Please see today’s Daily Investment Bulletin from Brooks Macdonald received this morning:

What has happened

Markets endured another day of extreme volatility yesterday with US equities trading at one point c. -2.5% before rallying to close over 2.5% higher on the day. The cause of the volatility was of course the CPI print although it is difficult to decipher what catalysed the late market rally other than perhaps a feeling that the CPI beat ‘could have been worse’.

UK

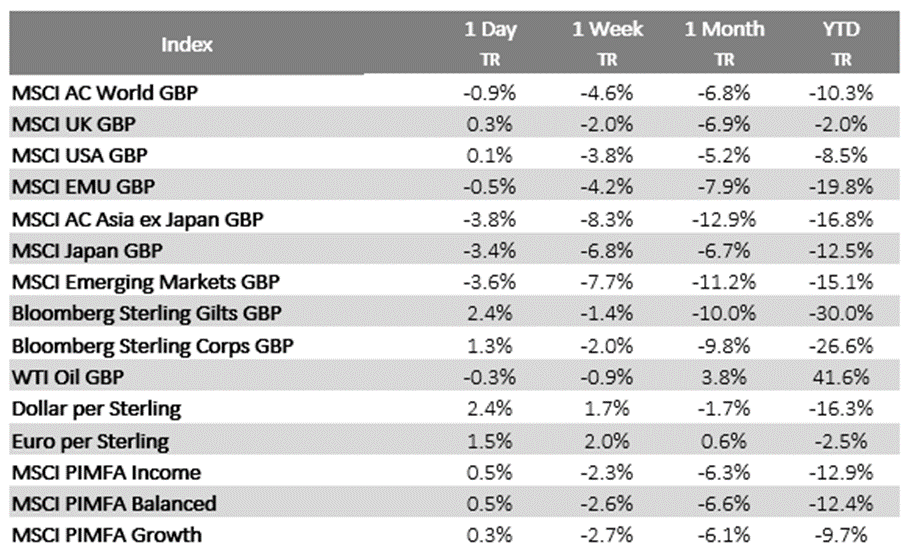

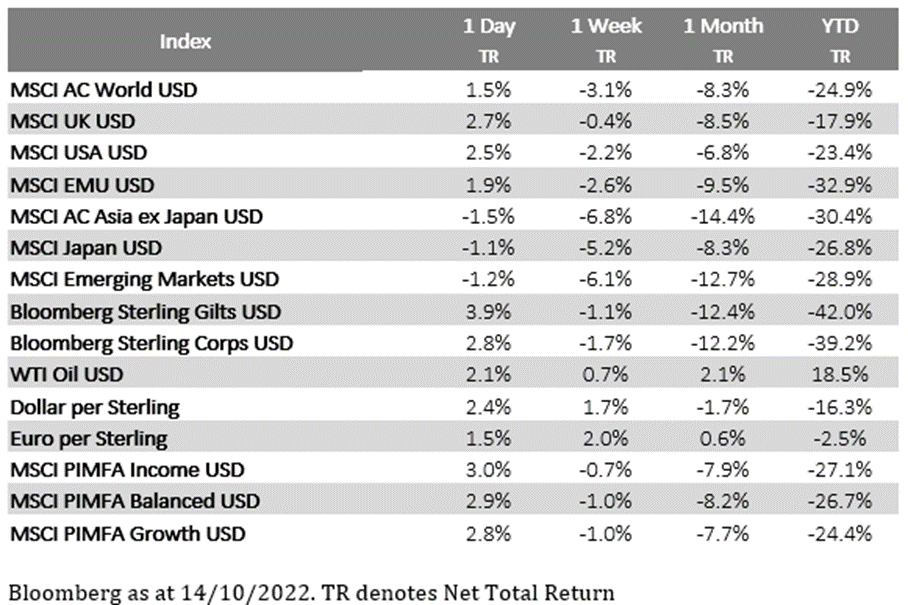

While the attention was firmly on the US yesterday, UK assets rallied yesterday on speculation that the Truss government could reverse some of the unfunded tax cuts announced in the ‘mini-budget.’ Sterling was a particular beneficiary of reports suggesting a U-turn on corporation tax rates may be on the cards. Adding further weight to speculation was the premature exit of Chancellor Kwarteng from the IMF conference in Washington, with sources suggesting he was returning to the UK to brief MPs on proposed changes. Yesterday saw sterling rally by over 2% against the US dollar, the largest gain since March of 2020. Gilt yields also fell as bond markets priced in reduced gilt supply from a less expansionary set of fiscal policies.

US CPI Report

There was little good news for the markets within the US CPI report with headline CPI coming in above expectations, at 0.4% month-on-month. Whilst the year-on-year measure ticked down, it fell by less than the market had hoped, now standing at 8.2%. Core CPI, the more important measure to gauge the transmission of inflation throughout the economy, rose by 0.6% month-on-month compared to expectations of 0.4%. In terms of the drivers of the inflationary pressure, these were broad-based, suggesting that the Federal Reserve will be emboldened to continue their rate hiking cycle apace. Markets have fully priced in a 75bp rate hike in November and have ratcheted up the probability of a further 75bp move in December of this year. With this repricing, Treasury yields rose yesterday, and equity markets sold off sharply before climbing into the end of the day.

What does Brooks Macdonald think

There has been much speculation over the cause of the late rally in US equities given the CPI report showed more inflationary pressures than the market had expected. With equity positioning being at extremely bearish levels coming into the data release, the simplest explanation may be that many in the market had a sense of relief that headline year-on-year continues to fall, even if it continues to remain stickier than economists had hoped.

Please continue to check our Blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.

Carl Mitchell – Dip PFS

14/10/2022