Please see this week’s Markets in a Minute update below from Brewin Dolphin, received yesterday afternoon – 28/04/2026

How could energy impact investment markets?

A tighter energy market could affect household and corporate earnings – what impact might this have on investment markets?

Key highlights

- What’s next in the U.S.-Iran war? Markets’ anticipation for a reopening of the Strait of Hormuz fell to 34% last week. The implications of a further five weeks of disruption are stark, causing additional tightening in the energy markets.

- Firms predict price rises: The Bank of England (BoE)’s Decision Maker Panel expects companies to raise prices by 4.4% over the next year and for inflation to reach 4% – double the BoE’s target.

- U.S. corporate earnings results: With about a quarter of companies having reported, aggregate earnings are coming in around 10% above expectations, producing a blended year-over-year growth rate of 14.4%.

The Iran war: Brinkmanship, blockades and fragile progress

The geopolitical stand-off between the U.S. and Iran over the Strait of Hormuz dominated market sentiment throughout the week. Oil prices returned to above $100 per barrel and risk appetite came under pressure.

Last week opened with both sides claiming the Strait was open to traffic, only for Iran to close it again after the U.S. failed to lift its naval blockade. A vessel was seized by the Americans for attempting to violate the restrictions, marking the first such incident.

Talks were scheduled in Islamabad, Pakistan last Tuesday, but Iran initially signalled it had no plans to send negotiators. By midweek, the U.S. had chosen to maintain the blockade while extending the ceasefire without an end date – a pragmatic acknowledgement that setting another deadline it might not enforce would damage credibility.

By Thursday, Iran had formally stated it had no plans to participate in negotiations, pushing Brent crude higher once more.

This led to a fall in anticipation of the reopening of the Strait of Hormuz. At the beginning of the week, there was a 60% chance of the Strait being reopened by the end of May, according to the Polymarket prediction market. By the end of the week, that had fallen to 34%. The implications of a further five weeks of disruption are stark, causing additional tightening in the energy markets.

Notably, while crude oil prices have retraced somewhat from their peaks, the pass-through to consumer fuel prices has been asymmetric – petrol prices at the pump remain stubbornly high despite some easing in wholesale markets. Towards the back end of the week, prices were rising once more.

This is frustrating because there’s growing evidence that the UK economy was picking up before the war began. UK retail sales numbers released for March show that UK consumers have been able to dip into accumulated savings, so the war hasn’t slowed their consumption. But it won’t take long for the effects to be more pronounced as the GfK consumer confidence survey showed consumers are anxious about the economy, and business optimism fell to its lowest level since COVID-19 according to the Confederation of British Industry.

The UK isn’t alone in this. Global purchasing managers indices (PMIs) showed that businesses are slowing production and raising prices. Most countries are experiencing price increases not seen since the brief window of extraordinary inflation in 2022.

Inflation is bad for political leaders. The decline in President Donald Trump’s net approval rating has started to accelerate.

In the UK, it’s yet another challenge for UK Prime Minister Sir Keir Starmer – in addition to the difficult testimony he gave to Parliament regarding the Peter Mandelson vetting affair, and the even more difficult evidence heard from former civil servant Oly Robbins, who oversaw the process.

The combination of these factors has made gilts the worst-performing major bond market since the onset of the war.

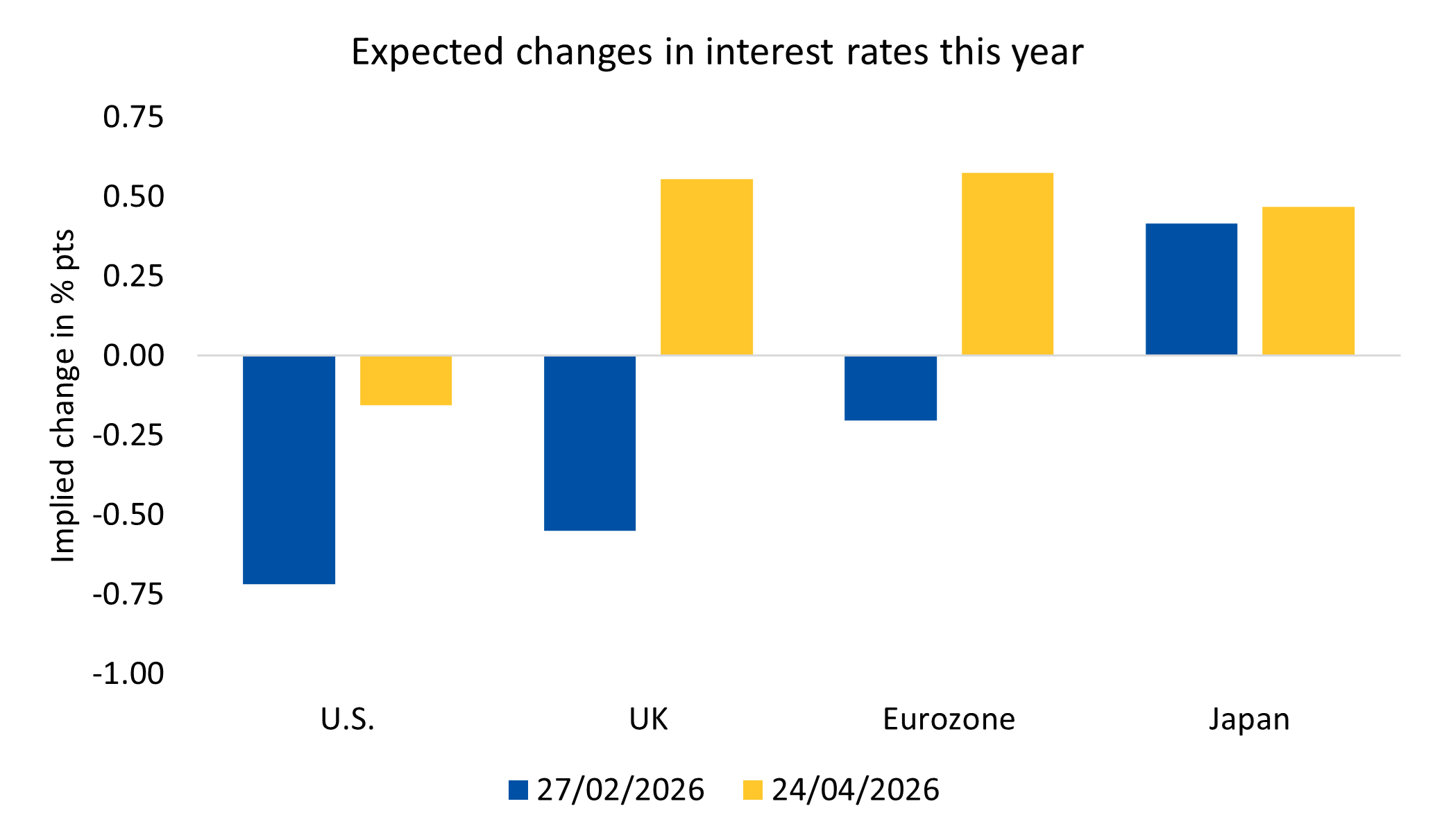

UK inflation data released last week offered few surprises. Inflation has picked up due to energy. The combination of the survey data and PMIs caused expected interest rates to rise from a single increase in 2026 to two hikes for both the UK and Europe.

Source: Bloomberg

We’re often asked why central banks would increase interest rates when the economy is struggling due to high prices elsewhere. The answer is that if it seems like higher oil-related prices feed through into higher wages, the central bank faces a wage price spiral, which can only be broken by deliberately weakening demand – done by raising interest rates.

In April, the Bank of England’s Decision Makers Panel of firms said it expects firms to raise prices by 4.4% over the next year, and for inflation to reach 4% – double the BoE’s target. However, the BoE’s agents – who speak to businesses and gauge how they’re feeling about things – learned firms are worried about their ability to pass on price increases, which means they’re more likely to ‘absorb’ them (suffer weaker profits). If companies don’t pass on the price increases, the BoE won’t need to raise interest rates.

Corporate earnings: Strong but facing elevated expectations

Earnings season continues with quite strong numbers overall emerging from businesses.

At a time when valuation multiples have contracted (the S&P 500 12-month forward price-to-earnings ratio has declined from 22.9 to 20.1), corporate earnings have been the engine driving equity markets higher.

With about a quarter of U.S. companies having reported, aggregate earnings are coming in around 10% above expectations, producing a blended year-over-year growth rate of 14.4%. Technology has been the standout, with earnings up 46% year-over-year. Corporate balance sheets remain in good shape, with interest coverage for U.S. non-financial businesses at very high levels, leaving ample capacity for continued investment.

Companies tend to beat their short-term earnings estimates by design – they edge down their guidance to reach something achievable. But longer-term expectations are high and must be met in order to justify the current valuations. Several cyclical, sector-specific, and structural factors suggest meeting currently elevated expectations will be challenging.

The boost to the economy from lower bond yields appears to be over. Fiscal policy for advanced economies in 2026 is projected to be neither loose nor tight. U.S. jobs growth has slowed to zero – and historically, every time non-farm payroll growth has dropped to zero or below, corporate earnings have followed. Earnings recessions have occurred roughly once every four years; the last was in 2023, implying one could be due by 2027.

The main anxieties facing company earnings at the moment are around AI-related capital expenditure by hyperscalers, which has boomed. The four major hyperscalers – Microsoft, Meta (Facebook), Amazon and Alphabet (Google) – are expected to spend over $600 billion this year, up from $200 billion just two years ago. However, there are legitimate questions about what returns they are likely to make on this investment.

The relevant CEOs themselves have acknowledged they’re investing not solely for attractive returns but for survival – a dynamic reminiscent of a prisoner’s dilemma, where mutual investment compresses margins.

So, while this seems very different from the previous tech bubble because these companies are incredibly profitable at the moment, there are some genuine reasons to fear that future profitability could disappoint.

Please continue to check our blog content for advice, planning issues and the latest investment market and economic updates from leading investment houses.

Charlotte Clarke

29/04/2026