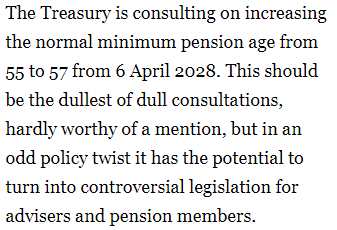

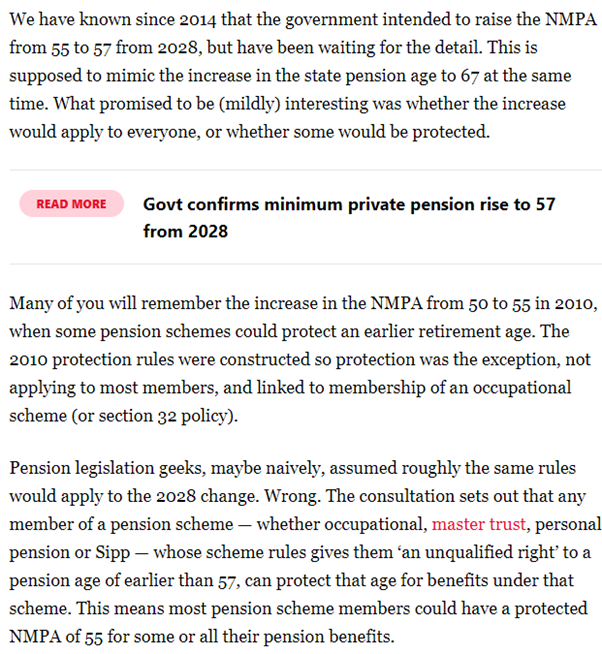

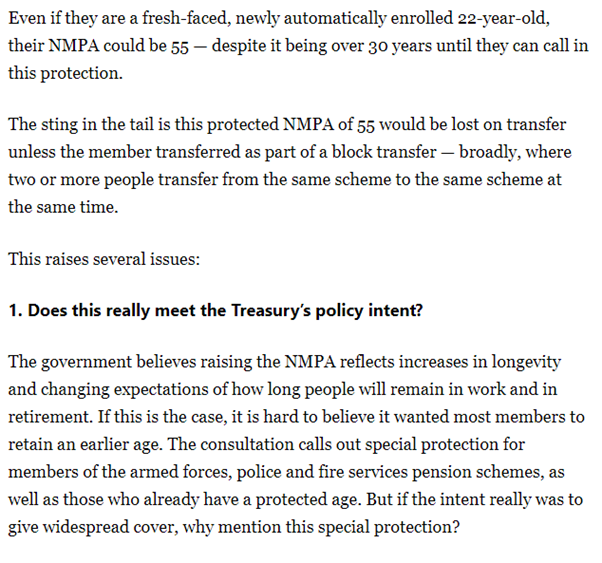

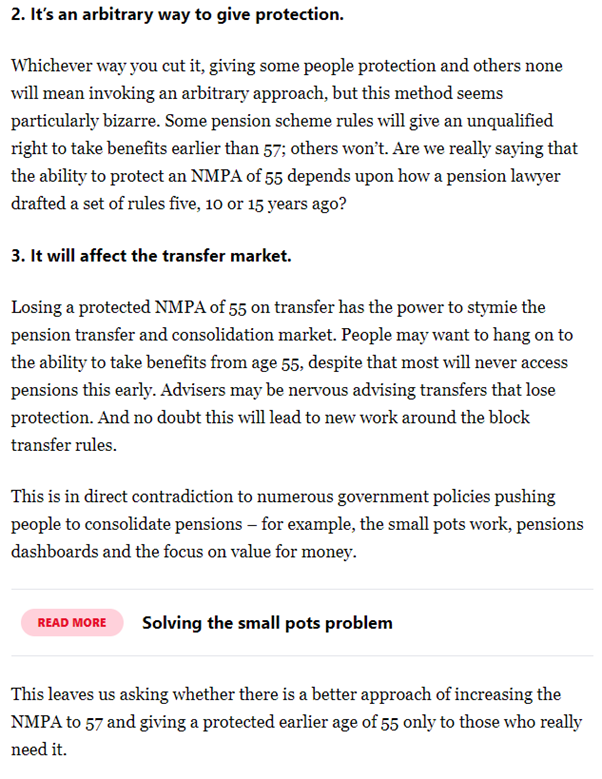

Please see below an article published by Money Marketing today, which was written by Rachel Vahey, a Senior Technical Consultant from AJ Bell. This article highlights some of the key considerations of the proposed changes to the Normal Minimum Pension Age moving from age 55 to age 57:

I think the above article helps highlight some of the key factors that will need to be factored in when considering possible pension consolidation exercises or general pension switches. It could be that to switch your pension to a new provider in the future could mean you losing a minimum pension age of 55 under the existing contract and instead not being able to access your pension benefits until age 57.

There are a few questions clients will have to consider with their I.F.A., which are:

- When do I realistically anticipate drawing pension benefits?

- How do I want to draw benefits from my pension? and

- Does this change (in minimum pension age) really impact on my plans?.

The reality is that you need a lot of capital to retire early and for the majority of people it’s not an option.

Another key issue that needs to be considered is that some old-style legacy pensions cannot facilitate Flexible Access to pension funds and instead force you to either purchase an Annuity or encash the pension.

All of the above really need to be weighed up very carefully before making any decision and taking financial advice will help you consider your own situation.

It remains to be seen how the government will implement the proposed changes and what the potential fallout could be, but we will keep you fully updated with any changes that are announced.

Please continue to check our Blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.

Please keep safe and healthy.

Carl Mitchell – Dip PFS

IFA and Paraplanner

19/04/2021