Please find below, an update on markets received from Tatton, this morning – 17/10/2022

Outlook: Bond markets 1 – UK Government 0

It is seldom that the UK alters the course of global capital markets, particularly given our domestic stock market comprises just 3.1% of global equities and 4.1% of the global government bond market. However, over the course of October, far bigger bond markets – like that of the US and Italy – have experienced significant changes in the wake of events earlier in the day in the UK.

In our view it can all be traced back to a profound misunderstanding of the UK’s relative position in the global competition for capital at just the point when central bank’s decisive anti-inflation measures have re-introduced fragility into capital markets not seen since the 2010-2012 Eurozone crisis. To this end, the US economy has been attracting huge swathes of capital and the US dollar has motored ahead, with interest rates and bond yields rising in parallel to expanding economic activity. In particular, the sharp rise in yields on US inflation-linked bonds has been at the heart of the stresses in the global economy. With the rest of the world facing massive competition for capital, it was unwise for the UK government to make a grab for more at a point when the costs have been made almost unbearable. To blame circumstances now suggests Liz Truss et al. were unaware of the situation when devising the policies. It’s no wonder the Chancellor is now a different person. Indeed, global markets have been cheered by signs the UK is unwinding its recent pronouncements. Should it reverse the bulk of policies that capital markets balked at as fiscally irresponsible, then rates and yields may still revert to the trajectory they were on before September’s fateful fiscal event. Whether they can do so fully will largely depend on how much of the reputational trust in UK institutions lost by international investors can be regained.

From the global perspective, beyond the UK’s domestic woes, the October 2022 UK bond market crisis will be remembered as the moment when central banks around the world were forced to grapple with something they have been denying for many months. Namely that their formidable efforts in forcing the inflation genie back into the bottle have unveiled fragilities in the global financial markets that may now hamper their ability to follow through with their inflation fighting strategy. The dependencies on ultra-low interest rates they had allowed to build up since the Global Financial Crisis mean that the risk that something, somewhere, in the global financial ecosystem would break – or at least seriously buckle – has now become all too apparent.

Will UK property downturn change the investment landscape?

In the wake of Kwasi Kwarteng’s ill-received fiscal event, lenders pulled swathes of mortgage products in expectation of sharply higher interest rates from the Bank of England (BoE). The potential effects on consumers and households were well-publicised – but as well as households, damage has also been done to equity markets – particularly to property funds and house builders. Both have fared substantially worse than the broader market throughout the year, and the latest drama precipitated another swipe down. The building sector has nearly halved in value since January, while real estate investment trusts (REITs) have lost around 40%.

Clearly, these problems precede the fiscal fallout – though it undoubtedly made the situation considerably worse. Both sectors fared well throughout the pandemic, buoyed by an increase in consumer savings and property deals. But the sharp contraction of monetary policy since the beginning of the year has made conditions extremely difficult.

With the UK probably already in recession, commercial property is one of the most vulnerable sectors. This would be the case even without the supply-side inflation pressures and fiscal imprudence, since house building and purchasing are extremely cyclical. We are also seeing this stress spread to banks with large property-related loans on their balance sheets – many of which have seen their share prices come under pressure. It seems that, having (somewhat) stabilised the pension fund problem in recent weeks, property is the new site of financial and economic instability.

Unfortunately for many property companies, there is little they can do about the situation. Balance sheet management has improved vastly in recent years, and property funds have made themselves much more resilient. But with the tide turning against them, some will probably fail – barring a shock turnaround in the underlying trends. However, improved balance sheets mean many of the larger players -particularly those unrelated to danger areas like inner city office space – will be able to weather the storm. When they come out the other side, they will find a significantly cheaper market ripe for plundering.

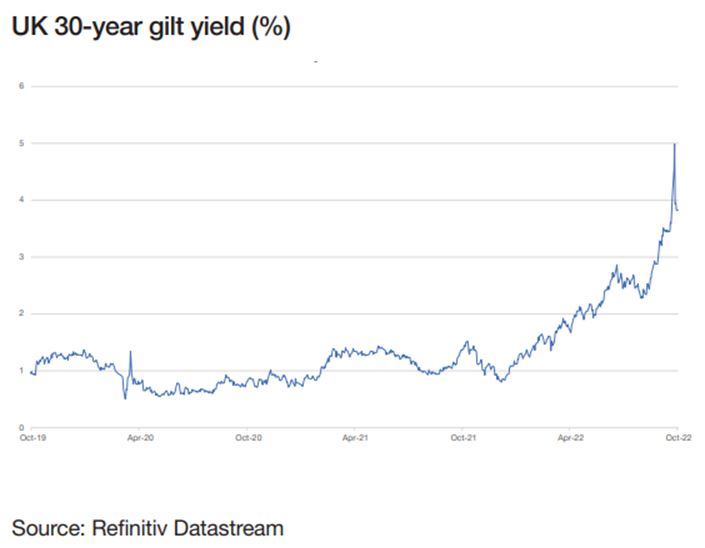

Headaches all round after the UK’s Gilt trip

The BoE’s emergency intervention three weeks ago was vital in stopping the gilt market bleed. But last week, Governor Andrew Bailey was keen to remind everyone that what the Old Lady giveth, she can taketh away. He responded to extension requests on the BoE’s bond-buying programme by firmly telling UK pension funds “you’ve got three days left”. Before giving way to optimism over the UK government’s latest U-turn, fear spread that pension funds would once again come under extreme pressure, with volatility pushing up collateral demands and making them forced sellers once more. The downturn was not limited to the UK either: US stocks fell sharply with investors concerned about global financial contagion. Bailey’s deadline was treated as an “all-time central bank gaffe” in some quarters, and sterling dropped hard and fast immediately after his comments.

But the BoE chief is in an unenviable position. His team is tasked with taming runaway inflation while avoiding a financial crisis triggered by government action that markets deemed fiscally profligate and irresponsible. In the current environment, these goals pull in opposite directions. Exceptionally high inflation requires exceptional monetary tightening, while the threat of pension fund collapse requires liquidity injections. Setting a timeline on these injections threatens to create a cliff-edge scenario, but open-ended purchases would undermine any monetary tightening done elsewhere. The BoE line was always that bond purchases were an emergency provision and would be dialled down when the immediate threat was gone.

We have grown used to near or below-zero real yields in the last decade and a half. But with the world in a sharp supply shortage (now mainly labour and fossil fuels), it is reasonable to think yields must move higher over the long-term to re-establish the balance between supply and demand. Currently, RPI-linked ten-year gilts yield 0.75% (above retail inflation). Runaway inflation necessitates some compression of activity from the BoE, meaning these real yield levels look justified. In fact, these yields arguably look attractive to global investors. That might seem bizarre, given BoE intervention seems to be the only thing keeping gilt markets intact. But the sharp sell-off had more to do with pension fund ‘fire sales’ because of a structural weak link in UK pension regulation, rather than underlying fundamentals.

The recent mayhem has caused many commentators to liken the UK to an emerging market, with fiscal imprudence and policy divergence from its central bank. But Britain is not an emerging market – it has highly functional financial and corporate structures and a highly skilled workforce. Recent bond movements bely this, but arguably suggests there are now bargains to be had. This is not to say we expect a sharp rebound (and thereby fall back in yields) – there are far too many intractable short-term problems for that – but there could be healthy returns in the future and, for the time being, yield-based return contributions we have not seen in over a decade.

Please continue to check our Blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.

David Purcell

17th October 2022