RPI) and 2.5% in the US (using CPI). Bonds yields rose in response, with the US 10-Year Treasury yield at 1.55% today and 10-year gilt yield at 1.14%, both a far cry from their levels in August. Despite this, equities rose with the technology heavyweights leading the charge after a weaker start to the week however taking the last few weeks in aggregate it is clear that these inflation concerns are weighing on risk appetite more generally.

US Politics

The US Senate will vote today on the suspension of the US debt ceiling however it is widely expected to be blocked by the Republicans given the comments on recent weeks. Senator Manchin (a key Democrat moderate) is said to be warming to a social infrastructure bill worth around $2tn (from the original $3.5tn) so there are signs that a consensus is starting to form ahead of the reconciliation bill which may need to include the debt ceiling and the ‘Build Back Better’ economic plan. Meanwhile on the race for the next Federal Reserve Chair, Senator Warren is positioning against the reconfirmation of Chair Powell with criticism that the incumbent ‘failed as a leader’. Financial betting markets are now pricing in a far more open field for this important role.

What does Brooks Macdonald think

The latest surge in energy prices puts further pressure on the transitory inflation narrative with inflation expectations increasing over the medium to longer term. Yesterday the Reserve Bank of New Zealand rose rates by 25bps joining the small, but growing, group of central banks responding to the inflationary pressures. Yesterday’s US composite PMI data was the weakest we’ve seen this year suggesting that, at the same time as we see inflation rising, growth momentum is slowing, posing further challenges to policymakers.

Bloomberg as at 06/10/2021. TR denotes Net Total Return

Another quick update from Brooks Macdonald, these regular investment bulletins help us keep up to date with what is happening in the markets.

Please continue to check back for our latest blog posts and updates.

Please see below ‘Markets in a Minute’ article received from Brewin Dolphin yesterday evening, which provides analysis of the markets’ reaction to high inflation, despite the widely held opinion that it is transitory and will subside.

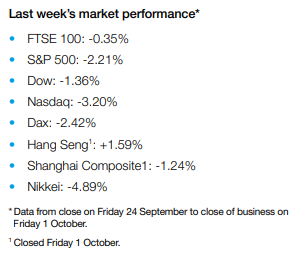

Most major stock markets fell sharply last week as fears about rising inflation and slowing economic growth weighed on investor sentiment.

The pan-European STOXX 600 tumbled 2.2% as eurozone consumer prices jumped to their highest level since September 2008. The FTSE 100 slipped 0.4% after the Bank of England’s governor said UK gross domestic product (GDP) would not recover to pre-pandemic levels until early next year.

In the US, the S&P 500 fell 2.2% amid uncertainty around the raising of the debt ceiling and difficulties surrounding the passing of the $1trn infrastructure bill. Reports of supply constraints also drove several companies’ share prices lower.

The gloomy mood spread into Asia, where Japan’s Nikkei 225 crashed 4.9% and China’s Shanghai Composite ended its holiday-shortened trading week down 1.2%.

Tech stocks drag Wall Street lower

Equities started this week in the red, with the S&P 500 and the Nasdaq down 1.3% and 2.1%, respectively, on Monday (4 October) driven by a rotation out of technology stocks and rising bond yields. Shares in Facebook tumbled 4.9% as its Instagram, WhatsApp and Facebook services suffered outages.

The selloff weighed on UK and European indices, which had already been dragged down earlier in the day by the announcement that trading in Evergrande shares had been suspended. The decision by OPEC+ to raise crude oil output by 400,000 barrels a day in November was also in focus.

On Tuesday, the FTSE 100 appeared to have shaken off Wall Street’s wobble, gaining 0.6% at the start of trading.

Eurozone inflation hits 13-year high

Figures released last week revealed the impact that soaring energy prices are having on inflation in the eurozone. In September, inflation accelerated to an annual pace of 3.4%, the highest level since 2008 and above the 3.3% forecast by economists. Energy costs were the biggest driver, soaring by 17% year-on-year. Core inflation, which strips out food and energy prices, also hit a 13-year high of 1.9%, according to the data from Eurostat.

Christine Lagarde, president of the European Central Bank, told the European Parliament earlier in the week that inflation could exceed the central bank’s forecasts, which have already been increased twice this year. “While inflation could prove weaker than foreseen if economic activity were to be affected by a renewed tightening of restrictions, there are some factors that could lead to stronger price pressures than are currently expected,” she said.

Nevertheless, Lagarde stuck to the official forecast that high inflation would prove transitory and that the rebound in energy prices and supply chain bottlenecks would ease in 2022.

It came after data showed German consumer prices rose by 4.1% in September from a year ago – the highest level in almost 30 years.

UK economic recovery delayed

The supply chain crisis means the UK’s economic recovery is likely to be delayed. Bank of England governor Andrew Bailey said GDP will not recover to pre-pandemic levels until early next year – up to two months later than was anticipated in August. He added that the Bank would keep a close watch on inflation expectations and the labour market.

Figures from the Office for National Statistics (ONS) showed GDP surged by 5.5% in the April to June quarter, better than its initial estimate of a 4.8% increase. The ONS said there were increases in all main components of expenditure, with the largest from household consumption following the easing of coronavirus restrictions.

However, monthly ONS figures showed the recovery largely stalled in July, growing by an estimated 0.1% from the previous month. There are concerns consumers will tighten their belts in the face of rising energy bills.

US consumer confidence falls

Over in the US, consumer confidence dropped in September for a third consecutive month, as the spread of the Delta variant and higher prices continued to dampen sentiment. The Conference Board’s index fell to 109.3 from a revised 115.2 in August, the lowest in seven months and far worse than the 115.0 expected by economists in a Bloomberg survey.

The present situation index, based on consumers’ assessment of current business and labour market conditions, fell to 143.4 from 148.9 and the expectations index, based on consumers’ short-term outlook for income, business and labour market conditions, fell to 86.6 from 92.8.

This came after the University of Michigan’s preliminary consumer sentiment index edged up in early September but remained close to a near-decade low. The report said high prices drove the declines in buying conditions for durable goods such as appliances and cars, adding “consumers have become much more concerned about rising inflation and slower wage growth and their negative impact on their living standards.”

Despite this, consumer spending rebounded by 0.8% in August following a 0.1% decline in July, according to the Commerce Department. The personal consumption expenditures (PCE) price gauge, which the Federal Reserve uses for its inflation target, rose by 0.4% from a month earlier and by 4.3% from a year earlier – the largest annual increase since 1991.

Please check in again with us soon for further news and relevant content.

Please find below, an update on market performance, received from Invesco yesterday.

A number of competing macroeconomic factors have been at play in recent months that have impacted financial markets. While vaccination rates continued to rise, the spread of the Delta variant has seen a large increase in new Covid cases, which saw further containment measures, notably in “zero-tolerance” countries, such as China. Despite that there was a general trend towards a further re-opening of economies and a return to normality. However, PMIs have been weakening as the pace of the recovery slows. Talk of a period of stagflation has increased, with inflation having risen sharply as base effects, supply chain issues and labour shortages have all impacted. While most Central Bankers and economists see the inflation risk as transitory, the underlying trend in monetary policy is for the removal of some of the extraordinary support that has been put in place over the past 18 months, led by tapering and ending of asset purchase programmes and rate hikes in due course. Concerns around US fiscal policy and the debt ceiling were increasingly in focus towards the end of the quarter. In China regulatory pressures and the fate of Evergrande, the second largest property developer, also weighed on investor market sentiment. Against this backdrop it was hardly surprising that financial markets have generally found it much tougher going as we approach autumn.

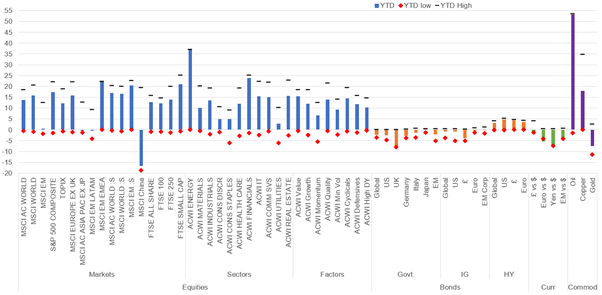

Not even a strong rally on Wall Street on Friday was enough to prevent global equities from having their worst week (MSCI ACWI -2.2%) since February. With China ending the week with small gains (MSCI China 0.4%) this limited EM losses (-1.1%) and ensured outperformance relative to DM (-2.3%). EM EMEA continued to benefit from rising Energy prices, rising 1.1% and leaving it up 22% YTD. Within DM weakness was across the board with Japan (-4.3%) and Europe ex UK (-2.6%) seeing the worst of the major market declines. Small Caps (-1.5%) outperformed slightly with DM and EM performing in-line. At a sector level performance was again dominated by Energy (4.6%) and it is now up 37.1% YTD, leaving it just over 13% ahead of the next best sector, Financials, which also had a good relative performance week (-0.1%). Underperformers were led by IT (-4.1%) and Health Care (-3.2%). Sector mix ensured that Value had a very strong week relative to Growth, falling just -0.9% compared to -3.4%. Rising yields have hurt long-duration assets. Quality (-3.4%) also had a tough week. UK equities had another strong relative week with the All Share down just -0.8% on the back of large cap outperformance (FTSE 100 -0.3%), as mid (FTSE 250 -2.7%) and small caps (FTSE Sm Caps -2%) struggled. Performance was boosted by a very strong Energy sector (6.9%), while Basic Materials (0.1%) also eked out a small gain. Industrials (-3.7%) and Utilities (-2.4%) were the main laggards.

Government bond yields were generally biased higher, albeit the moves in the UST and EZ bonds were marginal. The largest DM rise was in Gilts where the 10yr rose 8bp to close at 1%, its first time at that level since May 2019. It is now up 81bp since the start of the year. A further -1.5% for the Gilt index during the week left it down -7.6% YTD. Weak Gilts spread into £ IG with yields rising 10bp and the YTM above 2% for the first time since mid-2020. Yields rose less in US and Euro IG, with commensurate better relative performance. In HY, yields also rose 10-11bp across the board, but shorter duration meant that the sector outperformed IG, albeit still suffered small losses.

The US$ hit a one-year high during the week ending with the US Dollar Index seeing a gain of 0.8%, leaving it up 3.6% YTD. Both £ and the Euro lost 1%, with both close to their YTD lows. EM currencies also weakened with the JPM Emerging Market Currency Index down -0.5%, leaving it -4% YTD.

In commodities the Bloomberg Commodity Spot Index gained 2% and is now up 28.8% YTD. Energy (4.8%) and Softs (4%) led the gains again. While Oil prices saw a modest gain (1.5%) Natural Gas continued its sharp rise higher with an 8% gain. Industrial Metals struggled with Copper falling -2.2% and at 17.9% YTD is well below its 34.8% high. A contraction in the Chinese Manufacturing PMI for the first time in 19 months and a stronger US$ weighed. Gold eked out a small positive return (0.2%) its first in four weeks but is still down -7.5% YTD. Silver’s woes, however, have been far greater. It is down -14.6%.

Market performance last week (%)

Past performance is not a guide to future returns. Sources: Datastream as at 3 October 2021. See important information for details of the indices used.1

YTD market performance (%)

Past performance is not a guide to future returns. Sources: Datastream as at 3 October 2021. See important information for details of the indices used.1

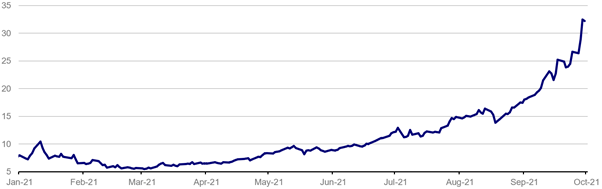

Chart of the week: ICE UK Natural Gas NBP Futures (US$/MMBtu)

Past performance is not a guide to future returns. Source: Datastream as at 2 October 2021.

There have been some spectacular moves in commodity prices this year and none more so than what has happened to natural gas prices, particularly in the UK and Europe. In the UK the ICE future for the current month has risen 490% YTD and 84% since the start of September.

This substantial jump matters for UK consumers and businesses given its importance as a source of power. EDF estimate that 78% of buildings are heated with gas. In the US by comparison it is just 50%. In terms of electricity generation, in 2020 35% came from gas, ahead of wind at 24% and nuclear at 14%. The impact on consumers is clear for all to see in Ofgem’s 12% and 13% hike to the energy price caps for default tariffs and pre-payment customers respectively, that took effect from last Friday. A further, potentially substantial, rise is likely when Ofgem reviews the cap again in February. Clearly this will have consequences for inflation with gas and electricity prices making up 3% of the CPI Basket. Deutsche Bank estimate that it could add 50-60bp to headline CPI. And household spending and industrial activity could also be impacted (fertiliser production being a recent example), so yet another headwind for an economy that is already showing signs of slowing.

Why have prices risen so much? A smorgasbord of factors have been at play. After a cold winter and spring, supplies have not been replenished as much as expected. The UK has the added problem compared to many other major European economies of having very little storage capacity, just 2% of its annual demand. Consequently, the country relies more on pipeline and LNG imports, with the UK importing more than half its gas (75% from Norway and Qatar). With competition for LNG supplies high due to elevated levels of demand in Asia, alongside restrictions to US LNG supply and the overall lack of LNG terminals and shipping, it is hardly a surprise that prices have surged. Pipeline flows from Norway, the biggest source of gas imports (55% of total in 2020), have also been under pressure due to higher levels of gas field maintenance this year and increased domestic demand due to water shortages for hydro. Nature hasn’t been helpful in the UK either with a lack of wind limiting the use of wind power.

How long will this surge in prices last? Some of the factors should be transitory; the wind will blow soon (!) and some shorter-term supply issues are likely to be resolved. However, key further out will be how long the surge in Asian demand continues and what sort of winter we experience. And while inventories remain depleted, prices could well remain elevated until well into next year. That’s certainly what futures are telling us in the UK with prices not dropping from current levels until the spring and then remaining well above pre-pandemic levels thereafter. This has obvious negative consequences for the growth/inflation outlook.

Key economic data in the week ahead

Employment data from the US will be the most scrutinised release of the week as the Fed has said the recovery in the labour market is key to its path towards tightening policy. Progress in Washington on the fiscal front and around the debt ceiling will be closely monitored. OPEC+ meets on Monday to review its output policy against the backdrop of an oil price that has recently risen above $80bbl for the first time since 2018.

In the US September’s ISM Service Index is released on Tuesday and although expected to remain strong at 59.9 this would be lower than August’s reading of 61.7. Before Non-Farm Payrolls, the ADP Employment Change published on Wednesday is estimated to show a 430k increase, higher than August’s 374k and the YTD average of 418k. Initial Jobless Claims unexpectedly rose for the third week in a row last week to 362k. Thursday’s reading is estimated to see a small decline to 350k. Friday’s September Non-Farm Payrolls are forecast to add 470k new jobs, an improvement on last month’s disappointing 235k. The unemployment rate is forecast to fall to 5.1% from 5.2% in August.

Although there will be no significant economic data released from the UK this week, the Chancellor of the Exchequer will speak at the Conservative Party conference on Monday and is expected to announce a package of grants to help households facing a cost-of-living crunch.

Retail sales in the EZ on Wednesday are forecast to have increased 0.9%mom in August following the 2.3%mom fall in July. This would leave it up 0.4%yoy, which would be the lowest rate of growth since March when the continent was emerging from stringent lockdown measures.

It is the Golden Week holiday in China. The Caixin Services Index for September is expected on Friday to show the sector still in contraction but improving to 49.2 from 46.7 in August.

Nothing of note from Japan this week.

Please continue to check our Blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.

Please see the below article from JP Morgan received this morning:

Companies that can get ahead of impending climate-change initiatives and work with governments to achieve their goals may benefit from first-mover advantage.

This November sees the UK play host to COP26 – the 26th Conference of Parties – where global leaders from almost 200 nations will come together and discuss climate objectives and, more importantly, revisit the commitments made as part of the 2015 Paris Agreement. The parties are likely to agree that efforts will need to be meaningfully increased to ensure that achieving net zero by 2050 is within reach. In the coming years, investors can expect a raft of policy changes, with governments increasingly targeting public spending on infrastructure. Corporates are likely to face higher costs as a result of broader adoption of carbon pricing systems, but may find that capital markets reward them for focusing future investment spending on climate-related projects. Companies that can get ahead of the impending change and work with governments to achieve their goals may benefit from first-mover advantage. We discuss the technology and policy developments required to reach net zero in more detail in our paper, “Achieving net zero: The path to a carbon neutral world.”

More ambition required on the path to net zero

The main aims of the Paris Agreement were to keep global temperatures from warming above 1.5 degrees Celsius and effectively reach net zero greenhouse gas emissions by 2050. Countries were asked to submit their own emission reduction targets in the form of NDCs (Nationally Determined Contributions) and review them every five years. Importantly, COP26 is the first meeting of global leaders since the end of the first five year period. We now know that the proposals set out in 2015 are not sufficient to meet the target of restricting global warming to 1.5 degrees.

Just over 110 parties – accounting for around half of global emissions – have submitted new NDCs, but the United Nations (UN) has judged that these proposals still fall well short of the degree of change required to meet the 1.5 degree target. The UN estimates that current national plans will lead global emissions in 2030 to be around 16% above 2010 levels. In order to be consistent with the 1.5 degree target, 2030 emissions need to be below 2010 levels by 45%. With progress wide of the mark, the current proposals and potential improvements are expected to form a significant part of discussions at COP26.

The US, UK and European Union are all among those to have submitted new plans to reach net zero by 2050. The US has pledged to cut net carbon emissions in half by 2030 (relative to emissions in 2005), while the EU plans to reduce its emissions by 55% by 2030, relative to 1990. The UK has one of the most ambitious plans, aiming to cut emissions by 68% by 2030 (relative to emissions in 1990), but is responsible for less than 1% of total global greenhouse gas emissions. In fact, these three developed nations make up just 25% of global carbon emissions, which only makes clearer the need for global coordination.

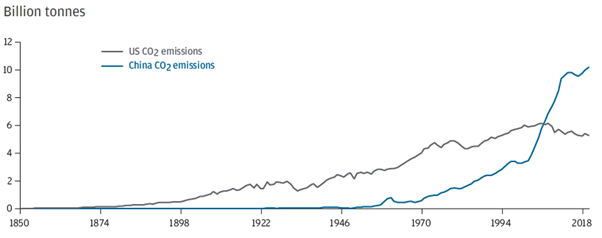

Herein lies the challenge at this conference. A significant number of countries have still not submitted an update of their emission reduction targets. COP26 can only be deemed a success if all countries – including those with the highest emissions – decide to increase ambitions when they update their targets for the next decade. China has not updated its NDC but has stated its intention to reach peak carbon emissions by 2030 and net zero by 2060 – a pledge that does not go far enough for a country that is responsible for the largest amount of global carbon emissions. Undoubtedly, China will argue that the onus should be placed on developed countries, which initiated the industrial revolution, have a longer history of emissions and have the financial means to cut down on them (Exhibit 1). With China’s attendance at COP26 still in doubt, the potential for climate disputes to catalyse geopolitical tensions is increasingly clear.

Exhibit 1: US and China CO2 emissions over time

The metrics used to measure emissions make a huge difference: on a per capita basis, the US has a greater level of emissions than China (Exhibit 2). It is also worth noting that around 14% of China’s carbon emissions are attributable to goods that are exported and consumed abroad, which underlines the major role that recipients of China’s exports have to play in helping China to reduce its emissions. Another key expectation from COP26 will be for developed countries to make good on their promise to deliver at least USD 100 billion in finance per year to support developing countries in their climate goals. OECD data suggests that around USD 80 billion was mobilised in 2018. Commitments to increase this support will perhaps encourage some of the important developing nations to step up their carbon-reduction initiatives.

Exhibit 2: Global CO2 emissions per capita

Considerations for investors

Investors should be prepared for climate-related headlines in the coming weeks, as COP26 acts as a catalyst for governments and corporates to make new, more ambitious commitments. We expect this to impact financial markets in multiple ways.

Green bond issuance set to grow

Green infrastructure spending will be a major focus for governments that are under pressure to demonstrate their climate credentials to an increasingly green electorate. There are already several examples. The Biden administration’s USD 2.3 trillion American Jobs Plan includes multiple spending measures aimed at clean energy technology and the transition to electric vehicles. It is a similar story across the Atlantic, with the UK government’s Ten Point Plan for a Green Industrial Revolution aiming to generate 250,000 green jobs. In Europe, at least 30% of spending in the EU’s EUR 750 billion recovery fund must have climate-related benefits. Yet with more than USD 13 trillion of global investment in electricity systems alone estimated to be required by 2050 if net zero targets are to be reached, the scale of the challenge is clear.

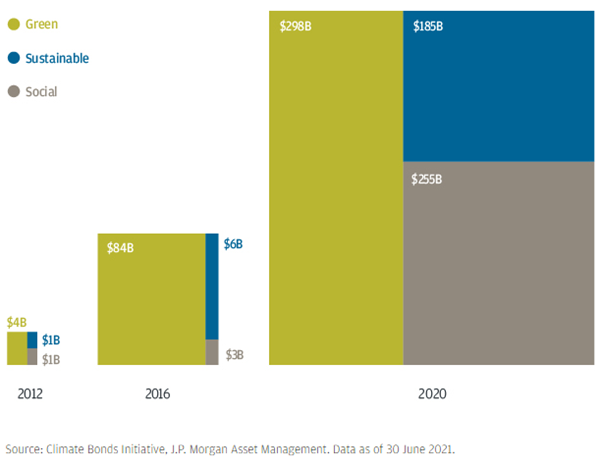

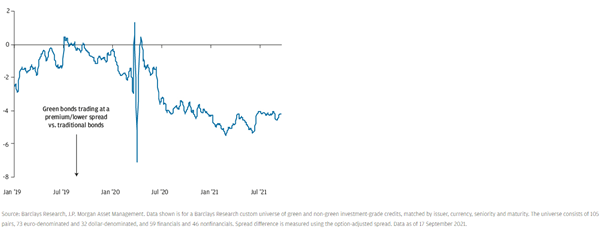

A rise in green bond issuance will be the key means by which governments will fund new climate-focused spending. The European Investment Bank became the first issuer of green bonds – for which proceeds are earmarked for environmentally friendly outcomes – back in 2007, and both governments and corporates have flocked to the sustainable bond market since, with green, social and sustainable bond issuance growing from just USD 6 billion in 2012 to over USD 700 billion last year. The popularity of the market is unsurprising given that strong demand for this debt often leads to lower borrowing costs for the issuer – a dynamic known as the green premium, or “greenium” (Exhibit 3). Despite this benefit, the US government remains a notable absentee from the green bond market. While officials have so far been reluctant to discuss this idea publicly, the emergence of a “Green Treasury” appears increasingly inevitable.

Exhibit 3a: Global sustainable, social and green bond issuance

Exhibit 3b: Spread between green and traditional corporate bonds

Private capital encouraged to be part of the solution

An acceleration in government spending is one piece of the puzzle, but we also expect to see further measures aimed at incentivising private capital to be part of the solution. Strengthened regulation that pressures large investors to tilt portfolios towards climate-friendly strategies is one way to achieve this outcome. Another route is for governments to co-invest alongside the private sector in public-private partnership models. This type of structure can often be used to ensure that initiatives that would be too risky for the private sector to invest in alone can still access the financing they require.

Corporate announcements to demonstrate the leaders and laggards

In the face of increasing investor scrutiny, the corporate sector is unlikely to wait for regulation to force its hand on tackling climate change. The number of companies signing up to science-based target commitments had already surpassed last year’s record by June of this year, and November’s summit will intensify pressure on corporations that are not yet on board. Those that are able to align with government goals will benefit from government spending and be rewarded with access to easier finance through capital markets. Central banks are likely to incorporate green bonds or tilt their corporate asset purchases towards companies that are making investments consistent with net zero, meaning these companies will likely benefit from relatively lower borrowing costs. Additionally, investors may find comfort in owning the bonds of these firms, particularly in more stressful market environments, in the knowledge that the central bank is likely to be a willing buyer.

In industries such as energy, logistics, airlines and farming that are typically carbon intensive, there are also reasons to be optimistic. Those that adopt policies that help reach net zero will likely gain market share and be viewed as part of the solution, rather than the problem. Whatever the industry under consideration, investors may find opportunities by identifying companies that are better prepared for the transition.

Carbon pricing likely to impact corporate profits

Reaching agreement on a global carbon pricing system will be one of the most challenging issues of the summit. We cover how such a system could work in our paper, “The implications of carbon pricing initiatives for investors.” While some regions, such as Europe, have already made substantial progress, firms will remain incentivised to outsource production to other regions with lower carbon costs until a global solution is reached. Without a global solution, regions that decide to go it alone also risk imposing a competitive disadvantage on the profit margins of their domestic corporations. The risk of disagreements on carbon pricing spilling over into broader international relations is clear, with Europe perhaps needing to introduce a carbon border tax if other countries decide not to adopt a carbon pricing system. Without substantial progress, the path to net zero looks worryingly steep.

Conclusion

Investors should be braced for a wave of new climate ambitions stemming from November’s COP26 summit. With the conference serving to shine a spotlight on the enormous challenge presented by the need to reach net zero by 2050, both the public and private sectors will be keen to stress the extent of their ambitions, with potentially market-moving implications. For investors, there are risks and opportunities across sectors. Companies that prove they can be a part of the solution will likely benefit from a lower cost of financing in the years to come, as both governments and the private sector look to tilt their spending towards green initiatives. For businesses that are poorly prepared for the climate transition – regardless of sector – life will only get tougher.

Keep checking back for more of our regular blog content including market insights and views from some of the world’s top investment managers.

Please see investment bulletin below from Brooks Macdonald received yesterday – 30/09/2021

What has happened

Equities bounced back slightly yesterday as global government bond yields found a new level. Both US and European equities saw muted gains, led by some of the more defensive subsectors such as food & beverages and utilities.

US Shutdown

Majority Leader Schumer said overnight that Senators had reached an agreement to introduce, and pass, a stopgap funding measure that would fund the government until the start of December. This bill will be voted on by the Senate today before moving over to the House of Representatives in short order as Congress looks to avert a shutdown at the end of today. The thornier issue remains the debt ceiling and bipartisan agreement there looks unlikely. In a sign of possible movement, House Speaker Pelosi said that the House would vote on the bipartisan physical infrastructure bill today which suggests sufficient cross-party support to pass the bill. This is despite progressive Democrats saying they would hold up the physical infrastructure bill until they could vote on this package alongside the wider social infrastructure bill. Progressive Democrats fear they would lose a key bargaining chip in this situation so should the $550bn package pass, we could see a fairly imminent watering down of the $3.5tn social package.

Focus on the UK

Despite growing expectations that the UK might raise rates at the end of this year or the start of 2022, sterling has been suffering. Yesterday saw sterling back to levels (versus the US dollar) that were last seen in December last year at the height of the Brexit deadline worries, as investors fear further disruptions over energy and fuel supplies. Markets are still trying to weigh up whether inflation expectations should be higher, due to higher energy prices in the short to medium term, or lower as investors price in lower consumer demand from higher prices for essentials and rising interest rates. This uncertainty is creating a fresh reason for international investors to avoid sterling for the short term.

What does Brooks Macdonald think

Arguably, at the start of September the market was overly complacent in the face of the risk of sustained inflation. September’s moves show a pricing in of two risks, one that inflation could be stickier and two that central banks may be more fearful of inflation expectations than tighter policy which could hamper growth. Whilst the signs still point to the current inflationary pressures being transitory, the markets at the end of September more accurately reflect the risks of the investor consensus being wrong.

Please continue to check back for our latest blog posts and updates.

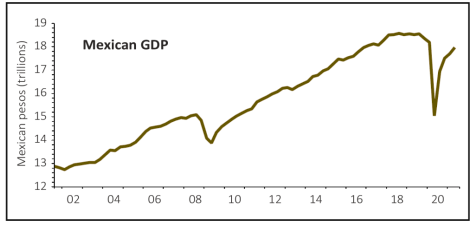

Please see below for one of AJ Bell’s latest articles received by us today 30/09/2021:

The second largest Latin American economy enjoys a big trade surplus with the US.

Mexico is the second largest economy in Latin America and its proximity to the economic juggernaut that is the US has helped support strong growth, with some intervening ups and downs, over the course of the last two decades.

In its interim report on the economic outlook in September 2021 the OECD lifted its growth forecast for Mexico for 2021 from 5% to 6.3% and for 2022 from 3.2% to 3.4%. The government led by Mexican president Andres Manuel Lopez Obrador has also recently announced plans to address tax issues and ease austerity measures in its latest budget to support the economy.

Like many countries Mexico is having to tackle the issue of inflation, with its central bank among several in emerging markets to increase interest rates in recent months to address the problem of rising prices.

In June consultants at Deloitte noted the role exports were playing in Mexico’s economic rebound: ‘The bold recovery of the American economy is bolstering Mexican exports to its northern neighbour. The trade balance saw a surplus of $26.6 billion, or 2.4% of GDP, in 2020, the highest level recorded since data became available in 1993.

‘In March 2021, exports grew 31% year over year to reach $43 billion, the largest expansion in almost a decade. This growth was driven by machinery and metal manufacturing, which expanded 6.6%; electronics and professional equipment also registered expansions of 21.3% and 14.5%, respectively.’

Please continue to utilise these blogs and expert insights to keep your own holistic view of the market up to date.

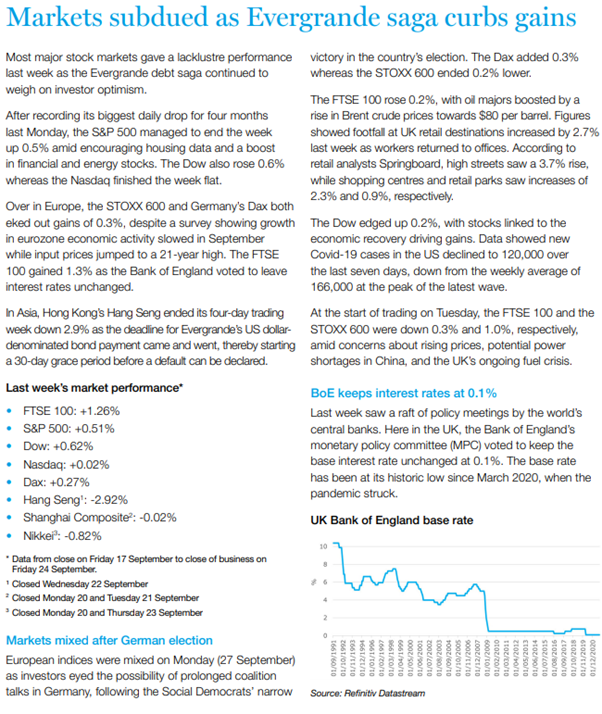

Please see below Brewin Dolphin’s latest market summary, which was received yesterday (28/09/2021) afternoon:

As you can see from the above, markets remained subdued last week as China’s Evergrande property business situation continued. The FTSE 100 had a better week than others as the Bank of England kept interest rates at 0.10%.

The US has signalled that rate hikes over there could come sooner than expected. This is something to monitor.

As stated last week, the negative sentiment towards China at the moment is likely to present buying opportunities in Chinese Equities.

Please continue to check our Blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.

Please see below article received from Legal & General yesterday afternoon, which provides a global market update and eases concern with regards to supply chain issues and inflation.

Don’t worry (much) about supply chains

Industrial companies are talking a lot about issues with their supply chains. But they haven’t taken the opportunity to change their guidance or deliver profit warnings. And market reaction to their comments was relatively muted.

We had a few companies with early quarter-ends give a flavour of what to expect from the rest of the reporting season. Of those early reporters, 74% beat analyst estimates and 80% outperformed the market the day after their results were released. Their figures cover a slightly different period than Q3, and while the sample is small, it looks somewhere between normal and better than average.

It also suggests that the disappointments from companies like FedEx*, Adobe* and Nike* may get the most attention but are not the norm.

There is clearly an impact on earnings from the supply chain bottlenecks, but so far it seems that the impact:

1.

is manageable for most companies

2.

can be covered with their earnings buffer by most companies

3.

is well anticipated and priced by the market

Bottom line: Indications so far are that we are heading for a fairly normal earnings season, which has little impact on markets at the aggregate level.

Germany’s election

Germans went to the polls on Sunday and granted the Social Democrats (SPD) a narrow victory, with almost 26% of the vote. Their leader, Olaf Scholz, said he had won a mandate to form the nation’s next government. Support for outgoing chancellor Angela Merkel’s CDU/CSU appears to have plunged to a historic low of 24%. The Greens secured almost 15% of the vote.

This will only mark the start of what will likely become lengthy coalition negotiations. Last time, this took a record six months, and this year’s prospect of a 3-party coalition across the political spectrum feels like a recipe for long rather than short negotiations.

There would have been really only one properly market-moving scenario: a left-wing, red-red-green government – but the Left party appears to have fallen just under the 5% hurdle.

The SPD and Greens had previously made it clear that they were leaning towards a more centrist, “traffic light” coalition with the Liberals (FDP), who won almost 12% of the vote.

Emerging market equities – what are we waiting for?

It’s easy to be bearish on emerging market equities amid double trouble from regulatory and growth risks. Increasing regulation in China across many industries is hitting the outlook for profits, and the uncertainty over the extent and duration of the crackdown means investors require an additional discount on top of their future earnings base case. At the same time, economic growth has slowed in tandem with the delta outbreak, and we expect an underwhelming rebound in Q4 as temporary regional lockdowns are likely to be required for some time. Then there’s the spillover from Evergrande’s* problems to the important property sector. Those are all drivers behind our below-consensus growth forecasts.

But equity markets have reacted…a lot.

The correction in Chinese equities (H-shares, not A-shares) is now one of the biggest in recent history. The HSCEI index is around 30% off its February peak, making it the third largest drawdown over the past decade. Emerging market equities have also been affected, having trailed developed markets by 20%, the third largest underperformance over the past 15 years.

Sentiment has turned very bearish. In an extreme reversal, emerging market equities have gone from everyone’s favourite long at the start of the year, in sell-side outlooks and investor surveys, to being the least popular in the latest fund manager survey since their low in 2016.

Valuations paint a similar picture. Relative to developed markets, emerging market equities are as cheap across many multiples as they have been in well over 10 years. Some of that clearly reflects falling earnings expectations, but earnings estimates have some way further to fall before catching up with what prices have already reflected.

Some of this sounds like a bull case in the making, but regulatory uncertainty and our below-consensus growth outlook are some of the factors holding us back — for now, at least. Nevertheless, we are watching a number of potential catalysts and signposts that could change our position:

•

President Xi or the Chinese government make a commitment to the private sector — and tech companies in particular.

•

Decreased sensitivity to regulatory news flow. We have seen some evidence of this in tech, but the price reaction to new sectors being targeted – e.g. casinos — remains severe.

•

A-shares selling off. The pain has so far been concentrated in H-shares. A-shares joining in the correction would be a sign of markets pricing the growth slowdown as much as the regulation theme, and a sign of domestic capitulation.

•

A larger-than-expected policy response to a slowdown. We expect policymakers to be slower than in the past in responding to stumbling growth, but evidence to the contrary would be a very positive catalyst.

•

Indications that our growth forecasts are too pessimistic and growth rebounds faster than we expect.

•

Vaccination convergence. Emerging market vaccinations are catching up with developed markets.

Bottom line: Emerging markets and China equities are becoming more interesting in some ways, but given our macro views, we believe it’s too early to buy.

We will continue to publish relevant content and news throughout the coming Autumn weeks, so please check in with us again soon.