Please see below Brewin Dolphin’s latest market summary, which was received late yesterday (20/10/2021) afternoon:

Global equities rose last week on the back of better-than[1]expected US retail sales and encouraging employment figures.

The S&P 500 and the Dow gained 1.8% and 1.6%, respectively, following a 0.7% jump in US retail sales in September and a decline in weekly jobless claims.

In Europe, the STOXX 600 surged 2.7% amid an encouraging start to the US earnings season. The FTSE 100 added 2.0% with airlines among the strongest performers after the US announced it would ease travel restrictions from 8 November.

Japan’s Nikkei 225 clawed back losses from the previous week to finish up 3.6%, as investors took comfort from new prime minister Fumio Kishida’s comments that he would not increase capital gains tax for the time being.

Last week’s market performance*

• FTSE 100: +1.95%

• S&P 500: +1.82%

• Dow: +1.58%

• Nasdaq: +2.18%

• Dax: +2.51%

• Hang Seng: +1.99%

• Shanghai Composite: -0.55%

• Nikkei: +3.64%

* Data from close on Friday 8 October to close of business on Friday 15 October.

Wall Street mixed as China GDP disappoints

Wall Street stocks gave a mixed performance on Monday (18 October) following disappointing gross domestic product (GDP) figures from China. The Dow slipped 0.1% whereas the S&P 500 and the Nasdaq gained 0.3% and 0.8%, respectively, as bond yields rose and data showed China GDP grew by 4.9% in the third quarter from a year ago, below the 5.3% growth expected by economists.

The sombre mood continued in London, where the FTSE 100 fell 0.4%. Figures from Rightmove showed average UK house prices jumped by 1.8% in October from the previous month – the biggest rise at this time of the year since 2015. On an annual basis, the average asking price is up 6.5% to £344,445. Meanwhile, the two-year gilt yield soared to its highest level since May 2019 – a sign that traders expect UK interest rates to rise soon.

The FTSE 100 was flat at the start of trading on Tuesday as investors awaited more earnings reports from the US.

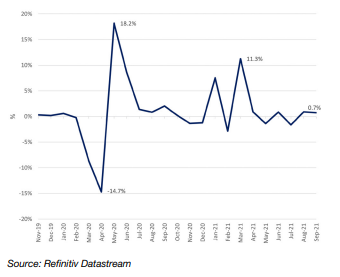

US retail sales surge as prices rise

Figures released by the Census Bureau last week showed US retail sales jumped by 0.7% in September, far better than the 0.2% decline expected by economists. Compared with a year ago, sales were up by 13.9%.

US retail sales – MoM change

The increase came as the government ended the enhanced benefits it had been providing during the pandemic. It was thought this would depress sales, but instead spending accelerated as workers and students returned to offices and schools.

Much of the increase was driven by higher prices, as US retail sales figures are calculated according to receipts as opposed to volume. Indeed, separate data showed inflation, as measured by the consumer price index (CPI), rose by 5.4% in September from a year ago, slightly higher than the 5.3% increase expected by analysts. On a monthly basis, prices increased by 0.4%, following a 0.3% rise in August. Core CPI, which excludes food and energy, rose by 4.0% from a year ago – well above the Federal Reserve’s 2.0% target.

Meanwhile, the University of Michigan’s consumer sentiment index slipped in early October to 71.4 from a final reading of 72.8 in September, suggesting consumers remain anxious despite spending more.

UK GDP rises by 0.4%

Here in the UK, figures showed GDP grew by 0.4% in August from the previous month, as the hospitality industry benefitted from the first full month of coronavirus restrictions being lifted in England. Accommodation and food service activities were the main contributor to growth in the services sector, rising by 10.3%. This was followed by arts, entertainment and recreation, up 8.5%. Despite the increase, the Office for National Statistics (ONS) said GDP remains 0.8% below its pre-pandemic level, while consumer-facing services are 4.7% below their pre-pandemic level.

Investors were also cheered by data that showed UK employers added 207,000 staff to their payrolls last month, shortly before the end of the furlough scheme. This meant the number of payrolled employees surged to 29.2 million – the highest level since records began in 2001. However, the unemployment rate for June to August was an estimated 4.5%, higher than the 4.0% rate seen before the pandemic.

Germany’s GDP forecast slashed

Over in Europe, Germany’s GDP forecast for 2021 was slashed last week by a group of economic research institutes. The group’s biannual report said the German economy would grow by 2.4% this year, down from its previous forecast of 3.7% growth. The researchers said the reduction was driven by the ongoing impact of Covid-19 on the service sector, and continuing supply chain issues. GDP is expected to grow by 4.8% in 2022, assuming the pandemic and supply chain disruptions are resolved.

Supply chain issues are affecting the eurozone more broadly, with industrial production falling in August by 1.6% from the previous month. Eurostat said one of the steepest declines was in Germany, where output dropped by 4.1%

Please continue to check our Blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.

David Purcell

21st October 2021